Deck 8: Cost Allocation: Practices

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Step-down allocations

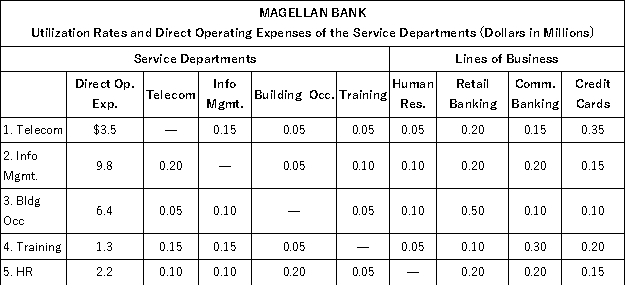

Magellan Bank has five service departments (telecom, information management, building occupancy, training, and human resources). The bank uses a step-down method of allocating service department costs to its three lines of business (retail banking, commercial banking, and credit cards). The following table contains the utilization rates of the five service departments and three lines of business. Also included in this table are the direct operating expenses of the service departments (in millions of dollars). Direct operating expenses of each service department do not contain any allocated service costs from the other service departments. For example, telecom spent $3.5 million dollars and provided services to other units within Magellan Bank. Information management consumed 15 percent of telecom's services. The order in which the service departments are allocated is also indicated in the table. The telecom department costs are allocated first, followed by information management, and the costs of the human resources department are allocated last. Required:

Required:

a. Using the step-down method and the order of departments specified in the table, what is the total allocated cost from information management to credit cards, including all the costs allocated to information management?

b. Information management costs are allocated based on terabytes of storage used by the other service departments and lines of business. If, instead of being second in the step-down sequence, information management became fifth in the sequence, would the allocated cost per terabyte increase or decrease? Explain precisely why it increases or decreases.

c. If instead of using the step-down method of allocating service department costs, Magellan uses the direct allocation method, what is the total allocated cost from information management to credit cards, including all the costs allocated to information management? (Note: Information management remains second in the list.)

Magellan Bank has five service departments (telecom, information management, building occupancy, training, and human resources). The bank uses a step-down method of allocating service department costs to its three lines of business (retail banking, commercial banking, and credit cards). The following table contains the utilization rates of the five service departments and three lines of business. Also included in this table are the direct operating expenses of the service departments (in millions of dollars). Direct operating expenses of each service department do not contain any allocated service costs from the other service departments. For example, telecom spent $3.5 million dollars and provided services to other units within Magellan Bank. Information management consumed 15 percent of telecom's services. The order in which the service departments are allocated is also indicated in the table. The telecom department costs are allocated first, followed by information management, and the costs of the human resources department are allocated last.

Required:a. Using the step-down method and the order of departments specified in the table, what is the total allocated cost from information management to credit cards, including all the costs allocated to information management?

b. Information management costs are allocated based on terabytes of storage used by the other service departments and lines of business. If, instead of being second in the step-down sequence, information management became fifth in the sequence, would the allocated cost per terabyte increase or decrease? Explain precisely why it increases or decreases.

c. If instead of using the step-down method of allocating service department costs, Magellan uses the direct allocation method, what is the total allocated cost from information management to credit cards, including all the costs allocated to information management? (Note: Information management remains second in the list.)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Beck Manufacturing is a contract manufacturer that assembles products for other companies. Beck has two service departments, Maintenance and Administration, and two operating divisions, Small Components and Large Components. The following data summarize the utilization of each service department: ![Beck Manufacturing is a contract manufacturer that assembles products for other companies. Beck has two service departments, Maintenance and Administration, and two operating divisions, Small Components and Large Components. The following data summarize the utilization of each service department: Square feet of floor space required by each user is the allocation base for allocating the Maintenance department cost of $950,000. Number of employees is used to allocate the Administration department cost of $567,000. Beck uses the step-down method of allocating service department costs to the two operating divisions. The $950,000 and $567,000 amounts represent the operating costs of the Maintenance and Administration departments, respectively, and they do not include any cost allocations from the other service departments. Required: a. Allocate the two service department costs to the two operating divisions using the step-down method where Maintenance is the first service department allocated and Administration is the second service department allocated. b. Allocate the two service department costs to the two operating divisions using the step-down method where Administration is the first service department allocated and Maintenance is the second service department allocated. c. Calculate the allocated cost per square foot and the allocated cost per employee resulting from using the step-down method where Maintenance is the first service department allocated and Administration is the second service department allocated (as in part [a]). d. Calculate the allocated cost per square foot and the allocated cost per employee resulting from using the step-down method where Administration is the first service department allocated and Maintenance is the second service department allocated (as in part [b]). e. Describe why the costs per square foot and the costs per employee vary in parts (c) and (d) above.<div style=padding-top: 35px>](https://storage.examlex.com/TB6416/11eaa3d8_3b24_75e9_9f8f_79a361276087_TB6416_00.jpg) Square feet of floor space required by each user is the allocation base for allocating the Maintenance department cost of $950,000. Number of employees is used to allocate the Administration department cost of $567,000. Beck uses the step-down method of allocating service department costs to the two operating divisions. The $950,000 and $567,000 amounts represent the operating costs of the Maintenance and Administration departments, respectively, and they do not include any cost allocations from the other service departments.

Square feet of floor space required by each user is the allocation base for allocating the Maintenance department cost of $950,000. Number of employees is used to allocate the Administration department cost of $567,000. Beck uses the step-down method of allocating service department costs to the two operating divisions. The $950,000 and $567,000 amounts represent the operating costs of the Maintenance and Administration departments, respectively, and they do not include any cost allocations from the other service departments.

