Deck 7: Accounting for Foreign Currency

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

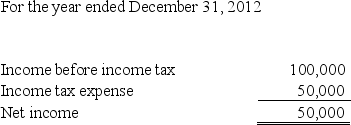

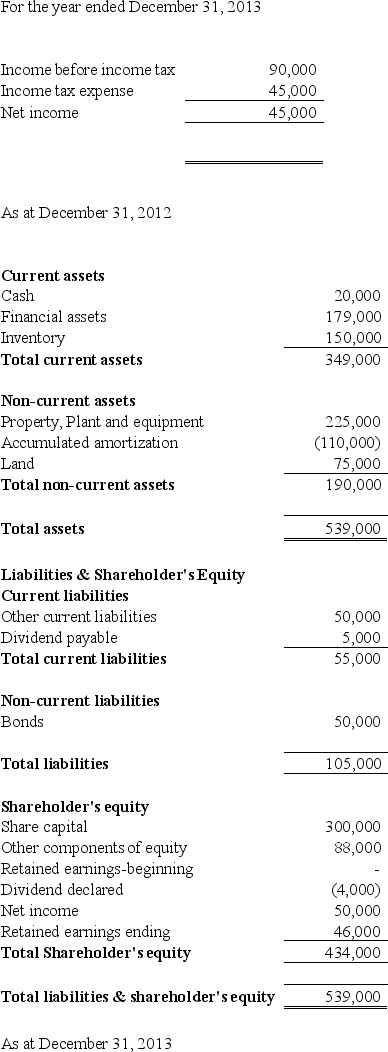

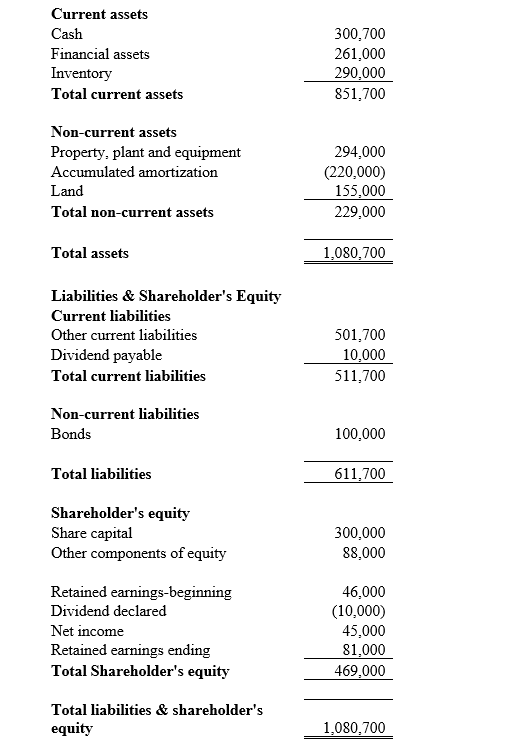

Mori Inc. is a company located in Canada and it uses the Canadian dollar as its functional currency. Mori Inc. began operations on January 1, 2012. Its shareholders are European. They would like the financial statements to be presented in Euros. The following is an excerpt from Mori Inc.'s financial statements for the 2012 and 2013 years. The changes in Other Comprehensive Income occurred evenly throughout the years. Dividends were declared at year-end.

The following exchange rates exist for the Euro relative to the Canadian dollar:

January 1, 2012 $1 Canadian = $1.40 Euro

December 31, 2012 $1 Canadian = $1.45 Euro

Average 2012 = $1 Canadian = $1.47 Euro

December 31, 2013 = $1 Canadian = $1.50 Euro

Average 2013 = $1 Canadian = $1.52 Euro

Required:

Translate the Mori Inc. financial statements as at December 31, 2013 from its functional currency to its presentation currency.

The following exchange rates exist for the Euro relative to the Canadian dollar:

January 1, 2012 $1 Canadian = $1.40 Euro

December 31, 2012 $1 Canadian = $1.45 Euro

Average 2012 = $1 Canadian = $1.47 Euro

December 31, 2013 = $1 Canadian = $1.50 Euro

Average 2013 = $1 Canadian = $1.52 Euro

Required:

Translate the Mori Inc. financial statements as at December 31, 2013 from its functional currency to its presentation currency.

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/57

Play

Full screen (f)

Deck 7: Accounting for Foreign Currency

1

Companies sometimes purchase derivative financial instruments to speculate on future foreign currency movements or to protect themselves from future fluctuations in currency rates.

