Deck 7: Special Issues in Accounting for an Investment in a Subsidiary

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

On January 1, 2016, Pepper Company purchased 90% of the common stock of Salt Company for $360,000 when Salt had total shareholders' equity as follows:

?

?

Any excess of cost over book value on this date is attributed to a patent, to be amortized over 10 years.The 8% preferred stock is cumulative, non-participating, and has a liquidating value of par plus dividends in arrears.There were no preferred dividends in arrears on January 1, 2016.Pepper elected to account for its investment in Salt using the cost method.

?

During 2016, Salt had a net loss of $10,000 and paid no dividends.In 2017, Salt had net income of $100,000 and paid dividends totaling $36,000.

?

During 2017, Salt sold merchandise to Pepper for $40,000, of which $20,000 is still held by Pepper on December 31, 2017.Salt's usual gross profit is 40%.

?

Required:

?

Complete the Figure 7-8 worksheet for consolidated financial statements for the year ended December 31, 2017.

?

?

?

?

?

Any excess of cost over book value on this date is attributed to a patent, to be amortized over 10 years.The 8% preferred stock is cumulative, non-participating, and has a liquidating value of par plus dividends in arrears.There were no preferred dividends in arrears on January 1, 2016.Pepper elected to account for its investment in Salt using the cost method.

?

During 2016, Salt had a net loss of $10,000 and paid no dividends.In 2017, Salt had net income of $100,000 and paid dividends totaling $36,000.

?

During 2017, Salt sold merchandise to Pepper for $40,000, of which $20,000 is still held by Pepper on December 31, 2017.Salt's usual gross profit is 40%.

?

Required:

?

Complete the Figure 7-8 worksheet for consolidated financial statements for the year ended December 31, 2017.

?

? Question

Question

On January 1, 2016, Pepper Company purchased 90% of the common stock of Salt Company for $360,000 when Salt had total shareholders' equity as follows:

?

?

Any excess of cost over book value on this date is attributed to a patent, to be amortized over 10 years.The 8% preferred stock is cumulative, non-participating, and has a liquidating value of par plus dividends in arrears.There were no preferred dividends in arrears on January 1, 2016.Pepper elected to account for its investment in Salt using the simple equity method.

?

During 2016, Salt had a net loss of $10,000 and paid no dividends.In 2017, Salt had net income of $100,000 and paid dividends totaling $36,000.

?

During 2017, Salt sold merchandise to Pepper for $40,000, of which $20,000 is still held by Pepper on December 31, 2017.Salt's usual gross profit is 40%.

?

Required:

?

Complete the Figure 7-7 worksheet for consolidated financial statements for the year ended December 31, 2017.

?

?

?

?

Any excess of cost over book value on this date is attributed to a patent, to be amortized over 10 years.The 8% preferred stock is cumulative, non-participating, and has a liquidating value of par plus dividends in arrears.There were no preferred dividends in arrears on January 1, 2016.Pepper elected to account for its investment in Salt using the simple equity method.

?

During 2016, Salt had a net loss of $10,000 and paid no dividends.In 2017, Salt had net income of $100,000 and paid dividends totaling $36,000.

?

During 2017, Salt sold merchandise to Pepper for $40,000, of which $20,000 is still held by Pepper on December 31, 2017.Salt's usual gross profit is 40%.

?

Required:

?

Complete the Figure 7-7 worksheet for consolidated financial statements for the year ended December 31, 2017.

?

?

Question

Question

Question

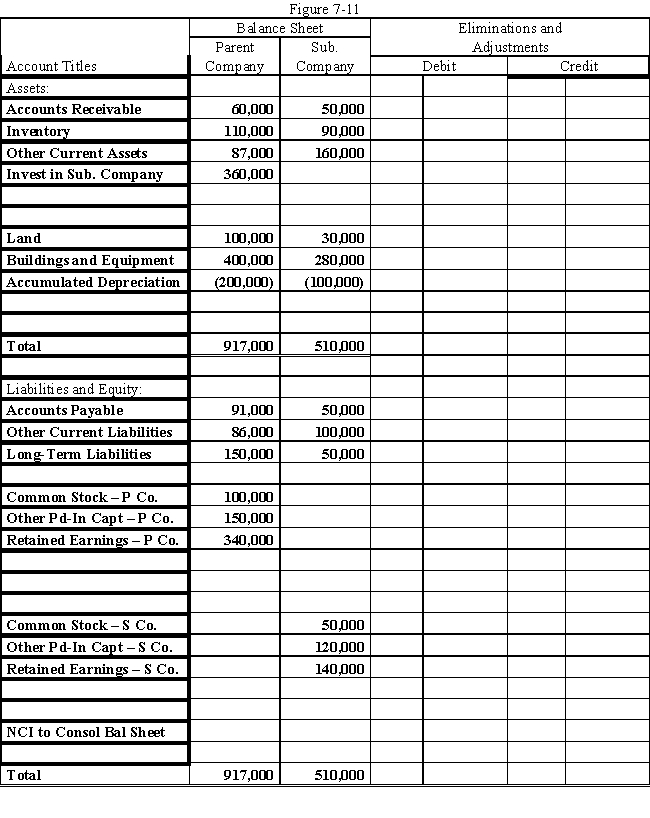

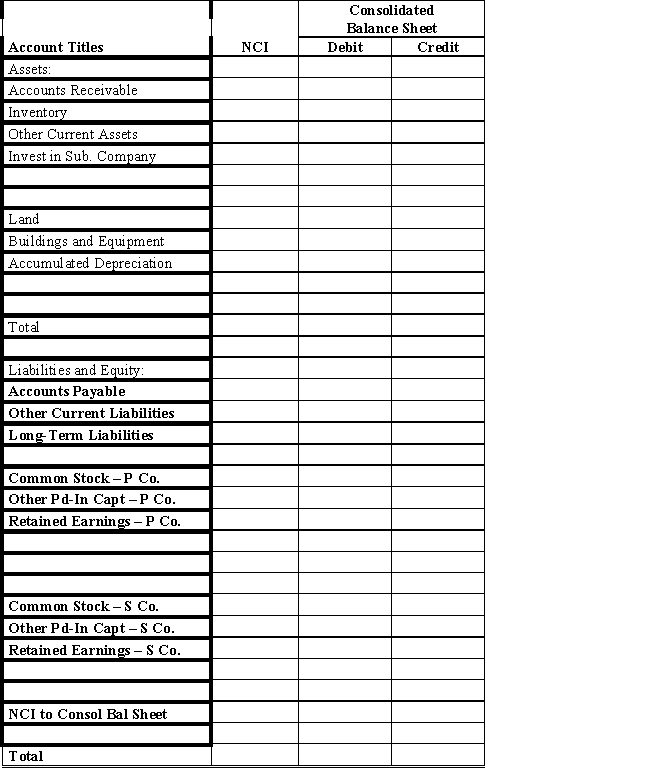

On January 1, 2016, Parent Company acquired 90% of the common stock of Subsidiary Company for $360,000.On this date, Subsidiary had total owners' equity of $270,000, including retained earnings of $100,000.

?

On January 1, 2016, any excess of cost over book value is attributable to the undervaluation of land, building, and goodwill.Land is worth $20,000 more than cost.Building is worth $60,000 more than book value.It has a remaining useful life of 6 years and is depreciated using the straight-line method.

?

During 2016, Parent has accounted for its investment in Subsidiary using the cost method.

?

During 2016, Subsidiary sold merchandise to Parent for $70,000, of which $20,000 is held by Parent on December 31, 2016.Subsidiary's usual gross profit on affiliated sales is 50%.

?

