Deck 7: Consolidated Financial Statements - Ownership Patterns and Income Taxes

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

What is the amount of taxable income reported on the consolidated income tax return?

A) $720,000.

B) $625,000.

C) $621,000.

D) $665,000.

E) $655,000.

Question

Question

The accrual-based net income of Eckston Inc.is calculated to be

A) $234,000.

B) $211,000.

C) $221,000.

D) $224,000.

E) $246,000.

Question

Question

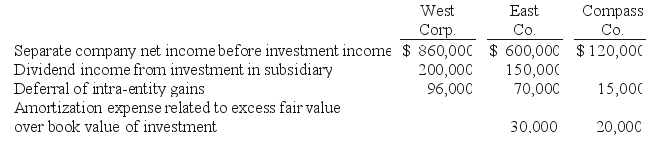

For West Corp.and consolidated subsidiaries, what total amount would be reported for the net income attributable to the noncontrolling interest?

A) $165,300.

B) $199,300.

C) $191,000.

D) $228,000.

E) $153,000.

Question

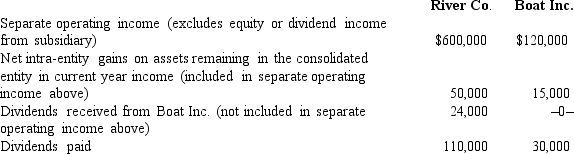

The amount of income tax expense that should be assigned to Boat using the separate return method is approximately:

A) $36,000

B) $31,500

C) $33,390

D) $32,750

E) $32,660

Question

The accrual-based net income of East Co.is calculated to be

A) $401,100.

B) $510,000.

C) $551,000.

D) $573,000.

E) $615,000.

Question

What is the amount of income tax expense that should be assigned to Boat using the percentage allocation method?

A) $31,500

B) $32,750

C) $36,000

D) $32,660

E) $30,390

Question

Question

The accrual-based net income of West Corp.is calculated to be

A) $ 734,000.

B) $1,261,000.

C) $1,123,900.

D) $1,140,700.

E) $1,149,700.

Question

Question

Question

What amount should be reported for consolidated net income?

A) $1,285,000.

B) $1,331,700.

C) $1,349,000.

D) $1,315,000.

E) $1,314,900.

Question

What was the net income attributable to the noncontrolling interest, assuming that the separate return method was used to assign the income tax expense?

A) $16,800

B) $14,450

C) $14,700

D) $17,450

E) $13,800

Question

Question

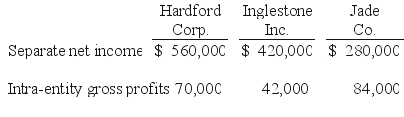

Hardford Corp. held 80% of Inglestone Inc., which, in turn, owned 80% of Jade Co. Excess amortization expense was not required by any of these acquisitions. Separate net income figures (without investment income) as well as upstream intra-entity gross profits (before deferral) included in the income for the current year follow:

The net income attributable to the noncontrolling interest of Jade Co.is calculated to be

A) $36,900.

B) $33,600.

C) $42,400.

D) $32,300.

E) $39,200.

The net income attributable to the noncontrolling interest of Jade Co.is calculated to be

A) $36,900.

B) $33,600.

C) $42,400.

D) $32,300.

E) $39,200.

Question

The accrual-based net income of Beagle Co.is calculated to be

A) $706,670.

B) $755,980.

C) $805,280.

D) $838,150.

E) $815,770.

Question

Hardford Corp. held 80% of Inglestone Inc., which, in turn, owned 80% of Jade Co. Excess amortization expense was not required by any of these acquisitions. Separate net income figures (without investment income) as well as upstream intra-entity gross profits (before deferral) included in the income for the current year follow:

The accrual-based net income of Jade Co.is calculated to be

A) $193,000.

B) $189,000.

C) $196,000.

D) $201,000.

E) $144,000.

The accrual-based net income of Jade Co.is calculated to be

A) $193,000.

B) $189,000.

C) $196,000.

D) $201,000.

E) $144,000.

Question

Question

Hardford Corp. held 80% of Inglestone Inc., which, in turn, owned 80% of Jade Co. Excess amortization expense was not required by any of these acquisitions. Separate net income figures (without investment income) as well as upstream intra-entity gross profits (before deferral) included in the income for the current year follow:

Compute the net income attributable to the noncontrolling interest in Ross for 2018.

A) $92,000.

B) $77,400.

C) $75,000.

D) $64,500.

E) $69,000.

Compute the net income attributable to the noncontrolling interest in Ross for 2018.

A) $92,000.

B) $77,400.

C) $75,000.

D) $64,500.

E) $69,000.

Question

Hardford Corp. held 80% of Inglestone Inc., which, in turn, owned 80% of Jade Co. Excess amortization expense was not required by any of these acquisitions. Separate net income figures (without investment income) as well as upstream intra-entity gross profits (before deferral) included in the income for the current year follow:

Compute Chase's attributed ownership in Ross.

A) 40.0%.

B) 64.0%.

C) 24.0%.

D) 32.0%.

E) 12.8%.

Compute Chase's attributed ownership in Ross.

A) 40.0%.

B) 64.0%.

C) 24.0%.

D) 32.0%.

E) 12.8%.

Question

Compute the amount allocated to trademarks recognized in the January 1, 2018 consolidated balance sheet.

A) $ 80,000.

B) $100,000.

C) $ 76,000.

D) $ 16,000.

E) $ -0-

Question

Hardford Corp. held 80% of Inglestone Inc., which, in turn, owned 80% of Jade Co. Excess amortization expense was not required by any of these acquisitions. Separate net income figures (without investment income) as well as upstream intra-entity gross profits (before deferral) included in the income for the current year follow:

Which of the following statements is true regarding goodwill?

A) For accounting purposes, goodwill may be amortized over a period not to exceed 40 years.

B) For accounting purposes, goodwill may be amortized over a period not to exceed 20 years.

C) For tax purposes, goodwill amortization cannot be deductible.

D) For tax purposes, goodwill amortization may be deductible over a 20-year period.

E) For tax purposes, goodwill amortization may be deductible over a 15-year period.

Which of the following statements is true regarding goodwill?

A) For accounting purposes, goodwill may be amortized over a period not to exceed 40 years.

B) For accounting purposes, goodwill may be amortized over a period not to exceed 20 years.

C) For tax purposes, goodwill amortization cannot be deductible.

D) For tax purposes, goodwill amortization may be deductible over a 20-year period.

E) For tax purposes, goodwill amortization may be deductible over a 15-year period.

Question

Compute Whitton's accrual-based consolidated net income for 2018.

A) $199,000.

B) $190,000.

C) $185,000.

D) $184,000.

E) $176,000.

Question

Hardford Corp. held 80% of Inglestone Inc., which, in turn, owned 80% of Jade Co. Excess amortization expense was not required by any of these acquisitions. Separate net income figures (without investment income) as well as upstream intra-entity gross profits (before deferral) included in the income for the current year follow:

The net income attributable to the noncontrolling interest of Inglestone Inc.is calculated to be

A) $106,950.

B) $102,640.

C) $114,530.

D) $106,960.

E) $103,680.

The net income attributable to the noncontrolling interest of Inglestone Inc.is calculated to be

A) $106,950.

B) $102,640.

C) $114,530.

D) $106,960.

E) $103,680.

