Deck 10: Translation and Consolidation of Foreign Currency Financial Statements

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

The following data relate to Questions 18-22:

During the year ended June 30 20X7, Johnson Ltd became deeply involved in trade with Malaysia. On July 1 20X6, the company acquired 50% of the share capital of a Malaysian palm oil producer, Plantations Berhad, for $7,000,000. For the year ended June 30 20X7, the following balance sheet and income statement were prepared by Plantations Berhad (amounts in thousands):

Income Statement for the Year ended June 30 20X7

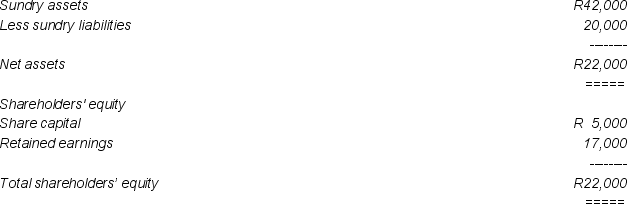

Balance Sheet as at June 30 20X7

Balance Sheet as at June 30 20X7

Statement of the Movement in Retained Earnings in the Year ended June 30 20X7

Statement of the Movement in Retained Earnings in the Year ended June 30 20X7

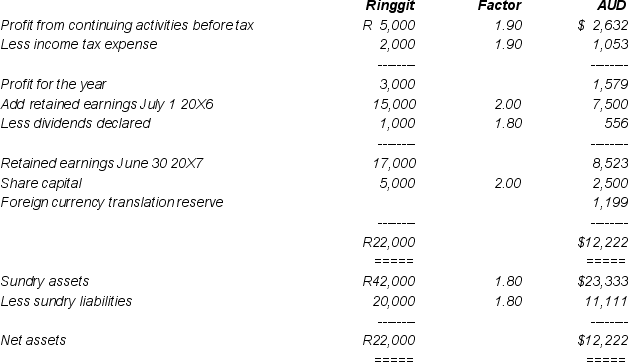

The functional currency of Plantations Berhad was Malaysian Ringgit. The following translation statement was prepared for the company (amounts in thousands):

The functional currency of Plantations Berhad was Malaysian Ringgit. The following translation statement was prepared for the company (amounts in thousands):

Additional information:

Additional information:

a) A deferred tax liability of 30% of the foreign currency translation reserve is to be recognised.

b) On July 1 20X6, as a partial hedge against its investment in Plantations Berhad, Johnson Ltd took out a three (3) year loan of R 8,000,000 from the Bank Negara at 12% interest, with interest payable quarterly commencing September 30 20X6.

c) On May 15 20X7 Johnson Ltd placed an order for R 2,000,000 in merchandise for resale from Malaysian Industries Berhad, payable in USD. The goods were shipped FOB on May 31 with settlement due on July 31 20X7.

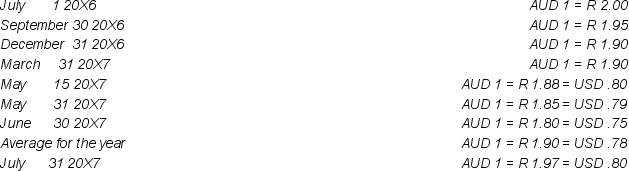

At relevant dates the exchange rates were:

The presentation currency and functional currency of Johnson Ltd was:

A) Malaysian ringgit and Australian dollars respectively.

B) Australian dollars and Australian dollars respectively.

C) Australian dollars and Malaysian ringgit respectively.

D) Malaysian ringgit and Malaysian ringgit respectively.

During the year ended June 30 20X7, Johnson Ltd became deeply involved in trade with Malaysia. On July 1 20X6, the company acquired 50% of the share capital of a Malaysian palm oil producer, Plantations Berhad, for $7,000,000. For the year ended June 30 20X7, the following balance sheet and income statement were prepared by Plantations Berhad (amounts in thousands):

Income Statement for the Year ended June 30 20X7

Balance Sheet as at June 30 20X7 Statement of the Movement in Retained Earnings in the Year ended June 30 20X7 The functional currency of Plantations Berhad was Malaysian Ringgit. The following translation statement was prepared for the company (amounts in thousands): Additional information:a) A deferred tax liability of 30% of the foreign currency translation reserve is to be recognised.

b) On July 1 20X6, as a partial hedge against its investment in Plantations Berhad, Johnson Ltd took out a three (3) year loan of R 8,000,000 from the Bank Negara at 12% interest, with interest payable quarterly commencing September 30 20X6.

c) On May 15 20X7 Johnson Ltd placed an order for R 2,000,000 in merchandise for resale from Malaysian Industries Berhad, payable in USD. The goods were shipped FOB on May 31 with settlement due on July 31 20X7.

At relevant dates the exchange rates were:

The presentation currency and functional currency of Johnson Ltd was:

A) Malaysian ringgit and Australian dollars respectively.

B) Australian dollars and Australian dollars respectively.

C) Australian dollars and Malaysian ringgit respectively.

D) Malaysian ringgit and Malaysian ringgit respectively.