On December 31, 2016, Parent still owes Subsidiary $5,000 for merchandise acquired in December.

?

On July 1, 2016, Parent sold to Subsidiary some equipment with a cost of $40,000 and a book value of $18,000.The sales price was $30,000.Subsidiary is depreciating the equipment over a 4-year life, assuming no salvage value and using the straight-line method.

?

Required:

?

Prepare a determination and distribution of excess schedule.Next, complete the Figure 7-11 worksheet for a consolidated balance sheet as of December 31, 2016.

?

?

On January 1, 2016, any excess of cost over book value is attributable to the undervaluation of land, building, and goodwill.Land is worth $20,000 more than cost.Building is worth $60,000 more than book value.It has a remaining useful life of 6 years and is depreciated using the straight-line method.

?

During 2016, Parent has accounted for its investment in Subsidiary using the cost method.

?

During 2016, Subsidiary sold merchandise to Parent for $70,000, of which $20,000 is held by Parent on December 31, 2016.Subsidiary's usual gross profit on affiliated sales is 50%.

?

On December 31, 2016, Parent still owes Subsidiary $5,000 for merchandise acquired in December.

?

On July 1, 2016, Parent sold to Subsidiary some equipment with a cost of $40,000 and a book value of $18,000.The sales price was $30,000.Subsidiary is depreciating the equipment over a 4-year life, assuming no salvage value and using the straight-line method.

?

Required:

?

Prepare a determination and distribution of excess schedule.Next, complete the Figure 7-11 worksheet for a consolidated balance sheet as of December 31, 2016.

?

Question

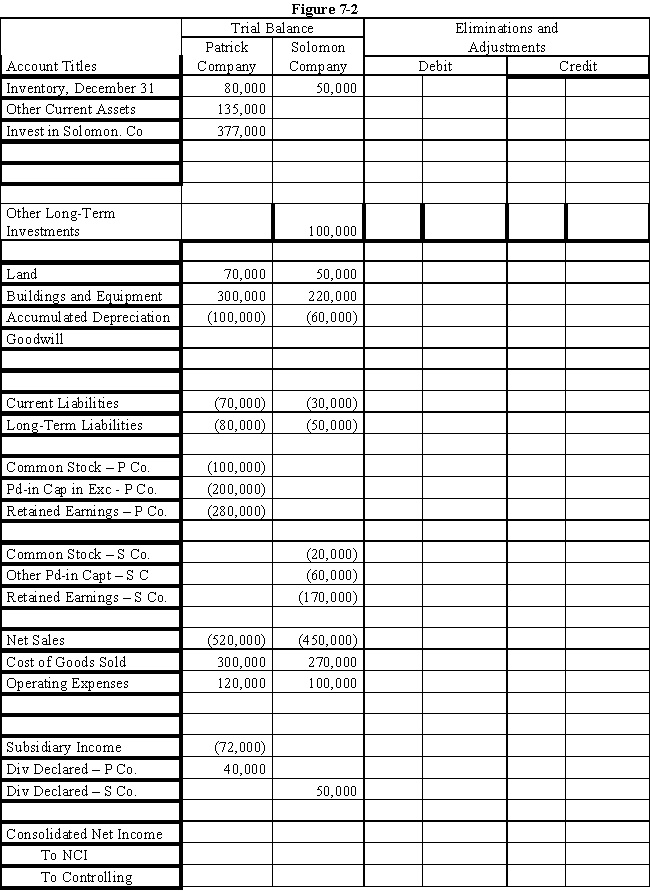

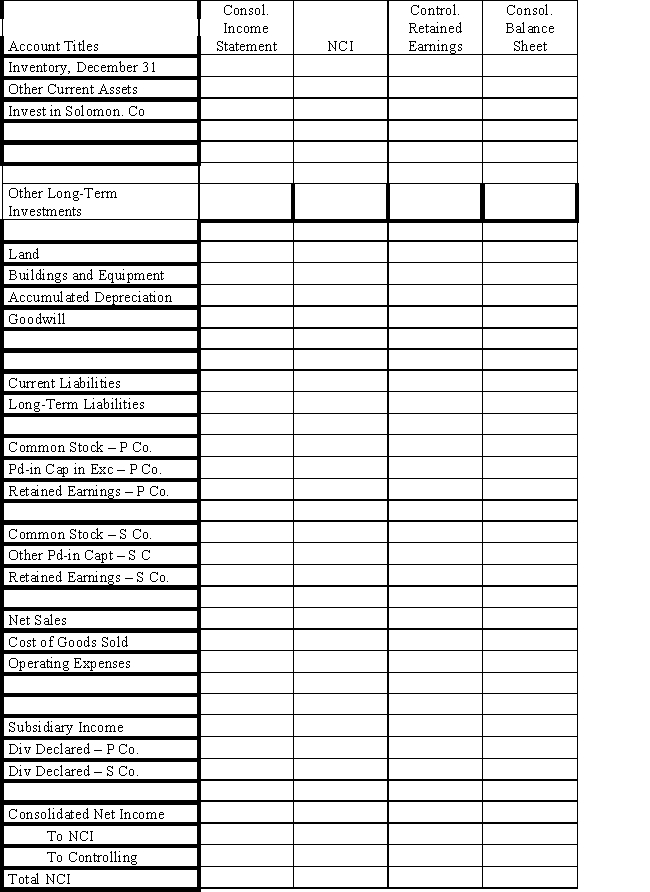

On January 1, 2016, Patrick Company purchased 60% of the common stock of Solomon Company for $180,000.On this date, Solomon had common stock, other paid-in capital, and retained earnings of $20,000, $60,000, and $120,000 respectively.

?

On January 1, 2016, the only tangible asset of Solomon that was undervalued was land, which was worth $15,000 more than book value.

?

On January 1, 2017, Patrick Company purchased an additional 30% of the common stock of Solomon Company for $140,000.

?

Net income and dividends for 2 years for Solomon Company were:

?

?

In the last quarter of 2017, Solomon sold $80,000 of goods to Patrick, at a gross profit rate of 30%.On December 31, 2017, $20,000 of these goods are in Patrick's ending inventory.In both 2016 and 2017, Patrick has accounted for its investment in Solomon using the simple equity method.

?

Required:

?

a.Using the information from the scenario or on the separate worksheet, prepare necessary determination and distribution of excess schedules for the two purchases.?

?

b.Complete the Figure 7-2 worksheet for consolidated financial statements for 2017.?

?

?

?

?

On January 1, 2016, the only tangible asset of Solomon that was undervalued was land, which was worth $15,000 more than book value.

?

On January 1, 2017, Patrick Company purchased an additional 30% of the common stock of Solomon Company for $140,000.

?

Net income and dividends for 2 years for Solomon Company were:

?

?

In the last quarter of 2017, Solomon sold $80,000 of goods to Patrick, at a gross profit rate of 30%.On December 31, 2017, $20,000 of these goods are in Patrick's ending inventory.In both 2016 and 2017, Patrick has accounted for its investment in Solomon using the simple equity method.

?

Required:

?

a.Using the information from the scenario or on the separate worksheet, prepare necessary determination and distribution of excess schedules for the two purchases.?

?

b.Complete the Figure 7-2 worksheet for consolidated financial statements for 2017.?

?