Question

Hardford Corp. held 80% of Inglestone Inc., which, in turn, owned 80% of Jade Co. Excess amortization expense was not required by any of these acquisitions. Separate net income figures (without investment income) as well as upstream intra-entity gross profits (before deferral) included in the income for the current year follow:

Which of the following statements is true regarding mutual ownership between a parent and its subsidiary?

A) The shares of the parent held by a subsidiary should be treated as outstanding stock on the consolidated balance sheet.

B) Only the subsidiary's shares held by the parent should be eliminated in consolidation.

C) The treasury stock approach is required to reflect parent shares held by the subsidiary.

D) The treasury stock approach is required to eliminate subsidiary shares held by the parent company.

E) The parent company does not need to file consolidated financial statements if there is mutual ownership.

Which of the following statements is true regarding mutual ownership between a parent and its subsidiary?

A) The shares of the parent held by a subsidiary should be treated as outstanding stock on the consolidated balance sheet.

B) Only the subsidiary's shares held by the parent should be eliminated in consolidation.

C) The treasury stock approach is required to reflect parent shares held by the subsidiary.

D) The treasury stock approach is required to eliminate subsidiary shares held by the parent company.

E) The parent company does not need to file consolidated financial statements if there is mutual ownership.

Question

Hardford Corp. held 80% of Inglestone Inc., which, in turn, owned 80% of Jade Co. Excess amortization expense was not required by any of these acquisitions. Separate net income figures (without investment income) as well as upstream intra-entity gross profits (before deferral) included in the income for the current year follow:

Which of the following statements is true regarding a subsidiary's investment in the parent company's stock?

A) The treasury stock approach focuses on the parent's control over its subsidiary.

B) For consolidation, both the parent and subsidiary must defer gross profit on remaining inventory from intra-entity transfers.

C) In consolidation, the parent's retained earnings will not be reduced by the dividends it paid to the subsidiary.

D) This corporate combination is known as mutual ownership.

E) All of these answer choices are true statements.

Which of the following statements is true regarding a subsidiary's investment in the parent company's stock?

A) The treasury stock approach focuses on the parent's control over its subsidiary.

B) For consolidation, both the parent and subsidiary must defer gross profit on remaining inventory from intra-entity transfers.

C) In consolidation, the parent's retained earnings will not be reduced by the dividends it paid to the subsidiary.

D) This corporate combination is known as mutual ownership.

E) All of these answer choices are true statements.

Question

Hardford Corp. held 80% of Inglestone Inc., which, in turn, owned 80% of Jade Co. Excess amortization expense was not required by any of these acquisitions. Separate net income figures (without investment income) as well as upstream intra-entity gross profits (before deferral) included in the income for the current year follow:

Which of the following statements is true regarding the filing of income taxes for an affiliated group?

A) Domestic subsidiaries greater than 50% ownership must file a consolidated tax return.

B) Domestic subsidiaries greater than 60% ownership must file a consolidated tax return.

C) Domestic subsidiaries greater than 80% ownership must file a consolidated tax return.

D) Domestic subsidiaries greater than 80% ownership may file a consolidated tax return.

E) Foreign subsidiaries must file a consolidated tax return.

Which of the following statements is true regarding the filing of income taxes for an affiliated group?

A) Domestic subsidiaries greater than 50% ownership must file a consolidated tax return.

B) Domestic subsidiaries greater than 60% ownership must file a consolidated tax return.

C) Domestic subsidiaries greater than 80% ownership must file a consolidated tax return.

D) Domestic subsidiaries greater than 80% ownership may file a consolidated tax return.

E) Foreign subsidiaries must file a consolidated tax return.

Question

Hardford Corp. held 80% of Inglestone Inc., which, in turn, owned 80% of Jade Co. Excess amortization expense was not required by any of these acquisitions. Separate net income figures (without investment income) as well as upstream intra-entity gross profits (before deferral) included in the income for the current year follow:

When indirect control is present, which of the following statements is true?

A) At least one company within the consolidated entity holds a parent and a subsidiary relationship.

B) The parent company owns a percent of subsidiary and subsidiary owns a percent of the parent.

C) Consolidated financial statements are required for only one subsidiary.

D) Recognition of income for an indirectly owned subsidiary is ignored.

E) Only dividend income is recognized for an indirectly owned subsidiary.

When indirect control is present, which of the following statements is true?

A) At least one company within the consolidated entity holds a parent and a subsidiary relationship.

B) The parent company owns a percent of subsidiary and subsidiary owns a percent of the parent.

C) Consolidated financial statements are required for only one subsidiary.

D) Recognition of income for an indirectly owned subsidiary is ignored.

E) Only dividend income is recognized for an indirectly owned subsidiary.

Question

Hardford Corp. held 80% of Inglestone Inc., which, in turn, owned 80% of Jade Co. Excess amortization expense was not required by any of these acquisitions. Separate net income figures (without investment income) as well as upstream intra-entity gross profits (before deferral) included in the income for the current year follow:

Which of the following statements is true regarding the subsidiary's investment in its parent's common stock?

A) All of the parent company's common stock is eliminated.

B) The consolidation worksheet entry to eliminate the subsidiary's investment in parent's common stock is debited to treasury stock.

C) The consolidation worksheet entry to eliminate the subsidiary's investment in parent's common stock is debited to retained earnings.

D) The consolidation worksheet entry to eliminate the subsidiary's investment in parent's common stock is debited to additional paid-in capital.

E) The investment in parent company's common stock is not eliminated in consolidation.

Which of the following statements is true regarding the subsidiary's investment in its parent's common stock?

A) All of the parent company's common stock is eliminated.

B) The consolidation worksheet entry to eliminate the subsidiary's investment in parent's common stock is debited to treasury stock.

C) The consolidation worksheet entry to eliminate the subsidiary's investment in parent's common stock is debited to retained earnings.

D) The consolidation worksheet entry to eliminate the subsidiary's investment in parent's common stock is debited to additional paid-in capital.

E) The investment in parent company's common stock is not eliminated in consolidation.

Question

Hardford Corp. held 80% of Inglestone Inc., which, in turn, owned 80% of Jade Co. Excess amortization expense was not required by any of these acquisitions. Separate net income figures (without investment income) as well as upstream intra-entity gross profits (before deferral) included in the income for the current year follow:

The benefits of filing a consolidated tax return include all of the following except

A) Gross profits from intra-entity transfers are not taxed until such amounts are recognized for financial statement reporting purposes.

B) Recognition of gross profits from intra-entity transfers is deferred for income tax recognition purposes.

C) The issuance of dividends between related entities are not taxable.

D) Losses incurred by an affiliated company can be used to reduce taxable income earned by other members to that affiliated group.

E) Gross profits on intra-entity transfers are taxed before they are recognized for financial statement reporting purposes in the year of the transfer, but any such losses are deferred.

The benefits of filing a consolidated tax return include all of the following except

A) Gross profits from intra-entity transfers are not taxed until such amounts are recognized for financial statement reporting purposes.

B) Recognition of gross profits from intra-entity transfers is deferred for income tax recognition purposes.

C) The issuance of dividends between related entities are not taxable.

D) Losses incurred by an affiliated company can be used to reduce taxable income earned by other members to that affiliated group.

E) Gross profits on intra-entity transfers are taxed before they are recognized for financial statement reporting purposes in the year of the transfer, but any such losses are deferred.

Question

The accrual-based net income of Maroon Corp.is calculated to be

A) $481,600.

B) $472,700.

C) $488,900.

D) $502,300.

E) $358,800.

Question

Compute the net income attributable to the noncontrolling interest for 2018.

