Deck 3: Business Combinations

Full screen (f)

Question

Question

Question

Question

Question

Question

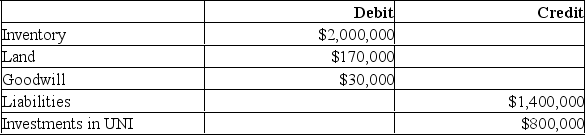

IOU Inc. purchased all of the outstanding common shares of UNI Inc. for cash of $800,000. On the date of acquisition, UNI's assets included $2,000,000 of Inventory, and Land with a Book value of $120,000. UNI also had $1,400,000 in Liabilities on that date. UNI's book values were equal to their fair market values, with the exception of the company's Land, which was estimated to have a fair market value which was $50,000 higher than its book value. Assuming that the purchase of the common shares of UNI Inc. was properly recorded at cost, which of the following journal entries is required to prepare Consolidated Financial Statements the day following the acquisition?

A)

B)

C)

D) No entry.

A)

B)

C)

D) No entry.

Question

Question

Question

Question

Question

Question

Question

Question

Question

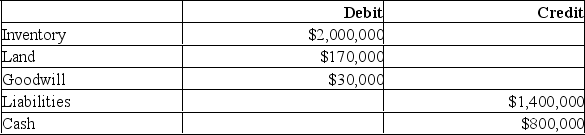

IOU Inc. purchased all of the outstanding common shares of UNI Inc. for cash of $800,000. On the date of acquisition, UNI's assets included $2,000,000 of Inventory and Land with a Book value of $120,000. UNI also had $1,400,000 in Liabilities on that date. UNI's book values were equal to their fair market values, with the exception of the company's Land, which was estimated to have a fair market value which was $50,000 higher than its book value.

Which of the following is the correct journal entry to record IOU's acquisition of UNI?

A.

B.

C.

D. No entry.

Which of the following is the correct journal entry to record IOU's acquisition of UNI?

A.

B.

C.

D. No entry.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

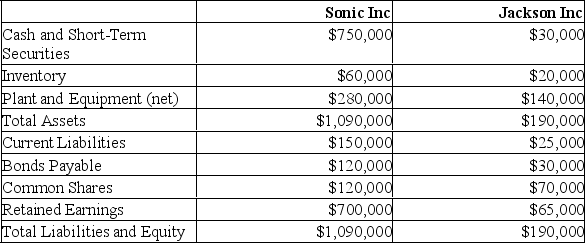

Sonic Enterprises Inc has decided to purchase 100% of the voting shares of Jackson Inc. for $300,000 in cash on May 1, 2019. On the date, the balance sheets of each of these companies were as follows:

On that date, the fair values of Jackson's assets and liabilities were as follows:

On that date, the fair values of Jackson's assets and liabilities were as follows:

Sonic's Book Values approximated their Fair Values on that date.

Sonic's Book Values approximated their Fair Values on that date.

Required:

a) Calculate the amount of Goodwill arising from this combination.

b) Prepare the journal entry to record Sonic's acquisition of Jackson's Shares.

c) Prepare Sonic's Consolidated Balance Sheet immediately following its acquisition of Jackson's assets.

On that date, the fair values of Jackson's assets and liabilities were as follows: Sonic's Book Values approximated their Fair Values on that date.Required:

a) Calculate the amount of Goodwill arising from this combination.

b) Prepare the journal entry to record Sonic's acquisition of Jackson's Shares.

c) Prepare Sonic's Consolidated Balance Sheet immediately following its acquisition of Jackson's assets.

Question

Question

Question

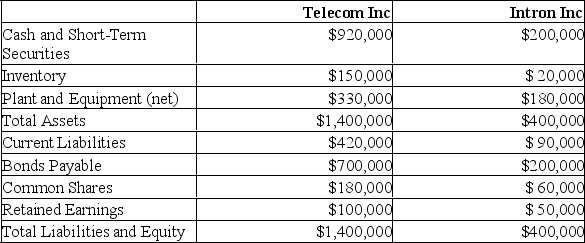

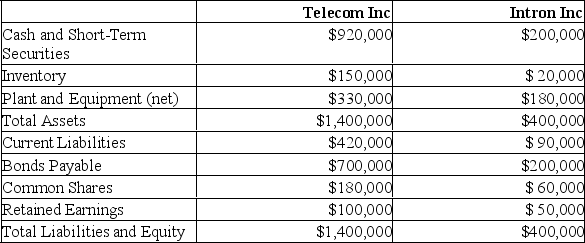

Telecom Inc has decided to purchase the shares of Intron Inc. for $300,000 in cash on July 1, 2019. On the date, the balance sheets of each of these companies were as follows:

On that date, the fair values of Intron's assets and liabilities were as follows:

On that date, the fair values of Intron's assets and liabilities were as follows:

Required:

Required:

Based on the information provided, answer the following:

a) Prepare the journal entry to record the purchases Intron's shares.

b) Prepare the consolidation entries (eliminating entries) that are required to prepare the Consolidated Financial Statements.

On that date, the fair values of Intron's assets and liabilities were as follows: Required:Based on the information provided, answer the following:

a) Prepare the journal entry to record the purchases Intron's shares.

b) Prepare the consolidation entries (eliminating entries) that are required to prepare the Consolidated Financial Statements.

Question

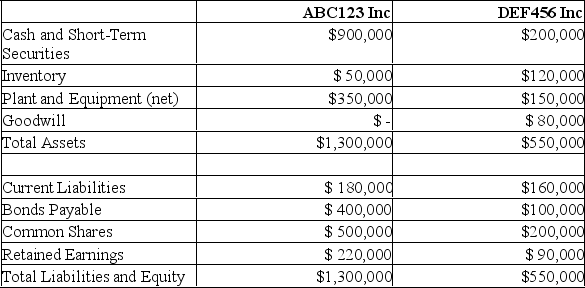

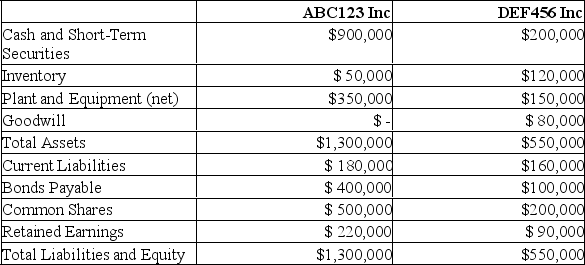

ABC123 Inc has decided to purchase 100% the voting shares of DEF456 for $400,000 in cash on July 1, 2019. On the date, the balance sheets of each of these companies were as follows:

On that date, the fair values of DEF456 Assets and Liabilities were as follows:

On that date, the fair values of DEF456 Assets and Liabilities were as follows:

In addition to the above, an independent appraiser deemed that DEF456 Inc. had trademarks with a fair market value of $100,000 which had not been accounted for. In turn, ABC123's fair market values were equal to their book values with the exception of the Company's Inventory and Plant and Equipment, which were said to have Fair Market Values of $30,000 and $480,000, respectively.

In addition to the above, an independent appraiser deemed that DEF456 Inc. had trademarks with a fair market value of $100,000 which had not been accounted for. In turn, ABC123's fair market values were equal to their book values with the exception of the Company's Inventory and Plant and Equipment, which were said to have Fair Market Values of $30,000 and $480,000, respectively.

Based on the information provided:

a) Calculate the amount of Goodwill arising from this combination.

b) Prepare the journal entry to record ABC123's acquisition of DEF456's shares.

c) Prepare ABC123's Consolidated Balance Sheet immediately following its acquisition of DEF123's voting shares.

On that date, the fair values of DEF456 Assets and Liabilities were as follows: In addition to the above, an independent appraiser deemed that DEF456 Inc. had trademarks with a fair market value of $100,000 which had not been accounted for. In turn, ABC123's fair market values were equal to their book values with the exception of the Company's Inventory and Plant and Equipment, which were said to have Fair Market Values of $30,000 and $480,000, respectively.Based on the information provided:

a) Calculate the amount of Goodwill arising from this combination.

b) Prepare the journal entry to record ABC123's acquisition of DEF456's shares.

c) Prepare ABC123's Consolidated Balance Sheet immediately following its acquisition of DEF123's voting shares.