True

2

Assets and liabilities (including comparatives)are translated at the spot rate at the date of the statement of financial position.

False

3

Non-monetary items are translated using the exchange rate at the balance sheet date. Any resulting foreign exchange gain or loss is recorded in other comprehensive income.

False

4

When a commercial transaction is denominated in another currency, foreign exchange gains and losses are realized.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

5

On March 1, 2013, Eddie Ltd. issued a purchase order to Liu Inc. to acquire a crane for $400,000 SGD. On the same day, Eddie entered into a forward contract to receive $400,000 SGD on July 31, 2013. The crane was delivered on June 1, 2013 and payment was made July 31, 2013. Eddie has an April 30 year-end. The following information has been provided: Assume that the transaction qualifies as a cash flow hedge. On March 1, at what amount should the forward contract be reported?

A)$312,400

B)$317,600

C)$0

D)$319,800

A)$312,400

B)$317,600

C)$0

D)$319,800

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

6

Which of the following statements about hedge accounting is TRUE?

A)Hedge accounting is mandatory.

B)Hedge accounting is applicable only if a receivable is being hedged.

C)Hedge accounting is optional.

D)Hedge accounting is applicable only if a liability is being hedged.

A)Hedge accounting is mandatory.

B)Hedge accounting is applicable only if a receivable is being hedged.

C)Hedge accounting is optional.

D)Hedge accounting is applicable only if a liability is being hedged.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

7

Functional currency is the currency in which the company conducts its primary business activity.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

8

In order to identify the foreign exchange component of a transaction, a company must establish the currency in which its books and records should be maintained.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

9

Where is the ineffective portion of a cash-flow hedge recognized on the financial statements?

A)As part of other comprehensive income.

B)As a separate component of equity.

C)It does not appear on the financial statements.

D)As part of net income.

A)As part of other comprehensive income.

B)As a separate component of equity.

C)It does not appear on the financial statements.

D)As part of net income.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

10

A transaction gain or loss at the settlement date is a change in the exchange rate quoted by a foreign exchange trader.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

11

The exchange rate in effect at the date of the transaction is called the spot exchange rate.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

12

Once a company's functional currency is identified, all transactions denominated in another currency are considered to be foreign currency transactions.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

13

Exchange gains and losses on accounts receivable/payable that are denominated in a foreign currency are deferred and reported upon settlement.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

14

When a company selects a presentation currency for its financial statements that is different than its functional currency, the statements must be translated into the functional currency.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

15

A derivative instrument cannot be a hedged item.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

16

Hedge accounting is applicable only if a receivable is being hedged.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

17

What is the effect of fluctuations in exchange rates on accounts payable?

A)Deferred and amortized.

B)Recognized immediately in income.

C)Recognized if losses, deferred if gains.

D)Deferred to maturity.

A)Deferred and amortized.

B)Recognized immediately in income.

C)Recognized if losses, deferred if gains.

D)Deferred to maturity.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

18

Exchange gains and losses on accounts receivable/payable that are denominated in a foreign currency are _______.

A)recognized in the periods in which exchange rates change.

B)deferred and reported upon settlement.

C)reported as adjustments to the transaction prices.

D)reported as equity adjustments from translation.

A)recognized in the periods in which exchange rates change.

B)deferred and reported upon settlement.

C)reported as adjustments to the transaction prices.

D)reported as equity adjustments from translation.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

19

The historical rate is the exchange rate at the beginning of the reporting period and the closing rate is the exchange rate at the end of the reporting period.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

20

Monetary items are translated using the exchange rate at the balance sheet date.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

21

On March 1, 2013, Chacin Ltd. issued a purchase order to No Worries (New Zealand)Inc. to acquire equipment for $400,000 New Zealand dollars. On the same day, Chacin entered into a forward contract to receive $400,000 New Zealand dollars on July 31, 2013. The equipment was delivered on June 1, 2013 and payment was made July 31, 2013. Chacin has an April 30 year-end. The following information has been provided: Assume that the transaction qualifies as a hedge. What is the cost of the hedge?

A)$4,960

B)$2,200

C)$4,640

D)$6,680

A)$4,960

B)$2,200

C)$4,640

D)$6,680

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

22

Which of the following is NOT one of the conditions that must be met to qualify for hedge accounting?

A)The effectiveness of the hedge can easily be determined.

