Deck 12: Special Property Transactions

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

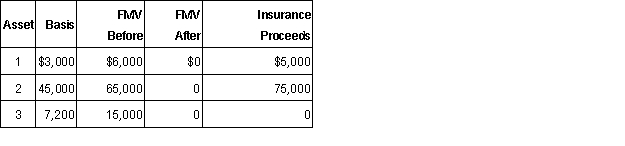

Knox operated a business which was damaged by a hurricane in 2015. His losses were as follows:  a. What is Knox's net casualty loss (if any) assuming his AGI is $85,000 prior the deduction? Assume he properly replaced all assets.

a. What is Knox's net casualty loss (if any) assuming his AGI is $85,000 prior the deduction? Assume he properly replaced all assets.

b. What is his basis in replacement Asset 1 purchased for $8,000 assuming Knox elected the non-recognition of gain from an involuntary conversion?

a. What is Knox's net casualty loss (if any) assuming his AGI is $85,000 prior the deduction? Assume he properly replaced all assets.b. What is his basis in replacement Asset 1 purchased for $8,000 assuming Knox elected the non-recognition of gain from an involuntary conversion?

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/72

Play

Full screen (f)

Deck 12: Special Property Transactions

1

The "similar or related in service or use" requirement for property involuntarily converted is less restrictive than the like-kind exchange requirements.

False

2

The exclusion of gain on the sale of a residence applies to only one sale every two years. The taxpayer is always ineligible for the exclusion if, during the two-year period ending on the date of sale of the present home, the taxpayer sold another home at a gain and excluded all or part of that gain no matter the reason for the sale.

False

3

Depreciation recapture on an asset sold using the installment method is recognized ratably as payments are received.

False

4

The installment method cannot be used to report gain from the sale of stock or securities that are traded on an established securities market.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

5

The like-kind exchange provisions are elective provisions.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

6

The IRC Section 121 exclusion of gain on the sale of a residence applies to the taxpayer's principal residence and a vacation home.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

7

The gross profit percentage is typically the gross profit divided by the contract price.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

8

A dealer of equipment can recognize gains using the installment method.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

9

Taxpayers are required to use the installment method for deferred payments unless the taxpayer elects not to use the installment method.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

10

An involuntary conversion results in money received. If the replacement property is purchased within the two-year period, the basis of the new property is its cost less the deferred gain.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

11

The adjusted basis of property received in a like-kind exchange can be calculated by taking the FMV of the property received less the gain postponed (plus loss postponed).

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

12

Exchange of one partnership interest for another partnership interest qualifies as a like-kind exchange.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

13

The receipt of boot in a like-kind exchange causes the recognition of a realized gain.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

14

To postpone any gain on an involuntary conversion, the taxpayer must purchase qualifying replacement property that is "similar or related in service or use" to the property involuntarily converted.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

15

On an involuntary conversion, gain is recognized to the extent of the lower of gain realized or the proceeds not used for replacement.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

16

The exchange of a 5-year class asset for a 7-year class asset would not qualify for "like-kind" treatment.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

17

To qualify for the IRC Section 121 exclusion of gain on the sale of a residence, the taxpayer must have lived in the home for a continuous two-year period.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

18

The replacement period for an involuntary conversion always ends two years after the close of the first taxable year in which any part of the gain is realized.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

19

If a taxpayer trades a personal-use asset for another asset, the exchange does not qualify as a like-kind exchange.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

20

The time period to replace property destroyed in an involuntary conversion is two years from the event.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

21

No deduction is allowed with respect to any loss from the sale or exchange of property, directly or indirectly, between related parties.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

22

The City of Greenville condemned 300 acres of Kayla's farmland. Kayla's land was worth $250,000 and her basis was $62,500. In payment to Kayla, the city gave Kayla 500 acres of similar land. An appraisal indicated that the land Kayla received was worth $265,000. What is Kayla's recognized gain or loss on the involuntary conversion and what is her basis in the land received?

A) $0 gain and $62,500 basis.

B) $0 gain and $262,500 basis.

C) $15,000 gain and $265,000 basis.

D)$202,500 gain and $265,000 basis.

A) $0 gain and $62,500 basis.

B) $0 gain and $262,500 basis.

C) $15,000 gain and $265,000 basis.