? Question

Question

Question

Question

Question

Question

Question

Question

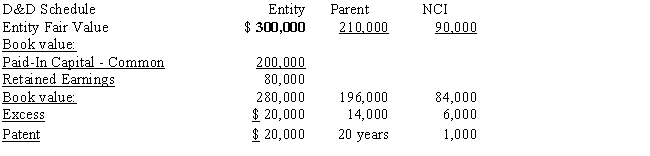

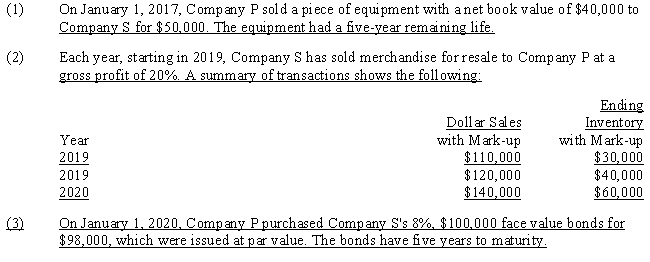

Company P Industries purchased a 70% interest in Company S on January 1, 2016, and prepared the following determination and distribution of excess schedule:

Since the purchase, there have been the following intercompany transactions:

Since the purchase, there have been the following intercompany transactions:

Required:

Required:

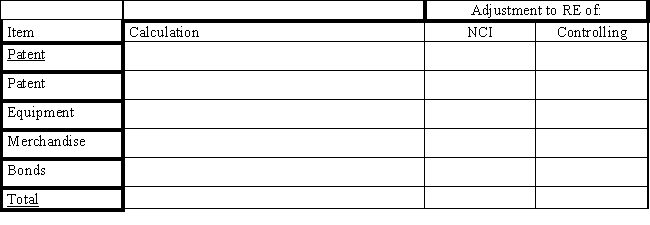

Complete the following schedule to adjust the retained earnings of the non-controlling and controlling interest on the December 31, 2020, worksheet for a consolidated balance sheet only.Company P uses the simple equity method to account for its investment.

Since the purchase, there have been the following intercompany transactions:

Required:

Complete the following schedule to adjust the retained earnings of the non-controlling and controlling interest on the December 31, 2020, worksheet for a consolidated balance sheet only.Company P uses the simple equity method to account for its investment.

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/42

Play

Full screen (f)

Deck 7: Special Issues in Accounting for an Investment in a Subsidiary

1

Which of the following statements is incorrect regarding a parent's purchase of additional subsidiary shares?

A)There can never be an income statement gain or loss.

B)Due to the constraints of conservatism, there can never be an income statement gain but a loss should be recognized if so indicated.

C)If the price paid to reacquire the shares exceeds their book value, the debit first is used to reduce existing paid-in capital in excess of par from retirement and the balance is a debit to Retained Earnings.

D)If the price paid to reacquire the shares is less than their book value, there is a credit to paid-in capital in excess of par from retirement.

A)There can never be an income statement gain or loss.

B)Due to the constraints of conservatism, there can never be an income statement gain but a loss should be recognized if so indicated.

C)If the price paid to reacquire the shares exceeds their book value, the debit first is used to reduce existing paid-in capital in excess of par from retirement and the balance is a debit to Retained Earnings.

D)If the price paid to reacquire the shares is less than their book value, there is a credit to paid-in capital in excess of par from retirement.

B

2

Control of a subsidiary was achieved with the initial investment in subsidiary stock.When a subsequent block of subsidiary's stock is purchased

A)the parent must change from the cost method to the equity method.

B)the parent must change from the equity method to the cost method.

C)no change in accounting methods is required.

D)none of the above.

A)the parent must change from the cost method to the equity method.

B)the parent must change from the equity method to the cost method.

C)no change in accounting methods is required.

D)none of the above.

C

3

Partridge purchased a 60% interest in Sparrow on January 1, 2016, for $240,000.At the time of the purchase, Sparrow had the following stockholders' equity:

Any excess is attributable to equipment with a 10-year life.On January 1, 2016, the retained earnings of Sparrow was $175,000.The entire investment was sold for $300,000 on January 1, 2016.The gain was ____.

A)$87,000

B)$90,000

C)$27,000

D)$78,000

Any excess is attributable to equipment with a 10-year life.On January 1, 2016, the retained earnings of Sparrow was $175,000.The entire investment was sold for $300,000 on January 1, 2016.The gain was ____.

A)$87,000

B)$90,000

C)$27,000

D)$78,000

$87,000

4

Partridge purchased a 60% interest in Sparrow on January 1, 2016, for $240,000.At the time of the purchase, Sparrow had the following stockholders' equity:

Any excess is attributable to goodwill.On January 1, 2016, the retained earnings of Sparrow was $175,000.The entire investment was sold for $300,000 on January 1, 2016.At that date, Partridge had on hand inventory it had purchased from Sparrow for $50,000.Sparrow has a gross profit percentage of 40%.The gain (loss) was ____.

A)$105,000

B)$81,000

C)$27,000

D)$39,000

Any excess is attributable to goodwill.On January 1, 2016, the retained earnings of Sparrow was $175,000.The entire investment was sold for $300,000 on January 1, 2016.At that date, Partridge had on hand inventory it had purchased from Sparrow for $50,000.Sparrow has a gross profit percentage of 40%.The gain (loss) was ____.

A)$105,000

B)$81,000

C)$27,000

D)$39,000

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

5

Patten Company purchased an 80% interest in Salty Inc.on January 1, 2016, for $500,000 when the stockholders' equity of Salty was $500,000.Any excess of cost was attributed to a building with a 20-year life.On July 1, 2019, Patten sold part of its investment and reduced its ownership interest to 60%.Salty earned $62,000, evenly, during 2019.The NCI share of 2019 consolidated income is

A)$10,000

B)$12,400

C)$16,725

D)$43,400

A)$10,000

B)$12,400

C)$16,725

D)$43,400

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

6

Pine Company purchased a 60% interest in the Scent Company on January 1, 2016 for $360,000.On that date, the stockholders' equity of Scent Company was $450,000.Any excess cost on 1/1/16 was attributable to goodwill.Pine purchased another 20% interest on January 1, 2019 for $200,000.On January 1, 2019, Scent Company's stockholders' equity was $700,000, the entire increase due to retained earnings.The excess of cost over book on the new block of stock is ____.

A)$60,000

B)$50,000

C)$48,000

D)$20,000

A)$60,000

B)$50,000

C)$48,000

D)$20,000

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

7

When selling an investment in a subsidiary, in order to record the appropriate gain or loss:

A)the investment must be adjusted to show the balance under the sophisticated equity method.

B)the investment must be adjusted to show the balance under the equity method.

C)a final consolidation must be prepared.

D)the unamortized balances of the excess of the purchase price over the book value of the investment must be written off.

A)the investment must be adjusted to show the balance under the sophisticated equity method.

B)the investment must be adjusted to show the balance under the equity method.

C)a final consolidation must be prepared.

D)the unamortized balances of the excess of the purchase price over the book value of the investment must be written off.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

8

If the sale of an investment in a subsidiary is deemed to be a disposal of a component of the entity, the appropriate accounting treatments for the results its operations for the period and the gain or loss on the sale are: Results of Operations for the Period Gain or Loss on the Sale

A)Normal recurring operations Extraordinary item

B)Discontinued operations Discontinued operations

C)Normal recurring operations Normal recurring operations

D)Normal recurring operations Discontinued operations

A)Normal recurring operations Extraordinary item

B)Discontinued operations Discontinued operations

C)Normal recurring operations Normal recurring operations

D)Normal recurring operations Discontinued operations

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

9

Page Company purchased an 80% interest in the common stock of the Seed Company for $600,000 on January 1, 2019, when Seed Company had the following stockholders' equity:

Any excess of cost over book value on the common stock purchase was attributed to goodwill.Page does not hold any of Seed's preferred stock.Seed had net income of $40,000 during 2019 and paid no dividends.