Question

Question

Question

Question

Question

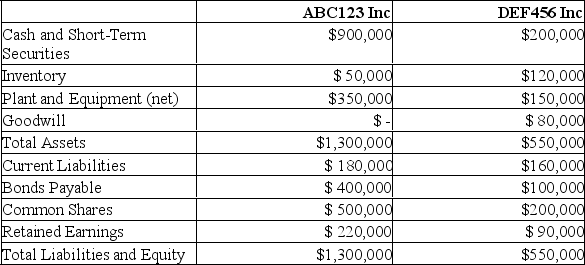

ABC123 Inc has decided to purchase 100% of the voting shares of DEF456 for $400,000 in Cash on July 1, 2019. On the date, the balance sheets of each of these companies were as follows:

On that date, the fair values of DEF456 Assets and Liabilities were as follows:

On that date, the fair values of DEF456 Assets and Liabilities were as follows:

In addition to the above, an independent appraiser deemed that DEF456 Inc. had trademarks with a fair market value of $100,000 which had not been accounted for. In turn, ABC123's fair market values were equal to their book values with the exception of the Company's Inventory and Plant and Equipment, which were said to have Fair Market Values of $30,000 and $480,000, respectively.

In addition to the above, an independent appraiser deemed that DEF456 Inc. had trademarks with a fair market value of $100,000 which had not been accounted for. In turn, ABC123's fair market values were equal to their book values with the exception of the Company's Inventory and Plant and Equipment, which were said to have Fair Market Values of $30,000 and $480,000, respectively.

Prepare any disclosure required for ABC123 Inc. under IFRS. Assume DEF456 has a reliable and specialized workforce that produces high-end loudspeakers for touring musicians and that ABC123 manufactures stage equipment needed for live music performances.

On that date, the fair values of DEF456 Assets and Liabilities were as follows: In addition to the above, an independent appraiser deemed that DEF456 Inc. had trademarks with a fair market value of $100,000 which had not been accounted for. In turn, ABC123's fair market values were equal to their book values with the exception of the Company's Inventory and Plant and Equipment, which were said to have Fair Market Values of $30,000 and $480,000, respectively.Prepare any disclosure required for ABC123 Inc. under IFRS. Assume DEF456 has a reliable and specialized workforce that produces high-end loudspeakers for touring musicians and that ABC123 manufactures stage equipment needed for live music performances.

Question

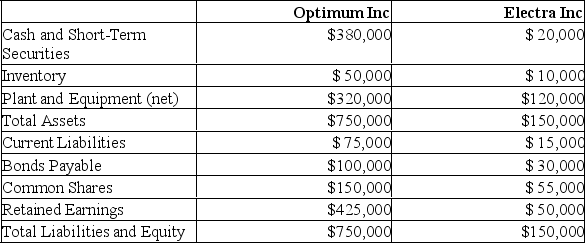

On April 1, 2019, the balance sheets of Optimum Inc. and Electra Inc. were as follows:

On that date, the fair values of Electra's Assets and Liabilities were as follows:

On that date, the fair values of Electra's Assets and Liabilities were as follows:

On April 1, 2019, Optimum issued 5,000 new common shares with a market value of $50.00 per share as consideration for Electra's net assets. Prior to the issue, Optimum had 10,000 outstanding common shares.

On April 1, 2019, Optimum issued 5,000 new common shares with a market value of $50.00 per share as consideration for Electra's net assets. Prior to the issue, Optimum had 10,000 outstanding common shares.

Required:

a) Calculate the amount of Goodwill arising from this combination.

b) Prepare the journal entry to record Optimum's acquisition of Electra's assets.

c) Prepare Optimum's Consolidated Balance Sheet immediately following its acquisition of Electra's assets.

d) Prepare Electra's Balance Sheet following the acquisition.

On that date, the fair values of Electra's Assets and Liabilities were as follows: On April 1, 2019, Optimum issued 5,000 new common shares with a market value of $50.00 per share as consideration for Electra's net assets. Prior to the issue, Optimum had 10,000 outstanding common shares.Required:

a) Calculate the amount of Goodwill arising from this combination.

b) Prepare the journal entry to record Optimum's acquisition of Electra's assets.

c) Prepare Optimum's Consolidated Balance Sheet immediately following its acquisition of Electra's assets.

d) Prepare Electra's Balance Sheet following the acquisition.

Question

Question

Question

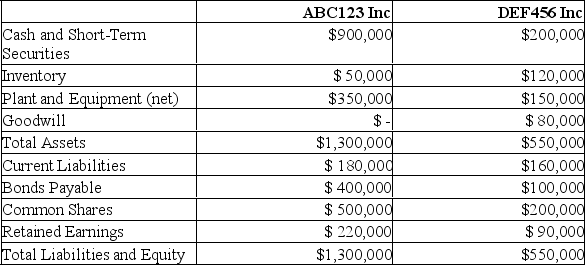

ABC123 Inc has decided to purchase 100% the voting shares of DEF456 by issuing common shares with a market value of $400,000 on July 1, 2019. On the date, the balance sheets of each of these companies were as follows:

On that date, the fair values of DEF456 Assets and Liabilities were as follows:

On that date, the fair values of DEF456 Assets and Liabilities were as follows:

In addition to the above, an independent appraiser deemed that DEF456 Inc. had trademarks with a fair market value of $100,000 which had not been accounted for.

In addition to the above, an independent appraiser deemed that DEF456 Inc. had trademarks with a fair market value of $100,000 which had not been accounted for.

Based on the information provided:

a) Calculate the amount of Goodwill arising from this combination.

b) Prepare the journal entry to record ABC123's acquisition of DEF456's shares.

c) Prepare ABC123's Consolidated Balance Sheet immediately following its acquisition of DEF123's voting shares.

On that date, the fair values of DEF456 Assets and Liabilities were as follows: In addition to the above, an independent appraiser deemed that DEF456 Inc. had trademarks with a fair market value of $100,000 which had not been accounted for.Based on the information provided:

a) Calculate the amount of Goodwill arising from this combination.

b) Prepare the journal entry to record ABC123's acquisition of DEF456's shares.

c) Prepare ABC123's Consolidated Balance Sheet immediately following its acquisition of DEF123's voting shares.

Question

Question

ABC123 Inc has decided to purchase 100% the voting shares of DEF456 for $400,000 in Cash on July 1, 2018. On the date, the balance sheets of each of these companies were as follows:

On that date, the fair values of DEF456 Assets and Liabilities were as follows:

On that date, the fair values of DEF456 Assets and Liabilities were as follows:

In addition to the above, an independent appraiser deemed that DEF456 Inc. had trademarks with a fair market value of $100,000 which had not been accounted for. In turn, ABC123's fair market values were equal to their book values with the exception of the Company's Inventory and Plant and Equipment, which were said to have Fair Market Values of $30,000 and $480,000, respectively.

In addition to the above, an independent appraiser deemed that DEF456 Inc. had trademarks with a fair market value of $100,000 which had not been accounted for. In turn, ABC123's fair market values were equal to their book values with the exception of the Company's Inventory and Plant and Equipment, which were said to have Fair Market Values of $30,000 and $480,000, respectively.

Calculate the goodwill arising from this business combination and state how it would be shown in the consolidated balance sheet on the acquisition date.

On that date, the fair values of DEF456 Assets and Liabilities were as follows: In addition to the above, an independent appraiser deemed that DEF456 Inc. had trademarks with a fair market value of $100,000 which had not been accounted for. In turn, ABC123's fair market values were equal to their book values with the exception of the Company's Inventory and Plant and Equipment, which were said to have Fair Market Values of $30,000 and $480,000, respectively.Calculate the goodwill arising from this business combination and state how it would be shown in the consolidated balance sheet on the acquisition date.