D)$202,500 gain and $265,000 basis.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

23

If married taxpayers live in their personal residence for more than two years, the couple can exclude a maximum of $250,000 on the gain from the sale of the residence.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

24

A barn with an adjusted basis of $125,000 was destroyed by a tornado on March 5, 2015. On May 15, 2015, the insurance company paid the owner $150,000. The owner reinvested $170,000 in another barn. What is the basis of the new barn if non-recognition of gain from an involuntary conversion is elected?

A) $0.

B) $120,000.

C) $145,000.

D)$170,000.

A) $0.

B) $120,000.

C) $145,000.

D)$170,000.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

25

An apartment building with an adjusted basis of $500,000 was destroyed by a tornado on April 30, 2015. On May 10, 2015, the insurance company paid the owner $695,000. The owner reinvested $570,000 in a new apartment complex. What is the basis of the new complex if non-recognition of gain from an involuntary conversion is elected?

A) $500,000.

B) $570,000.

C) $625,000.

D)$695,000.

A) $500,000.

B) $570,000.

C) $625,000.

D)$695,000.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

26

Gain realized on a like-kind exchange is excluded from income in all of the following circumstances except:

A) When boot is given.

B) When boot is received.

C) When a liability is assumed.

D)Both when boot is received and when a liability is assumed.

A) When boot is given.

B) When boot is received.

C) When a liability is assumed.

D)Both when boot is received and when a liability is assumed.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

27

In what instances, concerning involuntary conversions, must a taxpayer file an amended tax return (Form 1040X)?

A) When the taxpayer does not buy replacement property within the replacement period.

B) When the replacement property purchased by the taxpayer costs less than the amount realized for the converted property.

C) When the entire amount of the insurance proceeds is used to purchase replacement property.

D)Both when the taxpayer does not buy replacement property within the replacement period and when the replacement property purchased by the taxpayer costs less than the amount realized for the converted property.

A) When the taxpayer does not buy replacement property within the replacement period.

B) When the replacement property purchased by the taxpayer costs less than the amount realized for the converted property.

C) When the entire amount of the insurance proceeds is used to purchase replacement property.

D)Both when the taxpayer does not buy replacement property within the replacement period and when the replacement property purchased by the taxpayer costs less than the amount realized for the converted property.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

28

When a taxpayer is released from a liability in a like-kind exchange, the amount of the release:

A) Never triggers gain recognition.

B) Always triggers a gain to be recognized.

C) Is treated as boot and may trigger gain recognition.

D)Does not affect the like-kind exchange in any way.

A) Never triggers gain recognition.

B) Always triggers a gain to be recognized.

C) Is treated as boot and may trigger gain recognition.

D)Does not affect the like-kind exchange in any way.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

29

Ko exchanges computer equipment (five-year property) with an adjusted basis of $9,000 for a business auto (five-year property) worth $6,000. Ko also receives cash of $5,000. What are the recognized gain or loss and the basis of the new auto?

A) $0 and $9,000.

B) $0 and $6,000.

C) $2,000 and $11,000.

D)($3,000) and $12,000.

A) $0 and $9,000.

B) $0 and $6,000.

C) $2,000 and $11,000.

D)($3,000) and $12,000.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

30

The state condemned Cassidy's land on November 25, 2015. The land has a $400,000 basis. Cassidy received insurance proceeds of $610,000 on January 27, 2016. Cassidy has until what date to defer the gain under the involuntary conversion rules?

A) December 31, 2017.

B) November 25, 2017.

C) December 31, 2018.

D)December 31, 2019.

A) December 31, 2017.

B) November 25, 2017.

C) December 31, 2018.

D)December 31, 2019.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

31

The holding period of property received in a like-kind exchange:

A) Includes the holding period of the old asset exchanged.

B) Begins on the date of the exchange.

C) Begins on the date of the exchange property is identified.

D)Begins up to 180 days prior to the exchange.

A) Includes the holding period of the old asset exchanged.

B) Begins on the date of the exchange.

C) Begins on the date of the exchange property is identified.

D)Begins up to 180 days prior to the exchange.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

32

Samantha exchanges a truck used in her business with Phyllis for another truck. The basis of Samantha's old truck is $25,000, FMV is $33,000, and she gives Phyllis cash of $7,000. Phyllis's basis in her truck is $35,000 and its FMV is $40,000. What is Samantha's adjusted basis in the new truck she receives?

A) $25,000.

B) $32,000.

C) $33,000.

D)$40,000.

A) $25,000.

B) $32,000.