A) $11,000.

B) $10,800.

C) $ 9,000.

D) $ 8,200.

E) $ 7,200.

Question

Hardford Corp. held 80% of Inglestone Inc., which, in turn, owned 80% of Jade Co. Excess amortization expense was not required by any of these acquisitions. Separate net income figures (without investment income) as well as upstream intra-entity gross profits (before deferral) included in the income for the current year follow:

Which of the following statements is false concerning a father-son-grandson configuration?

A) This type of ownership pattern does not significantly alter the worksheet process.

B) Most worksheet entries are simply made twice.

C) The doubling of entries may seem overwhelming.

D) The individual consolidation procedures remain unaffected.

E) Consolidated financial statements are required for only the father and son companies.

Which of the following statements is false concerning a father-son-grandson configuration?

A) This type of ownership pattern does not significantly alter the worksheet process.

B) Most worksheet entries are simply made twice.

C) The doubling of entries may seem overwhelming.

D) The individual consolidation procedures remain unaffected.

E) Consolidated financial statements are required for only the father and son companies.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Using the percentage allocation method for assigning income tax expense, the income tax expense assigned to Hill is closest to:

A) $21,000.

B) $24,000.

C) $20,100.

D) $17,400.

E) $ 0.

Question

Question

Question

Under the separate return method, income tax expense that will be assigned to Hill is closest to:

A) $24,000.

B) $22,857.

C) $24,874.

D) $21,874.

E) $21,000.

Question

What is the income tax liability for the current year if consolidated tax returns are prepared?

A) $55,560.

B) $70,350.

C) $60,000.

D) $73,500.

E) $84,000.

Question

Compute accrual-based consolidated income before income tax.

A) $280,000.

B) $245,000.

C) $200,000.

D) $255,200.

E) $290,200.

Question

Question

Question

Question

Question

Question

Question

Which of the following statements is true?

A) Alpha and Beta must file a consolidated income tax return, but must exclude Gamma from the consolidated return.

B) Alpha, Beta, and Gamma must file a consolidated income tax return.

C) Alpha, Beta, and Gamma must file separate income tax returns because the ownership of Beta is less than 100%.

D) Alpha, Beta, and Gamma will probably not file a consolidated income tax return.

E) Alpha, Beta, and Gamma may file separate income tax returns or a consolidated income tax return.

Question

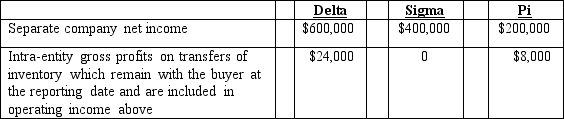

What is Pi's accrual-based net income for 2018?

A) $152,000.

B) $ 16,000.

C) $192,000.

D) $200,000.

E) $208,000.

Question

Question

What is the net income attributable to the noncontrolling interest in Pi for 2018?

A) $ 0.

B) $ 9,600.

C) $10,000.

D) $19,200.

E) $20,000.

Question

Question

What is Delta's accrual-based net income for 2018?

A) $1,091,520.

B) $1,115,520.

C) $1,168,000.

D) $1,168,520.

E) $1,200,000.

Question

What is Beta's accrual-based net income for 2018?

A) $200,000.

B) $276,800.

C) $280,000.

D) $296,000.

E) $300,000.

Question

Question

Question

What is Sigma's accrual-based income for 2018?

A) $400,000.

B) $592,000.

C) $540,000.

D) $572,800.

E) $600,000.

Question

What is the net income attributable to the noncontrolling interest in Sigma for 2018?

A) $55,240.

B) $56,420.

C) $57,280.

D) $59,420.

E) $60,000.

Question

What is the total net income attributable to the noncontrolling interest for 2018?

A) $55,240.

B) $66,020.

C) $67,280.

D) $76,280.

E) $76,480.

Question

What is Alpha's accrual-based net income for 2018?

A) $564,000.

B) $564,800.

C) $572,200.

D) $580,000.

E) $600,000.

Question

Question

What is Gamma's accrual-based net income for 2018?

A) $ 76,000.

B) $ 80,000.

C) $ 96,000.

D) $100,000.

E) $104,000.

Question

What is the total net income attributable to the noncontrolling interests for 2018?

A) $ 0.

B) $ 9,600.

C) $10,000.

D) $19,200.

E) $20,000.

Question

What is the net income attributable to the noncontrolling interest in Gamma for 2018?

A) $ 0.

B) $ 9,600.

C) $10,000.

D) $19,200.

E) $20,000.

Question

Question

Question

Which of the following statements is true?

A) Delta and Sigma must file a consolidated income tax return, but must exclude Pi from the consolidated return.

B) Delta, Sigma, and Pi must file a consolidated income tax return.

C) Delta, Sigma, and Pi must file separate income tax returns because the ownership of Sigma and Pi is less than 100%.

D) Delta, Sigma, and Pi will probably not file a consolidated income tax return.

E) Delta, Sigma, and Pi may file separate income tax returns or a consolidated income tax return.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/112

Play

Full screen (f)

Deck 7: Consolidated Financial Statements - Ownership Patterns and Income Taxes

1

Evanston Co.owned 60% of Montgomery Corp.Montgomery owned 75% of Noir Inc., and Noir owned 15% of Montgomery.This pattern of ownership would be called…

A) Mutual ownership.

B) Direct control.

C) Indirect control.

D) An affiliated group.

E) A connecting affiliation.

A) Mutual ownership.

B) Direct control.

C) Indirect control.

D) An affiliated group.

E) A connecting affiliation.

A

2

How would the 10% Investment in Prescott owned by Bell be presented in the consolidated balance sheet?

A) The 10% investment would be eliminated and no amount would be shown in the consolidated balance sheet.

B) The 10% investment would be reclassified in Bell's balance sheet as Treasury Stock before the consolidation process begins.

C) The 10% investment would be eliminated and the same dollar amount would appear as treasury stock in the consolidated balance sheet.

D) The 10% investment would be included as part of Additional Paid-In Capital because it is less than 20% and therefore indicates no significant influence is present.

E) Prescott would treat the shares owned by Bell as if they had been repurchased on the open market, and a treasury stock account would be set up on Prescott's books recording the shares at their fair value on the date of combination.

A) The 10% investment would be eliminated and no amount would be shown in the consolidated balance sheet.

B) The 10% investment would be reclassified in Bell's balance sheet as Treasury Stock before the consolidation process begins.

C) The 10% investment would be eliminated and the same dollar amount would appear as treasury stock in the consolidated balance sheet.

D) The 10% investment would be included as part of Additional Paid-In Capital because it is less than 20% and therefore indicates no significant influence is present.

E) Prescott would treat the shares owned by Bell as if they had been repurchased on the open market, and a treasury stock account would be set up on Prescott's books recording the shares at their fair value on the date of combination.

C

3

On January 1, 2018, a subsidiary bought 10% of the outstanding shares of its parent company.Although the total book value and fair value of the parent's net assets were $5.5 million, the consideration transferred for these shares was $590,000.During 2018, the parent reported separate net income of $714,000, before including investment income, while dividends declared were $196,000.How were these shares reported at December 31, 2018?

A) The investment was recorded for $641,800 at the end of 2018 and then eliminated for consolidation purposes.

B) Consolidated stockholders' equity was reduced by $641,800.

C) The investment was recorded for $590,000 at the end of 2018 and then eliminated for consolidation purposes.

D) Consolidated stockholders' equity was reduced by $639,800.

