Deck 4: Consolidated Financial Statements and Outside Ownership

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

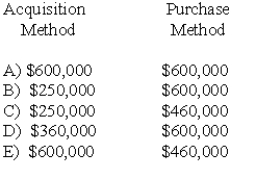

MacHeath Inc.bought 60% of the outstanding common stock of Nomes Inc.in a business combination that resulted in the recognition of goodwill.Nomes owned a piece of land that cost $250,000 but was worth $600,000 at the date of purchase.What value would be attributed to this land in a consolidated balance sheet at the date of takeover,according to the acquisition method per SFAS 141(R)and the purchase method per SFAS 141?

A)Entry A

B)Entry B

C)Entry C

D)Entry D

E)Entry E

A)Entry A

B)Entry B

C)Entry C

D)Entry D

E)Entry E

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Keefe,Inc. ,a calendar-year corporation,acquires 70% of George Company on September 1,2009 and an additional 10% on April 1,2010.Total annual amortization of $6,000 relates to the first acquisition.George reports the following figures for 2010:

Without regard for this investment,Keefe earns $300,000 in net income during 2010.

All net income is earned evenly throughout the year.

What is the controlling interest in consolidated net income for 2010?

A)$373,300

B)$372,850

C)$371,500

D)$376,000

E)$372,805

Without regard for this investment,Keefe earns $300,000 in net income during 2010.

All net income is earned evenly throughout the year.

What is the controlling interest in consolidated net income for 2010?

A)$373,300

B)$372,850

C)$371,500

D)$376,000

E)$372,805

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/51

Play

Full screen (f)

Deck 4: Consolidated Financial Statements and Outside Ownership

1

What is the consolidated balance of the Equipment account?

A)$666,400

B)$604,000

C)$756,000

D)$711,200

E)$764,000

A)$666,400

B)$604,000

C)$756,000

D)$711,200

E)$764,000

C

2

What amount should have been reported for the land on a consolidated balance sheet,according to SFAS 141(R),using the acquisition method?

A)$70,000

B)$75,000

C)$85,000

D)$92,500

E)$100,000

A)$70,000

B)$75,000

C)$85,000

D)$92,500

E)$100,000

E

3

What is the dollar amount of non-controlling interest which should appear on a balance sheet prepared immediately after consolidation according to the acquisition method per SFAS 141(R)?

A)$350,000

B)$300,000

C)$400,000

D)$370,000

E)$0

A)$350,000

B)$300,000

C)$400,000

D)$370,000

E)$0

C

4

What amount of excess land allocation would be included for the calculation of non-controlling interest,according to SFAS 141(R)?

A)$0

B)$7,500

C)$17,500

D)$25,000

E)$70,000

A)$0

B)$7,500

C)$17,500

D)$25,000

E)$70,000

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

5

What is the total amount of goodwill recognized per SFAS 141 (R)using the acquisition method?

A)$150,000

B)$250,000

C)$0

D)$120,000

E)$170,000

A)$150,000

B)$250,000

C)$0

D)$120,000

E)$170,000

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

6

Kordel Inc.holds 75% of the outstanding common stock of Raxston Corp.Raxston currently owes Kordel $500,000 for inventory acquired over the past few months.In preparing consolidated financial statements,what amount of this debt should be eliminated?

A)$375,000

B)$125,000

C)$300,000

D)$500,000

E)$0

A)$375,000

B)$125,000

C)$300,000

D)$500,000

E)$0

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

7

What amount should have been reported for the land on a consolidated balance sheet,assuming the investment was obtained prior to SFAS 141(R)and the purchase method,parent company concept,was used?

A)$70,000

B)$75,000

C)$85,000

D)$92,500

E)$100,000

A)$70,000

B)$75,000

C)$85,000

D)$92,500

E)$100,000

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

8

MacHeath Inc.bought 60% of the outstanding common stock of Nomes Inc.in a business combination that resulted in the recognition of goodwill.Nomes owned a piece of land that cost $250,000 but was worth $600,000 at the date of purchase.What value would be attributed to this land in a consolidated balance sheet at the date of takeover,according to the acquisition method per SFAS 141(R)and the purchase method per SFAS 141?

A)Entry A

B)Entry B

C)Entry C

D)Entry D

E)Entry E

A)Entry A

B)Entry B

C)Entry C

D)Entry D

E)Entry E

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

9

In consolidation,the total amount of expenses related to Kailey and to Denber's acquisition of Kailey for 2009 is determined to be

A)$206,667

B)$211,667

C)$221,667

D)$620,000

E)$635,000

A)$206,667

B)$211,667

C)$221,667

D)$620,000

E)$635,000

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

10

What amount of goodwill should be attributed to the non-controlling interest according to the acquisition method per SFAS 141(R)?

