Deck 12: Estimating the Cost of Capital

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Use the table for the question(s) below.

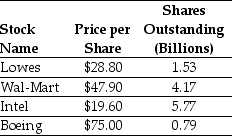

Consider the following stock price and shares outstanding data:

Which of the following is NOT an assumption used in deriving the Capital Asset Pricing Model (CAPM)?

A) Investors have homogeneous expectations regarding the volatilities, correlation, and expected returns of securities.

B) Investors have homogeneous risk adverse preferences toward taking on risk.

C) Investors hold only efficient portfolios of traded securities; that is, portfolios that yield the maximum expected return for the given level of volatility.

D) Investors can buy and sell all securities at competitive market prices without incurring taxes or transactions costs and can borrow and lend at the risk-free interest rate.

Consider the following stock price and shares outstanding data:

Which of the following is NOT an assumption used in deriving the Capital Asset Pricing Model (CAPM)?

A) Investors have homogeneous expectations regarding the volatilities, correlation, and expected returns of securities.

B) Investors have homogeneous risk adverse preferences toward taking on risk.

C) Investors hold only efficient portfolios of traded securities; that is, portfolios that yield the maximum expected return for the given level of volatility.

D) Investors can buy and sell all securities at competitive market prices without incurring taxes or transactions costs and can borrow and lend at the risk-free interest rate.

Question

Use the table for the question(s) below.

Consider the following stock price and shares outstanding data:

Assume that you have $100,000 to invest and you are interested in creating a value-weighted portfolio of these four stocks.The number of shares of Wal-Mart that you would hold in your portfolio is closest to:

A) 710

B) 1390

C) 1000

D) 870

Consider the following stock price and shares outstanding data:

Assume that you have $100,000 to invest and you are interested in creating a value-weighted portfolio of these four stocks.The number of shares of Wal-Mart that you would hold in your portfolio is closest to:

A) 710

B) 1390

C) 1000

D) 870

Question

Use the table for the question(s) below.

Consider the following stock price and shares outstanding data:

Which of the following statements is false?

A) If investors have homogeneous expectations, then each investor will identify the same portfolio as having the highest Sharpe ratio in the economy.

B) Homogeneous expectations are when all investors have the same estimates concerning future investments and returns.

C) There are many investors in the world, and each must have identical estimates of the volatilities, correlations, and expected returns of the available securities.

D) The combined portfolio of risky securities of all investors must equal the efficient portfolio.

Consider the following stock price and shares outstanding data:

Which of the following statements is false?

A) If investors have homogeneous expectations, then each investor will identify the same portfolio as having the highest Sharpe ratio in the economy.

B) Homogeneous expectations are when all investors have the same estimates concerning future investments and returns.

C) There are many investors in the world, and each must have identical estimates of the volatilities, correlations, and expected returns of the available securities.

D) The combined portfolio of risky securities of all investors must equal the efficient portfolio.

Question

Use the table for the question(s) below.

Consider the following stock price and shares outstanding data:

Which of the following statements is false?

A) If some security were not part of the efficient portfolio, then every investor would want to own it, and demand for this security would increase, causing its expected return to fall until it was no longer an attractive investment.

B) The efficient portfolio, the portfolio that all investors should hold, must be the same portfolio as the market portfolio of all risky securities.

C) Because every security is owned by someone, the sum of all investors' portfolios must equal the portfolio of all risky securities available in the market.

D) If all investors demand the efficient portfolio, and since the supply of securities is the market portfolio, then the two portfolios must coincide.

Consider the following stock price and shares outstanding data:

Which of the following statements is false?

A) If some security were not part of the efficient portfolio, then every investor would want to own it, and demand for this security would increase, causing its expected return to fall until it was no longer an attractive investment.

B) The efficient portfolio, the portfolio that all investors should hold, must be the same portfolio as the market portfolio of all risky securities.

C) Because every security is owned by someone, the sum of all investors' portfolios must equal the portfolio of all risky securities available in the market.

D) If all investors demand the efficient portfolio, and since the supply of securities is the market portfolio, then the two portfolios must coincide.

Question

Question

Use the table for the question(s) below.

Consider the following stock price and shares outstanding data:

The total market capitalization for all four stocks is closest to:

A) $479 billion

B) $415 billion

C) $2,100 billion

D) $200 billion

Consider the following stock price and shares outstanding data:

The total market capitalization for all four stocks is closest to:

A) $479 billion

B) $415 billion

C) $2,100 billion

D) $200 billion

Question

Use the table for the question(s) below.

Consider the following stock price and shares outstanding data:

The capital market line (CML)represents the highest expected return available for ________ level of volatility.

A) any

B) a zero

C) a high

D) a low

Consider the following stock price and shares outstanding data:

The capital market line (CML)represents the highest expected return available for ________ level of volatility.

A) any

B) a zero

C) a high

D) a low

Question

Use the table for the question(s) below.

Consider the following stock price and shares outstanding data:

Assume that you have $250,000 to invest and you are interested in creating a value-weighted portfolio of these four stocks.How many shares of each of the four stocks will you hold? What percentage of the shares outstanding of each stock will you hold?

Consider the following stock price and shares outstanding data:

Assume that you have $250,000 to invest and you are interested in creating a value-weighted portfolio of these four stocks.How many shares of each of the four stocks will you hold? What percentage of the shares outstanding of each stock will you hold?

Question

Question

Question

Use the table for the question(s) below.

Consider the following stock price and shares outstanding data:

Which of the following equations is incorrect?

A) E[RxCML] = rf + x(E[RMkt] + rf)

B) ri = rf + b(E[RMkt] - rf)

C) SD(RxCML)= xSD(RMkt)

D) E[RxCML] = (1 - x)rf + xE[RMkt]

Consider the following stock price and shares outstanding data:

Which of the following equations is incorrect?

A) E[RxCML] = rf + x(E[RMkt] + rf)

B) ri = rf + b(E[RMkt] - rf)

C) SD(RxCML)= xSD(RMkt)

D) E[RxCML] = (1 - x)rf + xE[RMkt]

Question

Question

Question

Use the table for the question(s) below.

Consider the following stock price and shares outstanding data:

If you are interested in creating a value-weighted portfolio of these four stocks,then the percentage amount that you would invest in Lowes is closest to:

A) 25%

B) 11%

C) 20.0%

D) 12%

Consider the following stock price and shares outstanding data:

If you are interested in creating a value-weighted portfolio of these four stocks,then the percentage amount that you would invest in Lowes is closest to:

A) 25%

B) 11%

C) 20.0%

D) 12%

Question

Use the table for the question(s) below.

Consider the following stock price and shares outstanding data:

Which of the following statements is false?

A) Because all investors should hold the risky securities in the same proportions as the efficient portfolio, their combined portfolio will also reflect the same proportions as the efficient portfolio.

B) When the CAPM assumptions hold, choosing an optimal portfolio is relatively straightforward: it is the combination of the risk-free investment and the market portfolio.

C) Graphically, when the tangent line goes through the market portfolio, it is called the security market line (SML).