E) Consolidated stockholders' equity was reduced by $590,000.

A) The investment was recorded for $641,800 at the end of 2018 and then eliminated for consolidation purposes.

B) Consolidated stockholders' equity was reduced by $641,800.

C) The investment was recorded for $590,000 at the end of 2018 and then eliminated for consolidation purposes.

D) Consolidated stockholders' equity was reduced by $639,800.

E) Consolidated stockholders' equity was reduced by $590,000.

E

4

D Corp.had investments, direct and indirect, in several subsidiaries: -E Co.is a domestic firm in which D Corp.owned a 90% interest

-F Co.is a domestic firm in which D Corp.owned 60% and E Co.owned 30%

-G Co.is a domestic firm wholly owned by E Co.

-H Co.is a foreign subsidiary in which D Corp.owned a 90% interest

-I Co.is a domestic firm in which D Corp.owned 50% and G Co.owned 25%

Which of these subsidiaries may be included in a consolidated income tax return?

A) E, F, G, H, and I.

B) E, G, H, and I.

C) E and F.

D) E, F, G, and H.

E) E, F, and G.

-F Co.is a domestic firm in which D Corp.owned 60% and E Co.owned 30%

-G Co.is a domestic firm wholly owned by E Co.

-H Co.is a foreign subsidiary in which D Corp.owned a 90% interest

-I Co.is a domestic firm in which D Corp.owned 50% and G Co.owned 25%

Which of these subsidiaries may be included in a consolidated income tax return?

A) E, F, G, H, and I.

B) E, G, H, and I.

C) E and F.

D) E, F, G, and H.

E) E, F, and G.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

5

On a consolidated income statement, what is the net income attributable to the noncontrolling interest?

A) $ 9,800.

B) $13,692.

C) $10,836.

D) $12,460.

E) $11,214.

A) $ 9,800.

B) $13,692.

C) $10,836.

D) $12,460.

E) $11,214.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

6

In a tax-free business combination,

A) The income tax basis for acquired assets and liabilities is adjusted to current fair value.

B) Any goodwill created by the combination may be amortized in calculating taxable income.

C) The subsidiary's assets and liabilities are assigned an income tax basis of zero dollars, so that they will have no future income tax consequences.

D) Any goodwill created by the combination must be deducted in total in calculating taxable income.

E) The subsidiary's cost basis for assets are retained for income tax calculations.

A) The income tax basis for acquired assets and liabilities is adjusted to current fair value.

B) Any goodwill created by the combination may be amortized in calculating taxable income.

C) The subsidiary's assets and liabilities are assigned an income tax basis of zero dollars, so that they will have no future income tax consequences.

D) Any goodwill created by the combination must be deducted in total in calculating taxable income.

E) The subsidiary's cost basis for assets are retained for income tax calculations.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

7

What is the amount of taxable income reported on the consolidated income tax return?

A) $720,000.

B) $625,000.

C) $621,000.

D) $665,000.

E) $655,000.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

8

What percentage of Tayle's income is attributed to Buckette's ownership interest?

A) 100%.

B) 75%.

C) 61%.

D) 40%.

E) 74%.

A) 100%.

B) 75%.

C) 61%.

D) 40%.

E) 74%.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

9

The accrual-based net income of Eckston Inc.is calculated to be

A) $234,000.

B) $211,000.

C) $221,000.

D) $224,000.

E) $246,000.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

10

What is this pattern of ownership called?

A) Pyramid ownership.

B) A connecting affiliation.

C) Mutual ownership.

D) An indirect affiliation.

E) An affiliated group.

A) Pyramid ownership.

B) A connecting affiliation.

C) Mutual ownership.

D) An indirect affiliation.

E) An affiliated group.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

11

For West Corp.and consolidated subsidiaries, what total amount would be reported for the net income attributable to the noncontrolling interest?

A) $165,300.

B) $199,300.

C) $191,000.

D) $228,000.

E) $153,000.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

12

The amount of income tax expense that should be assigned to Boat using the separate return method is approximately:

A) $36,000

B) $31,500

C) $33,390

D) $32,750

E) $32,660

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

13

The accrual-based net income of East Co.is calculated to be

A) $401,100.

B) $510,000.

C) $551,000.

D) $573,000.

E) $615,000.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

14

What is the amount of income tax expense that should be assigned to Boat using the percentage allocation method?

A) $31,500

B) $32,750

C) $36,000

D) $32,660

E) $30,390

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

15

Jastoon Co.acquired all of Wedner Co.for $588,000 cash in a tax-free transaction.On that date, the subsidiary had net assets with a $560,000 fair value but a $420,000 book value and income tax basis.The income tax rate was 30%.What amount of goodwill should have been recognized on the date of the acquisition?

A) $ 70,000.

B) $ 28,000.

C) $ (14,000).

D) $ 19,600.

E) $ 65,000.

A) $ 70,000.

B) $ 28,000.

C) $ (14,000).

D) $ 19,600.

E) $ 65,000.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

16

The accrual-based net income of West Corp.is calculated to be

A) $ 734,000.

B) $1,261,000.

C) $1,123,900.

D) $1,140,700.

E) $1,149,700.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

17

What amount of dividends should West Corp.recognize in its consolidated net income with respect to dividends received from Compass Co.?

A) $ -0-

B) $25,200.

C) $36,000.

D) $42,000.

E) $90,000.

A) $ -0-

B) $25,200.

C) $36,000.

D) $42,000.

E) $90,000.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

18

When Buckette prepares consolidated financial statements, it should include

A) Shuvelle but not Tayle.

B) Tayle but not Shuvelle.

C) Either Shuvelle or Tayle.

D) Shuvelle and Tayle.

E) Neither Shuvelle nor Tayle.

A) Shuvelle but not Tayle.

B) Tayle but not Shuvelle.

C) Either Shuvelle or Tayle.

D) Shuvelle and Tayle.

E) Neither Shuvelle nor Tayle.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

19

What amount should be reported for consolidated net income?

A) $1,285,000.

B) $1,331,700.

C) $1,349,000.

D) $1,315,000.

E) $1,314,900.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

20

What was the net income attributable to the noncontrolling interest, assuming that the separate return method was used to assign the income tax expense?

A) $16,800

B) $14,450

C) $14,700

D) $17,450

E) $13,800

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

21

Compute Lawrence's accrual-based net income for 2018.

A) $354,000.

B) $329,500.

C) $334,000.

D) $265,000.

E) $344,500.

A) $354,000.

B) $329,500.

C) $334,000.

D) $265,000.

E) $344,500.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

22

Hardford Corp. held 80% of Inglestone Inc., which, in turn, owned 80% of Jade Co. Excess amortization expense was not required by any of these acquisitions. Separate net income figures (without investment income) as well as upstream intra-entity gross profits (before deferral) included in the income for the current year follow:

The net income attributable to the noncontrolling interest of Jade Co.is calculated to be

A) $36,900.

B) $33,600.

C) $42,400.

D) $32,300.

E) $39,200.

The net income attributable to the noncontrolling interest of Jade Co.is calculated to be

A) $36,900.

B) $33,600.

C) $42,400.

D) $32,300.

E) $39,200.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

23

The accrual-based net income of Beagle Co.is calculated to be

A) $706,670.

B) $755,980.

C) $805,280.

D) $838,150.

E) $815,770.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

24

Hardford Corp. held 80% of Inglestone Inc., which, in turn, owned 80% of Jade Co. Excess amortization expense was not required by any of these acquisitions. Separate net income figures (without investment income) as well as upstream intra-entity gross profits (before deferral) included in the income for the current year follow:

The accrual-based net income of Jade Co.is calculated to be

A) $193,000.