The preferred stock is one year in arrears on January 1, 2019.The goodwill that will appear on the consolidated balance sheet prepared on January 1, 2019, is ____.

A)$80,000

B)$88,000

C)$210,000

D)$168,000

Any excess of cost over book value on the common stock purchase was attributed to goodwill.Page does not hold any of Seed's preferred stock.Seed had net income of $40,000 during 2019 and paid no dividends.

The preferred stock is one year in arrears on January 1, 2019.The goodwill that will appear on the consolidated balance sheet prepared on January 1, 2019, is ____.

A)$80,000

B)$88,000

C)$210,000

D)$168,000

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

10

Pine Company purchased a 60% interest in the Scent Company on January 1, 2016 for $360,000.On that date, the stockholders' equity of Scent Company was $450,000.Any excess cost on 1/1/16 was attributable to goodwill.Pine purchased another 20% interest on January 1, 2019 for $200,000.On January 1, 2019, Scent Company's stockholders' equity was $700,000, the entire increase due to retained earnings.As part of the consolidation process, the excess of the price paid over book on the new block of shares is treated as

A)additional goodwill

B)a loss on acquisition of additional subsidiary shares

C)an increase to Pine's Investment in Scent account

D)a reduction in parent's paid-in capital in excess of par

A)additional goodwill

B)a loss on acquisition of additional subsidiary shares

C)an increase to Pine's Investment in Scent account

D)a reduction in parent's paid-in capital in excess of par

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

11

Page Company purchased an 80% interest in the common stock of the Seed Company for $600,000 on January 1, 2019, when Seed Company had the following stockholders' equity:

Any excess of cost over book value on the common stock purchase was attributed to goodwill.Page does not hold any of Seed's preferred stock.Seed had net income of $40,000 during 2019 and paid no dividends.

The preferred stock is two years in arrears on January 1, 2019.The controlling interest's share of Seed's 2019 net income is ____.

A)$24,000

B)$23,360

C)$25,600

D)$32,000

Any excess of cost over book value on the common stock purchase was attributed to goodwill.Page does not hold any of Seed's preferred stock.Seed had net income of $40,000 during 2019 and paid no dividends.

The preferred stock is two years in arrears on January 1, 2019.The controlling interest's share of Seed's 2019 net income is ____.

A)$24,000

B)$23,360

C)$25,600

D)$32,000

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

12

A parent company owns a 90% interest in a subsidiary at the start of the year and during the year sells a 10% interest to reduce its ownership percentage to 80%.The most popular view of the transaction under current consolidations theory is that

A)it is a sale of an investment at a gain or a loss.

B)it is likened to a treasury stock transaction that may not result in a gain or a loss.

C)it is a transaction between the controlling and non-controlling ownership interests and has no effect on consolidated income.The transaction would impact only paid-in capital.

D)the increase or decrease in equity as a result of the sale is an adjustment to donated capital.

A)it is a sale of an investment at a gain or a loss.

B)it is likened to a treasury stock transaction that may not result in a gain or a loss.

C)it is a transaction between the controlling and non-controlling ownership interests and has no effect on consolidated income.The transaction would impact only paid-in capital.

D)the increase or decrease in equity as a result of the sale is an adjustment to donated capital.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

13

When a parent sells its subsidiary interest, a gain (loss) is recognized if the parent ?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

14

Parent has purchased additional shares of subsidiary stock.If the original investment blocks are carried at cost, the conversion to simple equity is based upon

A)the difference in subsidiary retained earnings at the beginning of the current fiscal year and the retained earnings when the first block was acquired.

B)the difference in subsidiary retained earnings at the beginning of the current fiscal year and the retained earnings when the block giving a controlling interest was acquired.

C)the difference in subsidiary retained earnings at the beginning of the current fiscal year and the retained earnings of each block at its acquisition.

D)the difference in subsidiary retained earnings at the beginning of the current fiscal year and the retained earnings when the last block was acquired.

A)the difference in subsidiary retained earnings at the beginning of the current fiscal year and the retained earnings when the first block was acquired.

B)the difference in subsidiary retained earnings at the beginning of the current fiscal year and the retained earnings when the block giving a controlling interest was acquired.

C)the difference in subsidiary retained earnings at the beginning of the current fiscal year and the retained earnings of each block at its acquisition.

D)the difference in subsidiary retained earnings at the beginning of the current fiscal year and the retained earnings when the last block was acquired.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

15

Partridge purchased a 60% interest in Sparrow on January 1, 2016, for $240,000.At the time of the purchase, Sparrow had the following stockholders' equity:

Any excess is attributable to equipment with a 10-year life.On January 1, 2016, the retained earnings of Sparrow was $175,000.During the first 6 months of 2016, $25,000 was earned by Sparrow.The entire investment was sold for $300,000 on July 1, 2016.The gain (loss) was ____.

A)$87,000

B)$78,000

C)$12,000

D)$60,000

Any excess is attributable to equipment with a 10-year life.On January 1, 2016, the retained earnings of Sparrow was $175,000.During the first 6 months of 2016, $25,000 was earned by Sparrow.The entire investment was sold for $300,000 on July 1, 2016.The gain (loss) was ____.

A)$87,000

B)$78,000

C)$12,000

D)$60,000

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

16

A new subsidiary is being formed.The parent company purchased 70% of the shares for $20 per share.The remaining shares were sold to a variety of outside interests for an average of $18 per share.The consolidated statements will show

A)a gain.

B)a loss.

C)only cash and related equity.

D)goodwill.

A)a gain.

B)a loss.

C)only cash and related equity.

D)goodwill.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

17

Pine Company purchased a 60% interest in the Scent Company on January 1, 2016 for $360,000.On that date, the stockholders' equity of Scent Company was $450,000.Any excess cost on 1/1/16 was attributable to goodwill.Pine purchased another 20% interest on January 1, 2019 for $200,000.On January 1, 2019, Scent Company's stockholders' equity was $700,000, the entire increase due to retained earnings.The goodwill balance on the December 31, 2019, balance sheet is ____.

A)$100,000

B)$60,000

C)$0

D)$150,000

A)$100,000

B)$60,000

C)$0

D)$150,000

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

18

In the year a parent sells its entire subsidiary investment, the results of subsidiary operations prior to the sale date are

A)consolidated to the point of sale.

B)shown on the balance sheet in the stockholders' equity section as an adjustment to retained earnings.

C)not reflected on any of the parent's statements.

D)not consolidated.

A)consolidated to the point of sale.

B)shown on the balance sheet in the stockholders' equity section as an adjustment to retained earnings.

C)not reflected on any of the parent's statements.

D)not consolidated.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

19

A new subsidiary is being formed.The parent company purchased 70% of the shares for $20 per share.The remaining shares were sold to a variety of outside interests for an average of $22 per share.The consolidated statements will show

A)a gain.

B)a loss.

C)only cash and related equity.

D)goodwill.

A)a gain.

B)a loss.

C)only cash and related equity.

D)goodwill.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

20

Page Company purchased an 80% interest in the common stock of the Seed Company for $600,000 on January 1, 2019, when Seed Company had the following stockholders' equity:

Any excess of cost over book value on the common stock purchase was attributed to goodwill.Page does not hold any of Seed's preferred stock.Seed had net income of $40,000 during 2019 and paid no dividends.

The preferred stock is two years in arrears on January 1, 2019.The non-controlling interest share of 2019 net income was ____.

A)$3,200

B)$6,000

C)$8,000

D)$16,000

Any excess of cost over book value on the common stock purchase was attributed to goodwill.Page does not hold any of Seed's preferred stock.Seed had net income of $40,000 during 2019 and paid no dividends.