D) A portfolio's risk premium and volatility are determined by the fraction that is invested in the market.

Consider the following stock price and shares outstanding data:

Which of the following statements is false?

A) Because all investors should hold the risky securities in the same proportions as the efficient portfolio, their combined portfolio will also reflect the same proportions as the efficient portfolio.

B) When the CAPM assumptions hold, choosing an optimal portfolio is relatively straightforward: it is the combination of the risk-free investment and the market portfolio.

C) Graphically, when the tangent line goes through the market portfolio, it is called the security market line (SML).

D) A portfolio's risk premium and volatility are determined by the fraction that is invested in the market.

Question

Use the table for the question(s) below.

Consider the following stock price and shares outstanding data:

Assume that you have $100,000 to invest and you are interested in creating a value-weighted portfolio of these four stocks.The percentage of the shares outstanding of Boeing that you would hold in your portfolio is closest to:

A) .000018%

B) .000020%

C) .000024%

D) .000031%

Consider the following stock price and shares outstanding data:

Assume that you have $100,000 to invest and you are interested in creating a value-weighted portfolio of these four stocks.The percentage of the shares outstanding of Boeing that you would hold in your portfolio is closest to:

A) .000018%

B) .000020%

C) .000024%

D) .000031%

Question

Question

Use the table for the question(s) below.

Consider the following stock price and shares outstanding data:

The market capitalization for Wal-Mart is closest to:

A) $415 billion

B) $276 billion

C) $479 billion

D) $200 billion

Consider the following stock price and shares outstanding data:

The market capitalization for Wal-Mart is closest to:

A) $415 billion

B) $276 billion

C) $479 billion

D) $200 billion

Question

Question

Question

Question

Question

Question

Question

Question

Use the table for the question(s) below.

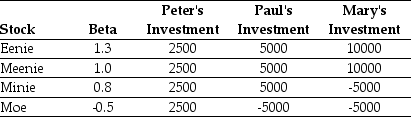

Consider the following three individuals' portfolios consisting of investments in four stocks:

The beta on Paul's portfolio is closest to:

A) 1.5

B) 1.8

C) 1.3

D) 1.0

Consider the following three individuals' portfolios consisting of investments in four stocks:

The beta on Paul's portfolio is closest to:

A) 1.5

B) 1.8

C) 1.3

D) 1.0

Question

Question

Question

Question

Question

Question

Use the table for the question(s) below.

Consider the following three individuals' portfolios consisting of investments in four stocks:

The beta on Peter's portfolio is closest to:

A) 0.7

B) 0.8

C) 1.8

D) 1.0

Consider the following three individuals' portfolios consisting of investments in four stocks:

The beta on Peter's portfolio is closest to:

A) 0.7

B) 0.8

C) 1.8

D) 1.0

Question

Question

Question

Question

Use the table for the question(s) below.

Consider the following three individuals' portfolios consisting of investments in four stocks:

Assuming that the risk-free rate is 4% and the expected return on the market is 12%,then calculate the required return on Mary's portfolio.

Consider the following three individuals' portfolios consisting of investments in four stocks:

Assuming that the risk-free rate is 4% and the expected return on the market is 12%,then calculate the required return on Mary's portfolio.

Question

Use the table for the question(s) below.

Consider the following three individuals' portfolios consisting of investments in four stocks:

Assuming that the risk-free rate is 4% and the expected return on the market is 12%,then required return on Paul's portfolio is closest to:

A) 20%

B) 22%

C) 18%

D) 16%

Consider the following three individuals' portfolios consisting of investments in four stocks:

Assuming that the risk-free rate is 4% and the expected return on the market is 12%,then required return on Paul's portfolio is closest to:

A) 20%

B) 22%

C) 18%

D) 16%

Question

Question

Use the table for the question(s) below.

Consider the following three individuals' portfolios consisting of investments in four stocks:

Assuming that the risk-free rate is 4% and the expected return on the market is 12%,then required return on Peter's portfolio is closest to:

A) 10%

B) 12%

C) 9%

D) 8%

Consider the following three individuals' portfolios consisting of investments in four stocks:

Assuming that the risk-free rate is 4% and the expected return on the market is 12%,then required return on Peter's portfolio is closest to:

A) 10%

B) 12%

C) 9%

D) 8%

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Use the table for the question(s) below.

Consider the following three individuals' portfolios consisting of investments in four stocks:

Explain how having different interest rates for borrowing and lending affects the CAPM and the SML.

Consider the following three individuals' portfolios consisting of investments in four stocks:

Explain how having different interest rates for borrowing and lending affects the CAPM and the SML.

Question

Question

Question

Question

Use the table for the question(s) below.

Consider the following three individuals' portfolios consisting of investments in four stocks:

Suppose that the risk-free rate is 5% and the market portfolio has an expected return of 13% with a volatility of 18%.Luther Industries has a volatility of 24% and a correlation with the market of .5.If you assume that the CAPM assumptions hold,then what is the expected return on Luther stock?

Consider the following three individuals' portfolios consisting of investments in four stocks:

Suppose that the risk-free rate is 5% and the market portfolio has an expected return of 13% with a volatility of 18%.Luther Industries has a volatility of 24% and a correlation with the market of .5.If you assume that the CAPM assumptions hold,then what is the expected return on Luther stock?

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/108

Play

Full screen (f)

Deck 12: Estimating the Cost of Capital

1

Which of the following statements is false?

A) A combination of portfolios on the efficient frontier of risky investments is also on the efficient frontier of risky investments.

B) The conclusion of the CAPM that investors should hold the market portfolio combined with the risk-free investment depends on the quality of an investor's information.

C) The SML holds with some rate r* between rs and rb in place of rf, where r* depends on the proportion of savers and borrowers in the economy.

D) In reality, investors have different information and spend varying amounts of effort on research for assorted stocks.

A) A combination of portfolios on the efficient frontier of risky investments is also on the efficient frontier of risky investments.

B) The conclusion of the CAPM that investors should hold the market portfolio combined with the risk-free investment depends on the quality of an investor's information.

C) The SML holds with some rate r* between rs and rb in place of rf, where r* depends on the proportion of savers and borrowers in the economy.

D) In reality, investors have different information and spend varying amounts of effort on research for assorted stocks.

The conclusion of the CAPM that investors should hold the market portfolio combined with the risk-free investment depends on the quality of an investor's information.

2

Which of the following statements is false?

A) The S&P 500 and the Wilshire 5000 indexes are both well-diversified indexes that roughly correspond to the market of Canadian stocks.

B) Practitioners commonly use the S&P 500 as the market portfolio in the CAPM with the belief that this index is the market portfolio.

C) Standard & Poor's Depository Receipts (SPDR, nicknamed "spider") trade on the American Stock Exchange and represent ownership in the S&P 500.

D) The S&P 500 was the first widely publicized value-weighted index and it has become a benchmark for professional investors.

A) The S&P 500 and the Wilshire 5000 indexes are both well-diversified indexes that roughly correspond to the market of Canadian stocks.