Required:

a. Allocate the two service department costs to the two operating divisions using the step-down method where Maintenance is the first service department allocated and Administration is the second service department allocated.

b. Allocate the two service department costs to the two operating divisions using the step-down method where Administration is the first service department allocated and Maintenance is the second service department allocated.

c. Calculate the allocated cost per square foot and the allocated cost per employee resulting from using the step-down method where Maintenance is the first service department allocated and Administration is the second service department allocated (as in part [a]).

d. Calculate the allocated cost per square foot and the allocated cost per employee resulting from using the step-down method where Administration is the first service department allocated and Maintenance is the second service department allocated (as in part [b]).

e. Describe why the costs per square foot and the costs per employee vary in parts (c) and (d) above.

Square feet of floor space required by each user is the allocation base for allocating the Maintenance department cost of $950,000. Number of employees is used to allocate the Administration department cost of $567,000. Beck uses the step-down method of allocating service department costs to the two operating divisions. The $950,000 and $567,000 amounts represent the operating costs of the Maintenance and Administration departments, respectively, and they do not include any cost allocations from the other service departments.Required:

a. Allocate the two service department costs to the two operating divisions using the step-down method where Maintenance is the first service department allocated and Administration is the second service department allocated.

b. Allocate the two service department costs to the two operating divisions using the step-down method where Administration is the first service department allocated and Maintenance is the second service department allocated.

c. Calculate the allocated cost per square foot and the allocated cost per employee resulting from using the step-down method where Maintenance is the first service department allocated and Administration is the second service department allocated (as in part [a]).

d. Calculate the allocated cost per square foot and the allocated cost per employee resulting from using the step-down method where Administration is the first service department allocated and Maintenance is the second service department allocated (as in part [b]).

e. Describe why the costs per square foot and the costs per employee vary in parts (c) and (d) above.

Question

Question

Question

Question

Question

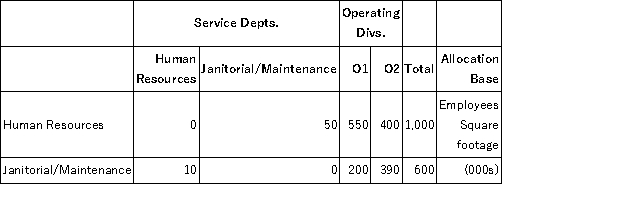

IFLAX manufactures commercial brushes in two operating divisions (O1 and O2) and has two service departments (Human Resources and Janitorial/Maintenance). The two service departments' costs are allocated to the two operating departments. Human Resources' costs of $600,000 are allocated based on the number of employees, and Janitorial/Maintenance costs of $800,000 are allocated based on square footage. The following table summarizes the number of employees and the square footage in each division and department.  Required:

Required:

a. Allocate the costs of the two service departments to the two operating divisions using the direct allocation method.

b. Allocate the costs of the two service departments to the two operating divisions using the step-down allocation method where Human Resources is allocated first and Janitorial/Maintenance is allocated second.

c. Allocate the costs of the two service departments to the two operating divisions using the step-down allocation method where Janitorial/Maintenance is allocated first and Human Resources is allocated second.

d. Compute the Human Resource Department cost per employee under the three allocation methods (direct allocation, step-down allocations where Human Resources is first, and the step-down method where Janitorial/Maintenance is first).

e. Compute the Janitorial/Maintenance cost per square foot under the three allocation methods (direct allocation, step-down allocations where Human Resources is first, and the step-down method where Janitorial/Maintenance is first).

f. Briefly discuss the various factors IFLAX management should consider in choosing how to allocate the two service department costs to the two operating divisions.

Required:a. Allocate the costs of the two service departments to the two operating divisions using the direct allocation method.

b. Allocate the costs of the two service departments to the two operating divisions using the step-down allocation method where Human Resources is allocated first and Janitorial/Maintenance is allocated second.

c. Allocate the costs of the two service departments to the two operating divisions using the step-down allocation method where Janitorial/Maintenance is allocated first and Human Resources is allocated second.

d. Compute the Human Resource Department cost per employee under the three allocation methods (direct allocation, step-down allocations where Human Resources is first, and the step-down method where Janitorial/Maintenance is first).

e. Compute the Janitorial/Maintenance cost per square foot under the three allocation methods (direct allocation, step-down allocations where Human Resources is first, and the step-down method where Janitorial/Maintenance is first).

f. Briefly discuss the various factors IFLAX management should consider in choosing how to allocate the two service department costs to the two operating divisions.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/26

Play

Full screen (f)

Deck 8: Cost Allocation: Practices

1

Somimad Sawmill manufactures two lumber products from a joint milling process. The two products developed are mine support braces (MSBs) and unseasoned commercial building lumber (CBL). A standard production run incurs joint costs of $300,000 and results in 60,000 units of MSB and 90,000 units of CBL. Each unprocessed unit of MSB sells for $2 per unit and each unprocessed unit of CBL sells for $4 per unit.

If the CBL is processed further at a cost of $200,000, it can be sold at $10 per unit but 10,000 units are unavoidably lost (with no discernible value). The MSB units can be coated with a preservative at a cost of $100,000 per production run and then sold for $3.50 each.

Required:

a. If no further work is done after the initial milling process, calculate the cost of CBL using physical quantities to allocate the joint cost.

b. If no further work is done after the initial milling process, calculate the cost of MSB using relative sales value to allocate the joint cost.

c. Should MSB and CBL be processed further or sold immediately after initial milling?

d. Given your decision in (c), prepare a schedule computing the completed cost assigned to each unit of MSB and CBL as charged to finished goods inventory. Use net realizable value for allocating joint costs.