Question

The following data relate to Questions 18-22:

During the year ended June 30 20X7, Johnson Ltd became deeply involved in trade with Malaysia. On July 1 20X6, the company acquired 50% of the share capital of a Malaysian palm oil producer, Plantations Berhad, for $7,000,000. For the year ended June 30 20X7, the following balance sheet and income statement were prepared by Plantations Berhad (amounts in thousands):

Income Statement for the Year ended June 30 20X7

Balance Sheet as at June 30 20X7

Statement of the Movement in Retained Earnings in the Year ended June 30 20X7

The functional currency of Plantations Berhad was Malaysian Ringgit. The following translation statement was prepared for the company (amounts in thousands):

Additional information:

a) A deferred tax liability of 30% of the foreign currency translation reserve is to be recognised.

b) On July 1 20X6, as a partial hedge against its investment in Plantations Berhad, Johnson Ltd took out a three (3) year loan of R 8,000,000 from the Bank Negara at 12% interest, with interest payable quarterly commencing September 30 20X6.

c) On May 15 20X7 Johnson Ltd placed an order for R 2,000,000 in merchandise for resale from Malaysian Industries Berhad, payable in USD. The goods were shipped FOB on May 31 with settlement due on July 31 20X7.

At relevant dates the exchange rates were:

In the consolidated balance sheet at June 30 20X7 of the group controlled by Johnson Ltd,the foreign currency translation reserve attributable to the members the parent entity would be (rounded to the nearest thousand dollars):

A) $311,111

B) $839,300

C) $108,538

D) None of the above.

During the year ended June 30 20X7, Johnson Ltd became deeply involved in trade with Malaysia. On July 1 20X6, the company acquired 50% of the share capital of a Malaysian palm oil producer, Plantations Berhad, for $7,000,000. For the year ended June 30 20X7, the following balance sheet and income statement were prepared by Plantations Berhad (amounts in thousands):

Income Statement for the Year ended June 30 20X7

Balance Sheet as at June 30 20X7 Statement of the Movement in Retained Earnings in the Year ended June 30 20X7 The functional currency of Plantations Berhad was Malaysian Ringgit. The following translation statement was prepared for the company (amounts in thousands): Additional information:a) A deferred tax liability of 30% of the foreign currency translation reserve is to be recognised.

b) On July 1 20X6, as a partial hedge against its investment in Plantations Berhad, Johnson Ltd took out a three (3) year loan of R 8,000,000 from the Bank Negara at 12% interest, with interest payable quarterly commencing September 30 20X6.

c) On May 15 20X7 Johnson Ltd placed an order for R 2,000,000 in merchandise for resale from Malaysian Industries Berhad, payable in USD. The goods were shipped FOB on May 31 with settlement due on July 31 20X7.

At relevant dates the exchange rates were:

In the consolidated balance sheet at June 30 20X7 of the group controlled by Johnson Ltd,the foreign currency translation reserve attributable to the members the parent entity would be (rounded to the nearest thousand dollars):

A) $311,111

B) $839,300

C) $108,538

D) None of the above.

Question

Question

Question

Question

The following data relate to Questions 18-22:

During the year ended June 30 20X7, Johnson Ltd became deeply involved in trade with Malaysia. On July 1 20X6, the company acquired 50% of the share capital of a Malaysian palm oil producer, Plantations Berhad, for $7,000,000. For the year ended June 30 20X7, the following balance sheet and income statement were prepared by Plantations Berhad (amounts in thousands):

Income Statement for the Year ended June 30 20X7

Balance Sheet as at June 30 20X7

Statement of the Movement in Retained Earnings in the Year ended June 30 20X7

The functional currency of Plantations Berhad was Malaysian Ringgit. The following translation statement was prepared for the company (amounts in thousands):

Additional information:

a) A deferred tax liability of 30% of the foreign currency translation reserve is to be recognised.

b) On July 1 20X6, as a partial hedge against its investment in Plantations Berhad, Johnson Ltd took out a three (3) year loan of R 8,000,000 from the Bank Negara at 12% interest, with interest payable quarterly commencing September 30 20X6.

c) On May 15 20X7 Johnson Ltd placed an order for R 2,000,000 in merchandise for resale from Malaysian Industries Berhad, payable in USD. The goods were shipped FOB on May 31 with settlement due on July 31 20X7.

At relevant dates the exchange rates were:

In the separate income statement of Johnson Ltd for the year ended June 30 20X7,the translation gain or loss arising on the loan from the Bank Negara was (rounded to the nearest thousand dollars):

A) A translation gain of $311,111

B) A translation loss of $444,000

C) A translation loss of $600,000

D) Nil, since any loss is initially recognised in equity.

During the year ended June 30 20X7, Johnson Ltd became deeply involved in trade with Malaysia. On July 1 20X6, the company acquired 50% of the share capital of a Malaysian palm oil producer, Plantations Berhad, for $7,000,000. For the year ended June 30 20X7, the following balance sheet and income statement were prepared by Plantations Berhad (amounts in thousands):

Income Statement for the Year ended June 30 20X7

Balance Sheet as at June 30 20X7 Statement of the Movement in Retained Earnings in the Year ended June 30 20X7 The functional currency of Plantations Berhad was Malaysian Ringgit. The following translation statement was prepared for the company (amounts in thousands): Additional information:a) A deferred tax liability of 30% of the foreign currency translation reserve is to be recognised.

b) On July 1 20X6, as a partial hedge against its investment in Plantations Berhad, Johnson Ltd took out a three (3) year loan of R 8,000,000 from the Bank Negara at 12% interest, with interest payable quarterly commencing September 30 20X6.

c) On May 15 20X7 Johnson Ltd placed an order for R 2,000,000 in merchandise for resale from Malaysian Industries Berhad, payable in USD. The goods were shipped FOB on May 31 with settlement due on July 31 20X7.