Question

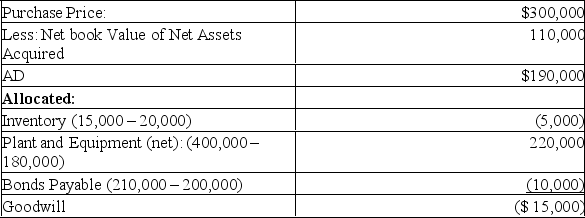

Telecom Inc has decided to purchase the shares of Intron Inc. for $300, 000 in Cash on July 1, 2019. On the date, the balance sheets of each of these companies were as follows:

On that date, the fair values of Intron's assets and liabilities were as follows:

On that date, the fair values of Intron's assets and liabilities were as follows:

Required:

Required:

Prepare the Consolidated Balance Sheet on date of acquisition.

Calculation and Allocation of Acquisition Differential:

On that date, the fair values of Intron's assets and liabilities were as follows: Required:Prepare the Consolidated Balance Sheet on date of acquisition.

Calculation and Allocation of Acquisition Differential:

Question

Question

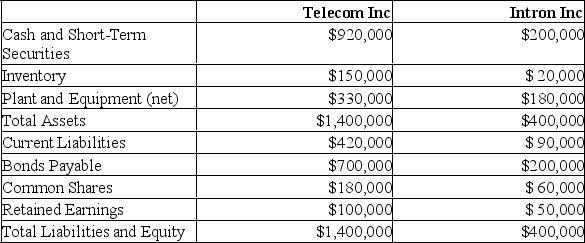

Telecom Inc has decided to purchase the net assets of Intron Inc. for $300, 000 in cash on July 1, 2019. On the date, the balance sheets of each of these companies were as follows:

On that date, the fair values of Intron's assets and liabilities were as follows:

On that date, the fair values of Intron's assets and liabilities were as follows:

Required:

Required:

Prepare the journal entry to record this purchase.

On that date, the fair values of Intron's assets and liabilities were as follows: Required:Prepare the journal entry to record this purchase.

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/61

Play

Full screen (f)

Deck 3: Business Combinations

1

IOU Inc. purchased all of the outstanding common shares of UNI Inc. for cash of $800,000. On the date of acquisition, UNI's assets included $2,000,000 of inventory, and land with a book value of $120,000. UNI also had $1,400,000 in liabilities on that date. UNI's book values were equal to their fair market values, with the exception of the company's land, which was estimated to have a fair market value which was $50,000 higher than its book value. How much goodwill would be created by IOU's acquisition of UNI?

A) $30,000

B) $50,000

C) $80,000

D) Nil

A) $30,000

B) $50,000

C) $80,000

D) Nil

A

2

How should intangible assets which are readily identifiable but not accurately measured be accounted for?

A) They should be ignored since they can't be accurately measured.

B) They should be independently appraised and accounted for at their appraised value.

C) They should be included in Goodwill.

D) They should be accounted for at an amount deemed reasonable by management.

A) They should be ignored since they can't be accurately measured.

B) They should be independently appraised and accounted for at their appraised value.

C) They should be included in Goodwill.

D) They should be accounted for at an amount deemed reasonable by management.

C

3

The process of preparing Consolidated Financial Statements involves the elimination of inter-company transactions between a Parent Company and its subsidiary. Where would these entries be recorded?

A) On the Parent's books only.

B) On the Subsidiary's books.

C) The entries are not recorded in the books of either company. The entries are only made on the working papers.

D) The effect of any inter-company transaction must be reflected on the books of both companies.

A) On the Parent's books only.

B) On the Subsidiary's books.

C) The entries are not recorded in the books of either company. The entries are only made on the working papers.

D) The effect of any inter-company transaction must be reflected on the books of both companies.

C

4

Parent and Sub Inc. had the following balance sheets on December 31, 2019: On January 1, 2020, Parent purchased all of Sub Inc.'s Common Shares for $40,000 in cash. On that date, Sub's Current Assets and Fixed Assets were worth $26,000 and $54,000, respectively. Assuming that Consolidated Financial Statements were prepared on that date, answer the following:

The Shareholders' Equity section of the Consolidated Balance Sheet would show what amount?

A) $19,000

B) $90,000

C) $98,000

D) $121,000

The Shareholders' Equity section of the Consolidated Balance Sheet would show what amount?

A) $19,000

B) $90,000

C) $98,000

D) $121,000

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

5

During an acquisition, when should intangible assets NOT be recognized apart from Goodwill?

A) The assets have been identified but not accounted for by the subsidiary.

B) The assets have been identified and accounted for by the subsidiary.

C) The assets can be sold, licensed or exchanged.

D) The assets have been accounted for by the subsidiary but have no Fair Value on the date of acquisition.

A) The assets have been identified but not accounted for by the subsidiary.

B) The assets have been identified and accounted for by the subsidiary.

C) The assets can be sold, licensed or exchanged.

D) The assets have been accounted for by the subsidiary but have no Fair Value on the date of acquisition.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

6

IOU Inc. purchased all of the outstanding common shares of UNI Inc. for cash of $800,000. On the date of acquisition, UNI's assets included $2,000,000 of Inventory, and Land with a Book value of $120,000. UNI also had $1,400,000 in Liabilities on that date. UNI's book values were equal to their fair market values, with the exception of the company's Land, which was estimated to have a fair market value which was $50,000 higher than its book value. Assuming that the purchase of the common shares of UNI Inc. was properly recorded at cost, which of the following journal entries is required to prepare Consolidated Financial Statements the day following the acquisition?

A)

B)

C)

D) No entry.

A)

B)

C)

D) No entry.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

7

The IASB standard (IFRS 3 Business Combinations) issued with respect to the treatment of negative goodwill requires that:

A) it must be recognized in income immediately as an extraordinary item.

B) it must be recognized in income immediately.

C) it can be deferred and amortized over a maximum of 40 years.

D) it must be reflected as an increase in Liabilities and a Reduction in Capital for the Parent Company.

A) it must be recognized in income immediately as an extraordinary item.

B) it must be recognized in income immediately.

C) it can be deferred and amortized over a maximum of 40 years.

D) it must be reflected as an increase in Liabilities and a Reduction in Capital for the Parent Company.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

8

Which of the following would NOT be included in the acquisition cost?

A) Share issue costs.

B) Fair value of any shares issued.

C) Fair value of contingent consideration.

D) Fair value of assets transferred.

A) Share issue costs.

B) Fair value of any shares issued.

C) Fair value of contingent consideration.

D) Fair value of assets transferred.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

9

Company Y purchases a controlling interest in Company Z on January 1, 2019. Which of the following would appear as the Shareholders' Equity amount on Company Y's Consolidated Balance Sheet on the date of acquisition?

A) Company Y's Shareholders' Equity.

B) The sum of the Shareholders' Equity of both companies.

C) Company Y's Shareholders' Equity as well as Company Y's proportional share of Company Z's net assets at book value.

D) Company Y's Shareholders' Equity as well as Company Y's proportional share of Company Z's net assets at fair market value.

A) Company Y's Shareholders' Equity.

B) The sum of the Shareholders' Equity of both companies.

C) Company Y's Shareholders' Equity as well as Company Y's proportional share of Company Z's net assets at book value.

D) Company Y's Shareholders' Equity as well as Company Y's proportional share of Company Z's net assets at fair market value.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

10

On January 1, 2019, A Company issued 6,000 new common shares to the shareholders of B Corporation for all of their shares in B Corporation. Prior to the new share issuance by A Company, it had 5,000 common shares issued and outstanding. The former shareholders of B Corporation would now own 55% (6,000/11,000) of the outstanding shares. What is the outcome of this transaction?

A) The legal parent, A Company, is treated as the subsidiary and the legal subsidiary, B Corporation, is treated as the parent for reporting purposes. Therefore, the consolidated balance sheet would incorporate B Corporation's net assets at carrying value and A Company's net assets at fair value.