B)The hedge relationship must be designated and documented.

C)The hedge is assessed at the beginning and at the end of the hedging period.

D)The hedge is expected to be effective.

A)The effectiveness of the hedge can easily be determined.

B)The hedge relationship must be designated and documented.

C)The hedge is assessed at the beginning and at the end of the hedging period.

D)The hedge is expected to be effective.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

23

Which of the following statements is TRUE?

A)The historical rate is the exchange rate at the date of the transaction and the closing rate is the exchange rate at the end of the reporting period.

B)The historical rate is the exchange rate at the beginning of the reporting period and the closing rate is the exchange rate at the end of the reporting period.

C)The historical rate is the exchange rate at the beginning of the reporting period and the forward rate is the exchange rate at the end of the reporting period.

D)The spot rate is the exchange rate at the date of the transaction and the closing rate is the exchange rate at the conclusion of a hedge instrument.

A)The historical rate is the exchange rate at the date of the transaction and the closing rate is the exchange rate at the end of the reporting period.

B)The historical rate is the exchange rate at the beginning of the reporting period and the closing rate is the exchange rate at the end of the reporting period.

C)The historical rate is the exchange rate at the beginning of the reporting period and the forward rate is the exchange rate at the end of the reporting period.

D)The spot rate is the exchange rate at the date of the transaction and the closing rate is the exchange rate at the conclusion of a hedge instrument.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

24

When a company selects a presentation currency for its financial statements that is different than its functional currency, the statements must be translated into the ____________ currency.

A)presentation

B)functional

C)transaction

D)foreign

A)presentation

B)functional

C)transaction

D)foreign

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

25

Using a _________ rate of exchange for all items appearing on the statement of financial position maintains the relationship in the retranslated financial statements (into the presentation currency)as that that existed in the foreign operation's financial statements (using the functional currency).

A)fluctuating

B)constant

C)spot

D)closing

A)fluctuating

B)constant

C)spot

D)closing

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

26

What is the exchange rate in effect at the date of the transaction called?

A)Forward rate.

B)Closing rate.

C)Settlement rate.

D)Spot rate.

A)Forward rate.

B)Closing rate.

C)Settlement rate.

D)Spot rate.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

27

A transaction gain or loss at the settlement date is:

A)A change in the exchange rate quoted by a foreign exchange trader.

B)Synonymous with the translation of foreign currency financial statements into dollars.

C)The difference between the recorded dollar amount of an account receivable denominated in a foreign currency and the amount of dollars received.

D)The difference between the buying and selling rate quoted by a foreign exchange trader at the settlement date.

A)A change in the exchange rate quoted by a foreign exchange trader.

B)Synonymous with the translation of foreign currency financial statements into dollars.

C)The difference between the recorded dollar amount of an account receivable denominated in a foreign currency and the amount of dollars received.

D)The difference between the buying and selling rate quoted by a foreign exchange trader at the settlement date.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

28

What is a currency swap an example of?

A)A futures contract.

B)A call option.

C)A forward contract.

D)A derivative instrument.

A)A futures contract.

B)A call option.

C)A forward contract.

D)A derivative instrument.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

29

Companies may operate in Canada, meaning that their offices are located in Canada, and their customers are Canadian. However, sometimes companies may decide they are willing to accept payment in a currency other than Canadian dollars. Which of the following statements is FALSE?

A)When a commercial transaction is denominated in another currency, foreign exchange gains and losses are realized.

B)When the books and records of a company are maintained in Canadian dollars, transactions that took place in another currency must be translated into Canadian dollars for inclusion into the records of the company.

C)When a Canadian seller decides to accept payment in Euros for its products, as a result of the accounting records being maintained in Canadian dollars, the Euros need to be converted into Canadian dollars.

D) When a Canadian seller decides to accept payment in Euros for its products, as a result of the accounting records being maintained in Canadian dollars, Euros will be converted to Canadian dollars using the average foreign exchange rate for the month.

A)When a commercial transaction is denominated in another currency, foreign exchange gains and losses are realized.

B)When the books and records of a company are maintained in Canadian dollars, transactions that took place in another currency must be translated into Canadian dollars for inclusion into the records of the company.

C)When a Canadian seller decides to accept payment in Euros for its products, as a result of the accounting records being maintained in Canadian dollars, the Euros need to be converted into Canadian dollars.