At relevant dates the exchange rates were:

In the separate income statement of Johnson Ltd for the year ended June 30 20X7,the translation gain or loss arising on the loan from the Bank Negara was (rounded to the nearest thousand dollars):

A) A translation gain of $311,111

B) A translation loss of $444,000

C) A translation loss of $600,000

D) Nil, since any loss is initially recognised in equity.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

The following data relate to Questions 18-22:

During the year ended June 30 20X7, Johnson Ltd became deeply involved in trade with Malaysia. On July 1 20X6, the company acquired 50% of the share capital of a Malaysian palm oil producer, Plantations Berhad, for $7,000,000. For the year ended June 30 20X7, the following balance sheet and income statement were prepared by Plantations Berhad (amounts in thousands):

Income Statement for the Year ended June 30 20X7

Balance Sheet as at June 30 20X7

Statement of the Movement in Retained Earnings in the Year ended June 30 20X7

The functional currency of Plantations Berhad was Malaysian Ringgit. The following translation statement was prepared for the company (amounts in thousands):

Additional information:

a) A deferred tax liability of 30% of the foreign currency translation reserve is to be recognised.

b) On July 1 20X6, as a partial hedge against its investment in Plantations Berhad, Johnson Ltd took out a three (3) year loan of R 8,000,000 from the Bank Negara at 12% interest, with interest payable quarterly commencing September 30 20X6.

c) On May 15 20X7 Johnson Ltd placed an order for R 2,000,000 in merchandise for resale from Malaysian Industries Berhad, payable in USD. The goods were shipped FOB on May 31 with settlement due on July 31 20X7.

At relevant dates the exchange rates were:

The transaction involving the purchase of the merchandise inventory from Malaysian Industries Berhad is:

A) A foreign currency transaction from the viewpoints of both Johnson Ltd and Malaysian Industries Berhad.

B) A foreign currency transaction from the viewpoint of Johnson Ltd, but not a foreign currency transaction from the viewpoint of Malaysian Industries Berhad.

C) Not a foreign currency transaction from the viewpoint of Johnson Ltd, but a foreign currency transaction from the viewpoint of Malaysian Industries Berhad.

D) Not a foreign currency transaction from the viewpoints of both Johnson Ltd and Malaysian Industries Berhad.

During the year ended June 30 20X7, Johnson Ltd became deeply involved in trade with Malaysia. On July 1 20X6, the company acquired 50% of the share capital of a Malaysian palm oil producer, Plantations Berhad, for $7,000,000. For the year ended June 30 20X7, the following balance sheet and income statement were prepared by Plantations Berhad (amounts in thousands):

Income Statement for the Year ended June 30 20X7

Balance Sheet as at June 30 20X7 Statement of the Movement in Retained Earnings in the Year ended June 30 20X7 The functional currency of Plantations Berhad was Malaysian Ringgit. The following translation statement was prepared for the company (amounts in thousands): Additional information:a) A deferred tax liability of 30% of the foreign currency translation reserve is to be recognised.

b) On July 1 20X6, as a partial hedge against its investment in Plantations Berhad, Johnson Ltd took out a three (3) year loan of R 8,000,000 from the Bank Negara at 12% interest, with interest payable quarterly commencing September 30 20X6.

c) On May 15 20X7 Johnson Ltd placed an order for R 2,000,000 in merchandise for resale from Malaysian Industries Berhad, payable in USD. The goods were shipped FOB on May 31 with settlement due on July 31 20X7.

At relevant dates the exchange rates were:

The transaction involving the purchase of the merchandise inventory from Malaysian Industries Berhad is:

A) A foreign currency transaction from the viewpoints of both Johnson Ltd and Malaysian Industries Berhad.

B) A foreign currency transaction from the viewpoint of Johnson Ltd, but not a foreign currency transaction from the viewpoint of Malaysian Industries Berhad.

C) Not a foreign currency transaction from the viewpoint of Johnson Ltd, but a foreign currency transaction from the viewpoint of Malaysian Industries Berhad.

D) Not a foreign currency transaction from the viewpoints of both Johnson Ltd and Malaysian Industries Berhad.

Question

Question

The following data relate to Questions 18-22:

During the year ended June 30 20X7, Johnson Ltd became deeply involved in trade with Malaysia. On July 1 20X6, the company acquired 50% of the share capital of a Malaysian palm oil producer, Plantations Berhad, for $7,000,000. For the year ended June 30 20X7, the following balance sheet and income statement were prepared by Plantations Berhad (amounts in thousands):

Income Statement for the Year ended June 30 20X7

Balance Sheet as at June 30 20X7

Statement of the Movement in Retained Earnings in the Year ended June 30 20X7

The functional currency of Plantations Berhad was Malaysian Ringgit. The following translation statement was prepared for the company (amounts in thousands):

Additional information:

a) A deferred tax liability of 30% of the foreign currency translation reserve is to be recognised.

b) On July 1 20X6, as a partial hedge against its investment in Plantations Berhad, Johnson Ltd took out a three (3) year loan of R 8,000,000 from the Bank Negara at 12% interest, with interest payable quarterly commencing September 30 20X6.

c) On May 15 20X7 Johnson Ltd placed an order for R 2,000,000 in merchandise for resale from Malaysian Industries Berhad, payable in USD. The goods were shipped FOB on May 31 with settlement due on July 31 20X7.

At relevant dates the exchange rates were:

At June 30 20X7 Johnson Ltd recognised its equity in the dividends declared by Plantations Berhad in its income statement.When the dividend was subsequently received from Plantations Berhad,the exchange rate was AUD 1 = R 1.78.The exchange gain or loss recognised by Johnson Ltd on receiving that dividend was (rounded to the nearest dollar)

A) A gain of $6,242

B) A loss of $3,121

C) A gain of $3,121

D) None of the above.