B) $189,000.

C) $196,000.

D) $201,000.

E) $144,000.

The accrual-based net income of Jade Co.is calculated to be

A) $193,000.

B) $189,000.

C) $196,000.

D) $201,000.

E) $144,000.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

25

Compute Chase's accrual-based net income for 2018.

A) $746,000.

B) $719,000.

C) $779,600.

D) $774,200.

E) $758,100.

A) $746,000.

B) $719,000.

C) $779,600.

D) $774,200.

E) $758,100.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

26

Hardford Corp. held 80% of Inglestone Inc., which, in turn, owned 80% of Jade Co. Excess amortization expense was not required by any of these acquisitions. Separate net income figures (without investment income) as well as upstream intra-entity gross profits (before deferral) included in the income for the current year follow:

Compute the net income attributable to the noncontrolling interest in Ross for 2018.

A) $92,000.

B) $77,400.

C) $75,000.

D) $64,500.

E) $69,000.

Compute the net income attributable to the noncontrolling interest in Ross for 2018.

A) $92,000.

B) $77,400.

C) $75,000.

D) $64,500.

E) $69,000.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

27

Hardford Corp. held 80% of Inglestone Inc., which, in turn, owned 80% of Jade Co. Excess amortization expense was not required by any of these acquisitions. Separate net income figures (without investment income) as well as upstream intra-entity gross profits (before deferral) included in the income for the current year follow:

Compute Chase's attributed ownership in Ross.

A) 40.0%.

B) 64.0%.

C) 24.0%.

D) 32.0%.

E) 12.8%.

Compute Chase's attributed ownership in Ross.

A) 40.0%.

B) 64.0%.

C) 24.0%.

D) 32.0%.

E) 12.8%.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

28

Compute the amount allocated to trademarks recognized in the January 1, 2018 consolidated balance sheet.

A) $ 80,000.

B) $100,000.

C) $ 76,000.

D) $ 16,000.

E) $ -0-

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

29

Hardford Corp. held 80% of Inglestone Inc., which, in turn, owned 80% of Jade Co. Excess amortization expense was not required by any of these acquisitions. Separate net income figures (without investment income) as well as upstream intra-entity gross profits (before deferral) included in the income for the current year follow:

Which of the following statements is true regarding goodwill?

A) For accounting purposes, goodwill may be amortized over a period not to exceed 40 years.

B) For accounting purposes, goodwill may be amortized over a period not to exceed 20 years.

C) For tax purposes, goodwill amortization cannot be deductible.

D) For tax purposes, goodwill amortization may be deductible over a 20-year period.

E) For tax purposes, goodwill amortization may be deductible over a 15-year period.

Which of the following statements is true regarding goodwill?

A) For accounting purposes, goodwill may be amortized over a period not to exceed 40 years.

B) For accounting purposes, goodwill may be amortized over a period not to exceed 20 years.

C) For tax purposes, goodwill amortization cannot be deductible.

D) For tax purposes, goodwill amortization may be deductible over a 20-year period.

E) For tax purposes, goodwill amortization may be deductible over a 15-year period.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

30

Compute Whitton's accrual-based consolidated net income for 2018.

A) $199,000.

B) $190,000.

C) $185,000.

D) $184,000.

E) $176,000.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

31

Hardford Corp. held 80% of Inglestone Inc., which, in turn, owned 80% of Jade Co. Excess amortization expense was not required by any of these acquisitions. Separate net income figures (without investment income) as well as upstream intra-entity gross profits (before deferral) included in the income for the current year follow:

The net income attributable to the noncontrolling interest of Inglestone Inc.is calculated to be

A) $106,950.

B) $102,640.

C) $114,530.

D) $106,960.

E) $103,680.

The net income attributable to the noncontrolling interest of Inglestone Inc.is calculated to be

A) $106,950.

B) $102,640.

C) $114,530.

D) $106,960.

E) $103,680.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

32

Hardford Corp. held 80% of Inglestone Inc., which, in turn, owned 80% of Jade Co. Excess amortization expense was not required by any of these acquisitions. Separate net income figures (without investment income) as well as upstream intra-entity gross profits (before deferral) included in the income for the current year follow:

Which of the following statements is true regarding mutual ownership between a parent and its subsidiary?

A) The shares of the parent held by a subsidiary should be treated as outstanding stock on the consolidated balance sheet.

B) Only the subsidiary's shares held by the parent should be eliminated in consolidation.

C) The treasury stock approach is required to reflect parent shares held by the subsidiary.

D) The treasury stock approach is required to eliminate subsidiary shares held by the parent company.

E) The parent company does not need to file consolidated financial statements if there is mutual ownership.

Which of the following statements is true regarding mutual ownership between a parent and its subsidiary?

A) The shares of the parent held by a subsidiary should be treated as outstanding stock on the consolidated balance sheet.

B) Only the subsidiary's shares held by the parent should be eliminated in consolidation.

C) The treasury stock approach is required to reflect parent shares held by the subsidiary.

D) The treasury stock approach is required to eliminate subsidiary shares held by the parent company.

E) The parent company does not need to file consolidated financial statements if there is mutual ownership.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

33

Hardford Corp. held 80% of Inglestone Inc., which, in turn, owned 80% of Jade Co. Excess amortization expense was not required by any of these acquisitions. Separate net income figures (without investment income) as well as upstream intra-entity gross profits (before deferral) included in the income for the current year follow:

Which of the following statements is true regarding a subsidiary's investment in the parent company's stock?

A) The treasury stock approach focuses on the parent's control over its subsidiary.

B) For consolidation, both the parent and subsidiary must defer gross profit on remaining inventory from intra-entity transfers.

C) In consolidation, the parent's retained earnings will not be reduced by the dividends it paid to the subsidiary.

D) This corporate combination is known as mutual ownership.

E) All of these answer choices are true statements.

Which of the following statements is true regarding a subsidiary's investment in the parent company's stock?

A) The treasury stock approach focuses on the parent's control over its subsidiary.

B) For consolidation, both the parent and subsidiary must defer gross profit on remaining inventory from intra-entity transfers.

C) In consolidation, the parent's retained earnings will not be reduced by the dividends it paid to the subsidiary.

D) This corporate combination is known as mutual ownership.

E) All of these answer choices are true statements.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

34

Hardford Corp. held 80% of Inglestone Inc., which, in turn, owned 80% of Jade Co. Excess amortization expense was not required by any of these acquisitions. Separate net income figures (without investment income) as well as upstream intra-entity gross profits (before deferral) included in the income for the current year follow:

Which of the following statements is true regarding the filing of income taxes for an affiliated group?

A) Domestic subsidiaries greater than 50% ownership must file a consolidated tax return.

B) Domestic subsidiaries greater than 60% ownership must file a consolidated tax return.

C) Domestic subsidiaries greater than 80% ownership must file a consolidated tax return.

D) Domestic subsidiaries greater than 80% ownership may file a consolidated tax return.

E) Foreign subsidiaries must file a consolidated tax return.

Which of the following statements is true regarding the filing of income taxes for an affiliated group?

A) Domestic subsidiaries greater than 50% ownership must file a consolidated tax return.

B) Domestic subsidiaries greater than 60% ownership must file a consolidated tax return.

C) Domestic subsidiaries greater than 80% ownership must file a consolidated tax return.