B) Practitioners commonly use the S&P 500 as the market portfolio in the CAPM with the belief that this index is the market portfolio.

C) Standard & Poor's Depository Receipts (SPDR, nicknamed "spider") trade on the American Stock Exchange and represent ownership in the S&P 500.

D) The S&P 500 was the first widely publicized value-weighted index and it has become a benchmark for professional investors.

Practitioners commonly use the S&P 500 as the market portfolio in the CAPM with the belief that this index is the market portfolio.

3

Which of the following statements is false?

A) The most familiar stock index in the United States is the Dow Jones Industrial Average (DJIA).

B) A portfolio in which each security is held in proportion to its market capitalization is called a price-weighted portfolio.

C) The Dow Jones Industrial Average (DJIA) consists of a portfolio of 30 large industrial stocks.

D) The Dow Jones Industrial Average (DJIA) is a price-weighted portfolio.

A) The most familiar stock index in the United States is the Dow Jones Industrial Average (DJIA).

B) A portfolio in which each security is held in proportion to its market capitalization is called a price-weighted portfolio.

C) The Dow Jones Industrial Average (DJIA) consists of a portfolio of 30 large industrial stocks.

D) The Dow Jones Industrial Average (DJIA) is a price-weighted portfolio.

A portfolio in which each security is held in proportion to its market capitalization is called a price-weighted portfolio.

4

Under the CAPM,the market portfolio is a well diversified,efficient portfolio representing ________ in the economy.

A) the diversified risk

B) the systematic risk

C) the market risk

D) the non-diversified risk

A) the diversified risk

B) the systematic risk

C) the market risk

D) the non-diversified risk

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

5

Which of the following statements is false?

A) Because of the higher and uncompensated risk involved, no investor should choose a portfolio with a negative alpha.

B) Because the average portfolio of all investors is the market portfolio, the average alpha for all investors is zero.

C) The market portfolio can be inefficient if a significant number of investors misinterpret information and believe they are earning a positive alpha when they are actually earning a negative alpha.

D) If no investor earns a positive alpha, then no investor can earn a negative alpha, and the market portfolio must be efficient.

A) Because of the higher and uncompensated risk involved, no investor should choose a portfolio with a negative alpha.

B) Because the average portfolio of all investors is the market portfolio, the average alpha for all investors is zero.

C) The market portfolio can be inefficient if a significant number of investors misinterpret information and believe they are earning a positive alpha when they are actually earning a negative alpha.

D) If no investor earns a positive alpha, then no investor can earn a negative alpha, and the market portfolio must be efficient.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

6

It is ________ that determines the cost of capital.

A) diversifiable risk

B) non-systematic risk

C) market risk

D) total risk

A) diversifiable risk

B) non-systematic risk

C) market risk

D) total risk

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

7

The Canadian S&P/TSX Composite Index is a ________ stock index.

A) price weighted

B) return weighted

C) risk weighted

D) value weighted

A) price weighted

B) return weighted

C) risk weighted

D) value weighted

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

8

Which of the following statements is false?

A) Because very little trading is required to maintain it, an equal-weighted portfolio is called a passive portfolio.

B) If the number of shares in a value-weighted portfolio does not change, but only the prices change, the portfolio will remain value-weighted.

C) The CAPM says that individual investors should hold the market portfolio, a value-weighted portfolio of all risky securities in the market.

D) A price-weighted portfolio holds an equal number of shares of each stock, independent of their size.

A) Because very little trading is required to maintain it, an equal-weighted portfolio is called a passive portfolio.

B) If the number of shares in a value-weighted portfolio does not change, but only the prices change, the portfolio will remain value-weighted.

C) The CAPM says that individual investors should hold the market portfolio, a value-weighted portfolio of all risky securities in the market.

D) A price-weighted portfolio holds an equal number of shares of each stock, independent of their size.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

9

Which of the following statements is false?

A) When an investor chooses her optimal portfolio, she will do so by finding the tangent line using the risk-free rate that corresponds to her investment horizon.

B) If the market portfolio is not efficient, savvy investors who recognize that the market portfolio is not optimal will push prices and expected returns back into balance.

C) Even though different investors may research different stocks, their information will not impact the market portfolio since there is no way to share this information with other investors.

D) In the real world borrowers pay higher interest rates than savers receive.

A) When an investor chooses her optimal portfolio, she will do so by finding the tangent line using the risk-free rate that corresponds to her investment horizon.

B) If the market portfolio is not efficient, savvy investors who recognize that the market portfolio is not optimal will push prices and expected returns back into balance.

C) Even though different investors may research different stocks, their information will not impact the market portfolio since there is no way to share this information with other investors.

D) In the real world borrowers pay higher interest rates than savers receive.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

10

Which of the following statements is false?

A) A market index reports the value of a particular portfolio of securities.

B) The S&P 500 is the standard portfolio used to represent "the market" when using the CAPM in practice.

C) Even though the S&P 500 includes only 500 of the more than 7,000 individual Canadian stocks in existence, it represents more than 70% of the Canadian stock market in terms of market capitalization.

D) The S&P 500 is an equal-weighted portfolio of 500 of the largest Canadian stocks.

A) A market index reports the value of a particular portfolio of securities.

B) The S&P 500 is the standard portfolio used to represent "the market" when using the CAPM in practice.

C) Even though the S&P 500 includes only 500 of the more than 7,000 individual Canadian stocks in existence, it represents more than 70% of the Canadian stock market in terms of market capitalization.

D) The S&P 500 is an equal-weighted portfolio of 500 of the largest Canadian stocks.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

11

Which of the following statements is false?

A) All investors should demand the same efficient portfolio of securities in the same proportions.

B) The Capital Asset Pricing Model (CAPM) allows corporate executives to identify the efficient portfolio (of risky assets) by using knowledge of the expected return of each security.

C) If investors hold the efficient portfolio, then the cost of capital for any investment project is equal to its required return calculated using its beta with the efficient portfolio.

D) The CAPM identifies the market portfolio as the efficient portfolio.

A) All investors should demand the same efficient portfolio of securities in the same proportions.

B) The Capital Asset Pricing Model (CAPM) allows corporate executives to identify the efficient portfolio (of risky assets) by using knowledge of the expected return of each security.

C) If investors hold the efficient portfolio, then the cost of capital for any investment project is equal to its required return calculated using its beta with the efficient portfolio.

D) The CAPM identifies the market portfolio as the efficient portfolio.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

12

Which of the following statements is false?

A) The market capitalization is the total market value of its outstanding shares.

B) The market portfolio is the portfolio of all risky investments.

C) Many practitioners believe it insensible to use the CAPM and the security market line as a practical means to estimate a stock's required return and therefore a firm's equity cost of capital.

D) To estimate the equity cost of capital using the CAPM, the first thing we need to do is identify the market portfolio.

A) The market capitalization is the total market value of its outstanding shares.

B) The market portfolio is the portfolio of all risky investments.

C) Many practitioners believe it insensible to use the CAPM and the security market line as a practical means to estimate a stock's required return and therefore a firm's equity cost of capital.