The preferred stock is two years in arrears on January 1, 2019.The non-controlling interest share of 2019 net income was ____.

A)$3,200

B)$6,000

C)$8,000

D)$16,000

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

21

When preparing a consolidated balance sheet worksheet when the investment account is maintained under the simple equity method:

A)the parent's share of subsidiary income should be eliminated against retained earnings.

B)the parent's share of the subsidiary's equity accounts may be eliminated directly against the investment account.

C)any intercompany sales must be eliminated against cost of goods sold.

D)the investment account should be converted to the cost method as of the end of the year.

A)the parent's share of subsidiary income should be eliminated against retained earnings.

B)the parent's share of the subsidiary's equity accounts may be eliminated directly against the investment account.

C)any intercompany sales must be eliminated against cost of goods sold.

D)the investment account should be converted to the cost method as of the end of the year.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

22

On January 1, 2016, Patrick Company purchased 60% of the common stock of Solomon Company for $180,000.On this date, Solomon had common stock, other paid-in capital, and retained earnings of $20,000, $60,000, and $120,000 respectively.

?

On January 1, 2016, the only tangible asset of Solomon that was undervalued was land, which was worth $15,000 more than book value.

?

On January 1, 2017, Patrick Company purchased an additional 30% of the common stock of Solomon Company for $140,000.

?

Net income and dividends for 2 years for Solomon Company were:

?

?

In the last quarter of 2017, Solomon sold $80,000 of goods to Patrick, at a gross profit rate of 30%.On December 31, 2017, $20,000 of these goods are in Patrick's ending inventory.In both 2016 and 2017, Patrick has accounted for its investment in Solomon using the cost method.

?

Required:

?

a.Using the information above or on the separate worksheet, prepare necessary determination and distribution of excess schedules for the two purchases.

?

On January 1, 2016, the only tangible asset of Solomon that was undervalued was land, which was worth $15,000 more than book value.

?

On January 1, 2017, Patrick Company purchased an additional 30% of the common stock of Solomon Company for $140,000.

?

Net income and dividends for 2 years for Solomon Company were:

?

?

In the last quarter of 2017, Solomon sold $80,000 of goods to Patrick, at a gross profit rate of 30%.On December 31, 2017, $20,000 of these goods are in Patrick's ending inventory.In both 2016 and 2017, Patrick has accounted for its investment in Solomon using the cost method.

?

Required:

?

a.Using the information above or on the separate worksheet, prepare necessary determination and distribution of excess schedules for the two purchases.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

23

On January 1, 2016, Company P purchased a 90% interest in Company S for $360,000.Company P prepared the following determination and distribution of excess schedule at that time:

?

?

Company S had income of $30,000 for 2016 and $40,000 for 2017.No dividends were paid.Company P sold its entire investment in Company S on January 1, 2019, for $340,000.

?

Required:

Prepare Company P's entries to record the sale assuming that Company P used the

a.simple equity method to reflect its investment in Company S.

b.cost method to reflect its investment in Company S.

?

?

Company S had income of $30,000 for 2016 and $40,000 for 2017.No dividends were paid.Company P sold its entire investment in Company S on January 1, 2019, for $340,000.

?

Required:

Prepare Company P's entries to record the sale assuming that Company P used the

a.simple equity method to reflect its investment in Company S.

b.cost method to reflect its investment in Company S.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

24

Plant Company owns 80% of the common stock of Surf Company.Surf Company also has outstanding preferred stock.Plant Company owned none of the preferred stock prior to January 1, 2020.Plant Company purchased 100% of the outstanding preferred stock on January 1, 2020, at a price in excess of book value.The result of this transaction with regard to the consolidated statements is that

A)there will be added goodwill.

B)there will be a loss recorded in the year of the purchase.

C)the preferred stock will not appear on the balance sheet and there may be a decrease in retained earnings as a result of the purchase.

D)the investment in preferred stock will appear on the balance sheet.

A)there will be added goodwill.

B)there will be a loss recorded in the year of the purchase.

C)the preferred stock will not appear on the balance sheet and there may be a decrease in retained earnings as a result of the purchase.

D)the investment in preferred stock will appear on the balance sheet.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

25

Pilatte Company acquired a 90% interest in the common stock of Sweet Company for $630,000 on January 1, 2019, when Sweet Company had the following stockholders' equity:

?

?

The preferred stock dividends are 2 years in arrears.Any excess is attributable to equipment with a 5-year life, which is undervalued by $40,000, and to goodwill.

?

Required:

?

Prepare a determination and distribution of excess schedule for the investment in Sweet Company.

?

?

The preferred stock dividends are 2 years in arrears.Any excess is attributable to equipment with a 5-year life, which is undervalued by $40,000, and to goodwill.

?

Required:

?

Prepare a determination and distribution of excess schedule for the investment in Sweet Company.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

26

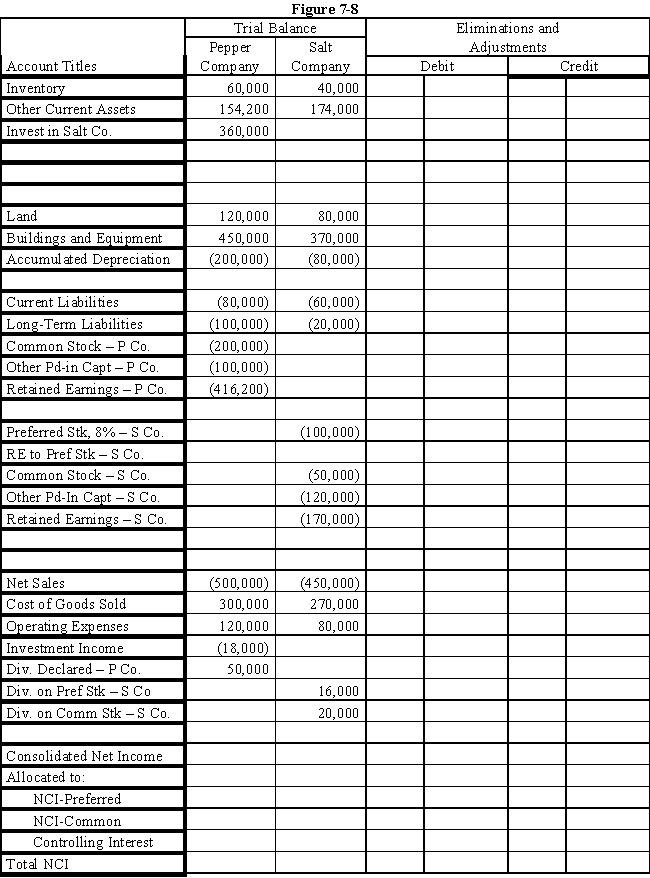

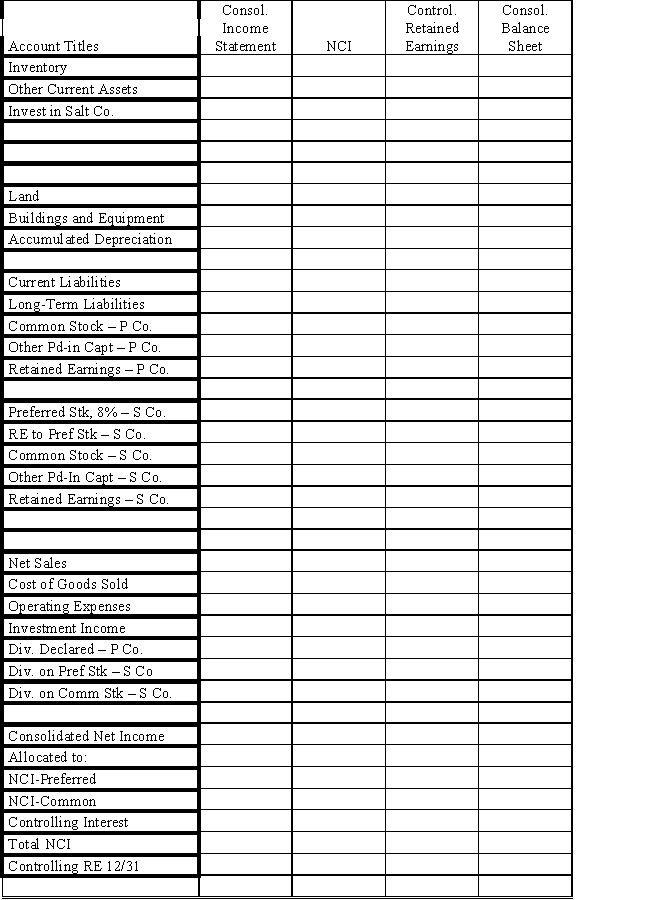

On January 1, 2016, Pepper Company purchased 90% of the common stock of Salt Company for $360,000 when Salt had total shareholders' equity as follows:

?

?

Any excess of cost over book value on this date is attributed to a patent, to be amortized over 10 years.The 8% preferred stock is cumulative, non-participating, and has a liquidating value of par plus dividends in arrears.There were no preferred dividends in arrears on January 1, 2016.Pepper elected to account for its investment in Salt using the cost method.

?

During 2016, Salt had a net loss of $10,000 and paid no dividends.In 2017, Salt had net income of $100,000 and paid dividends totaling $36,000.

?

During 2017, Salt sold merchandise to Pepper for $40,000, of which $20,000 is still held by Pepper on December 31, 2017.Salt's usual gross profit is 40%.

?

Required:

?

Complete the Figure 7-8 worksheet for consolidated financial statements for the year ended December 31, 2017.

?

?

?

?

Any excess of cost over book value on this date is attributed to a patent, to be amortized over 10 years.The 8% preferred stock is cumulative, non-participating, and has a liquidating value of par plus dividends in arrears.There were no preferred dividends in arrears on January 1, 2016.Pepper elected to account for its investment in Salt using the cost method.

?

During 2016, Salt had a net loss of $10,000 and paid no dividends.In 2017, Salt had net income of $100,000 and paid dividends totaling $36,000.

?

During 2017, Salt sold merchandise to Pepper for $40,000, of which $20,000 is still held by Pepper on December 31, 2017.Salt's usual gross profit is 40%.

?

Required:

?

Complete the Figure 7-8 worksheet for consolidated financial statements for the year ended December 31, 2017.

?

? Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

27

On January 1, 2016, Parent Company purchased 80% of the common stock of Subsidiary Company for $300,000.Any excess of cost over book value on this date is attributed to a patent, to be amortized over 10 years.

?

On this date, Subsidiary had total shareholders' equity as follows:

?

?

The 8% preferred stock is cumulative, non-participating, and has a liquidating value of par plus dividends in arrears.There were no preferred dividends in arrears on January 1, 2016.

?

During 2016, Subsidiary had a net loss of $10,000 and paid no dividends.In 2017, Subsidiary had net income of $20,000, but paid no dividends.In 2019, Subsidiary had net income of $100,000 and paid dividends, on preferred and common, totaling $50,000.

?

On January 1, 2017, Parent purchased $50,000 par value of Subsidiary's preferred stock for $52,000.At year end, the preferred is still held as an investment.

?

Required:

?

a.) Prepare Parent's journal entries for its investment in the subsidiary's preferred stock for 2017 and 2019.

b.) Calculate the increase in equity resulting from the retirement of preferred stock.

c.) Prepare the entries needed to eliminate the parent's investment in the subsidiary's preferred stock for the 2019 consolidated worksheet.

?

On this date, Subsidiary had total shareholders' equity as follows:

?

?

The 8% preferred stock is cumulative, non-participating, and has a liquidating value of par plus dividends in arrears.There were no preferred dividends in arrears on January 1, 2016.

?

During 2016, Subsidiary had a net loss of $10,000 and paid no dividends.In 2017, Subsidiary had net income of $20,000, but paid no dividends.In 2019, Subsidiary had net income of $100,000 and paid dividends, on preferred and common, totaling $50,000.

?

On January 1, 2017, Parent purchased $50,000 par value of Subsidiary's preferred stock for $52,000.At year end, the preferred is still held as an investment.

?

Required:

?

a.) Prepare Parent's journal entries for its investment in the subsidiary's preferred stock for 2017 and 2019.

b.) Calculate the increase in equity resulting from the retirement of preferred stock.

c.) Prepare the entries needed to eliminate the parent's investment in the subsidiary's preferred stock for the 2019 consolidated worksheet.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