C) $33,000.

D)$40,000.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

33

Raymond exchanges a rental lake house with an adjusted basis of $200,000 and fair market value of $320,000 for a rental beach house with a fair market value of $290,000 and $30,000 cash. What are the recognized gain or loss and the basis of the beach house?

A) $0 gain and $230,000 basis.

B) $30,000 gain and $200,000 basis.

C) $30,000 gain and $230,000 basis.

D)$120,000 gain and $320,000 basis.

A) $0 gain and $230,000 basis.

B) $30,000 gain and $200,000 basis.

C) $30,000 gain and $230,000 basis.

D)$120,000 gain and $320,000 basis.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

34

Related parties include the taxpayer's spouse, ancestors, lineal descendants, but not brothers and sisters.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

35

With an involuntary conversion, what is the time limit to purchase replacement property?

A) Two years from the conversion event.

B) It ends two years after the close of the taxable year the gain is realized.

C) There is no time limit.

D)Five years from the conversion event.

A) Two years from the conversion event.

B) It ends two years after the close of the taxable year the gain is realized.

C) There is no time limit.

D)Five years from the conversion event.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

36

On an involuntary conversion in which the taxpayer does not buy replacement property within the replacement period, the gain on the involuntary conversion and any tax due must be reported:

A) In the year the replacement period expires.

B) In the year the involuntary conversion occurred.

C) Never, because the tax year of the conversion would be closed.

D)As soon as the taxpayer knows replacement property will not be purchased.

A) In the year the replacement period expires.

B) In the year the involuntary conversion occurred.

C) Never, because the tax year of the conversion would be closed.

D)As soon as the taxpayer knows replacement property will not be purchased.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

37

A wash sale occurs when a taxpayer sells stock or securities at a loss and, within a period of 60 days before or 60 days after the sale, the taxpayer acquires substantially identical stock or securities.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

38

The purpose of the wash sale rules is to disallow a tax loss on the sale of securities where the ownership of a company is not reduced.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

39

The property to be received in a like-kind exchange must be identified within:

A) 45 days after the transfer of the property relinquished in the exchange.

B) 90 days after the transfer of the property relinquished in the exchange.

C) 180 days after the transfer of the property relinquished in the exchange.

D)There is no time limit to identify the property to be received.

A) 45 days after the transfer of the property relinquished in the exchange.

B) 90 days after the transfer of the property relinquished in the exchange.

C) 180 days after the transfer of the property relinquished in the exchange.

D)There is no time limit to identify the property to be received.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

40

Sanjay exchanges a warehouse he uses in his rental business for a building owned by Sidney which he will use in his rental business. The adjusted basis of Sanjay's building is $320,000 and the fair market value is $500,000. The adjusted basis of Sidney's warehouse is $160,000 and the fair market value is $500,000. Which of the following statements is correct?

A) Sanjay's recognized gain is $0 and his basis for the warehouse received is $500,000.

B) Sanjay's recognized gain is $180,000 and his basis for the warehouse received is $320,000.

C) Sanjay's recognized gain is $0 and his basis for the warehouse received is $320,000.

D)Sanjay's recognized gain is $180,000 and his basis for the warehouse received is $500,000.

A) Sanjay's recognized gain is $0 and his basis for the warehouse received is $500,000.

B) Sanjay's recognized gain is $180,000 and his basis for the warehouse received is $320,000.

C) Sanjay's recognized gain is $0 and his basis for the warehouse received is $320,000.

D)Sanjay's recognized gain is $180,000 and his basis for the warehouse received is $500,000.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

41

Libby exchanges a building she uses in her rental business for a building owned by Randy which she will use in her rental business. The adjusted basis of Libby's building is $80,000 and the fair market value is $125,000. The adjusted basis of Randy's building is $40,000 and the fair market value is $125,000. What is Libby's recognized gain on the transaction and her adjusted basis in the building she receives?

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

42

A wash sale occurs when:

A) A taxpayer sells and buys substantially identical stock.

B) A taxpayer sells stock and buys substantially identical stock within 30 days before or after the sale.

C) A taxpayer sells stock and buys substantially identical stock within 60 days before or after the sale.

D)When a taxpayer sells stock at the end of the year to offset a gain recognized earlier in the year.

A) A taxpayer sells and buys substantially identical stock.

B) A taxpayer sells stock and buys substantially identical stock within 30 days before or after the sale.