D) To estimate the equity cost of capital using the CAPM, the first thing we need to do is identify the market portfolio.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

13

The cost of capital is the best expected return available in the market on investments with ________ risk.

A) similar

B) bigger

C) smaller

D) different

A) similar

B) bigger

C) smaller

D) different

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

14

Which of the following statements is false?

A) Investors may have different information regarding expected returns, correlations, and volatilities, but they correctly interpret that information and the information contained in market prices and they adjust their estimates of expected returns in a rational way.

B) Investors may learn different information through their own research and observations, but as long as they understand the differences in information and learn from other investors by observing prices, the CAPM conclusions still stand.

C) Every investor, regardless of how much information he has access to, can guarantee himself an alpha of zero by holding the market portfolio.

D) The CAPM requires making the strong assumptions of homogeneous expectations.

A) Investors may have different information regarding expected returns, correlations, and volatilities, but they correctly interpret that information and the information contained in market prices and they adjust their estimates of expected returns in a rational way.

B) Investors may learn different information through their own research and observations, but as long as they understand the differences in information and learn from other investors by observing prices, the CAPM conclusions still stand.

C) Every investor, regardless of how much information he has access to, can guarantee himself an alpha of zero by holding the market portfolio.

D) The CAPM requires making the strong assumptions of homogeneous expectations.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

15

Which of the following statements is false?

A) The market portfolio contains more of the smallest stocks and less of the larger stocks.

B) For the market portfolio, the investment in each security is proportional to its market capitalization.

C) Because the market portfolio is defined as the total supply of securities, the proportions should correspond exactly to the proportion of the total market that each security represents.

D) Market capitalization is the total market value of the outstanding shares of a firm.

A) The market portfolio contains more of the smallest stocks and less of the larger stocks.

B) For the market portfolio, the investment in each security is proportional to its market capitalization.

C) Because the market portfolio is defined as the total supply of securities, the proportions should correspond exactly to the proportion of the total market that each security represents.

D) Market capitalization is the total market value of the outstanding shares of a firm.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

16

The cost of capital of any investment opportunity equals ________ of available investments with the same beta.

A) the realized return

B) the expected return

C) the level of systematic risk

D) the volatility of return

A) the realized return

B) the expected return

C) the level of systematic risk

D) the volatility of return

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following statements is false?

A) A value-weighted portfolio is an equal-ownership portfolio: we hold an equal fraction of the total number of shares outstanding of each security in the portfolio.

B) When buying a value-weighted portfolio, we end up purchasing the same percentage of shares of each firm.

C) To maintain a value-weighted portfolio, we do not need to trade securities and rebalance the portfolio unless the number of shares outstanding of some security changes.

D) In a value-weighted portfolio the fraction of money invested in any security corresponds to its share of the total number of shares outstanding of all securities in the portfolio.

A) A value-weighted portfolio is an equal-ownership portfolio: we hold an equal fraction of the total number of shares outstanding of each security in the portfolio.

B) When buying a value-weighted portfolio, we end up purchasing the same percentage of shares of each firm.

C) To maintain a value-weighted portfolio, we do not need to trade securities and rebalance the portfolio unless the number of shares outstanding of some security changes.

D) In a value-weighted portfolio the fraction of money invested in any security corresponds to its share of the total number of shares outstanding of all securities in the portfolio.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

18

Which of the following statements is false?

A) Short-term margin loans from a broker are often 1% to 2% lower than the rates paid on short-term Treasury securities.

B) In the real world investors have different information and expectations regarding securities.

C) The SML is still valid when interest rates differ.

D) When borrowing and lending occur at different rates there are different tangent portfolios identified.

A) Short-term margin loans from a broker are often 1% to 2% lower than the rates paid on short-term Treasury securities.

B) In the real world investors have different information and expectations regarding securities.

C) The SML is still valid when interest rates differ.

D) When borrowing and lending occur at different rates there are different tangent portfolios identified.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

19

The only way it can be possible to earn a positive alpha and beat the market is if some investors are holding portfolios with ________ alphas.

A) positive

B) zero

C) negative

D) none of the above

A) positive

B) zero

C) negative

D) none of the above

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

20

Which of the following statements is false?

A) There are two indexes that try to represent the performance of the Canadian stock market.

B) A market index reports the price of a particular portfolio of securities that make up the index.

C) Since 2002, Standard & Poor's Corporation of New York has managed the S&P/TSX Composite Index.

D) The S&P/TSX Composite Index is a popular portfolio used to represent the market index when applying the CAPM to Canadian stocks, as it represents about 95% of Canada's equity market capitalization.

A) There are two indexes that try to represent the performance of the Canadian stock market.

B) A market index reports the price of a particular portfolio of securities that make up the index.

C) Since 2002, Standard & Poor's Corporation of New York has managed the S&P/TSX Composite Index.

D) The S&P/TSX Composite Index is a popular portfolio used to represent the market index when applying the CAPM to Canadian stocks, as it represents about 95% of Canada's equity market capitalization.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

21

In practice which market index would best be used as a proxy for the market portfolio in the CAPM?

A) S&P 500

B) Dow Jones Industrial Average

C) Canadian Treasury Bill

D) Wilshire 5000

A) S&P 500

B) Dow Jones Industrial Average

C) Canadian Treasury Bill

D) Wilshire 5000

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

22

Use the table for the question(s) below.

Consider the following stock price and shares outstanding data:

Which of the following is NOT an assumption used in deriving the Capital Asset Pricing Model (CAPM)?

A) Investors have homogeneous expectations regarding the volatilities, correlation, and expected returns of securities.

B) Investors have homogeneous risk adverse preferences toward taking on risk.

C) Investors hold only efficient portfolios of traded securities; that is, portfolios that yield the maximum expected return for the given level of volatility.

D) Investors can buy and sell all securities at competitive market prices without incurring taxes or transactions costs and can borrow and lend at the risk-free interest rate.

Consider the following stock price and shares outstanding data:

Which of the following is NOT an assumption used in deriving the Capital Asset Pricing Model (CAPM)?

A) Investors have homogeneous expectations regarding the volatilities, correlation, and expected returns of securities.

B) Investors have homogeneous risk adverse preferences toward taking on risk.

C) Investors hold only efficient portfolios of traded securities; that is, portfolios that yield the maximum expected return for the given level of volatility.

D) Investors can buy and sell all securities at competitive market prices without incurring taxes or transactions costs and can borrow and lend at the risk-free interest rate.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

23

Use the table for the question(s) below.

Consider the following stock price and shares outstanding data:

Assume that you have $100,000 to invest and you are interested in creating a value-weighted portfolio of these four stocks.The number of shares of Wal-Mart that you would hold in your portfolio is closest to:

A) 710

B) 1390

C) 1000

D) 870

Consider the following stock price and shares outstanding data:

Assume that you have $100,000 to invest and you are interested in creating a value-weighted portfolio of these four stocks.The number of shares of Wal-Mart that you would hold in your portfolio is closest to:

A) 710

B) 1390

C) 1000

D) 870

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

24

Use the table for the question(s) below.