A)$0

B)$20,000

C)$30,000

D)$100,000

E)$120,000

A)$0

B)$20,000

C)$30,000

D)$100,000

E)$120,000

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

11

The non-controlling interest's share of the earnings of Harbor Corp.is calculated to be

A)$132,000

B)$150,000

C)$168,000

D)$160,000

E)$0

A)$132,000

B)$150,000

C)$168,000

D)$160,000

E)$0

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

12

What amount of goodwill should be attributed to Perch according to the acquisition method per SFAS 141(R)?

A)$150,000

B)$250,000

C)$0

D)$120,000

E)$170,000

A)$150,000

B)$250,000

C)$0

D)$120,000

E)$170,000

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

13

The non-controlling interest's share shown on Denber's income statement for 2009 is calculated to be

A)$22,000

B)$24,000

C)$48,000

D)$66,000

E)$72,000

A)$22,000

B)$24,000

C)$48,000

D)$66,000

E)$72,000

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

14

According to SFAS 160,Non-controlling Interests and Consolidated Financial Statements,a non-controlling interest is most likely to be shown as part of equity under the

A)Acquisition method

B)Proportionate consolidation method

C)Economic unit method

D)Parent company method

E)Proprietary method

A)Acquisition method

B)Proportionate consolidation method

C)Economic unit method

D)Parent company method

E)Proprietary method

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

15

The impact of the consolidation on consolidated net income for 2009 is determined to be

A)$31,000

B)$33,000

C)$55,000

D)$60,000

E)$39,000

A)$31,000

B)$33,000

C)$55,000

D)$60,000

E)$39,000

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

16

What is the non-controlling interest's share of the subsidiary's net income and what is the ending balance of the non-controlling interest in the subsidiary?

A)$50,400 and $397,600

B)$53,648 and $304,500

C)$56,000 and $296,800

D)$52,640 and $313,600

E)$55,270 and $297,300

A)$50,400 and $397,600

B)$53,648 and $304,500

C)$56,000 and $296,800

D)$52,640 and $313,600

E)$55,270 and $297,300

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

17

What is consolidated net income that is attributable to Royce's controlling interest?

A)$686,000

B)$560,000

C)$644,000

D)$635,600

E)$691,600

A)$686,000

B)$560,000

C)$644,000

D)$635,600

E)$691,600

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

18

What is the net effect of the inclusion of Harbor on consolidated net income for 2009?

A)$350,000

B)$308,000

C)$500,000

D)$440,000

E)$290,000

A)$350,000

B)$308,000

C)$500,000

D)$440,000

E)$290,000

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

19

What is the dollar amount of non-controlling interest which should appear on a balance sheet prepared immediately after consolidation according to the purchase method according to SFAS 141?

A)$350,000

B)$300,000

C)$400,000

D)$250,000

E)$0

A)$350,000

B)$300,000

C)$400,000

D)$250,000

E)$0

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

20

What is the dollar amount of Float Corp.'s net assets that would be represented on a balance sheet prepared immediately after consolidation according to the acquisition method per SFAS 141(R)?

A)$1,600,000

B)$1,480,000

C)$1,200,000

D)$1,780,000

E)$1,850,000

A)$1,600,000

B)$1,480,000

C)$1,200,000

D)$1,780,000

E)$1,850,000

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

21

When a parent uses the equity method throughout the year to account for investment in a subsidiary,which of the following statements is false before making adjustments on the consolidated worksheet?

A)Parent company net income equals controlling interest in consolidated net income

B)Parent company retained earnings equals consolidated retained earnings

C)Parent company total assets equals consolidated total assets

D)Parent company dividends equals consolidated dividends

E)Goodwill may need to be recorded

A)Parent company net income equals controlling interest in consolidated net income

B)Parent company retained earnings equals consolidated retained earnings

C)Parent company total assets equals consolidated total assets

D)Parent company dividends equals consolidated dividends

E)Goodwill may need to be recorded

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

22

What is consolidated current liabilities as of January 2,2009?

A)$70,000

B)$56,000

C)$64,400

D)$42,000

E)$58,100

A)$70,000

B)$56,000

C)$64,400

D)$42,000

E)$58,100

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

23

When a parent uses the partial equity method throughout the year to account for investment in a subsidiary,which of the following statements is false before making adjustments on the consolidated worksheet?