D) Domestic subsidiaries greater than 80% ownership may file a consolidated tax return.

E) Foreign subsidiaries must file a consolidated tax return.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

35

Hardford Corp. held 80% of Inglestone Inc., which, in turn, owned 80% of Jade Co. Excess amortization expense was not required by any of these acquisitions. Separate net income figures (without investment income) as well as upstream intra-entity gross profits (before deferral) included in the income for the current year follow:

When indirect control is present, which of the following statements is true?

A) At least one company within the consolidated entity holds a parent and a subsidiary relationship.

B) The parent company owns a percent of subsidiary and subsidiary owns a percent of the parent.

C) Consolidated financial statements are required for only one subsidiary.

D) Recognition of income for an indirectly owned subsidiary is ignored.

E) Only dividend income is recognized for an indirectly owned subsidiary.

When indirect control is present, which of the following statements is true?

A) At least one company within the consolidated entity holds a parent and a subsidiary relationship.

B) The parent company owns a percent of subsidiary and subsidiary owns a percent of the parent.

C) Consolidated financial statements are required for only one subsidiary.

D) Recognition of income for an indirectly owned subsidiary is ignored.

E) Only dividend income is recognized for an indirectly owned subsidiary.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

36

Hardford Corp. held 80% of Inglestone Inc., which, in turn, owned 80% of Jade Co. Excess amortization expense was not required by any of these acquisitions. Separate net income figures (without investment income) as well as upstream intra-entity gross profits (before deferral) included in the income for the current year follow:

Which of the following statements is true regarding the subsidiary's investment in its parent's common stock?

A) All of the parent company's common stock is eliminated.

B) The consolidation worksheet entry to eliminate the subsidiary's investment in parent's common stock is debited to treasury stock.

C) The consolidation worksheet entry to eliminate the subsidiary's investment in parent's common stock is debited to retained earnings.

D) The consolidation worksheet entry to eliminate the subsidiary's investment in parent's common stock is debited to additional paid-in capital.

E) The investment in parent company's common stock is not eliminated in consolidation.

Which of the following statements is true regarding the subsidiary's investment in its parent's common stock?

A) All of the parent company's common stock is eliminated.

B) The consolidation worksheet entry to eliminate the subsidiary's investment in parent's common stock is debited to treasury stock.

C) The consolidation worksheet entry to eliminate the subsidiary's investment in parent's common stock is debited to retained earnings.

D) The consolidation worksheet entry to eliminate the subsidiary's investment in parent's common stock is debited to additional paid-in capital.

E) The investment in parent company's common stock is not eliminated in consolidation.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

37

Hardford Corp. held 80% of Inglestone Inc., which, in turn, owned 80% of Jade Co. Excess amortization expense was not required by any of these acquisitions. Separate net income figures (without investment income) as well as upstream intra-entity gross profits (before deferral) included in the income for the current year follow:

The benefits of filing a consolidated tax return include all of the following except

A) Gross profits from intra-entity transfers are not taxed until such amounts are recognized for financial statement reporting purposes.

B) Recognition of gross profits from intra-entity transfers is deferred for income tax recognition purposes.

C) The issuance of dividends between related entities are not taxable.

D) Losses incurred by an affiliated company can be used to reduce taxable income earned by other members to that affiliated group.

E) Gross profits on intra-entity transfers are taxed before they are recognized for financial statement reporting purposes in the year of the transfer, but any such losses are deferred.

The benefits of filing a consolidated tax return include all of the following except

A) Gross profits from intra-entity transfers are not taxed until such amounts are recognized for financial statement reporting purposes.

B) Recognition of gross profits from intra-entity transfers is deferred for income tax recognition purposes.

C) The issuance of dividends between related entities are not taxable.

D) Losses incurred by an affiliated company can be used to reduce taxable income earned by other members to that affiliated group.

E) Gross profits on intra-entity transfers are taxed before they are recognized for financial statement reporting purposes in the year of the transfer, but any such losses are deferred.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

38

The accrual-based net income of Maroon Corp.is calculated to be

A) $481,600.

B) $472,700.

C) $488,900.

D) $502,300.

E) $358,800.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

39

Compute the net income attributable to the noncontrolling interest for 2018.

A) $11,000.

B) $10,800.

C) $ 9,000.

D) $ 8,200.

E) $ 7,200.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

40

Hardford Corp. held 80% of Inglestone Inc., which, in turn, owned 80% of Jade Co. Excess amortization expense was not required by any of these acquisitions. Separate net income figures (without investment income) as well as upstream intra-entity gross profits (before deferral) included in the income for the current year follow:

Which of the following statements is false concerning a father-son-grandson configuration?

A) This type of ownership pattern does not significantly alter the worksheet process.

B) Most worksheet entries are simply made twice.

C) The doubling of entries may seem overwhelming.

D) The individual consolidation procedures remain unaffected.

E) Consolidated financial statements are required for only the father and son companies.

Which of the following statements is false concerning a father-son-grandson configuration?

A) This type of ownership pattern does not significantly alter the worksheet process.

B) Most worksheet entries are simply made twice.

C) The doubling of entries may seem overwhelming.

D) The individual consolidation procedures remain unaffected.

E) Consolidated financial statements are required for only the father and son companies.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

41

Which of the following conditions will allow two companies to file a consolidated income tax return?

A) One company owns less than 50 percent of the other company's voting stock but has the ability to significantly influence the other company.

B) One company holds 50 percent of the other company's voting stock.

C) One company holds 75 percent of the other company's voting stock

D) One company holds 83 percent of the other company's voting stock.

E) None of the above.

A) One company owns less than 50 percent of the other company's voting stock but has the ability to significantly influence the other company.

B) One company holds 50 percent of the other company's voting stock.

C) One company holds 75 percent of the other company's voting stock

D) One company holds 83 percent of the other company's voting stock.

E) None of the above.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

42

Strong Company has had poor operating results in recent years and has a $160,000 net operating loss carryforward.Leader Corp.pays $700,000 to acquire Strong and is optimistic about its future profitability potential.The book value and fair value of Strong's identifiable net assets is $500,000 at date of acquisition.Strong's tax rate is 30% and Leader's tax rate is 40%.What is goodwill resulting from this business acquisition?

A) $ 40,000.

B) $ 88,000.

C) $104,000.

D) $152,000.

E) $248,000.

A) $ 40,000.

B) $ 88,000.

C) $104,000.

D) $152,000.

E) $248,000.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

43

White Company owns 60% of Cody Company. Separate tax returns are required. For 2017, White's operating income (excluding taxes and any income from Cody) was $300,000 while Cody reported a pretax income of $125,000. During the period, Cody declared total dividends of $25,000; $15,000 (60%) to White and $10,000 to the noncontrolling interest. White declared dividends of $180,000. The income tax rate for both companies is 30%.

Compute White's deferred income taxes for 2018.

A) $ 6,000.

B) $ 2,250.

C) $ 3,150.

D) $11,250.

E) $21,000.

Compute White's deferred income taxes for 2018.

A) $ 6,000.

B) $ 2,250.

C) $ 3,150.

D) $11,250.

E) $21,000.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

44

White Company owns 60% of Cody Company. Separate tax returns are required. For 2017, White's operating income (excluding taxes and any income from Cody) was $300,000 while Cody reported a pretax income of $125,000. During the period, Cody declared total dividends of $25,000; $15,000 (60%) to White and $10,000 to the noncontrolling interest. White declared dividends of $180,000. The income tax rate for both companies is 30%.

