Deck 7: Consolidated Cash Flow Statements

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

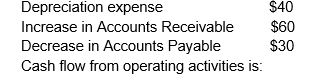

A company records a net profit of $220 for the year.Other information for the year:

A) $260

B) $330

C) $270

D) $170

A) $260

B) $330

C) $270

D) $170

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/25

Play

Full screen (f)

Deck 7: Consolidated Cash Flow Statements

1

A company has total sales revenue of $600,000 for a period.The balance of Accounts Receivable was $200,000 at the start of the year and $220,000 at the end of the year.Cash sales amounted to $50,000.Receipts from customers is:

A) $600,000

B) $530,000

C) $550,000

D) $580,000

A) $600,000

B) $530,000

C) $550,000

D) $580,000

D

2

The following items must be separately disclosed in a statement of cash flows:

A) interest paid and received

B) dividends paid and received

C) Both A and B

D) No separate disclosure required

A) interest paid and received

B) dividends paid and received

C) Both A and B

D) No separate disclosure required

C

3

Cash payments to buy back shares will be classified as:

A) cash flow from operating activities

B) cash flow from investing activities

C) cash flow from financing activities

D) none of the above

A) cash flow from operating activities

B) cash flow from investing activities

C) cash flow from financing activities

D) none of the above

C

4

A company holds $100,000 in a term deposit account as an interest-generating investment.For purposes of the statement of cash flows the term deposit will be classified as:

A) cash equivalent

B) investment

C) either cash equivalent or investment

D) none of the above

A) cash equivalent

B) investment

C) either cash equivalent or investment

D) none of the above

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

5

A company calculates its cash flows from operating activities as profit +/- accruals.This is:

A) the direct method

B) the indirect method

C) neither the direct or the indirect method

D) none of the above

A) the direct method

B) the indirect method

C) neither the direct or the indirect method

D) none of the above

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

6

The classification of an item as a cash equivalent means that changes in the balance:

A) will be disclosed in the statement of cash flows

B) will not be disclosed in the statement of cash flows

C) may be disclosed at discretion of the entity

D) none of the above

A) will be disclosed in the statement of cash flows

B) will not be disclosed in the statement of cash flows

C) may be disclosed at discretion of the entity

D) none of the above

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

7

Assets owned by a subsidiary acquired during the year are treated as negative financing cash flows in a consolidated statement of cash flows

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

8

A statement of cash flows can be prepared using:

A) reconstruction of ledgers approach

B) formula approach

C) spreadsheet approach

D) all of the above

A) reconstruction of ledgers approach

B) formula approach

C) spreadsheet approach

D) all of the above

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

9

The purpose of holding a cash equivalent is irrelevant for the classification in the statement of cash flows

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

10

Insurance proceeds from the destruction of a factory by fire would be classified as:

A) operating cash flow

B) financing cash flow

C) investing cash flow

D) none of the above

A) operating cash flow

B) financing cash flow

C) investing cash flow

D) none of the above

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

11

A reconciliation of profit and cash flows is required using either the direct or indirect method of disclosing cash flows from operations

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

12

A Ltd acquires 100% of shares of B Ltd for $195,000,financed by an issue of 100,000 x $1.50 shares and $45,000 cash.B Ltd has cash balances of $35,000 at the date of acquisition.A Ltd will record the following in its consolidated statement of cash flows:

A) cash flow from investing ($195,000)

B) cash flow from investing ($450,000)

C) cash flow from investing ($10,000)

D) cash flow from investing ($35,000)

A) cash flow from investing ($195,000)

B) cash flow from investing ($450,000)

C) cash flow from investing ($10,000)

D) cash flow from investing ($35,000)

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

13

A company records a net profit of $220 for the year.Other information for the year:

A) $260

B) $330

C) $270

D) $170

A) $260

B) $330

C) $270

D) $170

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

14

The time to maturity is relevant in the classification of cash equivalents

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

15

Cash flows from operating activities is the default classification in a statement of cash flows

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

16

The issue of shares to purchase non current assets will be disclosed:

A) as a financing activity

B) as an investment activity

C) as both a financing and investment activity

D) in the note disclosure to the statement of cash flows

A) as a financing activity

B) as an investment activity

C) as both a financing and investment activity

D) in the note disclosure to the statement of cash flows

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

17

Cash flows from operating activities can be calculated using:

A) the direct method

B) the indirect method

C) either the direct or indirect method

D) none of the above

A) the direct method

B) the indirect method

C) either the direct or indirect method

D) none of the above

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

18

The carrying amount of property plant and equipment is $1,000 at the start of the year and $1,400 at the end of the year.During the year the following occurred: Sale of equipment - carrying amount $40

Acquisition of equipment - financed by share issue $200

Depreciation expense for year $120.

Investing cash flow is:

A) ($400)

B) ($200)

C) ($160)

D) ($360)

Acquisition of equipment - financed by share issue $200

Depreciation expense for year $120.

Investing cash flow is:

A) ($400)

B) ($200)

C) ($160)

D) ($360)

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

19

AASB 107 requires the use of the direct method of calculating cash flows from operating activities.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

20

Accounting Standard AASB 107 Statement of Cash Flows mandates the provision of cash flow information from operating,financing and investing activities.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

21

Discuss the basis of classifying cash flows arising from interest paid.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

22

Discuss why Australia moved from a requirement to prepare a statement of sources and application of funds to a statement of cash flows.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

23

Discuss the treatment of subsidiaries acquired and disposed of in the consolidated statement of cash flows.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

24

In preparing a consolidated statement of cash flows what items can be shown on a net cash flow basis?

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

25

Why is cash flow from operating activities seen as a performance measure?

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 25 flashcards in this deck.