Answer

If the CBL is processed further at a cost of $200,000, it can be sold at $10 per unit but 10,000 units are unavoidably lost (with no discernible value). The MSB units can be coated with a preservative at a cost of $100,000 per production run and then sold for $3.50 each.

Required:

a. If no further work is done after the initial milling process, calculate the cost of CBL using physical quantities to allocate the joint cost.

b. If no further work is done after the initial milling process, calculate the cost of MSB using relative sales value to allocate the joint cost.

c. Should MSB and CBL be processed further or sold immediately after initial milling?

d. Given your decision in (c), prepare a schedule computing the completed cost assigned to each unit of MSB and CBL as charged to finished goods inventory. Use net realizable value for allocating joint costs.

Answer

a. Allocation using physical quantities b. Allocation using relative sales value c. Processing further d. Allocation using net realizable value

2

Mistical Herbals processes exotic plant materials into various fragrances and biological pastes used by perfume and cosmetic firms. One particular plant material, Xubonic root from the rain forest in Australia, is processed yielding four joint products: QV3, VX7, HM4, and LZ9. Each of these joint products can be sold as is after the joint production process or processed further. The following table describes the yield of each joint product from one batch, the selling prices of the intermediate and further processed products, and the costs of further processing each joint product. The joint cost of processing one batch of Xubonic root is $30,000. Required:

a. Allocate the $30,000 joint cost per batch to each of the joint products based on the number of ounces in each joint product.

b. To maximize firm value, which of the joint products should be processed further and which should be sold without further processing?

c. Based on your analysis in part (b) regarding the decisions to process further or not, should Mistical Herbals process batches of Xubonic root into the four joint products? Support your decision with a quantitative analysis and indicate how much profit or loss Mistical Herbals makes per batch.

d. Suppose the joint cost of $30,000 is allocated using the net realizable value of each joint product. Calculate the profits (loss) per joint product after allocating the joint cost using net realizable value.

e. Explain how the use of joint cost allocations enhances or harms the decision to process joint products.

a. Allocate the $30,000 joint cost per batch to each of the joint products based on the number of ounces in each joint product.

b. To maximize firm value, which of the joint products should be processed further and which should be sold without further processing?

c. Based on your analysis in part (b) regarding the decisions to process further or not, should Mistical Herbals process batches of Xubonic root into the four joint products? Support your decision with a quantitative analysis and indicate how much profit or loss Mistical Herbals makes per batch.

d. Suppose the joint cost of $30,000 is allocated using the net realizable value of each joint product. Calculate the profits (loss) per joint product after allocating the joint cost using net realizable value.

e. Explain how the use of joint cost allocations enhances or harms the decision to process joint products.

a. Allocated joint cost is $60 per ounce ($30,000 ÷ 500 ounces): b. Decisions to process further: c. Batches of Xubonic root should be produced because each batch yields profits of $3,200.

d. Profit after allocating joint cost using net realizable value: e. Joint cost allocations do not enhance the decision of whether to further process joint products or not. Joint cost allocations based on net realizable value does not harm the decision process, but it does not add anything. The decisions in part (b) to process each joint product further or sell after the split off point were made without any joint cost allocations.

d. Profit after allocating joint cost using net realizable value: e. Joint cost allocations do not enhance the decision of whether to further process joint products or not. Joint cost allocations based on net realizable value does not harm the decision process, but it does not add anything. The decisions in part (b) to process each joint product further or sell after the split off point were made without any joint cost allocations.

3

Step down vs. direct allocations

Critically evaluate the statement:

The step-down method is better than the direct allocation method because at least the step-down method captures on average half of the service flows between service departments. By comparison, the direct allocation method ignores all the service flows.

Critically evaluate the statement:

The step-down method is better than the direct allocation method because at least the step-down method captures on average half of the service flows between service departments. By comparison, the direct allocation method ignores all the service flows.

This statement is not correct for a number of reasons:

a. One allocation method can only be assessed as "better" than another one after specifying how the resulting accounting numbers are being used (taxes, decision making, control, etc.). Since the quote does not specify how the cost allocations are being used, there is no logical way to assess which method is better.

b. Presumably, one criteria implied by the quote is in terms of accuracy. That is, does the step-down method more accurately reflect the opportunity costs of resources consumed by the service department? Under this criterion, it is still not obvious that the step-down allocation method is more accurate than the direct allocation method. Both allocation methods are approximations and each contains errors.

Look at the formula for the overhead rate in the step down method:

Service department's allocation rate = (own cost + allocated costs from higher service departments)/(quantity of services provided to users below the service department)

The numerator becomes more accurate in terms of resources used by the service department the further down in the sequence of service departments. But the denominator becomes less accurate because fewer actual users are included in the denominator. Look at the first department in the sequence. Its numerator includes no service department costs allocated to it, and hence understates the resources consumed by the first department in the sequence. But its denominator includes all of the users of its services.

The direct allocation method also contains errors. The numerator excludes costs of resources consumed from other service departments and the denominator excludes other service department users.

c. Both methods include fixed service department costs, and hence the allocated costs per unit of service provided do not reflect marginal (variable) costs of the service provided.

a. One allocation method can only be assessed as "better" than another one after specifying how the resulting accounting numbers are being used (taxes, decision making, control, etc.). Since the quote does not specify how the cost allocations are being used, there is no logical way to assess which method is better.

b. Presumably, one criteria implied by the quote is in terms of accuracy. That is, does the step-down method more accurately reflect the opportunity costs of resources consumed by the service department? Under this criterion, it is still not obvious that the step-down allocation method is more accurate than the direct allocation method. Both allocation methods are approximations and each contains errors.