D) When a Canadian seller decides to accept payment in Euros for its products, as a result of the accounting records being maintained in Canadian dollars, Euros will be converted to Canadian dollars using the average foreign exchange rate for the month.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

30

On June 1, 2013, Donlands Canada Co. entered into a 90-day forward contract to sell $500,000 Singapore dollars (SGD)to its bank on August 29, 2013. The following information has been provided:

June 1, 90-day forward rate SGD$1 = $0.7750

July 1, 60-day forward rate SGD$1 = $0.7630

August 29, spot rate SGD$1 = $0.748

Donlands has a June 30 year-end. What is the exchange gain (loss)at June 30, 2013?

A)$(6,000)

B)$6,000

C)$0

D)$1,500

June 1, 90-day forward rate SGD$1 = $0.7750

July 1, 60-day forward rate SGD$1 = $0.7630

August 29, spot rate SGD$1 = $0.748

Donlands has a June 30 year-end. What is the exchange gain (loss)at June 30, 2013?

A)$(6,000)

B)$6,000

C)$0

D)$1,500

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

31

Which of the following items is a non-monetary item?

A)Accounts receivable.

B)Inventory.

C)Accounts payable.

D)Cash.

A)Accounts receivable.

B)Inventory.

C)Accounts payable.

D)Cash.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

32

At the balance sheet date, which of the following statements is TRUE?

A)Monetary items are translated using the exchange rate at the balance sheet date. Any resulting foreign exchange gain or loss is recorded in income.

B)Monetary items are translated using the exchange rate at the balance sheet date. Any resulting foreign exchange gain or loss is recorded in other comprehensive income.

C)Non-Monetary items are translated using the exchange rate at the balance sheet date. Any resulting foreign exchange gain or loss is recorded in income.

D)Non-Monetary items are translated using the exchange rate at the balance sheet date. Any resulting foreign exchange gain or loss is recorded in other comprehensive income.

A)Monetary items are translated using the exchange rate at the balance sheet date. Any resulting foreign exchange gain or loss is recorded in income.

B)Monetary items are translated using the exchange rate at the balance sheet date. Any resulting foreign exchange gain or loss is recorded in other comprehensive income.

C)Non-Monetary items are translated using the exchange rate at the balance sheet date. Any resulting foreign exchange gain or loss is recorded in income.

D)Non-Monetary items are translated using the exchange rate at the balance sheet date. Any resulting foreign exchange gain or loss is recorded in other comprehensive income.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

33

Under IFRS, which of the following statements is false regarding hedging?

A)Hedge accounting refers to a set of accounting rules that allow a company to smooth the impact of foreign currency fluctuations on income.

B)The gain or loss on a hedging instrument under a cash-flow hedge is first reported as other comprehensive income and then reclassified to income when the hedged item affects income.

C)The gain or loss on a hedging instrument under a cash-flow hedge is first reported as income.

D)Without the use of hedge accounting, an increased volatility on income would be realized resulting from a company's exposure to foreign currency risk.

A)Hedge accounting refers to a set of accounting rules that allow a company to smooth the impact of foreign currency fluctuations on income.

B)The gain or loss on a hedging instrument under a cash-flow hedge is first reported as other comprehensive income and then reclassified to income when the hedged item affects income.

C)The gain or loss on a hedging instrument under a cash-flow hedge is first reported as income.

D)Without the use of hedge accounting, an increased volatility on income would be realized resulting from a company's exposure to foreign currency risk.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

34

What exchange rate is usually used to report non-monetary assets on the statement of financial position?

A)Spot rate.

B)Closing rate.

C)Fair value.

D)Historical rate.

A)Spot rate.

B)Closing rate.

C)Fair value.

D)Historical rate.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

35

Which of the following typically cannot be a hedged item?

A)Derivative instrument.

B)Accounts receivable.

C)Accounts payable.

D)Purchase order.

A)Derivative instrument.

B)Accounts receivable.

C)Accounts payable.

D)Purchase order.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

36

On November 2, 2013, Choi Company purchased equipment for 100,000 Swiss francs (CHF)with payment requirement on March 30, 2014. To eliminate the risk of foreign exchange losses on this payable, Choi entered into a forward exchange contract on November 3, 2013 to receive CHF 100,000 at a forward rate of CHF1 = $2 on March 30, 2014. The spot rate was CHF1 = $1.95 on November 2, 2013 and CHF1 = $1.97 on December 1, 2013. How should the premium or discount on the forward exchange contract be accounted for if it is deemed to be a cash flow hedge?