A)Parent company net income will equal controlling interest in consolidated net income when initial value,book value and fair value of the investment are equal

B)Parent company net income will exceed controlling interest in consolidated net income when fair value acquired exceeds book value

C)Parent company net income will be less than controlling interest in consolidated net income when fair value acquired exceeds book value

D)Goodwill will be recognized if acquisition value exceeds fair value

E)Subsidiary net assets are valued at their book values

A)Parent company net income will equal controlling interest in consolidated net income when initial value,book value and fair value of the investment are equal

B)Parent company net income will exceed controlling interest in consolidated net income when fair value acquired exceeds book value

C)Parent company net income will be less than controlling interest in consolidated net income when fair value acquired exceeds book value

D)Goodwill will be recognized if acquisition value exceeds fair value

E)Subsidiary net assets are valued at their book values

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

24

When using the acquisition method for accounting for business combinations,all of the following statements are false regarding the sale of subsidiary shares except:

A)If control ceases to exist and significant influence ceases to exist,the difference between selling price and acquisition value is recorded as a realized gain or loss

B)If control ceases to exist and significant influence ceases to exist,the difference between selling price and acquisition value is recorded as an unrealized gain or loss

C)If control ceases to exist and significant influence ceases to exist,the difference between selling price and carrying value is recorded as a realized gain or loss

D)If control ceases to exist and significant influence ceases to exist,the difference between selling price and carrying value is recorded as an unrealized gain or loss

E)If control ceases to exist and significant influence ceases to exist,the difference between selling price and carrying value is recorded as an adjustment to retained earnings

A)If control ceases to exist and significant influence ceases to exist,the difference between selling price and acquisition value is recorded as a realized gain or loss

B)If control ceases to exist and significant influence ceases to exist,the difference between selling price and acquisition value is recorded as an unrealized gain or loss

C)If control ceases to exist and significant influence ceases to exist,the difference between selling price and carrying value is recorded as a realized gain or loss

D)If control ceases to exist and significant influence ceases to exist,the difference between selling price and carrying value is recorded as an unrealized gain or loss

E)If control ceases to exist and significant influence ceases to exist,the difference between selling price and carrying value is recorded as an adjustment to retained earnings

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

25

Under the acquisition method of accounting for business combinations,which of the following statements is true about consolidated financial statements?

A)The accounting emphasis in preparing consolidated financial statements is placed on the business combination being formed

B)The accounting emphasis in preparing consolidated financial statements is placed on the parent's investment

C)The objective of consolidated financial statements is to serve as a report to the stockholders of the parent company

D)The acquisition method is a hybrid of the purchase method and the pooling of interests method

E)The acquisition method is no longer allowed according to SFAS 141(R)

A)The accounting emphasis in preparing consolidated financial statements is placed on the business combination being formed

B)The accounting emphasis in preparing consolidated financial statements is placed on the parent's investment

C)The objective of consolidated financial statements is to serve as a report to the stockholders of the parent company

D)The acquisition method is a hybrid of the purchase method and the pooling of interests method

E)The acquisition method is no longer allowed according to SFAS 141(R)

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

26

All of the following statements regarding the sale of subsidiary shares are true except which of the following?

A)The use of specific identification based on serial number is acceptable

B)The use of the FIFO assumption is acceptable

C)The use of the averaging assumption is acceptable

D)The use of specific LIFO assumption is acceptable

E)The parent company must determine whether consolidation is still appropriate for the remaining shares owned

A)The use of specific identification based on serial number is acceptable

B)The use of the FIFO assumption is acceptable

C)The use of the averaging assumption is acceptable

D)The use of specific LIFO assumption is acceptable

E)The parent company must determine whether consolidation is still appropriate for the remaining shares owned

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

27

Keefe,Inc. ,a calendar-year corporation,acquires 70% of George Company on September 1,2009 and an additional 10% on April 1,2010.Total annual amortization of $6,000 relates to the first acquisition.George reports the following figures for 2010:

Without regard for this investment,Keefe earns $300,000 in net income during 2010.

All net income is earned evenly throughout the year.

What is the controlling interest in consolidated net income for 2010?

A)$373,300

B)$372,850

C)$371,500

D)$376,000

E)$372,805

Without regard for this investment,Keefe earns $300,000 in net income during 2010.

All net income is earned evenly throughout the year.

What is the controlling interest in consolidated net income for 2010?