Compute the income tax liability of White for 2018.

A) $93,600.

B) $91,350.

C) $94,500.

D) $90,900.

E) $90,000.

Compute the income tax liability of White for 2018.

A) $93,600.

B) $91,350.

C) $94,500.

D) $90,900.

E) $90,000.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

45

Under current U.S.tax law for consolidated tax returns:

A) One entity in the group can use another entity's net operating loss carryforward to its advantage.

B) The parent can use the net operating loss carryforward of another entity in the group.

C) A net operating loss carryforward if an entity will be unusable when consolidated tax returns are prepared.

D) A net operating loss carryforward of an entity in the group can only be used by that entity.

E) Since the tax return is for all entities in one consolidated group, the net operating loss carryforward of one entity must be pro-rated to all other entities in the group.

A) One entity in the group can use another entity's net operating loss carryforward to its advantage.

B) The parent can use the net operating loss carryforward of another entity in the group.

C) A net operating loss carryforward if an entity will be unusable when consolidated tax returns are prepared.

D) A net operating loss carryforward of an entity in the group can only be used by that entity.

E) Since the tax return is for all entities in one consolidated group, the net operating loss carryforward of one entity must be pro-rated to all other entities in the group.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

46

White Company owns 60% of Cody Company. Separate tax returns are required. For 2017, White's operating income (excluding taxes and any income from Cody) was $300,000 while Cody reported a pretax income of $125,000. During the period, Cody declared total dividends of $25,000; $15,000 (60%) to White and $10,000 to the noncontrolling interest. White declared dividends of $180,000. The income tax rate for both companies is 30%.

Compute the income tax liability of Cody for 2018.

A) $33,000.

B) $34,500.

C) $37,500.

D) $30,000.

E) $22,500.

Compute the income tax liability of Cody for 2018.

A) $33,000.

B) $34,500.

C) $37,500.

D) $30,000.

E) $22,500.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

47

Which of the following is true concerning the treasury stock approach in accounting for a subsidiary's investment in parent company stock?

A) The original cost of the subsidiary's investment reduces long-term liabilities.

B) The cost of parent shares is treated as if the shares are no longer outstanding.

C) The subsidiary must apply the equity method in accounting for the investment if the treasury stock approach is used.

D) The treasury stock approach increases total stockholders' equity.

E) The cost of parent shares is treated as if the shares are no longer issued.

A) The original cost of the subsidiary's investment reduces long-term liabilities.

B) The cost of parent shares is treated as if the shares are no longer outstanding.

C) The subsidiary must apply the equity method in accounting for the investment if the treasury stock approach is used.

D) The treasury stock approach increases total stockholders' equity.

E) The cost of parent shares is treated as if the shares are no longer issued.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

48

In a father-son-grandson combination, which of the following statements is true?

A) Companies that are solely in subsidiary positions must have their accrual-based net income computed first in the consolidation process.

B) Father-son-grandson configurations never require consolidation unless one company owns 100% of at least one other member of the combined group.

C) The order of the computation of accrual-based net income is not important in the consolidation process.

D) The parent must have its accrual-based net income computed first in the consolidation process.

E) None of these answer choices are correct.

A) Companies that are solely in subsidiary positions must have their accrual-based net income computed first in the consolidation process.

B) Father-son-grandson configurations never require consolidation unless one company owns 100% of at least one other member of the combined group.

C) The order of the computation of accrual-based net income is not important in the consolidation process.

D) The parent must have its accrual-based net income computed first in the consolidation process.

E) None of these answer choices are correct.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

49

Using the percentage allocation method for assigning income tax expense, the income tax expense assigned to Hill is closest to:

A) $21,000.

B) $24,000.

C) $20,100.

D) $17,400.

E) $ 0.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

50

How is goodwill amortized?

A) It is not amortized for reporting purposes or for tax purposes.

B) It is not amortized for reporting purposes, but is amortized over a 5-year life for tax purposes.

C) It is not amortized for tax purposes, but is amortized over a 5-year life for reporting purposes.

D) It is not amortized for tax purposes, but is amortized over a 15-year life for reporting purposes.

E) It is not amortized for reporting purposes, but is amortized over a 15-year life for tax purposes.

A) It is not amortized for reporting purposes or for tax purposes.

B) It is not amortized for reporting purposes, but is amortized over a 5-year life for tax purposes.

C) It is not amortized for tax purposes, but is amortized over a 5-year life for reporting purposes.

D) It is not amortized for tax purposes, but is amortized over a 15-year life for reporting purposes.

E) It is not amortized for reporting purposes, but is amortized over a 15-year life for tax purposes.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

51

Woods Company has one depreciable asset valued at $800,000.Because of recent losses, the company has a net operating loss carryforward of $150,000.The tax rate is 30%.The company was acquired for $1,000,000.It is more likely than not that the tax benefit will be realized.Compute the goodwill recognized for consolidated financial statements.

A) $ 0.

B) $155,000.

C) $200,000.

D) $305,000.

E) $350,000.

A) $ 0.

B) $155,000.

C) $200,000.

D) $305,000.

E) $350,000.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

52

Under the separate return method, income tax expense that will be assigned to Hill is closest to:

A) $24,000.

B) $22,857.

C) $24,874.

D) $21,874.

E) $21,000.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

53

What is the income tax liability for the current year if consolidated tax returns are prepared?

A) $55,560.

B) $70,350.

C) $60,000.

D) $73,500.

E) $84,000.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

54

Compute accrual-based consolidated income before income tax.

A) $280,000.

B) $245,000.

C) $200,000.

D) $255,200.

E) $290,200.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

55

On January 1, 2018, a subsidiary buys 12 percent of the outstanding voting stock of its parent corporation.The payment of $400,000 exceeded book value of the acquired shares by $80,000, attributable to a copyright with a 10-year useful life.During the year, the parent reported separate company income of $1,000,000 (excluding investment income from the subsidiary), and paid $120,000 in dividends.If the treasury stock approach is used, how is the Investment in Parent Stock reported in the consolidated balance sheet at December 31, 2018?

A) Consolidated stockholders' equity is reduced by $400,000.

B) Consolidated stockholders' equity is reduced by $320,000.

C) Included in current assets.

D) Included in noncurrent assets.

E) There is no effect on the consolidated balance sheet, because the effects have been eliminated.

A) Consolidated stockholders' equity is reduced by $400,000.

B) Consolidated stockholders' equity is reduced by $320,000.

C) Included in current assets.

D) Included in noncurrent assets.

E) There is no effect on the consolidated balance sheet, because the effects have been eliminated.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

56

On January 1, 2018, a subsidiary buys 8 percent of the outstanding voting stock of its parent corporation.The payment of $350,000 exceeded book value of the acquired shares by $50,000, attributable to a copyright with a 10-year useful life.During the year, the parent reported operating income of $675,000 (excluding investment income from the subsidiary), and paid $100,000 in dividends.If the treasury stock approach is used, how is the Investment in Parent Stock reported in the consolidated balance sheet at December 31, 2018?

A) Included in current assets.

B) Included in noncurrent assets.

C) Consolidated stockholders' equity is reduced by $350,000.

D) Consolidated stockholders' equity is reduced by $300,000.

E) There is no effect on the consolidated balance sheet, because the effects have been eliminated.

A) Included in current assets.

B) Included in noncurrent assets.

C) Consolidated stockholders' equity is reduced by $350,000.

D) Consolidated stockholders' equity is reduced by $300,000.