C) A taxpayer sells stock and buys substantially identical stock within 60 days before or after the sale.

D)When a taxpayer sells stock at the end of the year to offset a gain recognized earlier in the year.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

43

If a taxpayer excludes the gain on the sale of his personal residence and, within two years, sells a second residence, he or she can exclude (up to $250,000 for a single taxpayer):

A) The entire gain on the second sale if the sale is due to health, employment reasons or unforeseen circumstances.

B) The entire gain for any reason.

C) A ratio of the days owned divided by 730 days and only if the sale is due to health, employment reasons or unforeseen circumstances.

D)A ratio of the days owned divided by 730 days for any reason.

A) The entire gain on the second sale if the sale is due to health, employment reasons or unforeseen circumstances.

B) The entire gain for any reason.

C) A ratio of the days owned divided by 730 days and only if the sale is due to health, employment reasons or unforeseen circumstances.

D)A ratio of the days owned divided by 730 days for any reason.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

44

All of the following taxpayers can use the installment method to report gains from the sale of assets except:

A) A taxpayer who sells a parcel of land used in his trade or business.

B) A taxpayer who sells land he inherited from his father five years ago.

C) A taxpayer who sells a large piece of manufacturing equipment on which he took a Section 179 deduction for the total cost two years ago when purchased.

D)A taxpayer who sells a building used in his trade or business for five years that was depreciated using straight-line depreciation.

A) A taxpayer who sells a parcel of land used in his trade or business.

B) A taxpayer who sells land he inherited from his father five years ago.

C) A taxpayer who sells a large piece of manufacturing equipment on which he took a Section 179 deduction for the total cost two years ago when purchased.

D)A taxpayer who sells a building used in his trade or business for five years that was depreciated using straight-line depreciation.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

45

Jane and Jason (married taxpayers) sell their personal residence in 2015. In order to exclude the maximum gain allowed for married couples on the sale of the residence, they must:

A) Have owned the home for at least two years.

B) Lived in the home as their main residence for a least two years.

C) Not have sold another primary residence in the last two years.

D)All of these.

A) Have owned the home for at least two years.

B) Lived in the home as their main residence for a least two years.

C) Not have sold another primary residence in the last two years.

D)All of these.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

46

Raymond and Susan are married and 55 years old. They sell their personal residence for $850,000 cash. They purchased the house fifteen years ago for $200,000. What is the amount of gain that Raymond and Susan should recognize on the sale?

A) $0.

B) $150,000.

C) $500,000.

D)$650,000.

A) $0.

B) $150,000.

C) $500,000.

D)$650,000.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

47

The contract price in an installment sale is:

A) The selling price or the selling price reduced by any debt assumed by the buyer.

B) The selling price less the basis in the property.

C) The selling price less any selling expenses.

D)The gross profit divided by the selling price.

A) The selling price or the selling price reduced by any debt assumed by the buyer.

B) The selling price less the basis in the property.

C) The selling price less any selling expenses.

D)The gross profit divided by the selling price.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

48

Lee sells equipment (basis $10,000) to related party, Lee Construction Inc., for $6,000. The $4,000 loss is:

A) Deductible by Lee on his individual return.

B) Not deductible by Lee but Lee Construction has a basis of $10,000 in the asset.

C) Not deductible by Lee but Lee Construction has a basis of $6,000 in the asset.

D)None of these.

A) Deductible by Lee on his individual return.

B) Not deductible by Lee but Lee Construction has a basis of $10,000 in the asset.

C) Not deductible by Lee but Lee Construction has a basis of $6,000 in the asset.

D)None of these.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

49

When a loss is disallowed under the related party loss rules, the loss:

A) Is carried forward indefinitely.

B) Reduces the subsequent gain when the related party sells the asset.

C) Is lost forever even if the related party sells the asset at a gain.

D)None of these.

A) Is carried forward indefinitely.

B) Reduces the subsequent gain when the related party sells the asset.

C) Is lost forever even if the related party sells the asset at a gain.

D)None of these.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

50

Which of the following relationships are considered related parties?

A) A brother and sister.

B) A corporation and a 100% shareholder.

C) A partnership and a 66% partner.

D)All of these are related parties.

A) A brother and sister.

B) A corporation and a 100% shareholder.

C) A partnership and a 66% partner.