A)$373,300

B)$372,850

C)$371,500

D)$376,000

E)$372,805

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

28

Under the purchase methodof accounting for business combinations,which of the following statements is true about consolidated financial statements?

A)The accounting emphasis in preparing consolidated financial statements is placed on the business combination being formed

B)Holding control of a subsidiary provides the parent with an indivisible interest in that company

C)The objective of consolidated financial statements is to serve as a report to the stockholders of the parent company

D)The purchase method is a hybrid of the acquisition method and the pooling of interests method

E)The purchase method is no longer allowed for combinations occurring according to SFAS 141(R)

A)The accounting emphasis in preparing consolidated financial statements is placed on the business combination being formed

B)Holding control of a subsidiary provides the parent with an indivisible interest in that company

C)The objective of consolidated financial statements is to serve as a report to the stockholders of the parent company

D)The purchase method is a hybrid of the acquisition method and the pooling of interests method

E)The purchase method is no longer allowed for combinations occurring according to SFAS 141(R)

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

29

Which of the following statements is true regarding the sale of subsidiary shares when using the acquisition method for accounting for business combinations?

A)If control continues,the difference between selling price and acquisition value is recorded as a realized gain or loss

B)If control continues,the difference between selling price and acquisition value is an unrealized gain or loss

C)If control continues,the difference between selling price and carrying value is recorded as an adjustment to additional paid-in capital

D)If control continues,the difference between selling price and carrying value is recorded as a realized gain or loss

E)If control continues,the difference between selling price and carrying value is recorded as an adjustment to retained earnings

A)If control continues,the difference between selling price and acquisition value is recorded as a realized gain or loss

B)If control continues,the difference between selling price and acquisition value is an unrealized gain or loss

C)If control continues,the difference between selling price and carrying value is recorded as an adjustment to additional paid-in capital

D)If control continues,the difference between selling price and carrying value is recorded as a realized gain or loss

E)If control continues,the difference between selling price and carrying value is recorded as an adjustment to retained earnings

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

30

When a parent uses the acquisition method for business combinations and sells shares of its subsidiary,which of the following statements is false?

A)If majority control is still maintained,consolidated financial statements are still required

B)If majority control is not maintained but significant influence exists,the equity method to account for the investment is still used but consolidated financial statements are not required

C)If majority control is not maintained but significant influence exists,the equity method is still used to account for the investment and consolidated financial statements are still required

D)If majority control is not maintained and significant influence no longer exists,a prospective change in accounting principle to the fair value method is required

E)A gain or loss calculation must be prepared if control is lost

A)If majority control is still maintained,consolidated financial statements are still required

B)If majority control is not maintained but significant influence exists,the equity method to account for the investment is still used but consolidated financial statements are not required

C)If majority control is not maintained but significant influence exists,the equity method is still used to account for the investment and consolidated financial statements are still required

D)If majority control is not maintained and significant influence no longer exists,a prospective change in accounting principle to the fair value method is required

E)A gain or loss calculation must be prepared if control is lost

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

31

Which of the following statements is false regarding multiple acquisitions of a subsidiary's existing common stock and using the acquisition method per SFAS 141(R)?

A)The parent recognizes a larger percent of income from subsidiary

B)A step acquisition resulting in control may result in a parent recognizing a gain on revaluation

C)The book value of the subsidiary will increase

D)The parent's percent ownership in subsidiary will increase

E)Non-controlling interest in subsidiary's net income will decrease

A)The parent recognizes a larger percent of income from subsidiary

B)A step acquisition resulting in control may result in a parent recognizing a gain on revaluation

C)The book value of the subsidiary will increase

D)The parent's percent ownership in subsidiary will increase

E)Non-controlling interest in subsidiary's net income will decrease

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

32

When consolidating a subsidiary that was acquired on a date other than the first day of the fiscal year,which of the following statements is true in the presentation of consolidated financial statements?

A)Purchased pre-acquisition earnings are deducted from combined revenues and expenses

B)Purchased pre-acquisition earnings are added to combined revenues and expenses

C)Purchased pre-acquisition earnings are deducted from the beginning consolidated stockholders' equity

D)Purchased pre-acquisition earnings are added to the beginning consolidated stockholders' equity

E)Purchased pre-acquisition earnings are ignored on the consolidated income statement

A)Purchased pre-acquisition earnings are deducted from combined revenues and expenses

B)Purchased pre-acquisition earnings are added to combined revenues and expenses

C)Purchased pre-acquisition earnings are deducted from the beginning consolidated stockholders' equity

D)Purchased pre-acquisition earnings are added to the beginning consolidated stockholders' equity

E)Purchased pre-acquisition earnings are ignored on the consolidated income statement

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

33

What is consolidated current assets as of January 2,2009?