28

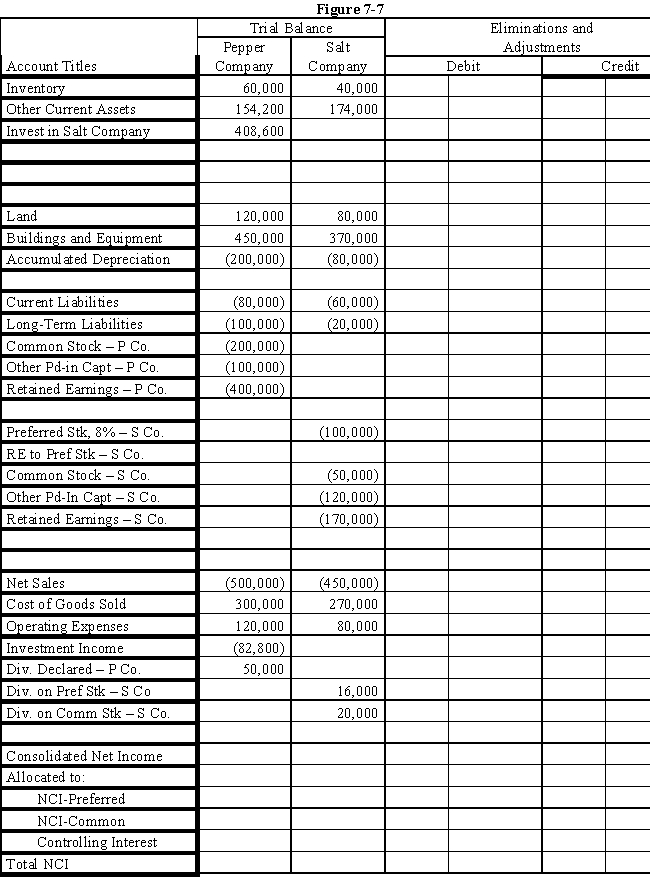

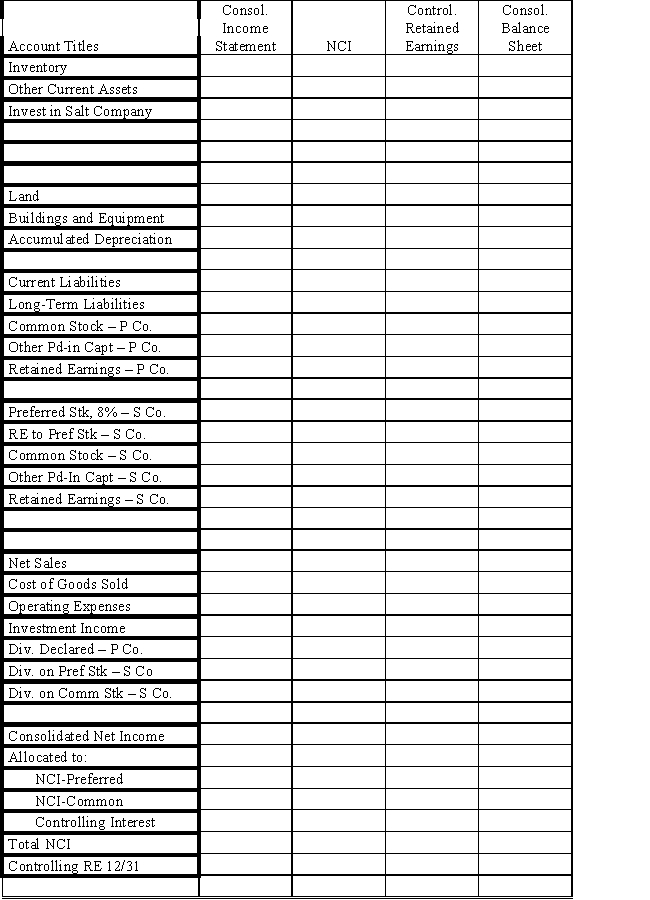

On January 1, 2016, Pepper Company purchased 90% of the common stock of Salt Company for $360,000 when Salt had total shareholders' equity as follows:

?

?

Any excess of cost over book value on this date is attributed to a patent, to be amortized over 10 years.The 8% preferred stock is cumulative, non-participating, and has a liquidating value of par plus dividends in arrears.There were no preferred dividends in arrears on January 1, 2016.Pepper elected to account for its investment in Salt using the simple equity method.

?

During 2016, Salt had a net loss of $10,000 and paid no dividends.In 2017, Salt had net income of $100,000 and paid dividends totaling $36,000.

?

During 2017, Salt sold merchandise to Pepper for $40,000, of which $20,000 is still held by Pepper on December 31, 2017.Salt's usual gross profit is 40%.

?

Required:

?

Complete the Figure 7-7 worksheet for consolidated financial statements for the year ended December 31, 2017.

?

?

?

?

Any excess of cost over book value on this date is attributed to a patent, to be amortized over 10 years.The 8% preferred stock is cumulative, non-participating, and has a liquidating value of par plus dividends in arrears.There were no preferred dividends in arrears on January 1, 2016.Pepper elected to account for its investment in Salt using the simple equity method.

?

During 2016, Salt had a net loss of $10,000 and paid no dividends.In 2017, Salt had net income of $100,000 and paid dividends totaling $36,000.

?

During 2017, Salt sold merchandise to Pepper for $40,000, of which $20,000 is still held by Pepper on December 31, 2017.Salt's usual gross profit is 40%.

?

Required:

?

Complete the Figure 7-7 worksheet for consolidated financial statements for the year ended December 31, 2017.

?

?

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

29

When you create an income distribution schedule for consolidated net income, the distributions:

A)are allocated equally between Company P and Company S.

B)should use the controlling/noncontrolling interest ownership with respect to both common and preferred shares.

C)for the parent Company P should convert its investment to its equity balance if it is not using the cost method.

D)none of the above

A)are allocated equally between Company P and Company S.

B)should use the controlling/noncontrolling interest ownership with respect to both common and preferred shares.

C)for the parent Company P should convert its investment to its equity balance if it is not using the cost method.

D)none of the above

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

30

On January 1, 2016, Poplar Company acquired 80% of the common stock of Sequoia Company for $400,000.On this date, Sequoia had total owners' equity of $400,000.The excess of cost over book value was due to a patent with remaining life of 10 years.Poplar adopted the simple equity method to account for its investment in Sequoia.

?

Sequoia's income for the three years 2016 through 2019 is $80,000, $60,000, and $100,000 respectively.All income is earned evenly throughout the year; Sub has paid no dividends.

?

On July 1, 2019, Poplar Company sold 50% of the total stock of Sequoia for $400,000, reducing its investment percentage to 30%.Prepare Poplar's general journal entries for 2019.

?

Sequoia's income for the three years 2016 through 2019 is $80,000, $60,000, and $100,000 respectively.All income is earned evenly throughout the year; Sub has paid no dividends.

?

On July 1, 2019, Poplar Company sold 50% of the total stock of Sequoia for $400,000, reducing its investment percentage to 30%.Prepare Poplar's general journal entries for 2019.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

31

On January 1, 2016, Parent Company acquired 90% of the common stock of Subsidiary Company for $360,000.On this date, Subsidiary had total owners' equity of $270,000, including retained earnings of $100,000.

?

On January 1, 2016, any excess of cost over book value is attributable to the undervaluation of land, building, and goodwill.Land is worth $20,000 more than cost.Building is worth $60,000 more than book value.It has a remaining useful life of 6 years and is depreciated using the straight-line method.

?

During 2016, Parent has accounted for its investment in Subsidiary using the cost method.

?

During 2016, Subsidiary sold merchandise to Parent for $70,000, of which $20,000 is held by Parent on December 31, 2016.Subsidiary's usual gross profit on affiliated sales is 50%.

?

On December 31, 2016, Parent still owes Subsidiary $5,000 for merchandise acquired in December.

?

On July 1, 2016, Parent sold to Subsidiary some equipment with a cost of $40,000 and a book value of $18,000.The sales price was $30,000.Subsidiary is depreciating the equipment over a 4-year life, assuming no salvage value and using the straight-line method.

?

Required:

?

Prepare a determination and distribution of excess schedule.Next, complete the Figure 7-11 worksheet for a consolidated balance sheet as of December 31, 2016.

?

?

On January 1, 2016, any excess of cost over book value is attributable to the undervaluation of land, building, and goodwill.Land is worth $20,000 more than cost.Building is worth $60,000 more than book value.It has a remaining useful life of 6 years and is depreciated using the straight-line method.

?

During 2016, Parent has accounted for its investment in Subsidiary using the cost method.

?

During 2016, Subsidiary sold merchandise to Parent for $70,000, of which $20,000 is held by Parent on December 31, 2016.Subsidiary's usual gross profit on affiliated sales is 50%.

?

On December 31, 2016, Parent still owes Subsidiary $5,000 for merchandise acquired in December.

?

On July 1, 2016, Parent sold to Subsidiary some equipment with a cost of $40,000 and a book value of $18,000.The sales price was $30,000.Subsidiary is depreciating the equipment over a 4-year life, assuming no salvage value and using the straight-line method.

?

Required:

?

Prepare a determination and distribution of excess schedule.Next, complete the Figure 7-11 worksheet for a consolidated balance sheet as of December 31, 2016.

?

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

32

On January 1, 2016, Patrick Company purchased 60% of the common stock of Solomon Company for $180,000.On this date, Solomon had common stock, other paid-in capital, and retained earnings of $20,000, $60,000, and $120,000 respectively.

?

On January 1, 2016, the only tangible asset of Solomon that was undervalued was land, which was worth $15,000 more than book value.

?

On January 1, 2017, Patrick Company purchased an additional 30% of the common stock of Solomon Company for $140,000.

?

Net income and dividends for 2 years for Solomon Company were:

?

?

In the last quarter of 2017, Solomon sold $80,000 of goods to Patrick, at a gross profit rate of 30%.On December 31, 2017, $20,000 of these goods are in Patrick's ending inventory.In both 2016 and 2017, Patrick has accounted for its investment in Solomon using the simple equity method.

?

Required:

?

a.Using the information from the scenario or on the separate worksheet, prepare necessary determination and distribution of excess schedules for the two purchases.?

?

b.Complete the Figure 7-2 worksheet for consolidated financial statements for 2017.?

?

?

?

On January 1, 2016, the only tangible asset of Solomon that was undervalued was land, which was worth $15,000 more than book value.