E) There is no effect on the consolidated balance sheet, because the effects have been eliminated.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

57

Why might a consolidated group file separate income tax returns?

A) There are no intra-entity transfers.

B) There are no deferred intra-entity gross profits in ending inventory.

C) One of the companies is a foreign company.

D) Parent owns 68 percent of one company and 82 percent of another.

E) All of these answer choices are correct.

A) There are no intra-entity transfers.

B) There are no deferred intra-entity gross profits in ending inventory.

C) One of the companies is a foreign company.

D) Parent owns 68 percent of one company and 82 percent of another.

E) All of these answer choices are correct.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

58

Which of the following statements is true concerning connecting affiliations and mutual ownerships?

A) In a mutual ownership, at least two companies in the consolidated group own portions of a third company.

B) There are at least four companies in a connecting affiliation.

C) In a connecting affiliation, at least one subsidiary owns stock in the parent company.

D) In a mutual ownership, the subsidiary owns a portion of the parent's stock.

E) There are only two companies in a connecting affiliation.

A) In a mutual ownership, at least two companies in the consolidated group own portions of a third company.

B) There are at least four companies in a connecting affiliation.

C) In a connecting affiliation, at least one subsidiary owns stock in the parent company.

D) In a mutual ownership, the subsidiary owns a portion of the parent's stock.

E) There are only two companies in a connecting affiliation.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

59

White Company owns 60% of Cody Company. Separate tax returns are required. For 2017, White's operating income (excluding taxes and any income from Cody) was $300,000 while Cody reported a pretax income of $125,000. During the period, Cody declared total dividends of $25,000; $15,000 (60%) to White and $10,000 to the noncontrolling interest. White declared dividends of $180,000. The income tax rate for both companies is 30%.

Compute Cody's undistributed earnings for 2018.

A) $ 62,500.

B) $125,000.

C) $ 87,500.

D) $100,000.

E) $ 70,000.

Compute Cody's undistributed earnings for 2018.

A) $ 62,500.

B) $125,000.

C) $ 87,500.

D) $100,000.

E) $ 70,000.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

60

Which of the following is not an advantage of filing a consolidated income tax return?

A) The existence of deferred losses in ending inventory.

B) The ability to use net operating losses of one company to offset profits of another company.

C) The existence of intra-entity gross profit remaining in ending inventory.

D) Transfers of inventory at a transfer price above cost.

E) There is no difference between U.S. GAAP and tax accounting rules for dividends paid to a parent by an 85%-owned subsidiary.

A) The existence of deferred losses in ending inventory.

B) The ability to use net operating losses of one company to offset profits of another company.

C) The existence of intra-entity gross profit remaining in ending inventory.

D) Transfers of inventory at a transfer price above cost.

E) There is no difference between U.S. GAAP and tax accounting rules for dividends paid to a parent by an 85%-owned subsidiary.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

61

Which of the following statements is true?

A) Alpha and Beta must file a consolidated income tax return, but must exclude Gamma from the consolidated return.

B) Alpha, Beta, and Gamma must file a consolidated income tax return.

C) Alpha, Beta, and Gamma must file separate income tax returns because the ownership of Beta is less than 100%.

D) Alpha, Beta, and Gamma will probably not file a consolidated income tax return.

E) Alpha, Beta, and Gamma may file separate income tax returns or a consolidated income tax return.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

62

What is Pi's accrual-based net income for 2018?

A) $152,000.

B) $ 16,000.

C) $192,000.

D) $200,000.

E) $208,000.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

63

Assuming that separate income tax returns are being filed, what deferred income tax asset is created?

A) $ 0.

B) $1,100.

C) $1,800.

D) $6,000.

E) $9,000.

A) $ 0.

B) $1,100.

C) $1,800.

D) $6,000.

E) $9,000.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

64

What is the net income attributable to the noncontrolling interest in Pi for 2018?

A) $ 0.

B) $ 9,600.

C) $10,000.

D) $19,200.

E) $20,000.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

65

Pear, Inc.owns 80 percent of Apple Corporation.During the current year, Apple reported operating income before tax of $400,000 and paid a dividend of $120,000.The income tax rate for each company is 40 percent and separate tax returns are prepared.What deferred income tax liability arising this year must be recognized in the consolidated balance sheet?

A) $ 0.

B) $ 7,680.

C) $17,920.

D) $38,400.

E) $51,200.

A) $ 0.

B) $ 7,680.

C) $17,920.

D) $38,400.

E) $51,200.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

66

What is Delta's accrual-based net income for 2018?

A) $1,091,520.

B) $1,115,520.

C) $1,168,000.

D) $1,168,520.

E) $1,200,000.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

67

What is Beta's accrual-based net income for 2018?

A) $200,000.

B) $276,800.

C) $280,000.

D) $296,000.

E) $300,000.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

68

Assuming that a consolidated income tax return is being filed, what deferred income tax asset is created?

A) $ 0.

B) $ 900.

C) $1,100.

D) $1,800.

E) $2,700.

A) $ 0.

B) $ 900.

C) $1,100.

D) $1,800.

E) $2,700.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

69

Reggie, Inc.owns 70 percent of Nancy Corporation.During the current year, Nancy reported operating income before tax of $100,000 and paid a dividend of $30,000.The income tax rate for both companies is 30 percent.What deferred income tax liability arising in the current year must be recognized in the consolidated balance sheet?

A) $1,680.

B) $2,400.

C) $1,470.

D) $9,800.

E) $2,940.

A) $1,680.

B) $2,400.

C) $1,470.

D) $9,800.

E) $2,940.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

70

What is Sigma's accrual-based income for 2018?

A) $400,000.

B) $592,000.

C) $540,000.

D) $572,800.

E) $600,000.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

71

What is the net income attributable to the noncontrolling interest in Sigma for 2018?

A) $55,240.

B) $56,420.

C) $57,280.

D) $59,420.

E) $60,000.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

72

What is the total net income attributable to the noncontrolling interest for 2018?

A) $55,240.

B) $66,020.

C) $67,280.

D) $76,280.

E) $76,480.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

73

What is Alpha's accrual-based net income for 2018?

A) $564,000.

B) $564,800.

C) $572,200.

D) $580,000.

E) $600,000.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

74

What is consolidated net income?

A) $229,500.

B) $237,000.

C) $245,000.

D) $232,500.

E) $240,000.

A) $229,500.

B) $237,000.

C) $245,000.

D) $232,500.

E) $240,000.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

75

What is Gamma's accrual-based net income for 2018?

A) $ 76,000.

B) $ 80,000.

C) $ 96,000.

D) $100,000.

E) $104,000.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

76

What is the total net income attributable to the noncontrolling interests for 2018?

A) $ 0.

B) $ 9,600.

C) $10,000.

D) $19,200.

E) $20,000.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

77

What is the net income attributable to the noncontrolling interest in Gamma for 2018?

A) $ 0.

B) $ 9,600.

C) $10,000.

D) $19,200.

E) $20,000.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

78

What will be reported as the net income attributable to the noncontrolling interest of Stance?

A) $6,500.

B) $8,000.

C) $9,000.

D) $7,500.

E) $1,000.

A) $6,500.

B) $8,000.

C) $9,000.

D) $7,500.

E) $1,000.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

79

What is net income attributable to the controlling interest of Paris?

A) $232,500.

B) $225,000.

C) $224,500.

D) $226,000.

E) $233,500.

A) $232,500.

B) $225,000.

C) $224,500.

D) $226,000.

E) $233,500.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

80