Consider the following stock price and shares outstanding data:

Which of the following statements is false?

A) If investors have homogeneous expectations, then each investor will identify the same portfolio as having the highest Sharpe ratio in the economy.

B) Homogeneous expectations are when all investors have the same estimates concerning future investments and returns.

C) There are many investors in the world, and each must have identical estimates of the volatilities, correlations, and expected returns of the available securities.

D) The combined portfolio of risky securities of all investors must equal the efficient portfolio.

Consider the following stock price and shares outstanding data:

Which of the following statements is false?

A) If investors have homogeneous expectations, then each investor will identify the same portfolio as having the highest Sharpe ratio in the economy.

B) Homogeneous expectations are when all investors have the same estimates concerning future investments and returns.

C) There are many investors in the world, and each must have identical estimates of the volatilities, correlations, and expected returns of the available securities.

D) The combined portfolio of risky securities of all investors must equal the efficient portfolio.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

25

Use the table for the question(s) below.

Consider the following stock price and shares outstanding data:

Which of the following statements is false?

A) If some security were not part of the efficient portfolio, then every investor would want to own it, and demand for this security would increase, causing its expected return to fall until it was no longer an attractive investment.

B) The efficient portfolio, the portfolio that all investors should hold, must be the same portfolio as the market portfolio of all risky securities.

C) Because every security is owned by someone, the sum of all investors' portfolios must equal the portfolio of all risky securities available in the market.

D) If all investors demand the efficient portfolio, and since the supply of securities is the market portfolio, then the two portfolios must coincide.

Consider the following stock price and shares outstanding data:

Which of the following statements is false?

A) If some security were not part of the efficient portfolio, then every investor would want to own it, and demand for this security would increase, causing its expected return to fall until it was no longer an attractive investment.

B) The efficient portfolio, the portfolio that all investors should hold, must be the same portfolio as the market portfolio of all risky securities.

C) Because every security is owned by someone, the sum of all investors' portfolios must equal the portfolio of all risky securities available in the market.

D) If all investors demand the efficient portfolio, and since the supply of securities is the market portfolio, then the two portfolios must coincide.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

26

Use the information for the question(s) below.

Tom's portfolio consists solely of an investment in Merck stock. Merck has an expected return of 13% and a volatility of 25%. The market portfolio has an expected return of 12% and a volatility of 18%. The risk-free rate is 4%. Assume that the CAPM assumptions hold in the market.

You currently own $100,000 worth of Wal-Mart stock.Suppose that Wal-Mart has an expected return of 14% and a volatility of 23%.The market portfolio has an expected return of 12% and a volatility of 16%.The risk-free rate is 5%.Assuming the CAPM assumptions hold,what alternative investment has the highest possible expected return while having the same volatility as Wal-Mart? What is the expected return of this portfolio?

Tom's portfolio consists solely of an investment in Merck stock. Merck has an expected return of 13% and a volatility of 25%. The market portfolio has an expected return of 12% and a volatility of 18%. The risk-free rate is 4%. Assume that the CAPM assumptions hold in the market.

You currently own $100,000 worth of Wal-Mart stock.Suppose that Wal-Mart has an expected return of 14% and a volatility of 23%.The market portfolio has an expected return of 12% and a volatility of 16%.The risk-free rate is 5%.Assuming the CAPM assumptions hold,what alternative investment has the highest possible expected return while having the same volatility as Wal-Mart? What is the expected return of this portfolio?

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

27

Use the table for the question(s) below.

Consider the following stock price and shares outstanding data:

The total market capitalization for all four stocks is closest to:

A) $479 billion

B) $415 billion

C) $2,100 billion

D) $200 billion

Consider the following stock price and shares outstanding data:

The total market capitalization for all four stocks is closest to:

A) $479 billion

B) $415 billion

C) $2,100 billion

D) $200 billion

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

28

Use the table for the question(s) below.

Consider the following stock price and shares outstanding data:

The capital market line (CML)represents the highest expected return available for ________ level of volatility.

A) any

B) a zero

C) a high

D) a low

Consider the following stock price and shares outstanding data:

The capital market line (CML)represents the highest expected return available for ________ level of volatility.

A) any

B) a zero

C) a high

D) a low

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

29

Use the table for the question(s) below.

Consider the following stock price and shares outstanding data:

Assume that you have $250,000 to invest and you are interested in creating a value-weighted portfolio of these four stocks.How many shares of each of the four stocks will you hold? What percentage of the shares outstanding of each stock will you hold?

Consider the following stock price and shares outstanding data:

Assume that you have $250,000 to invest and you are interested in creating a value-weighted portfolio of these four stocks.How many shares of each of the four stocks will you hold? What percentage of the shares outstanding of each stock will you hold?

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

30

Use the information for the question(s) below.

Tom's portfolio consists solely of an investment in Merck stock. Merck has an expected return of 13% and a volatility of 25%. The market portfolio has an expected return of 12% and a volatility of 18%. The risk-free rate is 4%. Assume that the CAPM assumptions hold in the market.

Assuming that Tom wants to maintain the current expected return on his portfolio,then the amount that Tom should invest in the market portfolio to minimize his volatility is closest to:

A) 100%

B) 90%

C) 125%

D) 110%

Tom's portfolio consists solely of an investment in Merck stock. Merck has an expected return of 13% and a volatility of 25%. The market portfolio has an expected return of 12% and a volatility of 18%. The risk-free rate is 4%. Assume that the CAPM assumptions hold in the market.

Assuming that Tom wants to maintain the current expected return on his portfolio,then the amount that Tom should invest in the market portfolio to minimize his volatility is closest to:

A) 100%

B) 90%

C) 125%

D) 110%

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

31

Use the information for the question(s) below.

Tom's portfolio consists solely of an investment in Merck stock. Merck has an expected return of 13% and a volatility of 25%. The market portfolio has an expected return of 12% and a volatility of 18%. The risk-free rate is 4%. Assume that the CAPM assumptions hold in the market.

You currently own $100,000 worth of Wal-Mart stock.Suppose that Wal-Mart has an expected return of 14% and a volatility of 23%.The market portfolio has an expected return of 12% and a volatility of 16%.The risk-free rate is 5%.Assuming the CAPM assumptions hold,what alternative investment has the lowest possible volatility while having the same expected return as Wal-Mart? What is the volatility of this portfolio?

Tom's portfolio consists solely of an investment in Merck stock. Merck has an expected return of 13% and a volatility of 25%. The market portfolio has an expected return of 12% and a volatility of 18%. The risk-free rate is 4%. Assume that the CAPM assumptions hold in the market.

You currently own $100,000 worth of Wal-Mart stock.Suppose that Wal-Mart has an expected return of 14% and a volatility of 23%.The market portfolio has an expected return of 12% and a volatility of 16%.The risk-free rate is 5%.Assuming the CAPM assumptions hold,what alternative investment has the lowest possible volatility while having the same expected return as Wal-Mart? What is the volatility of this portfolio?