A)It should be expensed on the maturity date of the forward exchange contract.

B)It should be expensed on the inception date of the forward exchange contract.

C)It should be expensed over the 5-month term of the forward exchange contract.

D)It should be added to the cost of the machine.

A)It should be expensed on the maturity date of the forward exchange contract.

B)It should be expensed on the inception date of the forward exchange contract.

C)It should be expensed over the 5-month term of the forward exchange contract.

D)It should be added to the cost of the machine.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

37

On November 2, 2013, Glasser Company purchased a machine for 100,000 Swiss francs (CHF)with payment requirement on March 30, 2014. To eliminate the risk of foreign exchange losses on this payable, Glasser entered into a forward exchange contract on November 3, 2013 to receive CHF 100,000 at a forward rate of CHF1 = $2 on March 30, 2014. The spot rate was CHF1 = $1.95 on November 2, 2013 and CHF1 = $1.97 on December 1, 2013. What is the amount of the premium or discount on the forward exchange contract?

A)A discount of $3,000.

B)A premium of $5,000.

C)A discount of $5,000.

D)A premium of $3,000.

A)A discount of $3,000.

B)A premium of $5,000.

C)A discount of $5,000.

D)A premium of $3,000.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

38

On January 1, 2012, Crawford Inc. issued 10,000,000 Euros (€)of bonds payable. The bonds are due on December 31, 2014. Over the life of the bonds, the exchange rates were as follows: What is the exchange gain (loss)recognized in income during 2014?

A)$(200,000)

B)$(800,000)

C)$ 800,000

D)$ 200,000

A)$(200,000)

B)$(800,000)

C)$ 800,000

D)$ 200,000

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

39

Donka Co. does a lot of business in Australia. It has numerous trade accounts receivables and accounts payables that are to be settled in Australian dollars. What type of hedge does Donka have?

A)Natural hedge.

B)Fair-value hedge.

C)Cash-flow hedge.

D)Hedge instrument.

A)Natural hedge.

B)Fair-value hedge.

C)Cash-flow hedge.

D)Hedge instrument.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

40

Which of the following statements regarding the translation of the financial statements into a presentation currency is FALSE?

A)Assets and liabilities (including comparatives)are translated at the average rate at the date of the statement of financial position.

B)Income and expenses (including comparatives)for each statement of comprehensive income presented are translated at exchange rates at the dates the transactions took place.

C)All resulting exchange differences are recognized in other comprehensive income.

D)For practical purposes, an average rate to approximate the actual exchange rate at the date of the transactions for income and expenses may be used as long as these items basically occur evenly over the period being presented.

A)Assets and liabilities (including comparatives)are translated at the average rate at the date of the statement of financial position.

B)Income and expenses (including comparatives)for each statement of comprehensive income presented are translated at exchange rates at the dates the transactions took place.

C)All resulting exchange differences are recognized in other comprehensive income.

D)For practical purposes, an average rate to approximate the actual exchange rate at the date of the transactions for income and expenses may be used as long as these items basically occur evenly over the period being presented.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

41

On January 1, 2012, Gupta Inc. issued 10,000,000 Euros (€)of bonds payable. The bonds are due on December 31, 2014. Over the life of the bonds, the exchange rates were as follows: What is the exchange gain (loss)recognized in income during 2013?

A)$(500,000)

B)$500,000

C)$1,000,000

D)$(1,000,000)

A)$(500,000)

B)$500,000

C)$1,000,000

D)$(1,000,000)

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

42

On December 1, 2013, Rollings Ltd. sold goods to Federer Ltd., a company located in Switzerland for 500,000 Swiss francs (CHF). At the date of sale, the spot rate was CHF1 = $1.0329. On the same date, Rollings acquired a 90-day forward contract at a rate of CHF1 = $1.0315. On March 1, 2014, Rollings receives full payment from Federer and delivered the Swiss francs in execution of the forward contract. The spot rate at March 1, 2014 was CHF1 = $1.0287. What amount should Rollings record for the sale?

A)$515,750

B)$500,000

C)$516,450

D)$514,350

A)$515,750

B)$500,000

C)$516,450

D)$514,350

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

43

Which of the following list would not be effective as a hedge for a Canadian company with a large number of transactions in Denmark?

A)Danish krone held by a Canadian bank.

B)A forward contract for the purchase of Danish krone.