During the year ended June 30 20X7, Johnson Ltd became deeply involved in trade with Malaysia. On July 1 20X6, the company acquired 50% of the share capital of a Malaysian palm oil producer, Plantations Berhad, for $7,000,000. For the year ended June 30 20X7, the following balance sheet and income statement were prepared by Plantations Berhad (amounts in thousands):

Income Statement for the Year ended June 30 20X7

Balance Sheet as at June 30 20X7 Statement of the Movement in Retained Earnings in the Year ended June 30 20X7 The functional currency of Plantations Berhad was Malaysian Ringgit. The following translation statement was prepared for the company (amounts in thousands): Additional information:a) A deferred tax liability of 30% of the foreign currency translation reserve is to be recognised.

b) On July 1 20X6, as a partial hedge against its investment in Plantations Berhad, Johnson Ltd took out a three (3) year loan of R 8,000,000 from the Bank Negara at 12% interest, with interest payable quarterly commencing September 30 20X6.

c) On May 15 20X7 Johnson Ltd placed an order for R 2,000,000 in merchandise for resale from Malaysian Industries Berhad, payable in USD. The goods were shipped FOB on May 31 with settlement due on July 31 20X7.

At relevant dates the exchange rates were:

At June 30 20X7 Johnson Ltd recognised its equity in the dividends declared by Plantations Berhad in its income statement.When the dividend was subsequently received from Plantations Berhad,the exchange rate was AUD 1 = R 1.78.The exchange gain or loss recognised by Johnson Ltd on receiving that dividend was (rounded to the nearest dollar)

A) A gain of $6,242

B) A loss of $3,121

C) A gain of $3,121

D) None of the above.

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/31

Play

Full screen (f)

Deck 10: Translation and Consolidation of Foreign Currency Financial Statements

1

The transactions of a foreign company must be recorded in:

A) its functional currency

B) its presentation currency

C) either functional or presentation currency

D) none of the above

A) its functional currency

B) its presentation currency

C) either functional or presentation currency

D) none of the above

A

2

When the functional currency of a foreign operation is a foreign currency,translation of financial statements is done using:

A) current rate method

B) temporal method

C) either current rate or temporal method

D) none of the above

A) current rate method

B) temporal method

C) either current rate or temporal method

D) none of the above

A

3

Which of the following factors indicate that the functional currency of a foreign operation is that of the reporting entity?

A) The activities of the foreign operation are carried out as an extension of the activities of the reporting entity rather than being carried out with a significant degree of autonomy.

B) Transactions with the reporting entity are a high proportion of the activities of the foreign operation.

C) The day-to-day financing of the foreign operation is supplied by the reporting entity and the cash flows of the foreign operation directly affect the cash flows of the reporting entity.

D) All of the above.

A) The activities of the foreign operation are carried out as an extension of the activities of the reporting entity rather than being carried out with a significant degree of autonomy.

B) Transactions with the reporting entity are a high proportion of the activities of the foreign operation.

C) The day-to-day financing of the foreign operation is supplied by the reporting entity and the cash flows of the foreign operation directly affect the cash flows of the reporting entity.

D) All of the above.

D

4

The primary economic environment in which an entity operates is determined by:

A) currency in which sales are denominated

B) currency in which costs are denominated

C) currency in which financing is obtained

D) all of the above

A) currency in which sales are denominated

B) currency in which costs are denominated

C) currency in which financing is obtained

D) all of the above

Unlock Deck

Unlock for access to all 31 flashcards in this deck.

Unlock Deck

k this deck

5

The presentation currency will be determined by:

A) requirements of accounting standards

B) management choice

C) domicile of majority shareholders

D) none of the above

A) requirements of accounting standards

B) management choice

C) domicile of majority shareholders

D) none of the above

Unlock Deck

Unlock for access to all 31 flashcards in this deck.

Unlock Deck

k this deck

6

An exchange rate stated in the indirect form as AUD 1.25 = USD 1.00 represents a reciprocal of:

A) )80

B) 1.00

C) 1.25

D) none of the above

A) )80

B) 1.00

C) 1.25

D) none of the above

Unlock Deck

Unlock for access to all 31 flashcards in this deck.

Unlock Deck

k this deck

7

The following data relate to Questions 18-22:

During the year ended June 30 20X7, Johnson Ltd became deeply involved in trade with Malaysia. On July 1 20X6, the company acquired 50% of the share capital of a Malaysian palm oil producer, Plantations Berhad, for $7,000,000. For the year ended June 30 20X7, the following balance sheet and income statement were prepared by Plantations Berhad (amounts in thousands):

Income Statement for the Year ended June 30 20X7

Balance Sheet as at June 30 20X7

Statement of the Movement in Retained Earnings in the Year ended June 30 20X7

The functional currency of Plantations Berhad was Malaysian Ringgit. The following translation statement was prepared for the company (amounts in thousands):

Additional information:

a) A deferred tax liability of 30% of the foreign currency translation reserve is to be recognised.

b) On July 1 20X6, as a partial hedge against its investment in Plantations Berhad, Johnson Ltd took out a three (3) year loan of R 8,000,000 from the Bank Negara at 12% interest, with interest payable quarterly commencing September 30 20X6.

c) On May 15 20X7 Johnson Ltd placed an order for R 2,000,000 in merchandise for resale from Malaysian Industries Berhad, payable in USD. The goods were shipped FOB on May 31 with settlement due on July 31 20X7.

At relevant dates the exchange rates were:

The presentation currency and functional currency of Johnson Ltd was:

A) Malaysian ringgit and Australian dollars respectively.

B) Australian dollars and Australian dollars respectively.

C) Australian dollars and Malaysian ringgit respectively.