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

32

Use the table for the question(s) below.

Consider the following stock price and shares outstanding data:

Which of the following equations is incorrect?

A) E[RxCML] = rf + x(E[RMkt] + rf)

B) ri = rf + b(E[RMkt] - rf)

C) SD(RxCML)= xSD(RMkt)

D) E[RxCML] = (1 - x)rf + xE[RMkt]

Consider the following stock price and shares outstanding data:

Which of the following equations is incorrect?

A) E[RxCML] = rf + x(E[RMkt] + rf)

B) ri = rf + b(E[RMkt] - rf)

C) SD(RxCML)= xSD(RMkt)

D) E[RxCML] = (1 - x)rf + xE[RMkt]

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

33

Use the information for the question(s) below.

Tom's portfolio consists solely of an investment in Merck stock. Merck has an expected return of 13% and a volatility of 25%. The market portfolio has an expected return of 12% and a volatility of 18%. The risk-free rate is 4%. Assume that the CAPM assumptions hold in the market.

Assuming that Tom wants to maintain the current expected return on his portfolio,then the minimum volatility that Tom could achieve by investing in the market portfolio and risk-free investment is closest to:

A) 20%

B) 25%

C) 22%

D) 18%

Tom's portfolio consists solely of an investment in Merck stock. Merck has an expected return of 13% and a volatility of 25%. The market portfolio has an expected return of 12% and a volatility of 18%. The risk-free rate is 4%. Assume that the CAPM assumptions hold in the market.

Assuming that Tom wants to maintain the current expected return on his portfolio,then the minimum volatility that Tom could achieve by investing in the market portfolio and risk-free investment is closest to:

A) 20%

B) 25%

C) 22%

D) 18%

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

34

Use the information for the question(s) below.

Tom's portfolio consists solely of an investment in Merck stock. Merck has an expected return of 13% and a volatility of 25%. The market portfolio has an expected return of 12% and a volatility of 18%. The risk-free rate is 4%. Assume that the CAPM assumptions hold in the market.

Assuming that Tom wants to maintain the current volatility of his portfolio,then the amount that Tom should invest in the market portfolio to maximize his expected return is closest to:

A) 72%

B) 92%

C) 110%

D) 140%

Tom's portfolio consists solely of an investment in Merck stock. Merck has an expected return of 13% and a volatility of 25%. The market portfolio has an expected return of 12% and a volatility of 18%. The risk-free rate is 4%. Assume that the CAPM assumptions hold in the market.

Assuming that Tom wants to maintain the current volatility of his portfolio,then the amount that Tom should invest in the market portfolio to maximize his expected return is closest to:

A) 72%

B) 92%

C) 110%

D) 140%

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

35

Use the table for the question(s) below.

Consider the following stock price and shares outstanding data:

If you are interested in creating a value-weighted portfolio of these four stocks,then the percentage amount that you would invest in Lowes is closest to:

A) 25%

B) 11%

C) 20.0%

D) 12%

Consider the following stock price and shares outstanding data:

If you are interested in creating a value-weighted portfolio of these four stocks,then the percentage amount that you would invest in Lowes is closest to:

A) 25%

B) 11%

C) 20.0%

D) 12%

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

36

Use the table for the question(s) below.

Consider the following stock price and shares outstanding data:

Which of the following statements is false?

A) Because all investors should hold the risky securities in the same proportions as the efficient portfolio, their combined portfolio will also reflect the same proportions as the efficient portfolio.

B) When the CAPM assumptions hold, choosing an optimal portfolio is relatively straightforward: it is the combination of the risk-free investment and the market portfolio.

C) Graphically, when the tangent line goes through the market portfolio, it is called the security market line (SML).

D) A portfolio's risk premium and volatility are determined by the fraction that is invested in the market.

Consider the following stock price and shares outstanding data:

Which of the following statements is false?

A) Because all investors should hold the risky securities in the same proportions as the efficient portfolio, their combined portfolio will also reflect the same proportions as the efficient portfolio.

B) When the CAPM assumptions hold, choosing an optimal portfolio is relatively straightforward: it is the combination of the risk-free investment and the market portfolio.

C) Graphically, when the tangent line goes through the market portfolio, it is called the security market line (SML).

D) A portfolio's risk premium and volatility are determined by the fraction that is invested in the market.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

37

Use the table for the question(s) below.

Consider the following stock price and shares outstanding data:

Assume that you have $100,000 to invest and you are interested in creating a value-weighted portfolio of these four stocks.The percentage of the shares outstanding of Boeing that you would hold in your portfolio is closest to:

A) .000018%

B) .000020%

C) .000024%

D) .000031%

Consider the following stock price and shares outstanding data:

Assume that you have $100,000 to invest and you are interested in creating a value-weighted portfolio of these four stocks.The percentage of the shares outstanding of Boeing that you would hold in your portfolio is closest to:

A) .000018%

B) .000020%

C) .000024%

D) .000031%

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

38

In practice which market index is most widely used as a proxy for the market portfolio in the CAPM?

A) Dow Jones Industrial Average

B) Wilshire 5000

C) S&P 500

D) Canadian Treasury Bill

A) Dow Jones Industrial Average

B) Wilshire 5000

C) S&P 500

D) Canadian Treasury Bill

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

39

Use the table for the question(s) below.

Consider the following stock price and shares outstanding data:

The market capitalization for Wal-Mart is closest to:

A) $415 billion

B) $276 billion

C) $479 billion

D) $200 billion

Consider the following stock price and shares outstanding data:

The market capitalization for Wal-Mart is closest to:

A) $415 billion

B) $276 billion

C) $479 billion

D) $200 billion

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

40

Use the information for the question(s) below.

Tom's portfolio consists solely of an investment in Merck stock. Merck has an expected return of 13% and a volatility of 25%. The market portfolio has an expected return of 12% and a volatility of 18%. The risk-free rate is 4%. Assume that the CAPM assumptions hold in the market.

Assuming that Tom wants to maintain the current volatility of his portfolio,then the maximum expected return that Tom could achieve by investing in the market portfolio and risk-free investment is closest to:

A) 13%

B) 15%

C) 16%

D) 12.%

Tom's portfolio consists solely of an investment in Merck stock. Merck has an expected return of 13% and a volatility of 25%. The market portfolio has an expected return of 12% and a volatility of 18%. The risk-free rate is 4%. Assume that the CAPM assumptions hold in the market.

Assuming that Tom wants to maintain the current volatility of his portfolio,then the maximum expected return that Tom could achieve by investing in the market portfolio and risk-free investment is closest to:

A) 13%

B) 15%

C) 16%

D) 12.%

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

41

Which of the following statements is false?

A) The risk premium of a security is equal to the market risk premium (the amount by which the market's expected return exceeds the risk-free rate), divided by the amount of market risk present in the security's returns measured by its beta with the market.

B) We refer to the beta of a security with the market portfolio simply as the securities beta.

C) There is a linear relationship between a stock's beta and its expected return.