A)$138,600

B)$134,400

C)$126,000

D)$140,000

E)$127,400

A)$138,600

B)$134,400

C)$126,000

D)$140,000

E)$127,400

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

34

What is consolidated noncurrent assets as of January 2,2009?

A)$182,000

B)$190,400

C)$187,600

D)$191,333

E)$189,000

A)$182,000

B)$190,400

C)$187,600

D)$191,333

E)$189,000

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

35

When a parent uses the initial value method throughout the year to account for investment in a subsidiary,which of the following statements is true before making adjustments on the consolidated worksheet?

A)Parent company net income equals consolidated net income

B)Parent company retained earnings equals consolidated retained earnings

C)Parent company total assets equals consolidated total assets

D)Parent company dividends equals consolidated dividends

E)Goodwill is never recognized

A)Parent company net income equals consolidated net income

B)Parent company retained earnings equals consolidated retained earnings

C)Parent company total assets equals consolidated total assets

D)Parent company dividends equals consolidated dividends

E)Goodwill is never recognized

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

36

Under the purchase method of accounting for business combinations,which of the following statements is false about consolidated financial statements?

A)Holding control of a subsidiary provides the parent with an indivisible interest in that company

B)Consolidated financial statements are produced primarily for the benefit of the parent company stockholders

C)The non-controlling interest is calculated at book value amounts

D)A portion of the subsidiary net assets is valued at book value and a portion is valued at fair value

E)All of the subsidiary net assets are valued at fair value

A)Holding control of a subsidiary provides the parent with an indivisible interest in that company

B)Consolidated financial statements are produced primarily for the benefit of the parent company stockholders

C)The non-controlling interest is calculated at book value amounts

D)A portion of the subsidiary net assets is valued at book value and a portion is valued at fair value

E)All of the subsidiary net assets are valued at fair value

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

37

In consolidation at December 31,2009,what adjustment is necessary for Hogan's Buildings account?

A)$1,620 increase

B)$1,620 decrease

C)$1,800 increase

D)$1,800 decrease

E)No change

A)$1,620 increase

B)$1,620 decrease

C)$1,800 increase

D)$1,800 decrease

E)No change

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

38

When a subsidiary is acquired sometime after the first day of the fiscal year,which of the following statements is true?

A)Income from subsidiary is not recognized until there is an entire year of consolidated operations

B)Income from subsidiary is recognized from date of acquisition to year-end

C)Excess cost over acquisition value is recognized at the beginning of the fiscal year

D)No goodwill can be recognized

E)Income from subsidiary is recognized for the entire year

A)Income from subsidiary is not recognized until there is an entire year of consolidated operations

B)Income from subsidiary is recognized from date of acquisition to year-end

C)Excess cost over acquisition value is recognized at the beginning of the fiscal year

D)No goodwill can be recognized

E)Income from subsidiary is recognized for the entire year

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

39

In consolidation at January 1,2009,what adjustment is necessary for Hogan's Buildings account?

A)$2,000 increase

B)$2,000 decrease

C)$1,800 increase

D)$1,800 decrease

E)No change

A)$2,000 increase

B)$2,000 decrease

C)$1,800 increase

D)$1,800 decrease

E)No change

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

40

In a step acquisition,using the acquisition method per SFAS 141(R),which of the following statements is false?

A)The acquisition method views a step acquisition essentially the same as a single step acquisition

B)Income from subsidiary is computed by applying a partial year for a new purchase acquired during the year

C)Income from subsidiary is computed for the entire year for a new purchase acquired during the year

D)Obtaining control through a step acquisition is a significant re-measurement event

E)Pre-acquisition earnings are included on the consolidated income statement

A)The acquisition method views a step acquisition essentially the same as a single step acquisition

B)Income from subsidiary is computed by applying a partial year for a new purchase acquired during the year

C)Income from subsidiary is computed for the entire year for a new purchase acquired during the year

D)Obtaining control through a step acquisition is a significant re-measurement event

E)Pre-acquisition earnings are included on the consolidated income statement

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

41

In consolidation at January 1,2009,what adjustment is necessary for Hogan's Land account?

A)$7,000 increase

B)$7,000 decrease

C)$6,300 increase

D)$6,300 decrease

E)No change

A)$7,000 increase

B)$7,000 decrease

C)$6,300 increase

D)$6,300 decrease

E)No change

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

42

In consolidation at December 31,2009,what net adjustment is necessary for Hogan's Patent account?