B) Since A Company shares were issued to the shareholders of B Company for the purchase, A Company will be the parent company and B Corporation, the subsidiary for reporting purposes. Therefore, the consolidated balance sheet would incorporate A Company's net assets at carrying value and B Corporation's net assets at fair value.

C) Since neither A Company nor B Corporation can be identified as the acquirer, the consolidated balance sheet would incorporate A Company's net assets at carrying value and B Corporation's net assets at carrying value.

D) Since neither A Company nor B Corporation can be identified as the acquirer, consolidated financial statements are not required. Each entity is only required to prepare separate entity financial statements

A) The legal parent, A Company, is treated as the subsidiary and the legal subsidiary, B Corporation, is treated as the parent for reporting purposes. Therefore, the consolidated balance sheet would incorporate B Corporation's net assets at carrying value and A Company's net assets at fair value.

B) Since A Company shares were issued to the shareholders of B Company for the purchase, A Company will be the parent company and B Corporation, the subsidiary for reporting purposes. Therefore, the consolidated balance sheet would incorporate A Company's net assets at carrying value and B Corporation's net assets at fair value.

C) Since neither A Company nor B Corporation can be identified as the acquirer, the consolidated balance sheet would incorporate A Company's net assets at carrying value and B Corporation's net assets at carrying value.

D) Since neither A Company nor B Corporation can be identified as the acquirer, consolidated financial statements are not required. Each entity is only required to prepare separate entity financial statements

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

11

Parent and Sub Inc. had the following balance sheets on December 31, 2019: On January 1, 2020, Parent purchased all of Sub Inc.'s Common Shares for $40,000 in cash. On that date, Sub's Current Assets and Fixed Assets were worth $26,000 and $54,000, respectively. Assuming that Consolidated Financial Statements were prepared on that date, answer the following:

The Current Assets of the combined entity should be valued at:

A) $70,000

B) $46,000

C) $114,000

D) $170,000

The Current Assets of the combined entity should be valued at:

A) $70,000

B) $46,000

C) $114,000

D) $170,000

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

12

How should the acquisition cost of a Business Combination be allocated prior to preparing Consolidated Financial Statements?

A) The acquisition cost should be allocated to the acquiree's book value.

B) The acquisition cost should be allocated to the acquired company's identifiable assets and liabilities to bring them to their fair value.

C) The acquisition cost should be reflected as an increase in the acquirer's Investment (in the subsidiary) account.

D) The treatment of the acquisition cost depends largely on the type of consideration given by the acquirer.

A) The acquisition cost should be allocated to the acquiree's book value.

B) The acquisition cost should be allocated to the acquired company's identifiable assets and liabilities to bring them to their fair value.

C) The acquisition cost should be reflected as an increase in the acquirer's Investment (in the subsidiary) account.

D) The treatment of the acquisition cost depends largely on the type of consideration given by the acquirer.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

13

IFRS 10 Consolidated Financial Statements outlines the requirements for identifying the company that is the acquirer in a business combination when it's not clear who that is. Which is NOT a consideration in determining which company is the acquirer?

A) If the means of payment is cash, which party is paying the cash.

B) Relative holdings of voting shares in the combined entity.

C) Voting rights of the respective parties after the combination of their businesses.

D) Any by-laws or provisions of the incorporation acts of each company that details the manner in which a business combination will occur at law.

A) If the means of payment is cash, which party is paying the cash.

B) Relative holdings of voting shares in the combined entity.

C) Voting rights of the respective parties after the combination of their businesses.

D) Any by-laws or provisions of the incorporation acts of each company that details the manner in which a business combination will occur at law.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

14

Which of the following regarding the preparation of Consolidated Financial Statement is correct?

A) Once the parent company prepares Consolidated Financial Statements, it no longer needs to prepare financial statements for its own activities.

B) Only the subsidiaries are required to prepare Financial Statements.

C) Consolidated Financial Statements are required by the Parent Company for reporting purposes only; each company must continue to prepare its own Financial Statements.

D) Consolidated Financial Statements are required only when both companies are publicly traded.

A) Once the parent company prepares Consolidated Financial Statements, it no longer needs to prepare financial statements for its own activities.

B) Only the subsidiaries are required to prepare Financial Statements.

C) Consolidated Financial Statements are required by the Parent Company for reporting purposes only; each company must continue to prepare its own Financial Statements.

D) Consolidated Financial Statements are required only when both companies are publicly traded.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

15

IOU Inc. purchased all of the outstanding common shares of UNI Inc. for cash of $800,000. On the date of acquisition, UNI's assets included $2,000,000 of Inventory and Land with a Book value of $120,000. UNI also had $1,400,000 in Liabilities on that date. UNI's book values were equal to their fair market values, with the exception of the company's Land, which was estimated to have a fair market value which was $50,000 higher than its book value.

Which of the following is the correct journal entry to record IOU's acquisition of UNI?

A.

B.

C.

D. No entry.

Which of the following is the correct journal entry to record IOU's acquisition of UNI?

A.

B.

C.

D. No entry.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

16

Company A has made an offer to purchase all of the outstanding shares of Company B for $10 per share (the current market value of the shares). In response to Company A's offer, the shareholders of Company B were given rights to purchase additional shares at $8 per share. Which of the following tactics were employed by Company B to prevent Company A from acquiring control of Company B?

A) Pac-man defence.

B) Selling the crown jewels.

C) Poison Pill.

D) Reverse-takeover.

A) Pac-man defence.

B) Selling the crown jewels.

C) Poison Pill.

D) Reverse-takeover.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

17

IOU Inc. purchased all of the outstanding common shares of UNI Inc. for cash of $800,000. On the date of acquisition, UNI's assets included $2,000,000 of Inventory, and Land with a Book value of $120,000. UNI also had $1,400,000 in Liabilities on that date. UNI's book values were equal to their fair market values, with the exception of the company's Land, which was estimated to have a fair market value which was $50,000 higher than its book value. UNI also had patent rights with a fair market value on acquisition date of $20,000 that were not shown on its balance sheet because the rights had been developed internally. How much goodwill would be created by IOU's acquisition of UNI?

A) $30,000

B) $10,000

C) $70,000

D) $80,000

A) $30,000

B) $10,000

C) $70,000

D) $80,000

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

18

Which of the following pertaining to Consolidated Financial Statements is correct?

A) The preparation of Consolidated Financial Statements means that the companies involved cease to operate as separate legal entities.

B) The preparation of Consolidated Financial Statements is at the Parent Company's discretion.

C) When one company has control over another, Consolidated Financial Statements must be prepared for the combined entity.

D) Before preparing Consolidated Financial Statements, a subsidiary's Financial Statements prior to the date of acquisition must be restated.

A) The preparation of Consolidated Financial Statements means that the companies involved cease to operate as separate legal entities.

B) The preparation of Consolidated Financial Statements is at the Parent Company's discretion.

C) When one company has control over another, Consolidated Financial Statements must be prepared for the combined entity.

D) Before preparing Consolidated Financial Statements, a subsidiary's Financial Statements prior to the date of acquisition must be restated.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

19

Parent and Sub Inc. had the following balance sheets on December 31, 2019: On January 1, 2020, Parent purchased all of Sub Inc.'s Common Shares for $40,000 in cash. On that date, Sub's Current Assets and Fixed Assets were worth $26,000 and $54,000, respectively. Assuming that Consolidated Financial Statements were prepared on that date, answer the following:

The Fixed Assets of the combined entity should be valued at:

A) $70,000

B) $120,000

C) $154,000

D) $160,000

The Fixed Assets of the combined entity should be valued at:

A) $70,000

B) $120,000

C) $154,000

D) $160,000

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

20

Parent and Sub Inc. had the following balance sheets on December 31, 2019: On January 1, 2020, Parent purchased all of Sub Inc.'s Common Shares for $40,000 in cash. On that date, Sub's Current Assets and Fixed Assets were worth $26,000 and $54,000, respectively. Assuming that Consolidated Financial Statements were prepared on that date, answer the following:

The Goodwill arising from this Business Combination would be:

A) ($17,000)

B) $120,000

C) $17,000

D) $7,000

The Goodwill arising from this Business Combination would be:

A) ($17,000)

B) $120,000

C) $17,000

D) $7,000

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

21

Company A has decided to purchase 100% of the voting shares of Company B for $100,000 cash on January 1, 2019. Immediately before the acquisition, A and B reported cash balances of $300,000 and $150,000 respectively. If Consolidated Financial Statements were prepared immediately following the acquisition, how much Cash would be reported on A's consolidated balance sheet?

