Deck 4: Intra-Group Transactions

Full screen (f)

Question

Question

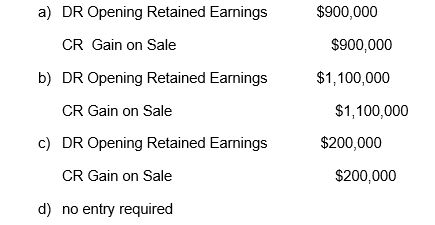

Assuming the same facts as for Question 12 but that 2 years later S sold the land outside the group for $1,200,000 the consolidation journal entry required would be (ignoring tax effects):

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

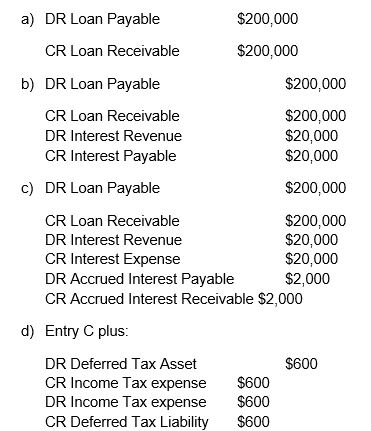

P Ltd lends $200,000 to its subsidiary S Ltd.At the end of the year S Ltd has paid interest of $18,000 and owes a further $2,000 (assume a tax rate of 30%)The required consolidation entry is:

Question

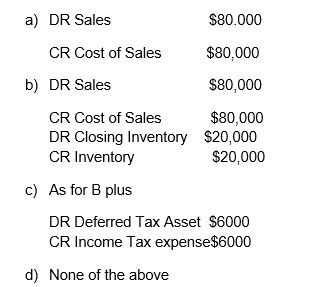

P Ltd sells inventory to its subsidiary S Ltd on the following basis: cost to P $60,000,sale price to S $80,000.All inventory is held by S at the end of the financial year (assume a tax rate of 30%).The periodic method is used to account for inventory.Therefore,the following consolidation entries are required:

Question

Question

Question

Question

Question

Question

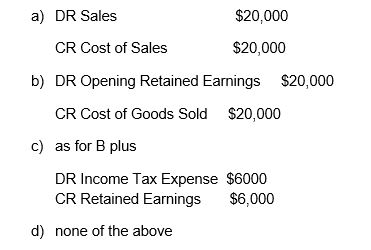

Using the same data as for question 9 what would be the consolidation entry required for the next financial year (assuming S sold all the inventory during the next year)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/36

Play

Full screen (f)

Deck 4: Intra-Group Transactions

1

A consolidation adjustment will have a tax effect if:

A) it adjusts the carrying amount of an asset

B) it adjusts the carrying amount of a liability

C) it recognises assets and liabilities not recorded in accounting records of group companies

D) all of the above

A) it adjusts the carrying amount of an asset

B) it adjusts the carrying amount of a liability

C) it recognises assets and liabilities not recorded in accounting records of group companies

D) all of the above

D

2

Assuming the same facts as for Question 12 but that 2 years later S sold the land outside the group for $1,200,000 the consolidation journal entry required would be (ignoring tax effects):

A

3

A parent company owns 80% of the issued capital of its subsidiary.On consolidation a sale of inventories between parent and subsidiary will be eliminated as follows:

A) 20% of sale amount

B) 80% of sale amount

C) 100% of sale amount

D) not eliminated

A) 20% of sale amount

B) 80% of sale amount

C) 100% of sale amount

D) not eliminated

C

4

A Ltd sells inventory to its parent P Ltd for $60,000 representing a mark up of 50% on cost.At year end 3/4 of the goods are still held by P Ltd.The unrealised profit to be eliminated on consolidation is:

A) $20,000

B) $15,000

C) $30,000

D) $10,000

A) $20,000

B) $15,000

C) $30,000

D) $10,000

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

5

Dividends paid by the parent company and all subsidiaries will be eliminated as consolidation adjustments

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

6

P Ltd sold an item of property plant and equipment to its subsidiary S Ltd on the following basis: cost to P Ltd $24,000.The equipment is 3 years old and had been depreciated at 10% per annum straight line.Sale Price was $20,000.The gain recorded by P Ltd on sale would be:

A) $20,000

B) $4,000

C) $3,200

D) nil

A) $20,000

B) $4,000

C) $3,200

D) nil

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

7

Using the same facts as Question 14 but assuming that S will depreciate the asset over its remaining estimated useful life of 8 years.What is the depreciation expense adjustment required on consolidation I year after the intra group sale?