A)$5,600

B)$8,800

C)$0

D)$7,700

E)$7,000

A)$5,600

B)$8,800

C)$0

D)$7,700

E)$7,000

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

43

In consolidation at December 31,2010,what adjustment is necessary for Hogan's Buildings account?

A)$1,440 increase

B)$1,440 decrease

C)$1,600 increase

D)$1,600 decrease

E)No change

A)$1,440 increase

B)$1,440 decrease

C)$1,600 increase

D)$1,600 decrease

E)No change

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

44

In consolidation at December 31,2009,what adjustment is necessary for Hogan's Land account?

A)$0

B)$7,000 increase

C)$6,300 increase

D)$6,300 decrease

E)$8,000 decrease

A)$0

B)$7,000 increase

C)$6,300 increase

D)$6,300 decrease

E)$8,000 decrease

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

45

In consolidation at December 31,2010,what net adjustment is necessary for Hogan's Patent account?

A)$4,200

B)$5,500

C)$0

D)$6,600

E)$8,8000

A)$4,200

B)$5,500

C)$0

D)$6,600

E)$8,8000

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

46

In consolidation at December 31,2010,what adjustment is necessary for Hogan's Land account?

A)$0

B)$7,000 increase

C)$6,300 increase

D)$6,300 decrease

E)$7,000 decrease

A)$0

B)$7,000 increase

C)$6,300 increase

D)$6,300 decrease

E)$7,000 decrease

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

47

In consolidation at December 31,2009,what adjustment is necessary for Hogan's Equipment account?

A)$3,000 increase

B)$3,000 decrease

C)$2,700 increase

D)$2,700 decrease

E)No change

A)$3,000 increase

B)$3,000 decrease

C)$2,700 increase

D)$2,700 decrease

E)No change

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

48

In consolidation at January 1,2009,what adjustment is necessary for Hogan's Patent account?

A)$7,000

B)$6,300

C)$0

D)$11,000

E)$9,900

A)$7,000

B)$6,300

C)$0

D)$11,000

E)$9,900

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

49

In consolidation at January 1,2009,what adjustment is necessary for Hogan's Equipment account?

A)$4,000 increase

B)$4,000 decrease

C)$3,600 increase

D)$3,600 decrease

E)No change

A)$4,000 increase

B)$4,000 decrease

C)$3,600 increase

D)$3,600 decrease

E)No change

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

50

For each of the following situations,select the best answer concerning consolidating financial information where there is a non-controlling interest in the subsidiary:

(A)Acquisition method.

(B)Purchase method.

(C)Acquisition method and Purchase method.

_____ 1.Reflects the cost principle,but also assigns a value to the non-controlling interest shares at book value.

_____ 2.Recognizes the non-controlling interest has a value to be reported,but since it is not a part of the exchange transaction,no new basis of accountability arises.

_____ 3.Recognizes that management effectively controls 100% of the net assets acquired and is thus accountable for the entire fair value.

_____ 4.Requires the computation of an implied value.

_____ 5.Recognizes the full fair value of partially owned acquisitions.

_____ 6.Non-controlling interest is reported at an implied fair value.

_____ 7.Non-controlling interest is reported at book value.

_____ 8.Required by SFAS 141(R)Business Combinations.

(A)Acquisition method.

(B)Purchase method.

(C)Acquisition method and Purchase method.

_____ 1.Reflects the cost principle,but also assigns a value to the non-controlling interest shares at book value.

_____ 2.Recognizes the non-controlling interest has a value to be reported,but since it is not a part of the exchange transaction,no new basis of accountability arises.

_____ 3.Recognizes that management effectively controls 100% of the net assets acquired and is thus accountable for the entire fair value.

_____ 4.Requires the computation of an implied value.

_____ 5.Recognizes the full fair value of partially owned acquisitions.

_____ 6.Non-controlling interest is reported at an implied fair value.

_____ 7.Non-controlling interest is reported at book value.

_____ 8.Required by SFAS 141(R)Business Combinations.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

51

In consolidation at December 31,2010,what adjustment is necessary for Hogan's Equipment account?

A)$2,000 increase

B)$2,000 decrease

C)$1,800 increase

D)$1,800 decrease

E)No change

A)$2,000 increase

B)$2,000 decrease

C)$1,800 increase

D)$1,800 decrease

E)No change

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 51 flashcards in this deck.