A) $250,000

B) $350,000

C) $450,000

D) $550,000

A) $250,000

B) $350,000

C) $450,000

D) $550,000

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

22

A Inc. is contemplating a business combination with B Inc. However, A Inc.'s management is uncertain as to whether it should purchase B's assets or a majority of B's voting shares. The fair market values of B's assets far exceed their book values. A's management should be advised that IN MOST CASES:

A) the purchase of B's shares would likely be the cheaper method of acquiring control; however, it would be less advantageous to the consolidated entity from tax standpoint.

B) the purchase of B's shares would likely be the cheaper method of acquiring control. It would also be more advantageous to the consolidated entity from a tax standpoint.

C) the purchase of B's shares would likely be the costlier method of acquiring control; however, it would be more advantageous to the consolidated entity from a tax standpoint.

D) the purchase of B's shares would likely be the costlier method of acquiring control. It would also be less advantageous to the consolidated entity from a tax standpoint.

A) the purchase of B's shares would likely be the cheaper method of acquiring control; however, it would be less advantageous to the consolidated entity from tax standpoint.

B) the purchase of B's shares would likely be the cheaper method of acquiring control. It would also be more advantageous to the consolidated entity from a tax standpoint.

C) the purchase of B's shares would likely be the costlier method of acquiring control; however, it would be more advantageous to the consolidated entity from a tax standpoint.

D) the purchase of B's shares would likely be the costlier method of acquiring control. It would also be less advantageous to the consolidated entity from a tax standpoint.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

23

Which of the following must be possible in order for a business combination to exist?

A) Control of a subsidiary's net assets that constitute a business

B) Ownership of 100 % of a subsidiary's voting shares

C) Ownership of all of a subsidiary's assets

D) Ownership of all of a subsidiary's operating assets

A) Control of a subsidiary's net assets that constitute a business

B) Ownership of 100 % of a subsidiary's voting shares

C) Ownership of all of a subsidiary's assets

D) Ownership of all of a subsidiary's operating assets

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

24

Under the new-entity method, which of the following statements is TRUE?

A) The net assets of the acquiring company remain at book value while those of the acquired company are recorded at fair value.

B) The net assets of the acquiring company are recorded at fair value while those of the acquired company are recorded at book value.

C) The net assets of both companies are recorded at fair market value.

D) The net assets of both companies are recorded at book value.

A) The net assets of the acquiring company remain at book value while those of the acquired company are recorded at fair value.

B) The net assets of the acquiring company are recorded at fair value while those of the acquired company are recorded at book value.

C) The net assets of both companies are recorded at fair market value.

D) The net assets of both companies are recorded at book value.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

25

Company A makes a hostile take-over bid for control of Company

A) Pac-man defence.

B) In response, Company B makes a counter-offer to purchase shares from Company A's shareholders. Which of the following best describes Company B's response?

B) Selling the crown jewels.

C) Poison pill.

D) Hostile defence.

A) Pac-man defence.

B) In response, Company B makes a counter-offer to purchase shares from Company A's shareholders. Which of the following best describes Company B's response?

B) Selling the crown jewels.

C) Poison pill.

D) Hostile defence.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

26

Which of the following is closest to IFRS 3 Business Combinations definition of control?

A) A company is deemed to have control over another only when it owns a majority of the voting shares of another company.

B) A company is deemed to have control when it can elect a majority of the Board members of another company.

C) Control is the ability to direct the activities of a company that most significantly affect the investor's returns.

D) Control exists only when a company has the continuing power to determine the operating and financing policies of another company and attempts to exercise such powers.

A) A company is deemed to have control over another only when it owns a majority of the voting shares of another company.

B) A company is deemed to have control when it can elect a majority of the Board members of another company.

C) Control is the ability to direct the activities of a company that most significantly affect the investor's returns.

D) Control exists only when a company has the continuing power to determine the operating and financing policies of another company and attempts to exercise such powers.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

27

A Inc. purchased 100% of the voting shares of B Inc. on July 1, 2019. Which of the following statements is TRUE?

A) The 2019 Consolidated Income Statement will include only the income of A Inc. from January 1, 2019 to June 30, 2019 and income for both A Inc. and B Inc. from July 1, 2019 to December 31, 2019.

B) The 2019 Consolidated Income Statement will include income for both A Inc. and B Inc. for the entire year.

C) The 2018 Income Statement (i.e. the comparative year), will retroactively include income for both A Inc. and B Inc.

D) The Consolidated Income Statement for 2019 will only include income from A Inc.

A) The 2019 Consolidated Income Statement will include only the income of A Inc. from January 1, 2019 to June 30, 2019 and income for both A Inc. and B Inc. from July 1, 2019 to December 31, 2019.

B) The 2019 Consolidated Income Statement will include income for both A Inc. and B Inc. for the entire year.

C) The 2018 Income Statement (i.e. the comparative year), will retroactively include income for both A Inc. and B Inc.

D) The Consolidated Income Statement for 2019 will only include income from A Inc.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

28

Which of the following statements is correct?

A) Under the new-entity method, both of the company's net assets are recorded at their fair market values for these assets on the date of acquisition.

B) Under the acquisition method, the acquirer company's net assets are revalued to fair value to reflect the substance of the transaction which, in essence is, a new company has been formed.

C) As of January 1st, 2011, the new-entity method must be used to account for business combinations where an acquirer can be identified.

D) The acquisition method is consistent with the historical cost principle while the New Entity Method is not.

A) Under the new-entity method, both of the company's net assets are recorded at their fair market values for these assets on the date of acquisition.

B) Under the acquisition method, the acquirer company's net assets are revalued to fair value to reflect the substance of the transaction which, in essence is, a new company has been formed.

C) As of January 1st, 2011, the new-entity method must be used to account for business combinations where an acquirer can be identified.

D) The acquisition method is consistent with the historical cost principle while the New Entity Method is not.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

29

A Corporation had net income of $50,000 in 2019 and $60,000 in 2020, excluding any income from its investment in B Company. B Company had net income of $30,000 in 2019 and $40,000 in 2020. On January 1, 2020, A Corporation acquired all of the outstanding common shares of B Company for a cash payment of $300,000. Assume that there was no acquisition differential on this business combination. What net income would A Corporation report for 2020 in its comparative consolidated financial statements at the end of 2020?

A) $40,000

B) $60,000

C) $80,000

D) $100,000

A) $40,000

B) $60,000

C) $80,000

D) $100,000

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

30

Zen Inc. owns 35% of Sun Inc.'s voting shares. Zen is by far the largest single shareholder of Sun Inc.'s shares, with the rest of Sun's shares being very widely held by individual investors. There was a very poor turnout at Sun Inc.'s recent annual meeting, enabling Zen Inc. to elect the majority of Sun's Board of Directors. Does Zen control Sun under IFRS?

A) No, Zen does not control Sun because it cannot exercise control over Sun without the cooperation of Sun's other shareholders.

B) Yes, Zen controls Sun because it is Sun's single largest shareholder group.

C) Yes, Zen is deemed to control Sun because it has elected a majority of Sun's Board members and the other shareholders are not organized in such a way to actively cooperate when they vote.

D) Zen could only control Sun if it owned 50% of Sun's voting shares.

A) No, Zen does not control Sun because it cannot exercise control over Sun without the cooperation of Sun's other shareholders.