A) CR $400

B) DR $400

C) CR $2,100

D) CR $2,500

A) CR $400

B) DR $400

C) CR $2,100

D) CR $2,500

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

8

Which of the following accounts cannot be altered by a consolidation adjusting entry:

A) income tax expense

B) income tax payable

C) deferred tax asset

D) deferred tax asset

A) income tax expense

B) income tax payable

C) deferred tax asset

D) deferred tax asset

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

9

P Ltd acquired inventories for $150,000 which were sold to its subsidiary S Ltd for $120,000 (assume a tax rate of 30%)On consolidation a deferred tax liability would be recorded for:

A) $45,000

B) $36,000

C) $9,000

D) Not recorded

A) $45,000

B) $36,000

C) $9,000

D) Not recorded

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

10

Unrealised profits on intra-group sale of inventories arise if:

A) the sale is an upstream transaction

B) the sale is a downstream transaction

C) the inventories are held within the group at date of consolidation

D) none of the above

A) the sale is an upstream transaction

B) the sale is a downstream transaction

C) the inventories are held within the group at date of consolidation

D) none of the above

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

11

Consolidation entries never adjust cash because intra-group transactions do not alter the group's cash position

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

12

P Ltd lends $200,000 to its subsidiary S Ltd.At the end of the year S Ltd has paid interest of $18,000 and owes a further $2,000 (assume a tax rate of 30%)The required consolidation entry is:

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

13

P Ltd sells inventory to its subsidiary S Ltd on the following basis: cost to P $60,000,sale price to S $80,000.All inventory is held by S at the end of the financial year (assume a tax rate of 30%).The periodic method is used to account for inventory.Therefore,the following consolidation entries are required:

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

14

P Ltd provides management services to its subsidiary company S Ltd for $100,000 per year.At the end of the current year S Ltd owes $20,000 of this fee.The entry required on consolidation is:

A) DR Management Fee Revenue $100,000 CR Management Fee Expense $100,000

B) DR Management Fee Revenue $100,000 CR Management Fee Expense $100,000

DR Accrued Fees Payable $20,000

CR Accrued Fees Receivable $20,000

C) DR Management Fees Revenue $80,000 CR Management Fees Expense $80,000

D) None of the above

A) DR Management Fee Revenue $100,000 CR Management Fee Expense $100,000

B) DR Management Fee Revenue $100,000 CR Management Fee Expense $100,000

DR Accrued Fees Payable $20,000

CR Accrued Fees Receivable $20,000

C) DR Management Fees Revenue $80,000 CR Management Fees Expense $80,000

D) None of the above

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

15

For assets valued using the revaluation model consolidation adjustment will be required :

A) when there is a revaluation increment

B) when there is a revaluation decrement

C) for both a revaluation increment and decrement

D) no adjustment required

A) when there is a revaluation increment

B) when there is a revaluation decrement

C) for both a revaluation increment and decrement

D) no adjustment required

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

16

S Ltd acquired land from its parent company P Ltd for $1,000,000 The land had originally cost P Ltd $100,000 (assume a tax rate of 30%)On consolidation the deferred tax asset will be recorded at:

A) $300,000

B) $30,000

C) $270,000

D) not recorded

A) $300,000

B) $30,000

C) $270,000

D) not recorded

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

17

An impairment loss will be recognised in the group accounts when non current assets are sold at a loss on an intra-group basis when:

A) value in use is greater than carrying amount

B) value in use is less than carrying amount

C) value in use is greater than sale price

D) value in use is less than sale price

A) value in use is greater than carrying amount

B) value in use is less than carrying amount

C) value in use is greater than sale price

D) value in use is less than sale price

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

18

Tax effect adjustments only apply to consolidation adjusting entries which affect the carrying amount of parent subsidiaries

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

19

Using the same data as for question 9 what would be the consolidation entry required for the next financial year (assuming S sold all the inventory during the next year)

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

20

A subsidiary which is 75% owned by its parent company pays a dividend of $100,000.On consolidation the amount to be eliminated is:

A) $75,000

B) $100,000

C) $25,000

D) Not eliminated

A) $75,000

B) $100,000

C) $25,000

D) Not eliminated

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

21

Unrealised gains and losses on intra-group sales of non-depreciable assets can only be realised by sale outside the group.

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

22

Explain why it is necessary to adjust unrealised profit in opening inventory on consolidation

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

23

Where a parent entity sells inventories to a subsidiary this is called an 'upstream' sale

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

24

When a depreciable asset is sold at a profit on an intra-group basis,a consolidation entry is required to recognise a deferred tax asset

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

25

Explain why cash will never be adjusted in consolidation journal entries

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

26

Explain why temporary differences (and therefore deferred tax adjustments)arise when depreciable assets are sold at a profit on an intra-group basis.

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

27

Deferred tax assets and liabilities arising from accrual of intra-group interest on loans should be offset as a consolidation adjustment

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

28

Where service fees are accrued by group members there is no tax effect on consolidation

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

29

Discuss the basis of recognition of tax effects relating to accrued revenue and expenses for such intra-group items as management fees and interest

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

30

The useful life of a depreciable asset can not change subsequent to an intra-group sale of the asset

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

31

Current accounting regulations require the separate disclosures in profit or loss of gains and losses on disposal of non current assets

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

32

A loss on intra-group sales of inventory will be regarded as realised by the group at the time of the sale only if the transfer price represents the net realisable value of the inventories

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

33

Explain why some consolidation adjusting entries are required to be carried forward to future years.

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

34

Unrealised profits on the intra-group sale of inventory will only be eliminated on consolidation in the year in which they arise

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

35

For non current assets measured using the revaluation model no consolidation adjustment is required for fair value increases or decreases.

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

36

Unrealised gains on the intra-group sale of depreciable assets are realised via depreciation charges over the remaining useful life of the asset

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 36 flashcards in this deck.