Look at the formula for the overhead rate in the step down method:

Service department's allocation rate = (own cost + allocated costs from higher service departments)/(quantity of services provided to users below the service department)

The numerator becomes more accurate in terms of resources used by the service department the further down in the sequence of service departments. But the denominator becomes less accurate because fewer actual users are included in the denominator. Look at the first department in the sequence. Its numerator includes no service department costs allocated to it, and hence understates the resources consumed by the first department in the sequence. But its denominator includes all of the users of its services.

The direct allocation method also contains errors. The numerator excludes costs of resources consumed from other service departments and the denominator excludes other service department users.

c. Both methods include fixed service department costs, and hence the allocated costs per unit of service provided do not reflect marginal (variable) costs of the service provided.

4

Each week Walters Company produces 15,000 pounds of Product A and 30,000 pounds of Product B by incurring a joint cost of $400,000. These two products can be sold as is or processed further. Further processing of either product does not delay the production of subsequent batches of the joint product. Data regarding these two products are as follows: Required:

To maximize Walters Company's manufacturing contribution margin, how much total separate variable costs of further processing should be incurred each week?

To maximize Walters Company's manufacturing contribution margin, how much total separate variable costs of further processing should be incurred each week?

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

5

Joint Cost versus Common Costs

What is the difference between joint costs and common costs?

What is the difference between joint costs and common costs?

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

6

Of the following statements, which is true?

A)Real estate taxes are an example of joint costs

B)The costs of harvesting a pineapple plantation are additional processing costs

C)Common costs are incurred only in disassembly

D)Joint cost allocations are helpful in assessing a product's profitability

E)None of the above

A)Real estate taxes are an example of joint costs

B)The costs of harvesting a pineapple plantation are additional processing costs

C)Common costs are incurred only in disassembly

D)Joint cost allocations are helpful in assessing a product's profitability

E)None of the above

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

7

Internal resources, such as the legal department, training department, information technology, tend to be under-utilized, leading to a death spiral, when:

A)managers may choose whether to purchase the service internally or externally

B)the internal pricing system seeks to recover sunk costs

C)managers may decide to reduce the quantity of services used

D)the internal pricing system utilizes full costs

E)all of the above

A)managers may choose whether to purchase the service internally or externally

B)the internal pricing system seeks to recover sunk costs

C)managers may decide to reduce the quantity of services used

D)the internal pricing system utilizes full costs

E)all of the above

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

8

Beware of Unit Costs, Costs Beyond the Split-off Point Are Not Necessarily All Variable

Table 8-12 in the text allocates joint costs using net realizable value as the allocation base. What critical assumptions underlie the analysis in Table 8-12? That is, under what circumstances can the data in this table be used to assess product line profitability?

Table 8-12 in the text allocates joint costs using net realizable value as the allocation base. What critical assumptions underlie the analysis in Table 8-12? That is, under what circumstances can the data in this table be used to assess product line profitability?

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

9

When considering the purchase of a large central system, such as power generation or computer networks, firms have to decide how big a system to acquire and whether, and, if so, how to charge users for it subsequently. Which is true?

A)Option A

B)Option B

C)Option C

D)Option D

E)Option E

A)Option A

B)Option B

C)Option C

D)Option D

E)Option E

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

10

The Parvis Paramount Pigsty (PPP) raises pigs, from which a variety of pork products are processed. The herd features the Danish Yorkshire, which typically reaches 105 kgs at maturity. The following table summarizes the production process of producing Porktry, Porfekt, and Porkatoo from one pig. Previous research has indicated that raising a Danish Yorkshire from breeding to disposition costs an average of €3 per kg. The ratio of pig parts to products is relatively inflexible; as yet, bio-engineering has failed to produce pigs with other than four legs. Of the statements below, which is true of the allocation of the joint costs?

A)By weight, Porktry is allocated € 81.41

B)By relative sales value, Porkatoo is allocated € 80.05

C)Since Porktry is the least profitable product, it should be discontinued and resources devoted to Porfekt

D)By relative net realizable values, Porfekt is allocated € 135.09

E)None of the above

A)By weight, Porktry is allocated € 81.41

B)By relative sales value, Porkatoo is allocated € 80.05

C)Since Porktry is the least profitable product, it should be discontinued and resources devoted to Porfekt

D)By relative net realizable values, Porfekt is allocated € 135.09

E)None of the above

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

11

Step-down allocations

Magellan Bank has five service departments (telecom, information management, building occupancy, training, and human resources). The bank uses a step-down method of allocating service department costs to its three lines of business (retail banking, commercial banking, and credit cards). The following table contains the utilization rates of the five service departments and three lines of business. Also included in this table are the direct operating expenses of the service departments (in millions of dollars). Direct operating expenses of each service department do not contain any allocated service costs from the other service departments. For example, telecom spent $3.5 million dollars and provided services to other units within Magellan Bank. Information management consumed 15 percent of telecom's services. The order in which the service departments are allocated is also indicated in the table. The telecom department costs are allocated first, followed by information management, and the costs of the human resources department are allocated last. Required:

a. Using the step-down method and the order of departments specified in the table, what is the total allocated cost from information management to credit cards, including all the costs allocated to information management?

b. Information management costs are allocated based on terabytes of storage used by the other service departments and lines of business. If, instead of being second in the step-down sequence, information management became fifth in the sequence, would the allocated cost per terabyte increase or decrease? Explain precisely why it increases or decreases.

c. If instead of using the step-down method of allocating service department costs, Magellan uses the direct allocation method, what is the total allocated cost from information management to credit cards, including all the costs allocated to information management? (Note: Information management remains second in the list.)