D) Malaysian ringgit and Malaysian ringgit respectively.

During the year ended June 30 20X7, Johnson Ltd became deeply involved in trade with Malaysia. On July 1 20X6, the company acquired 50% of the share capital of a Malaysian palm oil producer, Plantations Berhad, for $7,000,000. For the year ended June 30 20X7, the following balance sheet and income statement were prepared by Plantations Berhad (amounts in thousands):

Income Statement for the Year ended June 30 20X7

Balance Sheet as at June 30 20X7 Statement of the Movement in Retained Earnings in the Year ended June 30 20X7 The functional currency of Plantations Berhad was Malaysian Ringgit. The following translation statement was prepared for the company (amounts in thousands): Additional information:a) A deferred tax liability of 30% of the foreign currency translation reserve is to be recognised.

b) On July 1 20X6, as a partial hedge against its investment in Plantations Berhad, Johnson Ltd took out a three (3) year loan of R 8,000,000 from the Bank Negara at 12% interest, with interest payable quarterly commencing September 30 20X6.

c) On May 15 20X7 Johnson Ltd placed an order for R 2,000,000 in merchandise for resale from Malaysian Industries Berhad, payable in USD. The goods were shipped FOB on May 31 with settlement due on July 31 20X7.

At relevant dates the exchange rates were:

The presentation currency and functional currency of Johnson Ltd was:

A) Malaysian ringgit and Australian dollars respectively.

B) Australian dollars and Australian dollars respectively.

C) Australian dollars and Malaysian ringgit respectively.

D) Malaysian ringgit and Malaysian ringgit respectively.

Unlock Deck

Unlock for access to all 31 flashcards in this deck.

Unlock Deck

k this deck

8

The following data relate to Questions 18-22:

During the year ended June 30 20X7, Johnson Ltd became deeply involved in trade with Malaysia. On July 1 20X6, the company acquired 50% of the share capital of a Malaysian palm oil producer, Plantations Berhad, for $7,000,000. For the year ended June 30 20X7, the following balance sheet and income statement were prepared by Plantations Berhad (amounts in thousands):

Income Statement for the Year ended June 30 20X7

Balance Sheet as at June 30 20X7

Statement of the Movement in Retained Earnings in the Year ended June 30 20X7

The functional currency of Plantations Berhad was Malaysian Ringgit. The following translation statement was prepared for the company (amounts in thousands):

Additional information:

a) A deferred tax liability of 30% of the foreign currency translation reserve is to be recognised.

b) On July 1 20X6, as a partial hedge against its investment in Plantations Berhad, Johnson Ltd took out a three (3) year loan of R 8,000,000 from the Bank Negara at 12% interest, with interest payable quarterly commencing September 30 20X6.

c) On May 15 20X7 Johnson Ltd placed an order for R 2,000,000 in merchandise for resale from Malaysian Industries Berhad, payable in USD. The goods were shipped FOB on May 31 with settlement due on July 31 20X7.

At relevant dates the exchange rates were:

In the consolidated balance sheet at June 30 20X7 of the group controlled by Johnson Ltd,the foreign currency translation reserve attributable to the members the parent entity would be (rounded to the nearest thousand dollars):

A) $311,111

B) $839,300

C) $108,538

D) None of the above.

During the year ended June 30 20X7, Johnson Ltd became deeply involved in trade with Malaysia. On July 1 20X6, the company acquired 50% of the share capital of a Malaysian palm oil producer, Plantations Berhad, for $7,000,000. For the year ended June 30 20X7, the following balance sheet and income statement were prepared by Plantations Berhad (amounts in thousands):

Income Statement for the Year ended June 30 20X7

Balance Sheet as at June 30 20X7 Statement of the Movement in Retained Earnings in the Year ended June 30 20X7 The functional currency of Plantations Berhad was Malaysian Ringgit. The following translation statement was prepared for the company (amounts in thousands): Additional information:a) A deferred tax liability of 30% of the foreign currency translation reserve is to be recognised.

b) On July 1 20X6, as a partial hedge against its investment in Plantations Berhad, Johnson Ltd took out a three (3) year loan of R 8,000,000 from the Bank Negara at 12% interest, with interest payable quarterly commencing September 30 20X6.

c) On May 15 20X7 Johnson Ltd placed an order for R 2,000,000 in merchandise for resale from Malaysian Industries Berhad, payable in USD. The goods were shipped FOB on May 31 with settlement due on July 31 20X7.

At relevant dates the exchange rates were:

In the consolidated balance sheet at June 30 20X7 of the group controlled by Johnson Ltd,the foreign currency translation reserve attributable to the members the parent entity would be (rounded to the nearest thousand dollars):

A) $311,111

B) $839,300

C) $108,538

D) None of the above.

Unlock Deck

Unlock for access to all 31 flashcards in this deck.

Unlock Deck

k this deck

9

Under the current rate method foreign exchange differences are recognised in:

A) profit or loss

B) other comprehensive income

C) equity

D) none of the above

A) profit or loss

B) other comprehensive income

C) equity

D) none of the above

Unlock Deck

Unlock for access to all 31 flashcards in this deck.

Unlock Deck

k this deck

10

An exchange rate quoted in Australia of AUD 1.00 = USD 1.05 is an example of:

A) direct form of exchange rate

B) indirect form of exchange rate

C) neither form

D) none of the above

A) direct form of exchange rate

B) indirect form of exchange rate

C) neither form

D) none of the above

Unlock Deck

Unlock for access to all 31 flashcards in this deck.