C)A forward contract for the sale of Danish krone.

D)Canadian funds held by a Danish bank.

A)Danish krone held by a Canadian bank.

B)A forward contract for the purchase of Danish krone.

C)A forward contract for the sale of Danish krone.

D)Canadian funds held by a Danish bank.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

44

What is the purpose of derivative financial instruments? Provide some examples and explain how they work in practice.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

45

On June 1, 2013, Vandelay Co. entered into a 90-day forward contract to sell $1,000,000 Singapore dollars (USD)to its bank on August 29, 2013. The following information has been provided:

June 1, 90-day forward rate USD$1 = $0.9750

June 30, 60-day forward rate USD$1 = $0.9630

August 29, spot rate USD$1 = $0.948

Vandelay has a June 30 year-end. What is the exchange gain (loss)at June 30, 2013?

A)$(12,000)

B)$(27,000)

C)$(15,000)

D)$12,000

June 1, 90-day forward rate USD$1 = $0.9750

June 30, 60-day forward rate USD$1 = $0.9630

August 29, spot rate USD$1 = $0.948

Vandelay has a June 30 year-end. What is the exchange gain (loss)at June 30, 2013?

A)$(12,000)

B)$(27,000)

C)$(15,000)

D)$12,000

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

46

Under IFRS, which of the following statements about hedging a foreign currency risk of an accepted purchase order is TRUE?

A)It can be accounted for using either a fair-value hedge or a cash-flow hedge.

B)It is not eligible for hedge accounting until it becomes an accounts payable.

C)It must be accounted for using a fair-value hedge.

D)It must be accounted for using a cash-flow hedge.

A)It can be accounted for using either a fair-value hedge or a cash-flow hedge.

B)It is not eligible for hedge accounting until it becomes an accounts payable.

C)It must be accounted for using a fair-value hedge.

D)It must be accounted for using a cash-flow hedge.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

47

Once an entity's functional currency is identified, all transactions denominated in another currency are considered to be foreign currency transactions. What are some examples of foreign currency transactions?

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

48

Dante Ltd. manufactures and distributes transmissions to various companies in Europe. On April 2, 2013, Dante entered into a sales contract with a company in Germany to sell 1,000 transmissions. The contract price is €2,000 per transmission. Five hundred transmissions are to be delivered on June 30, 2013 and the remaining half is to be delivered on December 20, 2013. Payment is due in two instalments with half due on August 31, 2013 and the remaining half due January 30, 2014. However, the customer has the right to cancel the contract with 30 days' notice.

On April 2, 2013 Dante entered into a forward contract to hedge against the Euro exchange rate for €1 million coming due on January 31, 2014. Dante has a December 31 year end.

Delivery of the transmissions occurred on the dates specified and the company collected the receivables due and settled the forward contract January 30, 2014.

The exchange rates were as followed:

Required:

Assume that the forward contract is designated as a cash flow hedge since the sale is highly probable. Prepare the journal entries to record the sales and the hedge. Dante reports under IFRS.

On April 2, 2013 Dante entered into a forward contract to hedge against the Euro exchange rate for €1 million coming due on January 31, 2014. Dante has a December 31 year end.

Delivery of the transmissions occurred on the dates specified and the company collected the receivables due and settled the forward contract January 30, 2014.

The exchange rates were as followed:

Required:

Assume that the forward contract is designated as a cash flow hedge since the sale is highly probable. Prepare the journal entries to record the sales and the hedge. Dante reports under IFRS.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

49

Which of the following statements regarding the translation of financial statements from the "functional currency" to the "presentation currency" is FALSE?

A)Entities may choose to present their financial statements in any currency.

B)Given the rising trend towards globalization, management may like to present their financial statements in a currency different from their functional currency in order to attract investors or because it is required by local law or other regulation.

C)A company may display its statements in a language more relatable to a global marketplace used to viewing financial information denominated in a currency not functional to the entity.

D)Any gain or loss on translation is considered part of income.

A)Entities may choose to present their financial statements in any currency.

B)Given the rising trend towards globalization, management may like to present their financial statements in a currency different from their functional currency in order to attract investors or because it is required by local law or other regulation.

C)A company may display its statements in a language more relatable to a global marketplace used to viewing financial information denominated in a currency not functional to the entity.

D)Any gain or loss on translation is considered part of income.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

50

Upon translation, assets and liabilities are translated at the _________ rate at the presentation date and income statement items are translated using the _______ rate for the period.