Magellan Bank has five service departments (telecom, information management, building occupancy, training, and human resources). The bank uses a step-down method of allocating service department costs to its three lines of business (retail banking, commercial banking, and credit cards). The following table contains the utilization rates of the five service departments and three lines of business. Also included in this table are the direct operating expenses of the service departments (in millions of dollars). Direct operating expenses of each service department do not contain any allocated service costs from the other service departments. For example, telecom spent $3.5 million dollars and provided services to other units within Magellan Bank. Information management consumed 15 percent of telecom's services. The order in which the service departments are allocated is also indicated in the table. The telecom department costs are allocated first, followed by information management, and the costs of the human resources department are allocated last.

Required:a. Using the step-down method and the order of departments specified in the table, what is the total allocated cost from information management to credit cards, including all the costs allocated to information management?

b. Information management costs are allocated based on terabytes of storage used by the other service departments and lines of business. If, instead of being second in the step-down sequence, information management became fifth in the sequence, would the allocated cost per terabyte increase or decrease? Explain precisely why it increases or decreases.

c. If instead of using the step-down method of allocating service department costs, Magellan uses the direct allocation method, what is the total allocated cost from information management to credit cards, including all the costs allocated to information management? (Note: Information management remains second in the list.)

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

12

Williams manufactures a variety of iron products, made to customer specifications, in small batches. Willie Williams, owner, is concerned that he does not have an accurate understanding of the costs of production. You, a newly-minted MBA, have researched his business and identified various costs and cost drivers. The service departments (Janitorial, HR, and Data Services) are allocated to the two production departments (Welding and Assembly). Janitorial costs are allocated using square feet, HR using number of employees, and Data Services using number of transactions. You recall that there are several approaches to the allocation of service department costs, direct, step-down and reciprocal methods. If the direct method is used, which of the following is true?

A)The amount of Welding costs allocated to Assembly is $37,500

B)The amount of HR allocated to Janitorial is $2,604

C)The amount of Data Services costs allocated to Welding is $13,500

D)The amount of Janitorial costs allocated to Assembly is $4,909

E)None of the above

A)The amount of Welding costs allocated to Assembly is $37,500

B)The amount of HR allocated to Janitorial is $2,604

C)The amount of Data Services costs allocated to Welding is $13,500

D)The amount of Janitorial costs allocated to Assembly is $4,909

E)None of the above

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

13

Williams manufactures a variety of iron products, made to customer specifications, in small batches. Willie Williams, owner, is concerned that he does not have an accurate understanding of the costs of production. You, a newly-minted MBA, have researched his business and identified various costs and cost drivers. The service departments (Janitorial, HR, and Data Services) are allocated to the two production departments (Welding and Assembly). Janitorial costs are allocated using square feet, HR using number of employees, and Data Services using number of transactions. You recall that there are several approaches to the allocation of service department costs, direct, step-down and reciprocal methods. If the reciprocal method is applied, which is true?

A)Welding's total costs after allocation are $115,840.52

B)Assembly's total costs after allocation are greater than $100,000

C)Janitorial is allocated $1,119.74 from Data Svcs

D)HR's total costs after allocation are $46,059.25

E)None of the above

A)Welding's total costs after allocation are $115,840.52

B)Assembly's total costs after allocation are greater than $100,000

C)Janitorial is allocated $1,119.74 from Data Svcs

D)HR's total costs after allocation are $46,059.25

E)None of the above

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

14

Joint costs in different industries may be allocated using any of the following methods, except:

A)relative cubic footage of gases from a gas exploration process

B)relative sales values of fresh tomatoes, pulp tomatoes and tomato juice at the split-off point

C)relative profitability of pine planks, plywood, chips and sawdust at the split-off point

D)relative net realizable values at the split-off point of gold, silver, copper found in 100 tons of mining ore

E)none of the above

A)relative cubic footage of gases from a gas exploration process

B)relative sales values of fresh tomatoes, pulp tomatoes and tomato juice at the split-off point

C)relative profitability of pine planks, plywood, chips and sawdust at the split-off point

D)relative net realizable values at the split-off point of gold, silver, copper found in 100 tons of mining ore

E)none of the above

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

15

Which is not true of the various methods of allocating service department costs?

A)Application of the reciprocal method in a complex corporation usually requires the use of a computer

B)The direct method is quick to compute, accurate, and has low information requirements

C)There are multiple sequence possibilities for the step-down method

D)The choice of method affects the optimal allocation of resources

E)All of the above are true

A)Application of the reciprocal method in a complex corporation usually requires the use of a computer

B)The direct method is quick to compute, accurate, and has low information requirements

C)There are multiple sequence possibilities for the step-down method

D)The choice of method affects the optimal allocation of resources

E)All of the above are true

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

16

Cosmo Inc. operates two retail novelty stores: the Mall Store and the Town Store. Condensed monthly operating income data for Cosmo Inc. for November are presented in the accompanying table. Additional information regarding Cosmo's operations follows the statement. • One-fourth of each store's direct fixed expenses would continue through December of next year if either store were closed.

• Cosmo allocates common fixed expenses to each store on the basis of sales dollars.

• Management estimates that closing the Town Store would result in a 10 percent decrease in Mall Store sales, while closing the Mall Store would not affect Town Store sales.

• The operating results for November are representative of all months.

Required:

a. A decision by Cosmo Inc. to close the Town Store would result in a monthly increase (decrease) in Cosmo's operating income during next year of how much?

b. Cosmo is considering a promotional campaign at the Town Store that would not affect the Mall Store. Increasing monthly promotional expenses at the Town Store by $5,000 in order to increase Town Store sales by 10 percent would result in a monthly increase (decrease) in Cosmo's operating income during next year of how much?

c. Half of Town Store's dollar sales are from items sold at variable cost to attract customers to the store. Cosmo is considering deleting these items, a move that would reduce the Town Store's direct fixed expenses by 15 percent and result in the loss of 20 percent of Town Store's remaining sales volume. This change would not affect the Mall Store. A decision to eliminate the items sold at cost would result in a monthly increase (decrease) in Cosmo's operating income during next year of how much?