D)All of these are related parties.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

51

Jasmine sold land for $250,000 in 2015. The land had a basis of $118,000 and she incurred selling expenses of $10,000. Jasmine received $50,000 down in 2015 and will receive five additional annual payments of $40,000 each. How much income will Jasmine recognize in 2016 when she receives the first additional payment of $40,000?

A) $0.

B) $18,880.

C) $19,520.

D)$40,000.

A) $0.

B) $18,880.

C) $19,520.

D)$40,000.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

52

When a loss is disallowed under the wash sale rules,

A) The loss is lost forever.

B) The loss is carried over indefinitely.

C) The loss is added to the basis of the newly acquired stock.

D)None of these.

A) The loss is lost forever.

B) The loss is carried over indefinitely.

C) The loss is added to the basis of the newly acquired stock.

D)None of these.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

53

Jasmine sold land for $250,000 in 2015. The land had a basis of $118,000 and she incurred selling expenses of $10,000. Jasmine received $50,000 cash down in 2015 and will receive five additional annual payments of $40,000 each. What is Jasmine's gross profit percentage on the sale?

A) 47.2%.

B) 48.8%.

C) 51.2%.

D)100.0%.

A) 47.2%.

B) 48.8%.

C) 51.2%.

D)100.0%.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

54

The installment method cannot be used to report the gain on which of the following assets?

A) Land used in a trade or business.

B) Stock traded on a securities market.

C) Building used in a trade or business.

D)Stock in a privately-held business.

A) Land used in a trade or business.

B) Stock traded on a securities market.

C) Building used in a trade or business.

D)Stock in a privately-held business.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

55

Pierre sold a parcel of land for $50,000. He received $10,000 this year and signs a contract to receive four additional payments of $10,000 each plus interest. If Pierre had a basis in the land of $10,000 and incurred $2,500 in selling expenses, what is his gross profit percentage?

A) 10%.

B) 25%.

C) 75%.

D)100%.

A) 10%.

B) 25%.

C) 75%.

D)100%.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

56

The ownership test for the sale of a personal residence states:

A) That a taxpayer must have owned the home for at least two years.

B) That a taxpayer must have lived in the home for at least two years.

C) That a taxpayer be the original owner of the residence.

D)None of these.

A) That a taxpayer must have owned the home for at least two years.

B) That a taxpayer must have lived in the home for at least two years.

C) That a taxpayer be the original owner of the residence.

D)None of these.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

57

Julia exchanges a machine used in her business with Elvira for another machine. The basis of Julia's old machine is $100,000, FMV is $132,000, and she gives Elvira cash of $28,000. Elvira's basis in her machine is $140,000 and the FMV is $160,000. What, if any, gain is recognized on the transaction and what is the adjusted basis of the property received by Julia and by Elvira?

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

58

Matt and Opal were married in April of 2015. Matt has lived in his personal residence for fifteen years and Opal moved into the house after the marriage. Matt died in October 2015. Opal sold the house at a $300,000 gain in December, 2015. How much of the gain can Opal exclude?

A) $0.

B) $250,000.

C) $300,000.

D)None of these.

A) $0.

B) $250,000.

C) $300,000.

D)None of these.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

59

If one spouse sells a home and excludes the gain on the sale, the gain on the sale of a residence by the other spouse is:

A) Never excluded.

B) Excluded up to $500,000.

C) Excluded up to $250,000.

D)Excluded up to $250,000 plus any gain exclusion not used by the first spouse.

A) Never excluded.

B) Excluded up to $500,000.

C) Excluded up to $250,000.

D)Excluded up to $250,000 plus any gain exclusion not used by the first spouse.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

60

Tanner, who is single, purchased a house on April 15, 2001 for $215,000. During the time Tanner owned the house, he installed a swimming pool at a cost of $21,000 and replaced the deck at a cost of $18,000. On August 5, 2015, Tanner sold the house for $570,000. Tanner paid a sales commission of $30,000 and legal fees of $800 connected with the sale of the house. What is Tanner's recognized gain on the sale of the house?

A) $0.

B) $35,200.

C) $250,000.

D)$285,200.

A) $0.

B) $35,200.

C) $250,000.

D)$285,200.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

61

On June 15, 2015, Roco sold land held for investment to Scotty for $100,000 cash and an installment note of $500,000 payable in five equal annual installments beginning on June 15, 2016, plus interest at 10%. Roco's basis in the land is $300,000. What amount of gain is recognized in 2015 under the installment method?