B) Yes, Zen controls Sun because it is Sun's single largest shareholder group.

C) Yes, Zen is deemed to control Sun because it has elected a majority of Sun's Board members and the other shareholders are not organized in such a way to actively cooperate when they vote.

D) Zen could only control Sun if it owned 50% of Sun's voting shares.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

31

A Corporation had net income of $50,000 in 2019 and $60,000 in 2020, excluding any income from its investment in B Company. B Company had net income of $30,000 in 2019 and $40,000 in 2020. On January 1, 2020, A Corporation acquired all of the outstanding common shares of B Company for a cash payment of $300,000. Assume that there was no acquisition differential on this business combination. What net income would A Corporation report for 2019 in its comparative consolidated financial statements at the end of 2020?

A) $30,000

B) $50,000

C) $80,000

D) $100,000

A) $30,000

B) $50,000

C) $80,000

D) $100,000

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

32

How is negative goodwill treated under the acquisition method?

A) The acquiring company will report a gain on acquisition.

B) The acquiring company will report a loss on acquisition.

C) The negative goodwill will be included in other comprehensive income, as it is essentially an unrealized gain.

D) The negative goodwill is prorated and allocated to the fair value of the identifiable net assets of the acquired company.

A) The acquiring company will report a gain on acquisition.

B) The acquiring company will report a loss on acquisition.

C) The negative goodwill will be included in other comprehensive income, as it is essentially an unrealized gain.

D) The negative goodwill is prorated and allocated to the fair value of the identifiable net assets of the acquired company.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

33

A Inc. purchased 100% of B Inc.'s voting shares for cash. The assets and liabilities reported in the consolidated balance sheet of A Inc. prepared on the date of acquisition will include which of the following?

A) The book value of A's assets and liabilities plus the book value of B's assets and liabilities

B) The fair market value of A's assets and liabilities plus the book value of B's assets and liabilities

C) The book value of A's assets and liabilities plus the fair market value of B's assets and liabilities

D) The fair market value of A's assets and liabilities plus the fair market value of B's assets and liabilities

A) The book value of A's assets and liabilities plus the book value of B's assets and liabilities

B) The fair market value of A's assets and liabilities plus the book value of B's assets and liabilities

C) The book value of A's assets and liabilities plus the fair market value of B's assets and liabilities

D) The fair market value of A's assets and liabilities plus the fair market value of B's assets and liabilities

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

34

XYZ Inc. owns 55% of DEF Inc.'s 100,000 outstanding voting shares. Another company, GHI Inc., owns 40%, with the remaining shares being held by many individual investors. GHI Inc. also owns $25,000,000 worth of DEF Inc.'s $1,000 par value bonds, each of which is convertible to one voting share of DEF Inc. Which of the following statements regarding the control of DEF Inc. is correct?

A) XYZ Inc. has control over DEF Inc. as it owns a majority of DEF Inc.'s currently outstanding voting shares.

B) XYZ Inc. does not have control over DEF Inc., as it cannot exercise control over DEF's strategic operating, investing and Financing activities without the cooperation of GHI Inc.

C) XYZ Inc. has de facto control over DEF Inc.

D) As long as GHI Inc. does not exercise its option to convert its bonds to voting shares, XYZ Inc. has control over DEF Inc.

A) XYZ Inc. has control over DEF Inc. as it owns a majority of DEF Inc.'s currently outstanding voting shares.

B) XYZ Inc. does not have control over DEF Inc., as it cannot exercise control over DEF's strategic operating, investing and Financing activities without the cooperation of GHI Inc.

C) XYZ Inc. has de facto control over DEF Inc.

D) As long as GHI Inc. does not exercise its option to convert its bonds to voting shares, XYZ Inc. has control over DEF Inc.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

35

Company A wishes to acquire control of Company B's business. A consultant recommended that Company A can do this through a purchase of assets rather than a purchase of shares. Which of the following statements regarding the above scenario is correct?

A) Company A needs to purchase all of Company B's assets and assume all of its liabilities.

B) Company A only needs to acquire the assets of Company B that it needs to enhance its business operations.

C) Company A only needs to acquire control of Company B's fixed assets.

D) The consideration given by Company A must exceed 50% of the fair market value of Company B's net assets.

A) Company A needs to purchase all of Company B's assets and assume all of its liabilities.

B) Company A only needs to acquire the assets of Company B that it needs to enhance its business operations.

C) Company A only needs to acquire control of Company B's fixed assets.

D) The consideration given by Company A must exceed 50% of the fair market value of Company B's net assets.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

36

Assume that two companies wish to engage in a Business Combination involving a share exchange. Once the share exchange is consummated, each shareholder group will have an equal number of voting shares. Which of the following statements best describes the course of action that must be taken under these circumstances?

A) Other factors must be examined to determine which shareholder group is more dominant.

B) The company with the largest net assets (at fair market value) is deemed to be the acquirer.

C) No acquirer can be identified since no shareholder group has majority voting control, so the share exchange must be annulled.

D) The Boards of Directors of both companies must enter into discussions to agree on which party will be the acquirer.

A) Other factors must be examined to determine which shareholder group is more dominant.

B) The company with the largest net assets (at fair market value) is deemed to be the acquirer.

C) No acquirer can be identified since no shareholder group has majority voting control, so the share exchange must be annulled.

D) The Boards of Directors of both companies must enter into discussions to agree on which party will be the acquirer.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

37

Appendix B of IFRS 3 provides an extensive list of what must be disclosed for each Business Combination. Which of the following items is NOT included in that list?

A) The acquisition-date fair value of the total consideration given.

B) The primary reasons for the business combination and a description of how the acquirer obtained control of the acquiree.

C) The percentage of voting equity interests acquired.

D) The net assets of both companies at book value as disclosed in the financial statements of each company prior to the business combination.

A) The acquisition-date fair value of the total consideration given.

B) The primary reasons for the business combination and a description of how the acquirer obtained control of the acquiree.

C) The percentage of voting equity interests acquired.

D) The net assets of both companies at book value as disclosed in the financial statements of each company prior to the business combination.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

38

One company is considering entering into a business combination with another. The potential acquirer wishes to acquire the subsidiary's assets and liabilities but wishes to prepare Consolidated Financial Statements using the fair market values of its own assets and liabilities as well of those of its potential subsidiary. Can this be accomplished? (Assume that each of the methods is allowable)

A) Yes, this is permissible under the acquisition method.

B) Yes, this is permissible under the purchase method under certain circumstances.

C) Yes, this is permissible under the new-entity method.

D) No, this would not be possible under any circumstances.

A) Yes, this is permissible under the acquisition method.

B) Yes, this is permissible under the purchase method under certain circumstances.

C) Yes, this is permissible under the new-entity method.

D) No, this would not be possible under any circumstances.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

39

1234567 Inc. is contemplating a Business Combination with 7654321 Inc. One company is incorporated under Federal law, the other under provincial law. Is a statutory amalgamation permissible under these circumstances?

A) Yes, provided the combination is accounted for using the Acquisition Method.

B) Yes, provided the surviving corporation would have had control of the purchased company.

C) No, a statutory amalgamation would not be possible, since one company is incorporated under federal law and the other under provincial law.

D) Cannot be determined from the information given.

A) Yes, provided the combination is accounted for using the Acquisition Method.

B) Yes, provided the surviving corporation would have had control of the purchased company.

C) No, a statutory amalgamation would not be possible, since one company is incorporated under federal law and the other under provincial law.

D) Cannot be determined from the information given.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

40

IFRS 3 outlines the accounting requirements for business combinations. Which of the following statements is correct?

A) Companies may choose between the new entity method and the acquisition method when accounting for business combinations.

B) The only acceptable method of accounting for business combinations is the new entity method.

C) The only acceptable method of accounting for business combinations is the acquisition method.

D) The new entity method can only be used when cash is the sole consideration offered by the acquirer in a business combination.