• Cosmo allocates common fixed expenses to each store on the basis of sales dollars.

• Management estimates that closing the Town Store would result in a 10 percent decrease in Mall Store sales, while closing the Mall Store would not affect Town Store sales.

• The operating results for November are representative of all months.

Required:

a. A decision by Cosmo Inc. to close the Town Store would result in a monthly increase (decrease) in Cosmo's operating income during next year of how much?

b. Cosmo is considering a promotional campaign at the Town Store that would not affect the Mall Store. Increasing monthly promotional expenses at the Town Store by $5,000 in order to increase Town Store sales by 10 percent would result in a monthly increase (decrease) in Cosmo's operating income during next year of how much?

c. Half of Town Store's dollar sales are from items sold at variable cost to attract customers to the store. Cosmo is considering deleting these items, a move that would reduce the Town Store's direct fixed expenses by 15 percent and result in the loss of 20 percent of Town Store's remaining sales volume. This change would not affect the Mall Store. A decision to eliminate the items sold at cost would result in a monthly increase (decrease) in Cosmo's operating income during next year of how much?

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

17

Williams manufactures a variety of iron products, made to customer specifications, in small batches. Willie Williams, owner, is concerned that he does not have an accurate understanding of the costs of production. You, a newly-minted MBA, have researched his business and identified various costs and cost drivers. The service departments (Janitorial, HR, and Data Services) are allocated to the two production departments (Welding and Assembly). Janitorial costs are allocated using square feet, HR using number of employees, and Data Services using number of transactions. You recall that there are several approaches to the allocation of service department costs, direct, step-down and reciprocal methods. If the step-down method is used in this case, which sequence of allocations is not valid?

A)Data, Janitorial, HR

B)HR, Data, Janitorial

C)Data, HR, Janitorial

D)Janitorial, Welding, HR, Data Svcs, Assembly

E)All sequences above are acceptable

A)Data, Janitorial, HR

B)HR, Data, Janitorial

C)Data, HR, Janitorial

D)Janitorial, Welding, HR, Data Svcs, Assembly

E)All sequences above are acceptable

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

18

Williams manufactures a variety of iron products, made to customer specifications, in small batches. Willie Williams, owner, is concerned that he does not have an accurate understanding of the costs of production. You, a newly-minted MBA, have researched his business and identified various costs and cost drivers. The service departments (Janitorial, HR, and Data Services) are allocated to the two production departments (Welding and Assembly). Janitorial costs are allocated using square feet, HR using number of employees, and Data Services using number of transactions. You recall that there are several approaches to the allocation of service department costs, direct, step-down and reciprocal methods. If the step-down method is applied, allocating the most costly department first, which is true?

A)Janitorial's total costs after allocation are $18,036.48

B)Assembly's total costs after allocation are less than $100,000

C)Janitorial is allocated $3,953.28 from Data Svcs

D)HR's total costs after allocation are $50,160

E)None of the above

A)Janitorial's total costs after allocation are $18,036.48

B)Assembly's total costs after allocation are less than $100,000

C)Janitorial is allocated $3,953.28 from Data Svcs

D)HR's total costs after allocation are $50,160

E)None of the above

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

19

An insurance company has the following profitability analysis of its services: The common costs are fixed, are distributed equally among the services, and are not avoidable if one of the services is dropped.

Required:

What is the profitability of the remaining services if all services with losses are dropped?

Required:

What is the profitability of the remaining services if all services with losses are dropped?

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

20

Williams manufactures a variety of iron products, made to customer specifications, in small batches. Willie Williams, owner, is concerned that he does not have an accurate understanding of the costs of production. You, a newly-minted MBA, have researched his business and identified various costs and cost drivers. The service departments (Janitorial, HR, and Data Services) are allocated to the two production departments (Welding and Assembly). Janitorial costs are allocated using square feet, HR using number of employees, and Data Services using number of transactions. You recall that there are several approaches to the allocation of service department costs, direct, step-down and reciprocal methods. If the step-down method is applied, allocating the most costly department first, which is true?

A)Welding's fractional use of HR is 25/125

B)Assembly's fractional use of Janitorial is 4500/7500

C)Janitorial's fractional use of Data Svcs is 22/1000

D)HR's fractional use of Data Svcs is 180/450

E)None of the above

A)Welding's fractional use of HR is 25/125

B)Assembly's fractional use of Janitorial is 4500/7500

C)Janitorial's fractional use of Data Svcs is 22/1000

D)HR's fractional use of Data Svcs is 180/450

E)None of the above

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

21

Beck Manufacturing is a contract manufacturer that assembles products for other companies. Beck has two service departments, Maintenance and Administration, and two operating divisions, Small Components and Large Components. The following data summarize the utilization of each service department: Square feet of floor space required by each user is the allocation base for allocating the Maintenance department cost of $950,000. Number of employees is used to allocate the Administration department cost of $567,000. Beck uses the step-down method of allocating service department costs to the two operating divisions. The $950,000 and $567,000 amounts represent the operating costs of the Maintenance and Administration departments, respectively, and they do not include any cost allocations from the other service departments.

Required:

a. Allocate the two service department costs to the two operating divisions using the step-down method where Maintenance is the first service department allocated and Administration is the second service department allocated.

b. Allocate the two service department costs to the two operating divisions using the step-down method where Administration is the first service department allocated and Maintenance is the second service department allocated.

c. Calculate the allocated cost per square foot and the allocated cost per employee resulting from using the step-down method where Maintenance is the first service department allocated and Administration is the second service department allocated (as in part [a]).

d. Calculate the allocated cost per square foot and the allocated cost per employee resulting from using the step-down method where Administration is the first service department allocated and Maintenance is the second service department allocated (as in part [b]).

e. Describe why the costs per square foot and the costs per employee vary in parts (c) and (d) above.