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

62

Louis, who is single, sold his house in St. Louis at a gain of $240,000 on June 8, 2015. He properly excluded the gain. He took another job in Memphis. He purchased a new home in Memphis for $225,000 on August 5, 2015. Louis was transferred by his employer to New Orleans. Louis sold his Memphis house at a $36,000 gain on October 15, 2015. What is Louis's recognized gain on the Memphis house?

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

63

Richard's business is condemned by the state on July 10, 2015, as part of a plan to add a highway loop around the city. His adjusted basis in his business is $500,000. He receives condemnation proceeds of $610,000 on August 30, 2015. He purchases another business for $575,000 on September 15, 2015.

a. What is Richard's realized and recognized gain or loss?

b. What is Richard's basis in the new business?

a. What is Richard's realized and recognized gain or loss?

b. What is Richard's basis in the new business?

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

64

Basil, who is single, purchased a house on May 10, 1982, for $175,000. During the years Basil owned the house, he installed a pool at a cost of $20,000 and built a new garage at a cost of $20,000. On October 12, 2015, Basil sold the house for $518,000. Basil paid a sales commission of $24,600 and legal fees of $400 connected with the sale of the house. What is Basil's recognized gain on the sale of the house?

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

65

A warehouse with an adjusted basis of $125,000 was destroyed by a tornado on April 15, 2016. On June 15, 2016, the insurance company paid the owner $195,000. The owner reinvested $170,000 in a warehouse. What is the basis of the new warehouse if non-recognition of gain from an involuntary conversion is elected?

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

66

Edith owns farm land in western Montana. Her adjusted basis is $300,000 and the land is subject to a mortgage of $150,000. She exchanges her land for investment land in Wyoming owned by Dale. The investment land is worth $450,000. Dale assumes Edith's mortgage on the land. What is the amount of Edith's recognized gain or loss on the exchange and what is her adjusted basis in the land she received?

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

67

Dr. and Mrs. Spankle purchased a residence on January 12, 2011, for $250,000. On May 15, 2015, they sold the residence for $360,000, and paid selling expenses of $18,000. They purchased a new home for $354,000. Determine the Spankles' realized and recognized gain.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

68

Knox operated a business which was damaged by a hurricane in 2015. His losses were as follows: a. What is Knox's net casualty loss (if any) assuming his AGI is $85,000 prior the deduction? Assume he properly replaced all assets.

b. What is his basis in replacement Asset 1 purchased for $8,000 assuming Knox elected the non-recognition of gain from an involuntary conversion?

a. What is Knox's net casualty loss (if any) assuming his AGI is $85,000 prior the deduction? Assume he properly replaced all assets.b. What is his basis in replacement Asset 1 purchased for $8,000 assuming Knox elected the non-recognition of gain from an involuntary conversion?

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

69

On July 1, 2015, DJ sold equipment used in her business and reported the gain using the installment method. Her adjusted basis in the equipment was $150,000. The equipment was subject to $30,000 of depreciation recapture. DJ sold the property for $250,000, with $100,000 due on the date of the sale and $150,000 (plus interest at the Federal rate) due on August 1, 2016. What is the amount of gain recognized in 2015?

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

70

On December 28, 2015, Misty sold 300 shares of Low Grade, Inc. (a publicly traded company) at a loss of $8,500. On January 5, 2016, thinking that the stock price would rebound, Misty purchased 200 shares of Low Grade, Inc. for $7,000. What is the amount of the recognized loss on the December 28, 2015 sale and what is Misty's basis in the 200 shares she purchased on January 5, 2016?

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

71

Laverne exchanges a rental beach house with an adjusted basis of $400,000 and fair market value of $320,000 for a mini-storage building with a fair market value of $200,000 plus $120,000 cash. What is the recognized gain or loss on the exchange and the basis of the mini-storage building?

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

72

On February 12, 2015, Nelson sells stock (basis $175,000) to his son Wayne for $150,000, the stock's fair market value on the date of the sale. On October 21, 2015, Wayne sells the stock to an unrelated party. In each of the following independent cases, determine the tax consequences of the transactions to Nelson and Wayne.

a. Wayne sells the stock for $140,000.

b. Wayne sells the stock for $180,000.

c. Wayne sells the stock for $165,000.

a. Wayne sells the stock for $140,000.

b. Wayne sells the stock for $180,000.

c. Wayne sells the stock for $165,000.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 72 flashcards in this deck.