?

On January 1, 2017, Patrick Company purchased an additional 30% of the common stock of Solomon Company for $140,000.

?

Net income and dividends for 2 years for Solomon Company were:

?

?

In the last quarter of 2017, Solomon sold $80,000 of goods to Patrick, at a gross profit rate of 30%.On December 31, 2017, $20,000 of these goods are in Patrick's ending inventory.In both 2016 and 2017, Patrick has accounted for its investment in Solomon using the simple equity method.

?

Required:

?

a.Using the information from the scenario or on the separate worksheet, prepare necessary determination and distribution of excess schedules for the two purchases.?

?

b.Complete the Figure 7-2 worksheet for consolidated financial statements for 2017.?

?

? Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

33

Saddle Corporation is an 80%-owned subsidiary of Paso Company.On January 1, 2016, Saddle sold Paso a machine for $50,000.Saddle's cost was $60,000 and the book value was $40,000.The machine had a 5-year remaining life at the time of the sale.A consolidated balance sheet only is being prepared on December 31, 2019.The retained earnings of the controlling interest requires which of the following adjustments?

A)Debit $4,000

B)Debit $6,000

C)Debit $3,200

D)Debit $4,800

A)Debit $4,000

B)Debit $6,000

C)Debit $3,200

D)Debit $4,800

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

34

Pepin Company owns 75% of Savin Corp.Savin's net income in the current year was $60,000.Savin also has 10,000 shares of 4% cumulative preferred $10 par value stock outstanding.When Pepin purchased Savin, the excess purchase price of $50,000 was attributable to a patent having a life of 10 years.How much income is attributable to the controlling interest?

A)$45,000

B)$41,250

C)$37,250

D)$38,250

A)$45,000

B)$41,250

C)$37,250

D)$38,250

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

35

Company P has consistently sold merchandise for resale to its subsidiary at a gross profit of 20%.There were intercompany goods in both the subsidiary's beginning and ending inventory.As a result of these sales, which of the following amounts must be adjusted for when preparing only a consolidated balance sheet? ?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

36

On January 1, 2016, Poplar Company acquired 80% of the common stock of Sequoia Company for $400,000.On this date, Sequoia had total owners' equity of $400,000.The excess of cost over book value was due to a patent with remaining life of 10 years.Poplar adopted the simple equity method to account for its investment in Sequoia.

?

Sequoia's income for the three years 2016 through 2019 is $80,000, $60,000, and $100,000 respectively.All income is earned evenly throughout the year; Sub has paid no dividends.

?

On July 1, 2019, Poplar Company sold 10% of the total stock of Sequoia for $70,000, reducing its investment percentage to 70%.Prepare Poplar's general journal entries for 2019.

?

Sequoia's income for the three years 2016 through 2019 is $80,000, $60,000, and $100,000 respectively.All income is earned evenly throughout the year; Sub has paid no dividends.

?

On July 1, 2019, Poplar Company sold 10% of the total stock of Sequoia for $70,000, reducing its investment percentage to 70%.Prepare Poplar's general journal entries for 2019.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

37

Which of the following is not true of an investor's investment in the preferred stock of an investee?

A)Because preferred stock normally does not carry voting rights, an investor many not have controlling interest if owning 100% of the preferred stock.

B)The investor's purchase of investee's outstanding preferred stock viewed of a retirement of the stock.

C)Preferred stock is included in the Determination and Distribution of Excess Schedule to calculate goodwill.

D)Preferred stock dividends reduce the income available to the NCI.

A)Because preferred stock normally does not carry voting rights, an investor many not have controlling interest if owning 100% of the preferred stock.

B)The investor's purchase of investee's outstanding preferred stock viewed of a retirement of the stock.

C)Preferred stock is included in the Determination and Distribution of Excess Schedule to calculate goodwill.

D)Preferred stock dividends reduce the income available to the NCI.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

38

Company P owns a 90% interest in Company S.Company S has outstanding $100,000 of 10% bonds that were sold at face value and have 6 years to maturity as of the balance sheet date.Company P owns $70,000 of the bonds and has a remaining unamortized book value of $66,000.Company S bonds will be presented on the consolidated balance sheet as

A)bonds payable, $30,000.

B)bonds payable, $34,000.

C)bonds payable, $100,000.

D)bonds payable will not appear.

A)bonds payable, $30,000.

B)bonds payable, $34,000.

C)bonds payable, $100,000.

D)bonds payable will not appear.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

39

Parent Company owns an 80% interest in Subsidiary Company.Subsidiary Company has outstanding $200,000 of 8% bonds that were sold at face value and have 5 years to mature from the balance sheet date.Parent Company owns 75% of the bonds and has a remaining unamortized book value of $145,000.Subsidiary Company bonds will be presented on the consolidated balance sheet as

A)bonds payable, $55,000

B)bonds payable, $50,000

C)bonds payable, $ 5,000

D)bonds payable, $ 40,000

A)bonds payable, $55,000

B)bonds payable, $50,000

C)bonds payable, $ 5,000

D)bonds payable, $ 40,000

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

40

Company P Industries purchased a 70% interest in Company S on January 1, 2016, and prepared the following determination and distribution of excess schedule:

Since the purchase, there have been the following intercompany transactions:

Required:

Complete the following schedule to adjust the retained earnings of the non-controlling and controlling interest on the December 31, 2020, worksheet for a consolidated balance sheet only.Company P uses the simple equity method to account for its investment.

Since the purchase, there have been the following intercompany transactions:

Required:

Complete the following schedule to adjust the retained earnings of the non-controlling and controlling interest on the December 31, 2020, worksheet for a consolidated balance sheet only.Company P uses the simple equity method to account for its investment.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

41

A subsidiary company may have preferred stock as part of its equity structure.Further, suppose that the preferred stock is cumulative and in arrears on dividends.

?

Required:

?

a.What is the impact of the preferred stock on the excess of cost over book value on the original controlling investment in common stock?

?

?

b.What is the impact of the preferred stock on the annual distribution of income?

?

?

c.What is the theory followed in consolidated reporting when the parent purchases a portion of the subsidiary's preferred stock?

?

?

Required:

?

a.What is the impact of the preferred stock on the excess of cost over book value on the original controlling investment in common stock?

?

?

b.What is the impact of the preferred stock on the annual distribution of income?

?

?

c.What is the theory followed in consolidated reporting when the parent purchases a portion of the subsidiary's preferred stock?

?

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

42

It is common for a parent firm to record its investment in a subsidiary under either the cost or simple equity method to expedite the elimination process.This does create some complications, however, when all or a portion of the investment is sold.Assume that in each of the following cases, the parent sells its investment midway through its fiscal year.

?

?

(1) The parent owned an interest and sold all of its hol dings.

(2) The parent owned an interest and sold a interest to reduce its ownership percentage to .

(3) The parent owned an interest and sold a interest to reduce its ownership percentage to . Required:

?

a.For each of the above cases, comment on the procedures necessary to record the sale, where the investment is carried under simple equity, and the impact on consolidated income of the sale.?

?

b.For each of the above cases, state the added procedures that would be necessary if the investment was recorded under the cost method.

?

?

(1) The parent owned an interest and sold all of its hol dings.

(2) The parent owned an interest and sold a interest to reduce its ownership percentage to .

(3) The parent owned an interest and sold a interest to reduce its ownership percentage to . Required:

?

a.For each of the above cases, comment on the procedures necessary to record the sale, where the investment is carried under simple equity, and the impact on consolidated income of the sale.?

?

b.For each of the above cases, state the added procedures that would be necessary if the investment was recorded under the cost method.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 42 flashcards in this deck.