Square feet of floor space required by each user is the allocation base for allocating the Maintenance department cost of $950,000. Number of employees is used to allocate the Administration department cost of $567,000. Beck uses the step-down method of allocating service department costs to the two operating divisions. The $950,000 and $567,000 amounts represent the operating costs of the Maintenance and Administration departments, respectively, and they do not include any cost allocations from the other service departments.Required:

a. Allocate the two service department costs to the two operating divisions using the step-down method where Maintenance is the first service department allocated and Administration is the second service department allocated.

b. Allocate the two service department costs to the two operating divisions using the step-down method where Administration is the first service department allocated and Maintenance is the second service department allocated.

c. Calculate the allocated cost per square foot and the allocated cost per employee resulting from using the step-down method where Maintenance is the first service department allocated and Administration is the second service department allocated (as in part [a]).

d. Calculate the allocated cost per square foot and the allocated cost per employee resulting from using the step-down method where Administration is the first service department allocated and Maintenance is the second service department allocated (as in part [b]).

e. Describe why the costs per square foot and the costs per employee vary in parts (c) and (d) above.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

22

The Doe Company sells three products: sliced pineapples, crushed pineapples, and pineapple juice. The pineapple juice is a by-product of sliced pineapple, while crushed pineapples and sliced pineapples are produced simultaneously from the same pineapple. Some pineapple slices break, and these are used to make crushed pineapple.

The production process is as follows:

• A total of 100,000 pounds of pineapples is processed at a cost of $120,000 in Department 1. Twenty percent of the pineapples' weight is scrap and is discarded during processing. Twenty percent of the processed pineapple is crushed and transferred to Department 2. The remaining is transferred to Department 3.

• In Department 2, a further cost outlay of $15,000 is required to pack the crushed pineapple. Here a further 10 percent is lost in processing. The packed product is sold at $3 a pound.

• In Department 3, the material is processed at a total additional cost of $40,000. Thirty percent of the processed pineapple turns into juice and is sold at $0.50 a pound after $3,500 is incurred as selling costs. The remaining 70 percent is transferred to Department 4.

• Department 4 packs the sliced pineapple into tins. Costs incurred here total $25,000. The cans are then ready for sale at $4.00 a pound.

Required:

Prepare a schedule showing the allocation of the processing cost of $120,000 between crushed and sliced pineapple using the net realizable value method. The net realizable value of the juice is to be added to the sales value of the sliced pineapples.

The production process is as follows:

• A total of 100,000 pounds of pineapples is processed at a cost of $120,000 in Department 1. Twenty percent of the pineapples' weight is scrap and is discarded during processing. Twenty percent of the processed pineapple is crushed and transferred to Department 2. The remaining is transferred to Department 3.

• In Department 2, a further cost outlay of $15,000 is required to pack the crushed pineapple. Here a further 10 percent is lost in processing. The packed product is sold at $3 a pound.

• In Department 3, the material is processed at a total additional cost of $40,000. Thirty percent of the processed pineapple turns into juice and is sold at $0.50 a pound after $3,500 is incurred as selling costs. The remaining 70 percent is transferred to Department 4.

• Department 4 packs the sliced pineapple into tins. Costs incurred here total $25,000. The cans are then ready for sale at $4.00 a pound.

Required:

Prepare a schedule showing the allocation of the processing cost of $120,000 between crushed and sliced pineapple using the net realizable value method. The net realizable value of the juice is to be added to the sales value of the sliced pineapples.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

23

Donovan Steel has two profit centers: Ingots and Stainless Steel. These profit centers rely on services supplied by two service departments: electricity and water. The profit centers' consumption of the service departments' outputs (in millions) is given in the following table: The total operating costs of the two service departments are: Required:

a. Service department costs are allocated to profit centers using the step-down method. Water is the first service department allocated. Compute the cost of electricity per kilowatt-hour using the step-down allocation method.

b. Critically evaluate this allocation method.

a. Service department costs are allocated to profit centers using the step-down method. Water is the first service department allocated. Compute the cost of electricity per kilowatt-hour using the step-down allocation method.

b. Critically evaluate this allocation method.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

24

At the Hilton Apple Fest and Trade Expo, James Jones, owner of Jones Orchard, saw a sign displayed in front of a vendor's booth: i can get you pesticides at $10.00 a gallon-guaranteed in writing! Over a one-year period, the vendor guarantees delivery of between 350,000 and 500,000 gallons of pesticide at a maximum price of $10 per gallon. Since Jones Orchard is currently paying $11.30 per gallon, the offer is appealing. However, Jones uses only 25,000 gallons and the annual management fee for this service is a whopping $275,000.

The only way Jones can see to make the offer work is to form a buying consortium with other farmers. As long as all of the farmers are located within 10 square miles, the vendor is willing to allow the formation of a consortium. Including Jones Orchard, five farms are within this area. Their pesticide needs and anticipated costs are as follows: All of the farmers are willing to participate in the buying consortium as long as there is an anticipated cost savings for each farmer. Everyone agrees that each farmer should pay the same amount for materials. But allocation of the management fee is left entirely up to Jones.