Unlock Deck

k this deck

11

Under the temporal method all revenue and expense items are translated at:

A) historical rate

B) average rate

C) either historical or average rate

D) none of the above

A) historical rate

B) average rate

C) either historical or average rate

D) none of the above

Unlock Deck

Unlock for access to all 31 flashcards in this deck.

Unlock Deck

k this deck

12

The following data relate to Questions 18-22:

During the year ended June 30 20X7, Johnson Ltd became deeply involved in trade with Malaysia. On July 1 20X6, the company acquired 50% of the share capital of a Malaysian palm oil producer, Plantations Berhad, for $7,000,000. For the year ended June 30 20X7, the following balance sheet and income statement were prepared by Plantations Berhad (amounts in thousands):

Income Statement for the Year ended June 30 20X7

Balance Sheet as at June 30 20X7

Statement of the Movement in Retained Earnings in the Year ended June 30 20X7

The functional currency of Plantations Berhad was Malaysian Ringgit. The following translation statement was prepared for the company (amounts in thousands):

Additional information:

a) A deferred tax liability of 30% of the foreign currency translation reserve is to be recognised.

b) On July 1 20X6, as a partial hedge against its investment in Plantations Berhad, Johnson Ltd took out a three (3) year loan of R 8,000,000 from the Bank Negara at 12% interest, with interest payable quarterly commencing September 30 20X6.

c) On May 15 20X7 Johnson Ltd placed an order for R 2,000,000 in merchandise for resale from Malaysian Industries Berhad, payable in USD. The goods were shipped FOB on May 31 with settlement due on July 31 20X7.

At relevant dates the exchange rates were:

In the separate income statement of Johnson Ltd for the year ended June 30 20X7,the translation gain or loss arising on the loan from the Bank Negara was (rounded to the nearest thousand dollars):

A) A translation gain of $311,111

B) A translation loss of $444,000

C) A translation loss of $600,000

D) Nil, since any loss is initially recognised in equity.

During the year ended June 30 20X7, Johnson Ltd became deeply involved in trade with Malaysia. On July 1 20X6, the company acquired 50% of the share capital of a Malaysian palm oil producer, Plantations Berhad, for $7,000,000. For the year ended June 30 20X7, the following balance sheet and income statement were prepared by Plantations Berhad (amounts in thousands):

Income Statement for the Year ended June 30 20X7

Balance Sheet as at June 30 20X7 Statement of the Movement in Retained Earnings in the Year ended June 30 20X7 The functional currency of Plantations Berhad was Malaysian Ringgit. The following translation statement was prepared for the company (amounts in thousands): Additional information:a) A deferred tax liability of 30% of the foreign currency translation reserve is to be recognised.

b) On July 1 20X6, as a partial hedge against its investment in Plantations Berhad, Johnson Ltd took out a three (3) year loan of R 8,000,000 from the Bank Negara at 12% interest, with interest payable quarterly commencing September 30 20X6.

c) On May 15 20X7 Johnson Ltd placed an order for R 2,000,000 in merchandise for resale from Malaysian Industries Berhad, payable in USD. The goods were shipped FOB on May 31 with settlement due on July 31 20X7.

At relevant dates the exchange rates were:

In the separate income statement of Johnson Ltd for the year ended June 30 20X7,the translation gain or loss arising on the loan from the Bank Negara was (rounded to the nearest thousand dollars):

A) A translation gain of $311,111

B) A translation loss of $444,000

C) A translation loss of $600,000

D) Nil, since any loss is initially recognised in equity.

Unlock Deck

Unlock for access to all 31 flashcards in this deck.

Unlock Deck

k this deck

13

Alternative exchange rates which can be used to translate foreign currency amounts are:

A) historical or average

B) opening or closing

C) all of the above

D) none of the above

A) historical or average

B) opening or closing

C) all of the above

D) none of the above

Unlock Deck

Unlock for access to all 31 flashcards in this deck.

Unlock Deck

k this deck

14

Where the functional currency of a foreign operation is not that of an Australian company,in translating the financial statements of that operation into the presentation currency of the Australian company:

A) Foreign currency monetary items are translated at the closing rate and non-monetary items that are measured in terms of historical cost in a foreign currency are translated using the exchange rate at the date of the transaction.

B) Foreign currency monetary items and non-monetary items are translated at the closing rate.

C) Foreign currency monetary items and non-monetary items that are measured in terms of historical cost in a foreign currency are translated using the exchange rate at the date of the transaction.

D) None of the above.

A) Foreign currency monetary items are translated at the closing rate and non-monetary items that are measured in terms of historical cost in a foreign currency are translated using the exchange rate at the date of the transaction.

B) Foreign currency monetary items and non-monetary items are translated at the closing rate.

C) Foreign currency monetary items and non-monetary items that are measured in terms of historical cost in a foreign currency are translated using the exchange rate at the date of the transaction.

D) None of the above.

Unlock Deck

Unlock for access to all 31 flashcards in this deck.

Unlock Deck

k this deck

15

A 'natural hedge' occurs when an Australian company's foreign operation is financed using:

A) debt denominated in AUD

B) debt denominated in same currency as investment

C) debt denominated in any foreign currency

D) none of the above

A) debt denominated in AUD

B) debt denominated in same currency as investment

C) debt denominated in any foreign currency

D) none of the above

Unlock Deck

Unlock for access to all 31 flashcards in this deck.

Unlock Deck

k this deck

16

Translation of financial statements into the presentation currency requires:

A) translation of assets and liabilities at closing rate

B) translation of revenues and expenses at historical or average rate

C) both A and B

D) none of the above

A) translation of assets and liabilities at closing rate

B) translation of revenues and expenses at historical or average rate

C) both A and B

D) none of the above

Unlock Deck

Unlock for access to all 31 flashcards in this deck.