A) Companies may choose between the new entity method and the acquisition method when accounting for business combinations.

B) The only acceptable method of accounting for business combinations is the new entity method.

C) The only acceptable method of accounting for business combinations is the acquisition method.

D) The new entity method can only be used when cash is the sole consideration offered by the acquirer in a business combination.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

41

Company Inc. owns all of the outstanding voting shares of Firm Inc. On January 1st, 2019, Firm Inc. would like to purchase all of the voting shares of its main competitor, N-CORP Inc. Briefly discuss the purported accounting implications of this transaction.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

42

Sonic Enterprises Inc has decided to purchase 100% of the voting shares of Jackson Inc. for $300,000 in cash on May 1, 2019. On the date, the balance sheets of each of these companies were as follows:

On that date, the fair values of Jackson's assets and liabilities were as follows:

Sonic's Book Values approximated their Fair Values on that date.

Required:

a) Calculate the amount of Goodwill arising from this combination.

b) Prepare the journal entry to record Sonic's acquisition of Jackson's Shares.

c) Prepare Sonic's Consolidated Balance Sheet immediately following its acquisition of Jackson's assets.

On that date, the fair values of Jackson's assets and liabilities were as follows: Sonic's Book Values approximated their Fair Values on that date.Required:

a) Calculate the amount of Goodwill arising from this combination.

b) Prepare the journal entry to record Sonic's acquisition of Jackson's Shares.

c) Prepare Sonic's Consolidated Balance Sheet immediately following its acquisition of Jackson's assets.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

43

Great Western Manufacturing Inc. ("GWM") was acquired by Great Eastern Holding Ltd) ("GEH") in 2019. The Vice President, Finance of GWM has asked you, the manager in charge of this year's audit, whether or not GWM has to prepare consolidated financial statements for the year ended December 31, 2019. GWM has about fifteen wholly owned subsidiaries and has in the past prepared consolidated financial statements.

Required:

Prepare a discussion around the need to prepare consolidated financial statements.

Required:

Prepare a discussion around the need to prepare consolidated financial statements.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

44

On December 31, 2019, A Company has capital assets with a cost of $250,000 and accumulated depreciation of $150,000 and B Company has capital assets with a cost of $180,000 and accumulated depreciation of $80,000. B Company's capital assets have a fair value of $200,000 on that date. If Company A acquires Company B on January 1, 2020, and prepares a consolidated balance sheet on that date, at what values should the capital assets appear on that balance sheet (using the net method)?

A) Cost of $430,000 and accumulated depreciation of $230,000.

B) Cost of $450,000 and accumulated depreciation of $150,000.

C) Cost of $450,000 and accumulated depreciation of $230,000.

D) Cost of $680,000 and accumulated depreciation of $230,000.

A) Cost of $430,000 and accumulated depreciation of $230,000.

B) Cost of $450,000 and accumulated depreciation of $150,000.

C) Cost of $450,000 and accumulated depreciation of $230,000.

D) Cost of $680,000 and accumulated depreciation of $230,000.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

45

Telecom Inc has decided to purchase the shares of Intron Inc. for $300,000 in cash on July 1, 2019. On the date, the balance sheets of each of these companies were as follows:

On that date, the fair values of Intron's assets and liabilities were as follows:

Required:

Based on the information provided, answer the following:

a) Prepare the journal entry to record the purchases Intron's shares.

b) Prepare the consolidation entries (eliminating entries) that are required to prepare the Consolidated Financial Statements.

On that date, the fair values of Intron's assets and liabilities were as follows: Required:Based on the information provided, answer the following:

a) Prepare the journal entry to record the purchases Intron's shares.

b) Prepare the consolidation entries (eliminating entries) that are required to prepare the Consolidated Financial Statements.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

46

ABC123 Inc has decided to purchase 100% the voting shares of DEF456 for $400,000 in cash on July 1, 2019. On the date, the balance sheets of each of these companies were as follows:

On that date, the fair values of DEF456 Assets and Liabilities were as follows:

In addition to the above, an independent appraiser deemed that DEF456 Inc. had trademarks with a fair market value of $100,000 which had not been accounted for. In turn, ABC123's fair market values were equal to their book values with the exception of the Company's Inventory and Plant and Equipment, which were said to have Fair Market Values of $30,000 and $480,000, respectively.

Based on the information provided:

a) Calculate the amount of Goodwill arising from this combination.

b) Prepare the journal entry to record ABC123's acquisition of DEF456's shares.

c) Prepare ABC123's Consolidated Balance Sheet immediately following its acquisition of DEF123's voting shares.

On that date, the fair values of DEF456 Assets and Liabilities were as follows: In addition to the above, an independent appraiser deemed that DEF456 Inc. had trademarks with a fair market value of $100,000 which had not been accounted for. In turn, ABC123's fair market values were equal to their book values with the exception of the Company's Inventory and Plant and Equipment, which were said to have Fair Market Values of $30,000 and $480,000, respectively.Based on the information provided:

a) Calculate the amount of Goodwill arising from this combination.

b) Prepare the journal entry to record ABC123's acquisition of DEF456's shares.

c) Prepare ABC123's Consolidated Balance Sheet immediately following its acquisition of DEF123's voting shares.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

47

Company A makes an offer to purchase all of the shares of Company B from Company B's shareholders. The board of directors of Company B does not feel that the offer is adequate and seeks out another purchaser who might offer more for the shares. This defence to the takeover is referred as:

A) White knight.

B) Pac-man defence.

C) Poison pill.

D) Selling the crown jewels.

A) White knight.

B) Pac-man defence.

C) Poison pill.

D) Selling the crown jewels.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

48

In general, which of the following statements about the income tax implications of the form of a business combination is true?

A) An acquisition of shares is generally better for the acquirer but worse for the vendor.

B) An acquisition of net assets is generally better for the acquirer but worse for the vendor.

C) An acquisition of shares is generally better for both the acquirer and the vendor.

D) An acquisition of net assets is generally better for both the acquirer and the vendor

A) An acquisition of shares is generally better for the acquirer but worse for the vendor.

B) An acquisition of net assets is generally better for the acquirer but worse for the vendor.

C) An acquisition of shares is generally better for both the acquirer and the vendor.

D) An acquisition of net assets is generally better for both the acquirer and the vendor

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

49

When are parent companies allowed to comprehensively revalue the assets and liabilities of a subsidiary to their fair values at the acquisition date through the use of push-down accounting, following a business combination?

A) When reporting under ASPE and there is a significant non-controlling interest

B) When reporting under ASPE and there is an insignificant (or no) non-controlling interest

C) When reporting under IFRS and there is a significant non-controlling interest

D) When reporting under IFRS and there is an insignificant (or no) non-controlling interest

A) When reporting under ASPE and there is a significant non-controlling interest

B) When reporting under ASPE and there is an insignificant (or no) non-controlling interest

C) When reporting under IFRS and there is a significant non-controlling interest

D) When reporting under IFRS and there is an insignificant (or no) non-controlling interest

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

50

Which of the following is required when preparing a consolidated balance sheet on the date of the formation of a subsidiary by its parent company?

A) The assets and liabilities of the subsidiary must be revalued to fair value.

B) The goodwill from the business combination must be calculated.

C) The parent's investment account must be eliminated against the subsidiary's share capital.

D) The parent's investment account must be eliminated against the subsidiary's retained earnings.

A) The assets and liabilities of the subsidiary must be revalued to fair value.

B) The goodwill from the business combination must be calculated.

C) The parent's investment account must be eliminated against the subsidiary's share capital.

D) The parent's investment account must be eliminated against the subsidiary's retained earnings.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

51

ABC123 Inc has decided to purchase 100% of the voting shares of DEF456 for $400,000 in Cash on July 1, 2019. On the date, the balance sheets of each of these companies were as follows:

On that date, the fair values of DEF456 Assets and Liabilities were as follows:

In addition to the above, an independent appraiser deemed that DEF456 Inc. had trademarks with a fair market value of $100,000 which had not been accounted for. In turn, ABC123's fair market values were equal to their book values with the exception of the Company's Inventory and Plant and Equipment, which were said to have Fair Market Values of $30,000 and $480,000, respectively.

Prepare any disclosure required for ABC123 Inc. under IFRS. Assume DEF456 has a reliable and specialized workforce that produces high-end loudspeakers for touring musicians and that ABC123 manufactures stage equipment needed for live music performances.

On that date, the fair values of DEF456 Assets and Liabilities were as follows: In addition to the above, an independent appraiser deemed that DEF456 Inc. had trademarks with a fair market value of $100,000 which had not been accounted for. In turn, ABC123's fair market values were equal to their book values with the exception of the Company's Inventory and Plant and Equipment, which were said to have Fair Market Values of $30,000 and $480,000, respectively.Prepare any disclosure required for ABC123 Inc. under IFRS. Assume DEF456 has a reliable and specialized workforce that produces high-end loudspeakers for touring musicians and that ABC123 manufactures stage equipment needed for live music performances.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

52

On April 1, 2019, the balance sheets of Optimum Inc. and Electra Inc. were as follows:

On that date, the fair values of Electra's Assets and Liabilities were as follows:

On April 1, 2019, Optimum issued 5,000 new common shares with a market value of $50.00 per share as consideration for Electra's net assets. Prior to the issue, Optimum had 10,000 outstanding common shares.

Required:

a) Calculate the amount of Goodwill arising from this combination.

b) Prepare the journal entry to record Optimum's acquisition of Electra's assets.

c) Prepare Optimum's Consolidated Balance Sheet immediately following its acquisition of Electra's assets.

d) Prepare Electra's Balance Sheet following the acquisition.

On that date, the fair values of Electra's Assets and Liabilities were as follows: On April 1, 2019, Optimum issued 5,000 new common shares with a market value of $50.00 per share as consideration for Electra's net assets. Prior to the issue, Optimum had 10,000 outstanding common shares.Required:

a) Calculate the amount of Goodwill arising from this combination.

b) Prepare the journal entry to record Optimum's acquisition of Electra's assets.

c) Prepare Optimum's Consolidated Balance Sheet immediately following its acquisition of Electra's assets.

d) Prepare Electra's Balance Sheet following the acquisition.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

53

Which of the following is NOT required for an investor to have control over an investee?

A) The investor must have power over the investee.

B) The investor must have exposure to variable returns from the investment.

C) The investor must be able to use its power to affect the amount of its returns.

D) The investor must currently own a majority of the voting shares of the investee.

A) The investor must have power over the investee.

B) The investor must have exposure to variable returns from the investment.

C) The investor must be able to use its power to affect the amount of its returns.

D) The investor must currently own a majority of the voting shares of the investee.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

54

Which of the following is considered to be part of the acquisition cost of a subsidiary?

A) Due diligence fees paid to lawyers.

B) The fair value of assets transferred by the acquirer.

C) The costs of issuing debt or shares.

D) Amounts paid to accountants for advice.

A) Due diligence fees paid to lawyers.

B) The fair value of assets transferred by the acquirer.

C) The costs of issuing debt or shares.

D) Amounts paid to accountants for advice.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

55

ABC123 Inc has decided to purchase 100% the voting shares of DEF456 by issuing common shares with a market value of $400,000 on July 1, 2019. On the date, the balance sheets of each of these companies were as follows:

On that date, the fair values of DEF456 Assets and Liabilities were as follows:

In addition to the above, an independent appraiser deemed that DEF456 Inc. had trademarks with a fair market value of $100,000 which had not been accounted for.

Based on the information provided:

a) Calculate the amount of Goodwill arising from this combination.

b) Prepare the journal entry to record ABC123's acquisition of DEF456's shares.

c) Prepare ABC123's Consolidated Balance Sheet immediately following its acquisition of DEF123's voting shares.

On that date, the fair values of DEF456 Assets and Liabilities were as follows: In addition to the above, an independent appraiser deemed that DEF456 Inc. had trademarks with a fair market value of $100,000 which had not been accounted for.Based on the information provided:

a) Calculate the amount of Goodwill arising from this combination.

b) Prepare the journal entry to record ABC123's acquisition of DEF456's shares.

c) Prepare ABC123's Consolidated Balance Sheet immediately following its acquisition of DEF123's voting shares.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

56

Which of the following is NOT considered to be part of the acquisition cost of a subsidiary?

A) Any cash paid to the seller.

B) The fair value of contingent consideration.

C) Present value of any promises by the acquirer to pay cash in the future.

D) The cost of issuing shares as part of the consideration.

A) Any cash paid to the seller.

B) The fair value of contingent consideration.

C) Present value of any promises by the acquirer to pay cash in the future.

D) The cost of issuing shares as part of the consideration.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

57

ABC123 Inc has decided to purchase 100% the voting shares of DEF456 for $400,000 in Cash on July 1, 2018. On the date, the balance sheets of each of these companies were as follows:

On that date, the fair values of DEF456 Assets and Liabilities were as follows:

In addition to the above, an independent appraiser deemed that DEF456 Inc. had trademarks with a fair market value of $100,000 which had not been accounted for. In turn, ABC123's fair market values were equal to their book values with the exception of the Company's Inventory and Plant and Equipment, which were said to have Fair Market Values of $30,000 and $480,000, respectively.

Calculate the goodwill arising from this business combination and state how it would be shown in the consolidated balance sheet on the acquisition date.

On that date, the fair values of DEF456 Assets and Liabilities were as follows: In addition to the above, an independent appraiser deemed that DEF456 Inc. had trademarks with a fair market value of $100,000 which had not been accounted for. In turn, ABC123's fair market values were equal to their book values with the exception of the Company's Inventory and Plant and Equipment, which were said to have Fair Market Values of $30,000 and $480,000, respectively.Calculate the goodwill arising from this business combination and state how it would be shown in the consolidated balance sheet on the acquisition date.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

58

Telecom Inc has decided to purchase the shares of Intron Inc. for $300, 000 in Cash on July 1, 2019. On the date, the balance sheets of each of these companies were as follows:

On that date, the fair values of Intron's assets and liabilities were as follows:

Required:

Prepare the Consolidated Balance Sheet on date of acquisition.

Calculation and Allocation of Acquisition Differential:

On that date, the fair values of Intron's assets and liabilities were as follows: Required:Prepare the Consolidated Balance Sheet on date of acquisition.

Calculation and Allocation of Acquisition Differential:

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

59

IFRS 10 states that a parent is not required to present consolidated financial statements for external reporting purposes if the parent meets certain conditions. Which of the following conditions is NOT correct?

A) Its ultimate or any intermediate parent produces financial statements available for public use and that comply with IFRS in which subsidiaries are consolidated.

B) It does not have any debt or equity instruments traded in a public market.

C) It has filed, or is in the process of filing, financial statements with a regulatory organization for the purposes of a public offering.

D) It is a wholly-owned subsidiary of another entity and its other owners have been informed about the parent not presenting consolidated financial statement.

A) Its ultimate or any intermediate parent produces financial statements available for public use and that comply with IFRS in which subsidiaries are consolidated.

B) It does not have any debt or equity instruments traded in a public market.

C) It has filed, or is in the process of filing, financial statements with a regulatory organization for the purposes of a public offering.

D) It is a wholly-owned subsidiary of another entity and its other owners have been informed about the parent not presenting consolidated financial statement.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

60

Telecom Inc has decided to purchase the net assets of Intron Inc. for $300, 000 in cash on July 1, 2019. On the date, the balance sheets of each of these companies were as follows:

On that date, the fair values of Intron's assets and liabilities were as follows:

Required:

Prepare the journal entry to record this purchase.

On that date, the fair values of Intron's assets and liabilities were as follows: Required:Prepare the journal entry to record this purchase.

Unlock Deck

Unlock for access to all 61 flashcards in this deck.

Unlock Deck

k this deck

61