Required:

a. Based upon the numbers provided, demonstrate that this consortium could work.

b. Jones initially considers allocating the management fee either (1) equally between all members or (2) based upon each farmer's percentage of total gallons needed. Would either method work? Show allocation by each method.

c. Jones believes it would make sense to allocate the management fee on an ability-to-pay basis. As the chapter allocates joint costs based upon net realizable value, allocate the management fee based upon the potential dollar savings opportunity of each farm. Is this method feasible?

d. Consider the issue of private versus public information as it relates to the cost allocation schemes presented in this problem. Address whether the information required to implement each scheme is essentially held in common by all of the farmers in the consortium or privately held by each individual farmer. In particular, given that the consortium will allocate the management fee by ability to pay, how might each farmer's privately held cost information serve to undermine the consortium's future existence?

The only way Jones can see to make the offer work is to form a buying consortium with other farmers. As long as all of the farmers are located within 10 square miles, the vendor is willing to allow the formation of a consortium. Including Jones Orchard, five farms are within this area. Their pesticide needs and anticipated costs are as follows: All of the farmers are willing to participate in the buying consortium as long as there is an anticipated cost savings for each farmer. Everyone agrees that each farmer should pay the same amount for materials. But allocation of the management fee is left entirely up to Jones.

Required:

a. Based upon the numbers provided, demonstrate that this consortium could work.

b. Jones initially considers allocating the management fee either (1) equally between all members or (2) based upon each farmer's percentage of total gallons needed. Would either method work? Show allocation by each method.

c. Jones believes it would make sense to allocate the management fee on an ability-to-pay basis. As the chapter allocates joint costs based upon net realizable value, allocate the management fee based upon the potential dollar savings opportunity of each farm. Is this method feasible?

d. Consider the issue of private versus public information as it relates to the cost allocation schemes presented in this problem. Address whether the information required to implement each scheme is essentially held in common by all of the farmers in the consortium or privately held by each individual farmer. In particular, given that the consortium will allocate the management fee by ability to pay, how might each farmer's privately held cost information serve to undermine the consortium's future existence?

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

25

Barry's Fashions operates a Downtown Store and a Mall Store. Both stores use three centralized, corporate service departments (human resources, maintenance, and information management). The following table summarizes the allocation bases used to allocate each service department, the operating expenses (in millions) incurred by each service department, and the amount of each allocation base used by the three service departments and the two stores. Required:

(Round all fractions to three significant digits.)

a. Using the direct allocation method for allocating service department costs, calculate the amount of information management expense allocated to the Mall Store.

b. Using the direct allocation method for allocating service department costs, calculate the allocated cost per line printed for information management services.

c. Using the step-down allocation method for allocating service department costs, calculate the amount of information management expense allocated to the Mall Store. Note that the order of the service departments is as indicated in the table.

d. Using the step-down allocation method for allocating service department costs, calculate the allocated cost per line printed for information management services. Note that the order of the service departments is as indicated in the table.

e. Compare and contrast your answers in parts (b) and (d). First, describe why you get different answers. Second, which number would you recommend management use?

(Round all fractions to three significant digits.)

a. Using the direct allocation method for allocating service department costs, calculate the amount of information management expense allocated to the Mall Store.

b. Using the direct allocation method for allocating service department costs, calculate the allocated cost per line printed for information management services.

c. Using the step-down allocation method for allocating service department costs, calculate the amount of information management expense allocated to the Mall Store. Note that the order of the service departments is as indicated in the table.

d. Using the step-down allocation method for allocating service department costs, calculate the allocated cost per line printed for information management services. Note that the order of the service departments is as indicated in the table.

e. Compare and contrast your answers in parts (b) and (d). First, describe why you get different answers. Second, which number would you recommend management use?

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

26

IFLAX manufactures commercial brushes in two operating divisions (O1 and O2) and has two service departments (Human Resources and Janitorial/Maintenance). The two service departments' costs are allocated to the two operating departments. Human Resources' costs of $600,000 are allocated based on the number of employees, and Janitorial/Maintenance costs of $800,000 are allocated based on square footage. The following table summarizes the number of employees and the square footage in each division and department. Required:

a. Allocate the costs of the two service departments to the two operating divisions using the direct allocation method.

b. Allocate the costs of the two service departments to the two operating divisions using the step-down allocation method where Human Resources is allocated first and Janitorial/Maintenance is allocated second.

c. Allocate the costs of the two service departments to the two operating divisions using the step-down allocation method where Janitorial/Maintenance is allocated first and Human Resources is allocated second.

d. Compute the Human Resource Department cost per employee under the three allocation methods (direct allocation, step-down allocations where Human Resources is first, and the step-down method where Janitorial/Maintenance is first).

e. Compute the Janitorial/Maintenance cost per square foot under the three allocation methods (direct allocation, step-down allocations where Human Resources is first, and the step-down method where Janitorial/Maintenance is first).

f. Briefly discuss the various factors IFLAX management should consider in choosing how to allocate the two service department costs to the two operating divisions.

Required:a. Allocate the costs of the two service departments to the two operating divisions using the direct allocation method.

b. Allocate the costs of the two service departments to the two operating divisions using the step-down allocation method where Human Resources is allocated first and Janitorial/Maintenance is allocated second.

c. Allocate the costs of the two service departments to the two operating divisions using the step-down allocation method where Janitorial/Maintenance is allocated first and Human Resources is allocated second.

d. Compute the Human Resource Department cost per employee under the three allocation methods (direct allocation, step-down allocations where Human Resources is first, and the step-down method where Janitorial/Maintenance is first).

e. Compute the Janitorial/Maintenance cost per square foot under the three allocation methods (direct allocation, step-down allocations where Human Resources is first, and the step-down method where Janitorial/Maintenance is first).

f. Briefly discuss the various factors IFLAX management should consider in choosing how to allocate the two service department costs to the two operating divisions.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 26 flashcards in this deck.