Unlock Deck

k this deck

17

Cash flows from foreign operations denominated in a foreign currency will normally be translated using:

A) historical rates

B) average rates

C) closing rates

D) none of the above

A) historical rates

B) average rates

C) closing rates

D) none of the above

Unlock Deck

Unlock for access to all 31 flashcards in this deck.

Unlock Deck

k this deck

18

Foreign currency transactions include:

A) sale of goods to a foreign buyer

B) purchase of goods from a foreign supplier

C) borrowing from a foreign lender where loan is denominated in a foreign currency

D) all of the above

A) sale of goods to a foreign buyer

B) purchase of goods from a foreign supplier

C) borrowing from a foreign lender where loan is denominated in a foreign currency

D) all of the above

Unlock Deck

Unlock for access to all 31 flashcards in this deck.

Unlock Deck

k this deck

19

Translation of financial statements of foreign operations into the functional currency requires use of:

A) current rate method

B) temporal method

C) either current rate or temporal method

D) none of the above

A) current rate method

B) temporal method

C) either current rate or temporal method

D) none of the above

Unlock Deck

Unlock for access to all 31 flashcards in this deck.

Unlock Deck

k this deck

20

What of the following factors indicate that the functional currency of a foreign operation is not that of the reporting entity?

A) The activities of the foreign operation are carried out with a significant degree of autonomy.

B) There are no material inter-entity transactions or other exchanges between the foreign entity and the reporting entity.

C) The day-to-day financing of the foreign operation is not supplied by the reporting entity and the cash flows of the reporting entity are largely unaffected by the cash flows of the foreign operation.

D) All of the above.

A) The activities of the foreign operation are carried out with a significant degree of autonomy.

B) There are no material inter-entity transactions or other exchanges between the foreign entity and the reporting entity.

C) The day-to-day financing of the foreign operation is not supplied by the reporting entity and the cash flows of the reporting entity are largely unaffected by the cash flows of the foreign operation.

D) All of the above.

Unlock Deck

Unlock for access to all 31 flashcards in this deck.

Unlock Deck

k this deck

21

Where the choice of an entity's functional currency is not clear cut the choice should be based on currency of largest proportion of export sales.

Unlock Deck

Unlock for access to all 31 flashcards in this deck.

Unlock Deck

k this deck

22

The translation gain or loss on a foreign operation using the current rate method represents the effect of exchange rate movements on net assets.

Unlock Deck

Unlock for access to all 31 flashcards in this deck.

Unlock Deck

k this deck

23

Discuss the objectives of translation of financial statements of foreign operations.

Unlock Deck

Unlock for access to all 31 flashcards in this deck.

Unlock Deck

k this deck

24

Discuss the treatment of differences in accounting standards when consolidating foreign operations.

Unlock Deck

Unlock for access to all 31 flashcards in this deck.

Unlock Deck

k this deck

25

Discuss whether the use of the current rate method provides adequate disclosure of the exposure of a foreign operation to exchange rate movements.

Unlock Deck

Unlock for access to all 31 flashcards in this deck.

Unlock Deck

k this deck

26

A foreign exchange gain arising from translating financial statements should always be recorded as revenue

Unlock Deck

Unlock for access to all 31 flashcards in this deck.

Unlock Deck

k this deck

27

The following data relate to Questions 18-22:

During the year ended June 30 20X7, Johnson Ltd became deeply involved in trade with Malaysia. On July 1 20X6, the company acquired 50% of the share capital of a Malaysian palm oil producer, Plantations Berhad, for $7,000,000. For the year ended June 30 20X7, the following balance sheet and income statement were prepared by Plantations Berhad (amounts in thousands):

Income Statement for the Year ended June 30 20X7

Balance Sheet as at June 30 20X7

Statement of the Movement in Retained Earnings in the Year ended June 30 20X7

The functional currency of Plantations Berhad was Malaysian Ringgit. The following translation statement was prepared for the company (amounts in thousands):

Additional information:

a) A deferred tax liability of 30% of the foreign currency translation reserve is to be recognised.

b) On July 1 20X6, as a partial hedge against its investment in Plantations Berhad, Johnson Ltd took out a three (3) year loan of R 8,000,000 from the Bank Negara at 12% interest, with interest payable quarterly commencing September 30 20X6.

c) On May 15 20X7 Johnson Ltd placed an order for R 2,000,000 in merchandise for resale from Malaysian Industries Berhad, payable in USD. The goods were shipped FOB on May 31 with settlement due on July 31 20X7.

At relevant dates the exchange rates were:

The transaction involving the purchase of the merchandise inventory from Malaysian Industries Berhad is:

A) A foreign currency transaction from the viewpoints of both Johnson Ltd and Malaysian Industries Berhad.

B) A foreign currency transaction from the viewpoint of Johnson Ltd, but not a foreign currency transaction from the viewpoint of Malaysian Industries Berhad.

C) Not a foreign currency transaction from the viewpoint of Johnson Ltd, but a foreign currency transaction from the viewpoint of Malaysian Industries Berhad.

D) Not a foreign currency transaction from the viewpoints of both Johnson Ltd and Malaysian Industries Berhad.