A)average; closing

B)closing; average

C) forward; closing

D)spot; average.

A)average; closing

B)closing; average

C) forward; closing

D)spot; average.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

51

A transaction loss would result from

A)an increase in the foreign exchange rate in relation to the Canadian rate applicable to an asset denominated in a foreign currency.

B)a decrease in the foreign exchange rate in relation to the Canadian rate applicable to a liability denominated in a foreign currency.

C)the import of merchandise when the transaction is denominated in a foreign currency.

D)a decrease in the foreign exchange rate in relation to the Canadian rate applicable to an asset denominated in a foreign currency.

A)an increase in the foreign exchange rate in relation to the Canadian rate applicable to an asset denominated in a foreign currency.

B)a decrease in the foreign exchange rate in relation to the Canadian rate applicable to a liability denominated in a foreign currency.

C)the import of merchandise when the transaction is denominated in a foreign currency.

D)a decrease in the foreign exchange rate in relation to the Canadian rate applicable to an asset denominated in a foreign currency.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

52

Bommarito Corp., a Swiss firm, bought merchandise from Trilis Company of New Brunswick on December 15, 2013 for 20,000 CHF payable on January 14, 2014. Trilis and Bommarito both close their books on December 31. The 20,000 CHF was paid on January 14, 2014. The exchange rates for CHF were:

December 15,2013 spot

December 15,2013 30 day forward

December

December 31,2013 14 day forward

January Required:

A)Provide the journal entries for Bommarito (the buyer)at each of the above dates, as required.

B)Provide the journal entries for Trilis Company (the seller)at each of the above dates as required.

December 15,2013 spot

December 15,2013 30 day forward

December

December 31,2013 14 day forward

January Required:

A)Provide the journal entries for Bommarito (the buyer)at each of the above dates, as required.

B)Provide the journal entries for Trilis Company (the seller)at each of the above dates as required.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

53

How does a company establish the currency in which its books and records should be maintained?

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

54

Which of the following statements regarding functional currency is FALSE?

A)Functional currency is the currency in which the company conducts its primary business activity.

B)Foreign currency exists when a company transacts in a currency other than its functional currency.

C)The currency of the country in which an entity normally operates is its functional currency.

D)Functional currency must be determined first before foreign currency transactions can be identified.

A)Functional currency is the currency in which the company conducts its primary business activity.

B)Foreign currency exists when a company transacts in a currency other than its functional currency.

C)The currency of the country in which an entity normally operates is its functional currency.

D)Functional currency must be determined first before foreign currency transactions can be identified.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

55

Mori Inc. is a company located in Canada and it uses the Canadian dollar as its functional currency. Mori Inc. began operations on January 1, 2012. Its shareholders are European. They would like the financial statements to be presented in Euros. The following is an excerpt from Mori Inc.'s financial statements for the 2012 and 2013 years. The changes in Other Comprehensive Income occurred evenly throughout the years. Dividends were declared at year-end.

The following exchange rates exist for the Euro relative to the Canadian dollar:

January 1, 2012 $1 Canadian = $1.40 Euro

December 31, 2012 $1 Canadian = $1.45 Euro

Average 2012 = $1 Canadian = $1.47 Euro

December 31, 2013 = $1 Canadian = $1.50 Euro

Average 2013 = $1 Canadian = $1.52 Euro

Required:

Translate the Mori Inc. financial statements as at December 31, 2013 from its functional currency to its presentation currency.

The following exchange rates exist for the Euro relative to the Canadian dollar:

January 1, 2012 $1 Canadian = $1.40 Euro

December 31, 2012 $1 Canadian = $1.45 Euro

Average 2012 = $1 Canadian = $1.47 Euro

December 31, 2013 = $1 Canadian = $1.50 Euro

Average 2013 = $1 Canadian = $1.52 Euro

Required:

Translate the Mori Inc. financial statements as at December 31, 2013 from its functional currency to its presentation currency.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

56

What are the steps involved in the translation of the financial statements into a presentation currency?

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

57

In order to identify the foreign exchange component of a transaction, a company must establish the currency in which its books and records should be maintained. This is the ___________________________

A)domestic currency.

B)currency of the primary economic environment in which a company operates.

C)foreign currency.

D)translation currency.

A)domestic currency.

B)currency of the primary economic environment in which a company operates.

C)foreign currency.

D)translation currency.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 57 flashcards in this deck.