D) A security with a negative beta has a negative correlation with the market, which means that this security tends to perform well when the rest of the market is doing poorly.

A) The risk premium of a security is equal to the market risk premium (the amount by which the market's expected return exceeds the risk-free rate), divided by the amount of market risk present in the security's returns measured by its beta with the market.

B) We refer to the beta of a security with the market portfolio simply as the securities beta.

C) There is a linear relationship between a stock's beta and its expected return.

D) A security with a negative beta has a negative correlation with the market, which means that this security tends to perform well when the rest of the market is doing poorly.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

42

Which of the following statements is false?

A) The beta of a security is the ratio of its volatility due to market risk to the volatility of the market as a whole.

B) Under the CAPM assumptions, the market portfolio is efficient, so beta is the appropriate measure of risk to determine a security's risk premium.

C) Under the CAPM assumptions, we can identify the efficient portfolio: it is equal to the market portfolio.

D) We can determine the expected return for a security and the cost of capital of an investment opportunity by using the risk-free investment as a benchmark

A) The beta of a security is the ratio of its volatility due to market risk to the volatility of the market as a whole.

B) Under the CAPM assumptions, the market portfolio is efficient, so beta is the appropriate measure of risk to determine a security's risk premium.

C) Under the CAPM assumptions, we can identify the efficient portfolio: it is equal to the market portfolio.

D) We can determine the expected return for a security and the cost of capital of an investment opportunity by using the risk-free investment as a benchmark

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

43

The beta for the risk free investment is closest to:

A) 1

B) 0

C) Unable to answer this question without knowing the risk free rate.

D) Unable to answer this question without knowing the market's volatility.

A) 1

B) 0

C) Unable to answer this question without knowing the risk free rate.

D) Unable to answer this question without knowing the market's volatility.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

44

The beta for the market portfolio is closest to:

A) 1

B) 0

C) Unable to answer this question without knowing the market's expected return.

D) Unable to answer this question without knowing the market's volatility.

A) 1

B) 0

C) Unable to answer this question without knowing the market's expected return.

D) Unable to answer this question without knowing the market's volatility.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

45

Which of the following statements is false?

A) We can improve the performance of our portfolio by selling stocks with negative alphas.

B) The market portfolio is on the SML, and according to the CAPM, since all other portfolios are inefficient they will not fall on the SML.

C) The difference between a stock's expected return and its required return according to the security market line is called the stock's alpha.

D) The risk premium for any security is proportional to its beta with the market.

A) We can improve the performance of our portfolio by selling stocks with negative alphas.

B) The market portfolio is on the SML, and according to the CAPM, since all other portfolios are inefficient they will not fall on the SML.

C) The difference between a stock's expected return and its required return according to the security market line is called the stock's alpha.

D) The risk premium for any security is proportional to its beta with the market.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

46

Use the information for the question(s) below.

Suppose that the risk-free rate is 5% and the market portfolio has an expected return of 13% with a volatility of 18%. Monsters Inc. has a 24% volatility and a correlation with the market of .60, while California Gold Mining has a 32% volatility and a correlation with the market of -.7. Assume the CAPM assumptions hold.

California Gold Mining's required return is closest to:

A) -5%

B) 13%

C) 15%

D) 5%

Suppose that the risk-free rate is 5% and the market portfolio has an expected return of 13% with a volatility of 18%. Monsters Inc. has a 24% volatility and a correlation with the market of .60, while California Gold Mining has a 32% volatility and a correlation with the market of -.7. Assume the CAPM assumptions hold.

California Gold Mining's required return is closest to:

A) -5%

B) 13%

C) 15%

D) 5%

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

47

Use the table for the question(s) below.

Consider the following three individuals' portfolios consisting of investments in four stocks:

The beta on Paul's portfolio is closest to:

A) 1.5

B) 1.8

C) 1.3

D) 1.0

Consider the following three individuals' portfolios consisting of investments in four stocks:

The beta on Paul's portfolio is closest to:

A) 1.5

B) 1.8

C) 1.3

D) 1.0

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

48

Use the information for the question(s) below.

Suppose that the risk-free rate is 5% and the market portfolio has an expected return of 13% with a volatility of 18%. Monsters Inc. has a 24% volatility and a correlation with the market of .60, while California Gold Mining has a 32% volatility and a correlation with the market of -.7. Assume the CAPM assumptions hold.

Monsters' beta with the market is closest to:

A) 1.3

B) 1.0

C) 0.6

D) 0.8

Suppose that the risk-free rate is 5% and the market portfolio has an expected return of 13% with a volatility of 18%. Monsters Inc. has a 24% volatility and a correlation with the market of .60, while California Gold Mining has a 32% volatility and a correlation with the market of -.7. Assume the CAPM assumptions hold.

Monsters' beta with the market is closest to:

A) 1.3

B) 1.0

C) 0.6

D) 0.8

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

49

Use the information for the question(s) below.

Suppose that the risk-free rate is 5% and the market portfolio has an expected return of 13% with a volatility of 18%. Monsters Inc. has a 24% volatility and a correlation with the market of .60, while California Gold Mining has a 32% volatility and a correlation with the market of -.7. Assume the CAPM assumptions hold.

Suppose that Monsters' expected return is 12%.Then Monsters' alpha is closest to:

A) -2.0%

B) -1.0%

C) 1.0%

D) 0.5%

Suppose that the risk-free rate is 5% and the market portfolio has an expected return of 13% with a volatility of 18%. Monsters Inc. has a 24% volatility and a correlation with the market of .60, while California Gold Mining has a 32% volatility and a correlation with the market of -.7. Assume the CAPM assumptions hold.

Suppose that Monsters' expected return is 12%.Then Monsters' alpha is closest to:

A) -2.0%

B) -1.0%

C) 1.0%

D) 0.5%

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

50

Which of the following statements is false?

A) The expected return of a portfolio should correspond to the portfolio's beta.

B) Graphically the line through the risk-free investment and the market portfolio is called the capital market line (CML).

C) The beta of a portfolio is the weighted average beta of the securities in the portfolio.

D) By holding a negative beta security, an investor can reduce the overall market risk of his or her portfolio.

A) The expected return of a portfolio should correspond to the portfolio's beta.

B) Graphically the line through the risk-free investment and the market portfolio is called the capital market line (CML).

C) The beta of a portfolio is the weighted average beta of the securities in the portfolio.

D) By holding a negative beta security, an investor can reduce the overall market risk of his or her portfolio.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

51

Use the information for the question(s) below.

Suppose that the risk-free rate is 5% and the market portfolio has an expected return of 13% with a volatility of 18%. Monsters Inc. has a 24% volatility and a correlation with the market of .60, while California Gold Mining has a 32% volatility and a correlation with the market of -.7. Assume the CAPM assumptions hold.

Suppose that California Gold Mining's expected return is 2%.Then California Gold Mining's alpha is closest to:

A) -3%

B) -13%

C) 7%

D) -11%

Suppose that the risk-free rate is 5% and the market portfolio has an expected return of 13% with a volatility of 18%. Monsters Inc. has a 24% volatility and a correlation with the market of .60, while California Gold Mining has a 32% volatility and a correlation with the market of -.7. Assume the CAPM assumptions hold.