During the year ended June 30 20X7, Johnson Ltd became deeply involved in trade with Malaysia. On July 1 20X6, the company acquired 50% of the share capital of a Malaysian palm oil producer, Plantations Berhad, for $7,000,000. For the year ended June 30 20X7, the following balance sheet and income statement were prepared by Plantations Berhad (amounts in thousands):

Income Statement for the Year ended June 30 20X7

Balance Sheet as at June 30 20X7 Statement of the Movement in Retained Earnings in the Year ended June 30 20X7 The functional currency of Plantations Berhad was Malaysian Ringgit. The following translation statement was prepared for the company (amounts in thousands): Additional information:a) A deferred tax liability of 30% of the foreign currency translation reserve is to be recognised.

b) On July 1 20X6, as a partial hedge against its investment in Plantations Berhad, Johnson Ltd took out a three (3) year loan of R 8,000,000 from the Bank Negara at 12% interest, with interest payable quarterly commencing September 30 20X6.

c) On May 15 20X7 Johnson Ltd placed an order for R 2,000,000 in merchandise for resale from Malaysian Industries Berhad, payable in USD. The goods were shipped FOB on May 31 with settlement due on July 31 20X7.

At relevant dates the exchange rates were:

The transaction involving the purchase of the merchandise inventory from Malaysian Industries Berhad is:

A) A foreign currency transaction from the viewpoints of both Johnson Ltd and Malaysian Industries Berhad.

B) A foreign currency transaction from the viewpoint of Johnson Ltd, but not a foreign currency transaction from the viewpoint of Malaysian Industries Berhad.

C) Not a foreign currency transaction from the viewpoint of Johnson Ltd, but a foreign currency transaction from the viewpoint of Malaysian Industries Berhad.

D) Not a foreign currency transaction from the viewpoints of both Johnson Ltd and Malaysian Industries Berhad.

Unlock Deck

Unlock for access to all 31 flashcards in this deck.

Unlock Deck

k this deck

28

Under current accounting standards a company may choose between the current rate and temporal methods of translating foreign currency financial statements.

Unlock Deck

Unlock for access to all 31 flashcards in this deck.

Unlock Deck

k this deck

29

The following data relate to Questions 18-22:

During the year ended June 30 20X7, Johnson Ltd became deeply involved in trade with Malaysia. On July 1 20X6, the company acquired 50% of the share capital of a Malaysian palm oil producer, Plantations Berhad, for $7,000,000. For the year ended June 30 20X7, the following balance sheet and income statement were prepared by Plantations Berhad (amounts in thousands):

Income Statement for the Year ended June 30 20X7

Balance Sheet as at June 30 20X7

Statement of the Movement in Retained Earnings in the Year ended June 30 20X7

The functional currency of Plantations Berhad was Malaysian Ringgit. The following translation statement was prepared for the company (amounts in thousands):

Additional information:

a) A deferred tax liability of 30% of the foreign currency translation reserve is to be recognised.

b) On July 1 20X6, as a partial hedge against its investment in Plantations Berhad, Johnson Ltd took out a three (3) year loan of R 8,000,000 from the Bank Negara at 12% interest, with interest payable quarterly commencing September 30 20X6.

c) On May 15 20X7 Johnson Ltd placed an order for R 2,000,000 in merchandise for resale from Malaysian Industries Berhad, payable in USD. The goods were shipped FOB on May 31 with settlement due on July 31 20X7.

At relevant dates the exchange rates were:

At June 30 20X7 Johnson Ltd recognised its equity in the dividends declared by Plantations Berhad in its income statement.When the dividend was subsequently received from Plantations Berhad,the exchange rate was AUD 1 = R 1.78.The exchange gain or loss recognised by Johnson Ltd on receiving that dividend was (rounded to the nearest dollar)

A) A gain of $6,242

B) A loss of $3,121

C) A gain of $3,121

D) None of the above.

During the year ended June 30 20X7, Johnson Ltd became deeply involved in trade with Malaysia. On July 1 20X6, the company acquired 50% of the share capital of a Malaysian palm oil producer, Plantations Berhad, for $7,000,000. For the year ended June 30 20X7, the following balance sheet and income statement were prepared by Plantations Berhad (amounts in thousands):

Income Statement for the Year ended June 30 20X7

Balance Sheet as at June 30 20X7 Statement of the Movement in Retained Earnings in the Year ended June 30 20X7 The functional currency of Plantations Berhad was Malaysian Ringgit. The following translation statement was prepared for the company (amounts in thousands): Additional information:a) A deferred tax liability of 30% of the foreign currency translation reserve is to be recognised.

b) On July 1 20X6, as a partial hedge against its investment in Plantations Berhad, Johnson Ltd took out a three (3) year loan of R 8,000,000 from the Bank Negara at 12% interest, with interest payable quarterly commencing September 30 20X6.

c) On May 15 20X7 Johnson Ltd placed an order for R 2,000,000 in merchandise for resale from Malaysian Industries Berhad, payable in USD. The goods were shipped FOB on May 31 with settlement due on July 31 20X7.

At relevant dates the exchange rates were:

At June 30 20X7 Johnson Ltd recognised its equity in the dividends declared by Plantations Berhad in its income statement.When the dividend was subsequently received from Plantations Berhad,the exchange rate was AUD 1 = R 1.78.The exchange gain or loss recognised by Johnson Ltd on receiving that dividend was (rounded to the nearest dollar)

A) A gain of $6,242

B) A loss of $3,121

C) A gain of $3,121

D) None of the above.

Unlock Deck

Unlock for access to all 31 flashcards in this deck.

Unlock Deck

k this deck

30

The term 'foreign currency transaction' refers to a transaction denominated in other than Australian dollars

Unlock Deck

Unlock for access to all 31 flashcards in this deck.

Unlock Deck

k this deck

31

Accounting for a foreign subsidiary must use the 'translate then consolidate' approach

Unlock Deck

Unlock for access to all 31 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 31 flashcards in this deck.