Suppose that California Gold Mining's expected return is 2%.Then California Gold Mining's alpha is closest to:

A) -3%

B) -13%

C) 7%

D) -11%

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

52

Use the information for the question(s) below.

Suppose that the risk-free rate is 5% and the market portfolio has an expected return of 13% with a volatility of 18%. Monsters Inc. has a 24% volatility and a correlation with the market of .60, while California Gold Mining has a 32% volatility and a correlation with the market of -.7. Assume the CAPM assumptions hold.

California Gold Mining's beta with the market is closest to:

A) 0.9

B) 1.25

C) -0.9

D) -1.25

Suppose that the risk-free rate is 5% and the market portfolio has an expected return of 13% with a volatility of 18%. Monsters Inc. has a 24% volatility and a correlation with the market of .60, while California Gold Mining has a 32% volatility and a correlation with the market of -.7. Assume the CAPM assumptions hold.

California Gold Mining's beta with the market is closest to:

A) 0.9

B) 1.25

C) -0.9

D) -1.25

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

53

Use the table for the question(s) below.

Consider the following three individuals' portfolios consisting of investments in four stocks:

The beta on Peter's portfolio is closest to:

A) 0.7

B) 0.8

C) 1.8

D) 1.0

Consider the following three individuals' portfolios consisting of investments in four stocks:

The beta on Peter's portfolio is closest to:

A) 0.7

B) 0.8

C) 1.8

D) 1.0

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

54

Which of the following statements is false?

A) The market portfolio is the efficient portfolio.

B) Many practitioners believe it is sensible to use the CAPM and the security market line as a practical means to estimate a stock's required return and therefore a firm's equity cost of capital.

C) If we plot individual securities according to their expected return and beta, the CAPM implies that they should all fall along the CML.

D) As savvy investors attempt to trade to improve their portfolios, they raise the price and lower the expected return of the positive alpha stocks, and they depress the price and raise the expected return of negative alpha stocks, until the stocks are once again on the security market line and the market portfolio is efficient.

A) The market portfolio is the efficient portfolio.

B) Many practitioners believe it is sensible to use the CAPM and the security market line as a practical means to estimate a stock's required return and therefore a firm's equity cost of capital.

C) If we plot individual securities according to their expected return and beta, the CAPM implies that they should all fall along the CML.

D) As savvy investors attempt to trade to improve their portfolios, they raise the price and lower the expected return of the positive alpha stocks, and they depress the price and raise the expected return of negative alpha stocks, until the stocks are once again on the security market line and the market portfolio is efficient.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

55

Which of the following statements is false?

A) To improve the performance of their portfolios, investors who are holding the market portfolio will compare the expected return of each security with its required return from the security market line.

B) The Sharpe ratio of a portfolio will increase if we sell stocks with positive alphas.

C) When a stock's alpha is not zero, investors can improve upon the performance of the market portfolio.

D) When the market portfolio is efficient, all stocks are on the security market line and have an alpha of zero.

A) To improve the performance of their portfolios, investors who are holding the market portfolio will compare the expected return of each security with its required return from the security market line.

B) The Sharpe ratio of a portfolio will increase if we sell stocks with positive alphas.

C) When a stock's alpha is not zero, investors can improve upon the performance of the market portfolio.

D) When the market portfolio is efficient, all stocks are on the security market line and have an alpha of zero.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

56

Use the information for the question(s) below.

Suppose that the risk-free rate is 5% and the market portfolio has an expected return of 13% with a volatility of 18%. Monsters Inc. has a 24% volatility and a correlation with the market of .60, while California Gold Mining has a 32% volatility and a correlation with the market of -.7. Assume the CAPM assumptions hold.

Monsters' required return is closest to:

A) 10.0%

B) 13.0%

C) 11.5%

D) 15.5%

Suppose that the risk-free rate is 5% and the market portfolio has an expected return of 13% with a volatility of 18%. Monsters Inc. has a 24% volatility and a correlation with the market of .60, while California Gold Mining has a 32% volatility and a correlation with the market of -.7. Assume the CAPM assumptions hold.

Monsters' required return is closest to:

A) 10.0%

B) 13.0%

C) 11.5%

D) 15.5%

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

57

Use the table for the question(s) below.

Consider the following three individuals' portfolios consisting of investments in four stocks:

Assuming that the risk-free rate is 4% and the expected return on the market is 12%,then calculate the required return on Mary's portfolio.

Consider the following three individuals' portfolios consisting of investments in four stocks:

Assuming that the risk-free rate is 4% and the expected return on the market is 12%,then calculate the required return on Mary's portfolio.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

58

Use the table for the question(s) below.

Consider the following three individuals' portfolios consisting of investments in four stocks:

Assuming that the risk-free rate is 4% and the expected return on the market is 12%,then required return on Paul's portfolio is closest to:

A) 20%

B) 22%

C) 18%

D) 16%

Consider the following three individuals' portfolios consisting of investments in four stocks:

Assuming that the risk-free rate is 4% and the expected return on the market is 12%,then required return on Paul's portfolio is closest to:

A) 20%

B) 22%

C) 18%

D) 16%

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

59

If the market portfolio is efficient,the relationship between a stock's beta and its expected return is a ________ relationship.

A) linear

B) upward sloping

C) downward sloping

D) None of the above

A) linear

B) upward sloping

C) downward sloping

D) None of the above

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

60

Use the table for the question(s) below.

Consider the following three individuals' portfolios consisting of investments in four stocks:

Assuming that the risk-free rate is 4% and the expected return on the market is 12%,then required return on Peter's portfolio is closest to:

A) 10%

B) 12%

C) 9%

D) 8%

Consider the following three individuals' portfolios consisting of investments in four stocks:

Assuming that the risk-free rate is 4% and the expected return on the market is 12%,then required return on Peter's portfolio is closest to:

A) 10%

B) 12%

C) 9%

D) 8%

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

61

The ________ cost of debt to the firm can be ________ once the tax deductibility of interest payments is considered.

A) equivalent, lower

B) equivalent, effective

C) effective, higher

D) effective, lower

A) equivalent, lower

B) equivalent, effective

C) effective, higher

D) effective, lower

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

62

If there is a significant risk that the firm will default on its obligation,however,________ of the firm's debt,which is promised return,will ________ investors' expected return.

A) the risk level, overstate

B) the yield to maturity, understate

C) the risk level, understate

D) the yield to maturity, overstate

A) the risk level, overstate

B) the yield to maturity, understate

C) the risk level, understate

D) the yield to maturity, overstate

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

63

Why does the yield to maturity of a firm's debt generally overestimate its debt cost of capital?

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

64

The yield to maturity of a bond is the ________ an investor will earn from holding the bond to maturity and receiving its promised payments.

A) IRR

B) coupon rate

C) rate of return

D) capital gain

A) IRR

B) coupon rate

C) rate of return

D) capital gain

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck