Deck 5: Responsibility Accounting and Transfer Pricing

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Responsibility Centers

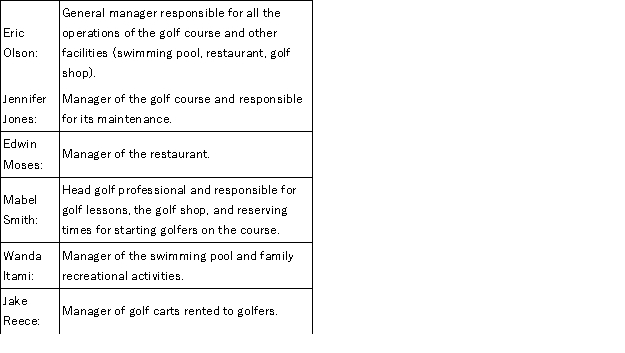

The Maple Way Golf Course is a private club that is owned by the members. It has the following managers and organizational structure: Required:

Required:

Describe each of the managers in terms of being responsible for a cost, profit, or investment center and possible performance measures for each manager.

The Maple Way Golf Course is a private club that is owned by the members. It has the following managers and organizational structure:

Required:Describe each of the managers in terms of being responsible for a cost, profit, or investment center and possible performance measures for each manager.

Question

Question

Question

Question

Question

Question

Question

Question

Perverse Incentives from Accelerated Depreciation on ROI

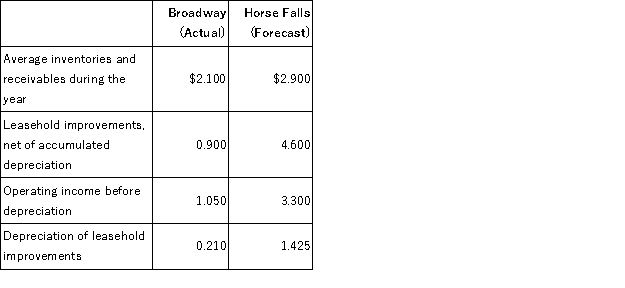

Joan Chris is the Denver district manager of Stale-Mart, an old established chain of more than 100 department stores. Her district contains eight stores in the Denver metropolitan area. One of her stores, the Broadway store, is over 30 years old. Chris began working at the Broadway store as an assistant buyer when the store first opened, and she has fond memories of the store. The Broadway store remains profitable, in part because it is mostly fully depreciated, even though it is small, is in a location that is not seeing rising property values, and has had falling sales volume.

Stale-Mart owns neither the land nor the buildings that house its stores but rather leases them from developers. Lease payments are included in "operating income before depreciation." Each store requires substantial leasehold improvements for interior decoration, display cases, and equipment. These expenditures are capitalized and depreciated as fixed assets by Stale-Mart. Leasehold improvements are depreciated using accelerated methods with estimated lives substantially shorter than the economic life of the store.

All eight stores report to Chris, and like all Stale-Mart district managers, 50 percent of her compensation is a bonus based on the average return on investment of the eight stores (total profits from the eight stores divided by the total eight-store investment). Investment in each store is the sum of inventories, receivables, and leasehold improvements, net of accumulated depreciation.

She is considering a proposal to open a store in the new upscale Horse Falls Mall three miles from the Broadway store. If the Horse Falls proposal is accepted, the Broadway store will be closed. Here are data for the two stores (in millions of dollars): Assume that the forecasts for Horse Falls are accurate. Also assume that the Broadway store data are likely to persist for the next four years with little variation.

Assume that the forecasts for Horse Falls are accurate. Also assume that the Broadway store data are likely to persist for the next four years with little variation.

Stale-Mart finds itself losing market share to newer chains that have opened stores in growth areas of the cities in which they operate. The rate of return on Stale-Mart stock lags that of other firms in the retail department store industry. Its cost of capital is 20 percent.

Required:

a. Calculate the return on total investment and residual income for the Broadway and Horse Falls stores.

b. Chris expects to retire in five years. Do you expect her to accept the proposal to open the Horse Falls store and close the Broadway store? Explain why.

c. Offer a plausible hypothesis supported by facts in the problem that explains why Stale-Mart is losing market share and also explains the poor relative performance of its stock price. What changes at Stale-Mart would you suggest to correct the problem?

Joan Chris is the Denver district manager of Stale-Mart, an old established chain of more than 100 department stores. Her district contains eight stores in the Denver metropolitan area. One of her stores, the Broadway store, is over 30 years old. Chris began working at the Broadway store as an assistant buyer when the store first opened, and she has fond memories of the store. The Broadway store remains profitable, in part because it is mostly fully depreciated, even though it is small, is in a location that is not seeing rising property values, and has had falling sales volume.

Stale-Mart owns neither the land nor the buildings that house its stores but rather leases them from developers. Lease payments are included in "operating income before depreciation." Each store requires substantial leasehold improvements for interior decoration, display cases, and equipment. These expenditures are capitalized and depreciated as fixed assets by Stale-Mart. Leasehold improvements are depreciated using accelerated methods with estimated lives substantially shorter than the economic life of the store.

All eight stores report to Chris, and like all Stale-Mart district managers, 50 percent of her compensation is a bonus based on the average return on investment of the eight stores (total profits from the eight stores divided by the total eight-store investment). Investment in each store is the sum of inventories, receivables, and leasehold improvements, net of accumulated depreciation.

She is considering a proposal to open a store in the new upscale Horse Falls Mall three miles from the Broadway store. If the Horse Falls proposal is accepted, the Broadway store will be closed. Here are data for the two stores (in millions of dollars):

Assume that the forecasts for Horse Falls are accurate. Also assume that the Broadway store data are likely to persist for the next four years with little variation.Stale-Mart finds itself losing market share to newer chains that have opened stores in growth areas of the cities in which they operate. The rate of return on Stale-Mart stock lags that of other firms in the retail department store industry. Its cost of capital is 20 percent.

Required:

a. Calculate the return on total investment and residual income for the Broadway and Horse Falls stores.

b. Chris expects to retire in five years. Do you expect her to accept the proposal to open the Horse Falls store and close the Broadway store? Explain why.

c. Offer a plausible hypothesis supported by facts in the problem that explains why Stale-Mart is losing market share and also explains the poor relative performance of its stock price. What changes at Stale-Mart would you suggest to correct the problem?

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/26

Play

Full screen (f)

Deck 5: Responsibility Accounting and Transfer Pricing

1

The following investment opportunities are available to an investment center manager: Required:

a. If the investment manager is currently making a return on investment of 16 percent, which project(s) would the manager want to pursue?

b. If the cost of capital is 10 percent and the annual earnings approximate cash flows excluding finance charges, which project(s) should be chosen?

c. Suppose only one project can be chosen and the annual earnings approximate cash flows excluding finance charges. Which project should be chosen?

a. If the investment manager is currently making a return on investment of 16 percent, which project(s) would the manager want to pursue?

b. If the cost of capital is 10 percent and the annual earnings approximate cash flows excluding finance charges, which project(s) should be chosen?

c. Suppose only one project can be chosen and the annual earnings approximate cash flows excluding finance charges. Which project should be chosen?

a. The ROI of the four projects are: The manager would only want to accept projects that would raise the existing ROI above 16 percent. Only project B would raise the existing ROI.

b. All projects with an ROI greater than the cost of capital of 10 percent should be chosen. Therefore, projects A, B, and D should be chosen.

c. The project with the highest residual income should be chosen. The residual incomes of the four projects are: Project D has the highest residual income and should be chosen.

b. All projects with an ROI greater than the cost of capital of 10 percent should be chosen. Therefore, projects A, B, and D should be chosen.

c. The project with the highest residual income should be chosen. The residual incomes of the four projects are: Project D has the highest residual income and should be chosen.

2

Grammy Girl Products (GGP) has two divisions, Bones and Biscuits, both of which usually have independence in sourcing and pricing decisions. There is an unlimited supply of raw bones. Biscuits manufactures, amongst other items, a specialty product called BisBone. The BisBone formula requires 70% bone meal and 30% cereal per lbs, plus a dollop of meat flavoring. BisBone is usually sold in 20-lbs cases and processed bones in 5-lbs packs. Cost and sales pricing data appears below. In lieu of its normal processing, Bones sometimes grinds raw bones into bone meal (grinding costs $.05 per lbs) When bone meal is sold to Biscuits, bulk packaging is used which costs $1 per 100 lbs sack; when sold to other firms, it is packed in 50lbs containers, costing $3 each. Bones prices the container product at $180. Biscuits just received an order for 800 cases of one of its specialty products, BisBone, and is contemplating purchasing bone meal from its sister division. Should Biscuits buy bone meal from Bones at the price calculated in Q5-9?

A)Yes, because it is $0.55 per lb cheaper than its external supplier's

B)No, because it is $0.55 per lb more costly than its external supplier's

C)Yes, because it is $0.025 per lb cheaper than its external supplier's

D)No, because it is $0.60 per lb more costly than its external supplier's

E)None of the above

A)Yes, because it is $0.55 per lb cheaper than its external supplier's

B)No, because it is $0.55 per lb more costly than its external supplier's

C)Yes, because it is $0.025 per lb cheaper than its external supplier's

D)No, because it is $0.60 per lb more costly than its external supplier's

E)None of the above

No, because it is $0.55 per lb more costly than its external supplier's

3

Grammy Girl Products (GGP) has two divisions, Bones and Biscuits, both of which usually have independence in sourcing and pricing decisions. There is an unlimited supply of raw bones. Biscuits manufactures, amongst other items, a specialty product called BisBone. The BisBone formula requires 70% bone meal and 30% cereal per lbs, plus a dollop of meat flavoring. BisBone is usually sold in 20-lbs cases and processed bones in 5-lbs packs. Cost and sales pricing data appears below. In lieu of its normal processing, Bones sometimes grinds raw bones into bone meal (grinding costs $.05 per lbs) When bone meal is sold to Biscuits, bulk packaging is used which costs $1 per 100 lbs sack; when sold to other firms, it is packed in 50lbs containers, costing $3 each. Bones prices the container product at $180. Biscuits just received an order for 800 cases of one of its specialty products, BisBone, and is contemplating purchasing bone meal from its sister division. If Bones is at capacity and has sufficient outside customers for the containers, what is the minimum price that it should quote Biscuits per sack of bone meal to maximize GGP's profits?

A)$245

B)$360

C)$297.50

D)$355

E)None of the above

A)$245

B)$360

C)$297.50

D)$355

E)None of the above

$355

4

Transfer Prices and Capacity

Jefferson Company has two divisions: Jefferson Bottles and Jefferson Juice. Jefferson Bottles makes glass containers, which it sells to Jefferson Juice and other companies. Jefferson Bottles has a capacity of 10 million bottles a year. Jefferson Juice currently has a capacity of 3 million bottles of juice per year. Jefferson Bottles has a fixed cost of $100,000 per year and a variable cost of $0.01/bottle. Jefferson Bottles can currently sell all of its output at $0.03/bottle.

Required:

a. What should Jefferson Bottles charge Jefferson Juice for bottles so that both divisions will make appropriate decentralized planning decisions?

b. If Jefferson Bottles can only sell 5 million bottles to outside buyers, what should Jefferson Bottles charge Jefferson Juice for bottles so that both divisions will make appropriate decentralized planning decisions?

Jefferson Company has two divisions: Jefferson Bottles and Jefferson Juice. Jefferson Bottles makes glass containers, which it sells to Jefferson Juice and other companies. Jefferson Bottles has a capacity of 10 million bottles a year. Jefferson Juice currently has a capacity of 3 million bottles of juice per year. Jefferson Bottles has a fixed cost of $100,000 per year and a variable cost of $0.01/bottle. Jefferson Bottles can currently sell all of its output at $0.03/bottle.

Required:

a. What should Jefferson Bottles charge Jefferson Juice for bottles so that both divisions will make appropriate decentralized planning decisions?

b. If Jefferson Bottles can only sell 5 million bottles to outside buyers, what should Jefferson Bottles charge Jefferson Juice for bottles so that both divisions will make appropriate decentralized planning decisions?

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

5

A soft drink company has three bottling plants throughout the country. Bottling occurs at the regional level because of the high cost of transporting bottled soft drinks. The parent company supplies each plant with the syrup. The bottling plants combine the syrup with carbonated soda to make and bottle the soft drinks. The bottled soft drinks are then sent to regional grocery stores.

The bottling plants are treated as costs centers. The managers of the bottling plants are evaluated based on minimizing the cost per soft drink bottled and delivered. Each bottling plant uses the same equipment, but some produce more bottles of soft drinks because of different demand. The costs and output for each bottling plant are: Required:

a. Estimate the average cost per unit for each plant.

b. Why would the manager of plant A be unhappy with using the average cost as the performance measure?

c. What is an alternative performance measure that would make the manager of plant A happier?

d. Under what circumstances might the average cost be a better performance measure?

The bottling plants are treated as costs centers. The managers of the bottling plants are evaluated based on minimizing the cost per soft drink bottled and delivered. Each bottling plant uses the same equipment, but some produce more bottles of soft drinks because of different demand. The costs and output for each bottling plant are: Required:

a. Estimate the average cost per unit for each plant.

b. Why would the manager of plant A be unhappy with using the average cost as the performance measure?

c. What is an alternative performance measure that would make the manager of plant A happier?

d. Under what circumstances might the average cost be a better performance measure?

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

6

Mesopotamian Materials Inc. (MMI) has two decentralized divisions (Ur and Babylon) that have decision making responsibility over the amount of resources invested in their divisions. Recent financial extracts for both divisions are presented below: *Net income is after tax but before interest MMI's weighted average cost of capital (WACC) is 11.5%. The MMI measures division performance based on the book value of net assets. The producer price index 15 years ago was 100, 116 five years ago, and currently is 125.

Using historical costs, which is true?

A)Ur's return on sales (net income percentage) is 14%

B)Ur's return on net assets (RONA) is 74%

C)Babylon's net asset turnover is 6.75

D)Babylon's return on assets (ROA) is 40%

E)None of the above

Using historical costs, which is true?

A)Ur's return on sales (net income percentage) is 14%

B)Ur's return on net assets (RONA) is 74%

C)Babylon's net asset turnover is 6.75

D)Babylon's return on assets (ROA) is 40%

E)None of the above

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

7

Mesopotamian Materials Inc. (MMI) has two decentralized divisions (Ur and Babylon) that have decision making responsibility over the amount of resources invested in their divisions. Recent financial extracts for both divisions are presented below: *Net income is after tax but before interest MMI's weighted average cost of capital (WACC) is 11.5%. The MMI measures division performance based on the book value of net assets. The producer price index 15 years ago was 100, 116 five years ago, and currently is 125.

Which is true, when fixed asset costs are adjusted upward for inflation?

A)Babylon's RONA is 35.8%

B)Babylon's RONA is 26.3%

C)Ur's depreciation expense increases by $19 more than Babylon's

D)Babylon's price adjustment multiplier is 1.16

E)None of the above

Which is true, when fixed asset costs are adjusted upward for inflation?

A)Babylon's RONA is 35.8%

B)Babylon's RONA is 26.3%

C)Ur's depreciation expense increases by $19 more than Babylon's

D)Babylon's price adjustment multiplier is 1.16

E)None of the above

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

8

Grammy Girl Products (GGP) has two divisions, Bones and Biscuits, both of which usually have independence in sourcing and pricing decisions. There is an unlimited supply of raw bones. Biscuits manufactures, amongst other items, a specialty product called BisBone. The BisBone formula requires 70% bone meal and 30% cereal per lbs, plus a dollop of meat flavoring. BisBone is usually sold in 20-lbs cases and processed bones in 5-lbs packs. Cost and sales pricing data appears below. In lieu of its normal processing, Bones sometimes grinds raw bones into bone meal (grinding costs $.05 per lbs) When bone meal is sold to Biscuits, bulk packaging is used which costs $1 per 100 lbs sack; when sold to other firms, it is packed in 50lbs containers, costing $3 each. Bones prices the container product at $180. Biscuits just received an order for 800 cases of one of its specialty products, BisBone, and is contemplating purchasing bone meal from its sister division. If Bones is operating below capacity, what is the minimum price that it should quote Biscuits per sack of bone meal to maximize GGP's profits?

A)$240

B)$239

C)$251.20

D)$296

E)None of the above

A)$240

B)$239

C)$251.20

D)$296

E)None of the above

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

9

Decision Rights Assignments and EVA

At a Stern-Stewart conference, one of the topics discussed was "taking EVA to the shop floor." This session described "driving EVA analysis, decision making and incentives down through every level of an organization." If you were attending this session, what questions would you ask the panelists?

At a Stern-Stewart conference, one of the topics discussed was "taking EVA to the shop floor." This session described "driving EVA analysis, decision making and incentives down through every level of an organization." If you were attending this session, what questions would you ask the panelists?

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

10

Mesopotamian Materials Inc. (MMI) has two decentralized divisions (Ur and Babylon) that have decision making responsibility over the amount of resources invested in their divisions. Recent financial extracts for both divisions are presented below: *Net income is after tax but before interest MMI's weighted average cost of capital (WACC) is 11.5%. The MMI measures division performance based on the book value of net assets. The producer price index 15 years ago was 100, 116 five years ago, and currently is 125.

Using historical costs, which is true?

A)Babylon is a profit center

B)At a WACC of 5%, Ur's residual income is lower than Babylon's by $122

C)At the planned WACC (11.5%), Ur's residual income is higher than Babylon's by $87

D)At a WACC of 25%, Ur's residual income is higher than Babylon's by $122

E)None of the above

Using historical costs, which is true?

A)Babylon is a profit center

B)At a WACC of 5%, Ur's residual income is lower than Babylon's by $122

C)At the planned WACC (11.5%), Ur's residual income is higher than Babylon's by $87

D)At a WACC of 25%, Ur's residual income is higher than Babylon's by $122

E)None of the above

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

11

Given the following division performance indicators, which is true?

A)A's return on assets is double that of B

B)C is the best division at managing its assets

C)A's sales are 66.7% bigger than C's

D)B would benefit least from a 10% increase in sales

E)All of the above

A)A's return on assets is double that of B

B)C is the best division at managing its assets

C)A's sales are 66.7% bigger than C's

D)B would benefit least from a 10% increase in sales

E)All of the above

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

12

The Eastern University Business School teaches some undergraduate business courses for students in the Eastern University College of Arts and Science (CAS). The 6,000 undergraduates generate 2,000 undergraduate student course enrollments in business courses per year. The B-school and CAS are treated as profit centers in that their budgets contain student tuition revenues as well as costs. The deans have discretion to set tuition and salaries and determine hiring as long as they operate with no deficit (revenues = expenses). Undergraduate tuition is $12,000 per year and each student takes eight courses per year. Average undergraduate financial aid amounts to 20% of gross tuition. The current transfer price rule is gross tuition per course less average financial aid.

This transfer price rule gives net tuition to the B-school as a revenue and deducts an equal amount from the CAS budget. The CAS dean argues that the current system is grossly unfair. CAS must provide costly services for undergraduates to maintain a top-rated undergraduate program. For example, career counseling, academic advising, sports programs, and the admissions office are costs that must be incurred if undergraduates are to enroll at Eastern. Therefore, the CAS dean argues, the average cost of these services per undergraduate student course enrollment should be deducted from the tuition transfer price. These undergraduate student services total $9.6 million per year.

Required:

a. Calculate the current revenue the B-school is receiving from undergraduate business courses. What will it be if the CAS dean's proposal is adopted?

b. Discuss the pros and cons of the CAS dean's proposal.

c. As special assistant to the B-school dean, prepare a response to the proposed tuition transfer pricing scheme.

This transfer price rule gives net tuition to the B-school as a revenue and deducts an equal amount from the CAS budget. The CAS dean argues that the current system is grossly unfair. CAS must provide costly services for undergraduates to maintain a top-rated undergraduate program. For example, career counseling, academic advising, sports programs, and the admissions office are costs that must be incurred if undergraduates are to enroll at Eastern. Therefore, the CAS dean argues, the average cost of these services per undergraduate student course enrollment should be deducted from the tuition transfer price. These undergraduate student services total $9.6 million per year.

Required:

a. Calculate the current revenue the B-school is receiving from undergraduate business courses. What will it be if the CAS dean's proposal is adopted?

b. Discuss the pros and cons of the CAS dean's proposal.

c. As special assistant to the B-school dean, prepare a response to the proposed tuition transfer pricing scheme.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

13

Responsibility Centers

The Maple Way Golf Course is a private club that is owned by the members. It has the following managers and organizational structure: Required:

Describe each of the managers in terms of being responsible for a cost, profit, or investment center and possible performance measures for each manager.

The Maple Way Golf Course is a private club that is owned by the members. It has the following managers and organizational structure:

Required:Describe each of the managers in terms of being responsible for a cost, profit, or investment center and possible performance measures for each manager.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

14

A chair manufacturer has two divisions: framing and upholstering. The framing costs are $100 per chair and the upholstering costs are $200 per chair. The company makes 5,000 chairs each year, which are sold for $500.

Required:

a. What is the profit of each division if the transfer price is $150?

b. What is the profit of each division if the transfer price is $200?

Required:

a. What is the profit of each division if the transfer price is $150?

b. What is the profit of each division if the transfer price is $200?

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

15

Transfer Prices

The Alpha Division of the Carlson Company manufactures product X at a variable cost of $40 per unit. Alpha Division's fixed costs, which are sunk, are $20 per unit. The market price of X is $70 per unit. Beta Division of Carlson Company uses product X to make Y. The variable costs to convert X to Y are $20 per unit and the fixed costs, which are sunk, are $10 per unit. The product Y sells for $80 per unit.

Required:

a. What transfer price of X causes divisional managers to make decentralized decisions that maximize Carlson Company's profit if each division is treated as a profit center?

b. Given the transfer price from part (a), what should the manager of the Beta Division do?

c. Suppose there is no market price for product X. What transfer price should be used for decentralized decision-making?

d. If there is no market for product X, is the operations of the Beta Division profitable?

The Alpha Division of the Carlson Company manufactures product X at a variable cost of $40 per unit. Alpha Division's fixed costs, which are sunk, are $20 per unit. The market price of X is $70 per unit. Beta Division of Carlson Company uses product X to make Y. The variable costs to convert X to Y are $20 per unit and the fixed costs, which are sunk, are $10 per unit. The product Y sells for $80 per unit.

Required:

a. What transfer price of X causes divisional managers to make decentralized decisions that maximize Carlson Company's profit if each division is treated as a profit center?

b. Given the transfer price from part (a), what should the manager of the Beta Division do?

c. Suppose there is no market price for product X. What transfer price should be used for decentralized decision-making?

d. If there is no market for product X, is the operations of the Beta Division profitable?

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

16

Economic value added (EVA):

A)is a variant of residual income

B)ignores taxes

C)is a registered trademark owned by Stern Stewart & Co

D)is easy to administer

E)a) and c) only

A)is a variant of residual income

B)ignores taxes

C)is a registered trademark owned by Stern Stewart & Co

D)is easy to administer

E)a) and c) only

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

17

Grammy Girl Products (GGP) has two divisions, Bones and Biscuits, both of which usually have independence in sourcing and pricing decisions. There is an unlimited supply of raw bones. Biscuits manufactures, amongst other items, a specialty product called BisBone. The BisBone formula requires 70% bone meal and 30% cereal per lbs, plus a dollop of meat flavoring. BisBone is usually sold in 20-lbs cases and processed bones in 5-lbs packs. Cost and sales pricing data appears below. In lieu of its normal processing, Bones sometimes grinds raw bones into bone meal (grinding costs $.05 per lbs) When bone meal is sold to Biscuits, bulk packaging is used which costs $1 per 100 lbs sack; when sold to other firms, it is packed in 50lbs containers, costing $3 each. Bones prices the container product at $180. Biscuits just received an order for 800 cases of one of its specialty products, BisBone, and is contemplating purchasing bone meal from its sister division. Should GGP encourage an internal transaction for this order if Bones has outside customers for the bone meal, and, if so, at what price?

A)No, because it will undermine the benefits of decentralization

B)Yes, at $2.70 per lb

C)No, because GGP will be worse off

D)Yes, at the external market price of $3 per lb

E)Yes, but at some other price

A)No, because it will undermine the benefits of decentralization

B)Yes, at $2.70 per lb

C)No, because GGP will be worse off

D)Yes, at the external market price of $3 per lb

E)Yes, but at some other price

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

18

Which is true of a firm's transfer pricing policy?

A)Produces optimal results when set at the head office

B)Always promotes goal congruence

C)Leads to accurate measures of local performance

D)Is often designed to minimize tax expense

E)All of the above

A)Produces optimal results when set at the head office

B)Always promotes goal congruence

C)Leads to accurate measures of local performance

D)Is often designed to minimize tax expense

E)All of the above

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

19

Complex companies adopt decentralization in order to realize all of the following benefits, except:

A)delegation of control to lower levels of management, thus facilitating their training and development

B)improved awareness of, and response to, local conditions

C)reduced record-keeping

D)shorter elapsed time from problem identification to decision-making and implementation

E)no exceptions above

A)delegation of control to lower levels of management, thus facilitating their training and development

B)improved awareness of, and response to, local conditions

C)reduced record-keeping

D)shorter elapsed time from problem identification to decision-making and implementation

E)no exceptions above

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

20

Mesopotamian Materials Inc. (MMI) has two decentralized divisions (Ur and Babylon) that have decision making responsibility over the amount of resources invested in their divisions. Recent financial extracts for both divisions are presented below: *Net income is after tax but before interest MMI's weighted average cost of capital (WACC) is 11.5%. The MMI measures division performance based on the book value of net assets. The producer price index 15 years ago was 100, 116 five years ago, and currently is 125.

Ur can increase its ROI by:

A)increasing product contribution margin

B)increasing sales volume

C)reducing discretionary expenses

D)taking on debt

E)all of the above

Ur can increase its ROI by:

A)increasing product contribution margin

B)increasing sales volume

C)reducing discretionary expenses

D)taking on debt

E)all of the above

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

21

Perverse Incentives from Accelerated Depreciation on ROI

Joan Chris is the Denver district manager of Stale-Mart, an old established chain of more than 100 department stores. Her district contains eight stores in the Denver metropolitan area. One of her stores, the Broadway store, is over 30 years old. Chris began working at the Broadway store as an assistant buyer when the store first opened, and she has fond memories of the store. The Broadway store remains profitable, in part because it is mostly fully depreciated, even though it is small, is in a location that is not seeing rising property values, and has had falling sales volume.

Stale-Mart owns neither the land nor the buildings that house its stores but rather leases them from developers. Lease payments are included in "operating income before depreciation." Each store requires substantial leasehold improvements for interior decoration, display cases, and equipment. These expenditures are capitalized and depreciated as fixed assets by Stale-Mart. Leasehold improvements are depreciated using accelerated methods with estimated lives substantially shorter than the economic life of the store.

All eight stores report to Chris, and like all Stale-Mart district managers, 50 percent of her compensation is a bonus based on the average return on investment of the eight stores (total profits from the eight stores divided by the total eight-store investment). Investment in each store is the sum of inventories, receivables, and leasehold improvements, net of accumulated depreciation.

She is considering a proposal to open a store in the new upscale Horse Falls Mall three miles from the Broadway store. If the Horse Falls proposal is accepted, the Broadway store will be closed. Here are data for the two stores (in millions of dollars): Assume that the forecasts for Horse Falls are accurate. Also assume that the Broadway store data are likely to persist for the next four years with little variation.

Stale-Mart finds itself losing market share to newer chains that have opened stores in growth areas of the cities in which they operate. The rate of return on Stale-Mart stock lags that of other firms in the retail department store industry. Its cost of capital is 20 percent.

Required:

a. Calculate the return on total investment and residual income for the Broadway and Horse Falls stores.

b. Chris expects to retire in five years. Do you expect her to accept the proposal to open the Horse Falls store and close the Broadway store? Explain why.

c. Offer a plausible hypothesis supported by facts in the problem that explains why Stale-Mart is losing market share and also explains the poor relative performance of its stock price. What changes at Stale-Mart would you suggest to correct the problem?

Joan Chris is the Denver district manager of Stale-Mart, an old established chain of more than 100 department stores. Her district contains eight stores in the Denver metropolitan area. One of her stores, the Broadway store, is over 30 years old. Chris began working at the Broadway store as an assistant buyer when the store first opened, and she has fond memories of the store. The Broadway store remains profitable, in part because it is mostly fully depreciated, even though it is small, is in a location that is not seeing rising property values, and has had falling sales volume.

Stale-Mart owns neither the land nor the buildings that house its stores but rather leases them from developers. Lease payments are included in "operating income before depreciation." Each store requires substantial leasehold improvements for interior decoration, display cases, and equipment. These expenditures are capitalized and depreciated as fixed assets by Stale-Mart. Leasehold improvements are depreciated using accelerated methods with estimated lives substantially shorter than the economic life of the store.

All eight stores report to Chris, and like all Stale-Mart district managers, 50 percent of her compensation is a bonus based on the average return on investment of the eight stores (total profits from the eight stores divided by the total eight-store investment). Investment in each store is the sum of inventories, receivables, and leasehold improvements, net of accumulated depreciation.

She is considering a proposal to open a store in the new upscale Horse Falls Mall three miles from the Broadway store. If the Horse Falls proposal is accepted, the Broadway store will be closed. Here are data for the two stores (in millions of dollars):

Assume that the forecasts for Horse Falls are accurate. Also assume that the Broadway store data are likely to persist for the next four years with little variation.Stale-Mart finds itself losing market share to newer chains that have opened stores in growth areas of the cities in which they operate. The rate of return on Stale-Mart stock lags that of other firms in the retail department store industry. Its cost of capital is 20 percent.

Required:

a. Calculate the return on total investment and residual income for the Broadway and Horse Falls stores.

b. Chris expects to retire in five years. Do you expect her to accept the proposal to open the Horse Falls store and close the Broadway store? Explain why.

c. Offer a plausible hypothesis supported by facts in the problem that explains why Stale-Mart is losing market share and also explains the poor relative performance of its stock price. What changes at Stale-Mart would you suggest to correct the problem?

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

22

Transfer Prices and External Sourcing

Levis is a large manufacturer of office equipment, including copiers. Its electronics division is a cost center. Currently, electronics sells circuit boards to other divisions exclusively. Levis has a policy that internal transfers are to be priced at full cost (fixed + variable). Thirty percent of the cost of a board is considered fixed.

The electronics division is operating at 75 percent of capacity. Because there is excess capacity, electronics is seeking opportunities to sell boards to non-Levis firms. The electronics division policy on non-Levis sales states that each job must cover full cost and a minimum 10 percent profit. Electronics division management will be measured on its ability to make the minimum profit on any non-Levis contracts that are accepted.

Copy products is another Levis division. Copy products has recently reached an agreement with Siviy, a non-Levis firm, for the assembly of subsystems for a copier. Copy products has selected Siviy because of Siviy's low labor cost. The subsystem Siviy will assemble requires circuit boards. Copy products has stipulated that Siviy must purchase the circuit boards from the electronics division because of electronics' high quality and dependability.

Electronic products is anxious to accept this new work from copy products because it will increase electronic product's workload by 15 percent.

In negotiating a contract price with Siviy, copy products needs to take into account the cost of the circuit boards from electronics. The financial analyst from copy products assumes that electronics will sell the circuit boards to Siviy at full cost (the same as the internal transfer price). Electronics is considering adding the minimum 10 percent profit margin to their full cost and transferring at that price to Siviy.

Copy products is preparing to negotiate its contract with Siviy. Develop and discuss at least three options that may be used in establishing the transfer price between the electronics division and Siviy. Discuss the advantages and disadvantages of each.

Levis is a large manufacturer of office equipment, including copiers. Its electronics division is a cost center. Currently, electronics sells circuit boards to other divisions exclusively. Levis has a policy that internal transfers are to be priced at full cost (fixed + variable). Thirty percent of the cost of a board is considered fixed.

The electronics division is operating at 75 percent of capacity. Because there is excess capacity, electronics is seeking opportunities to sell boards to non-Levis firms. The electronics division policy on non-Levis sales states that each job must cover full cost and a minimum 10 percent profit. Electronics division management will be measured on its ability to make the minimum profit on any non-Levis contracts that are accepted.

Copy products is another Levis division. Copy products has recently reached an agreement with Siviy, a non-Levis firm, for the assembly of subsystems for a copier. Copy products has selected Siviy because of Siviy's low labor cost. The subsystem Siviy will assemble requires circuit boards. Copy products has stipulated that Siviy must purchase the circuit boards from the electronics division because of electronics' high quality and dependability.

Electronic products is anxious to accept this new work from copy products because it will increase electronic product's workload by 15 percent.

In negotiating a contract price with Siviy, copy products needs to take into account the cost of the circuit boards from electronics. The financial analyst from copy products assumes that electronics will sell the circuit boards to Siviy at full cost (the same as the internal transfer price). Electronics is considering adding the minimum 10 percent profit margin to their full cost and transferring at that price to Siviy.

Copy products is preparing to negotiate its contract with Siviy. Develop and discuss at least three options that may be used in establishing the transfer price between the electronics division and Siviy. Discuss the advantages and disadvantages of each.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

23

Comparing ROA and EVA

General Motors's CFO, Michael Losh, converted GM's performance measure for compensation from net income to ROA. In explaining the move), he said, "ROA was a logical next step because all those other measures generally have focused on the income statement. Moving to ROA means that we're going to focus not only on the income statement, but on the balance sheet and effective utilization of the assets and liabilities that are on the balance sheet as well.

"ROA is a better measure for us than EVA. … EVA is simpler conceptually, because it automatically builds on growth, whereas with this approach we know that we've got to have growth as an overlying objective. … EVA is more comprehensive. And that has a certain appeal to me. But, given our situation, particularly in our North American operations, it just would not have been the right measure.

"ROA works for us and EVA doesn't because our operations have to deal with those two different kinds of starting points. Within GM, in our North American operations, you've got a classic turnaround situation, and in our international operations, you've got a classic growth situation. You can apply ROA to both; you can't apply EVA to both."

Required:

a. Explain how ROA focuses on both the income statement and the balance sheet.

b. Explain why EVA is more "comprehensive" than ROA.

c. Do you agree with Losh's statement that "you can apply ROA to both; you can't apply EVA to both"? Explain.

General Motors's CFO, Michael Losh, converted GM's performance measure for compensation from net income to ROA. In explaining the move), he said, "ROA was a logical next step because all those other measures generally have focused on the income statement. Moving to ROA means that we're going to focus not only on the income statement, but on the balance sheet and effective utilization of the assets and liabilities that are on the balance sheet as well.

"ROA is a better measure for us than EVA. … EVA is simpler conceptually, because it automatically builds on growth, whereas with this approach we know that we've got to have growth as an overlying objective. … EVA is more comprehensive. And that has a certain appeal to me. But, given our situation, particularly in our North American operations, it just would not have been the right measure.

"ROA works for us and EVA doesn't because our operations have to deal with those two different kinds of starting points. Within GM, in our North American operations, you've got a classic turnaround situation, and in our international operations, you've got a classic growth situation. You can apply ROA to both; you can't apply EVA to both."

Required:

a. Explain how ROA focuses on both the income statement and the balance sheet.

b. Explain why EVA is more "comprehensive" than ROA.

c. Do you agree with Losh's statement that "you can apply ROA to both; you can't apply EVA to both"? Explain.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

24

Sunstar sells a full line of small home kitchen appliances, including toasters, coffee makers, blenders, and bread machines. It is organized into a marketing division and a manufacturing division. The manufacturing division is composed of several plants, each a cost center, making one type of appliance. The toaster plant makes different models of toasters and toaster ovens. Most of the parts, such as the heating elements and racks for each toaster, are purchased externally, but a few are manufactured in the plant, including the sheet metal forming the body of the toaster. The toaster plant has a number of departments including sheet metal fabrication, purchasing, assembly, quality assurance, packaging, and shipping.

Each toaster model has a product manager who is responsible for manufacturing the product. Each product manager manages several similar models. Product managers, with the help of purchasing, negotiate prices and delivery schedules with external part vendors. Sunstar's corporate headquarters sets all the toaster models' selling prices and quarterly production quotas to maximize profits. Product managers' compensation and promotions are based on lowering unit costs and meeting corporate headquarters' production quota.

The product manager sets production schedule quotas for the product and is responsible for ensuring that the distribution division of Sunstar has the appropriate number of toasters at each distribution center. Product managers have discretion over outsourcing, production methods, and labor scheduling to manufacture the particular models under their control. For example, they do not have to produce the exact number of toasters set by corporate headquarters quarterly, but rather product managers have some discretion to produce more or fewer toasters as long as the distribution centers have enough inventory to meet demand.

The following data were collected for one particular toaster oven, model CVP-6907. These data are corporate forecasts for model CVP-6907 in regard to how prices and total manufacturing costs are expected to vary with the number of toasters manufactured (and sold) per day. In addition to the manufacturing costs reported in the table, there are $10 of variable selling and distribution costs per toaster.

Required:

a. What daily production quantity would you expect the product manager for model CVP-6907 to set? Why?

b. Evaluate Sunstar's performance evaluation system as it pertains to product managers. What behavior does it likely create among manufacturing product managers?

c. Describe the changes you would recommend Sunstar consider making in its performance evaluation system for manufacturing product managers.

Each toaster model has a product manager who is responsible for manufacturing the product. Each product manager manages several similar models. Product managers, with the help of purchasing, negotiate prices and delivery schedules with external part vendors. Sunstar's corporate headquarters sets all the toaster models' selling prices and quarterly production quotas to maximize profits. Product managers' compensation and promotions are based on lowering unit costs and meeting corporate headquarters' production quota.

The product manager sets production schedule quotas for the product and is responsible for ensuring that the distribution division of Sunstar has the appropriate number of toasters at each distribution center. Product managers have discretion over outsourcing, production methods, and labor scheduling to manufacture the particular models under their control. For example, they do not have to produce the exact number of toasters set by corporate headquarters quarterly, but rather product managers have some discretion to produce more or fewer toasters as long as the distribution centers have enough inventory to meet demand.

The following data were collected for one particular toaster oven, model CVP-6907. These data are corporate forecasts for model CVP-6907 in regard to how prices and total manufacturing costs are expected to vary with the number of toasters manufactured (and sold) per day. In addition to the manufacturing costs reported in the table, there are $10 of variable selling and distribution costs per toaster.

Required:

a. What daily production quantity would you expect the product manager for model CVP-6907 to set? Why?

b. Evaluate Sunstar's performance evaluation system as it pertains to product managers. What behavior does it likely create among manufacturing product managers?

c. Describe the changes you would recommend Sunstar consider making in its performance evaluation system for manufacturing product managers.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

25

Transfer Pricing in the Presence of Divisional Interdependencies

PepsiCo, a major soft drink company, had a restaurant division consisting of Kentucky Fried Chicken, Taco Bell, and Pizza Hut. The only cola beverage these restaurants served was Pepsi. Assume that the major reason PepsiCo owned fast food restaurants is an attempt to increase its share of the cola market. Under this assumption, some Pizza Hut patrons who order a cola at the restaurant and are told they are drinking a Pepsi will switch and become Pepsi drinkers instead of Coke drinkers on other purchase occasions. However, studies have shown that some customers refuse to eat at restaurants unless they can get a Coke.

PepsiCo sells Pepsi Cola to non-PepsiCo restaurants at $0.53 per gallon. This is the market price of Pepsi-Cola. Pepsi-Cola's variable manufacturing cost is $0.09 per gallon and its total (fixed and variable) manufacturing cost is $0.22 per gallon. PepsiCo produces Pepsi-Cola in numerous plants located around the world. Plant capacity can be added in small increments (e.g., a half-million gallons per year). The cost of additional capacity is approximately equal to the fixed costs per gallon of $0.13.

Required:

What transfer price should be set for Pepsi transferred from the soft drink division of PepsiCo to a PepsiCo restaurant such as Taco Bell? Justify your answer.

PepsiCo, a major soft drink company, had a restaurant division consisting of Kentucky Fried Chicken, Taco Bell, and Pizza Hut. The only cola beverage these restaurants served was Pepsi. Assume that the major reason PepsiCo owned fast food restaurants is an attempt to increase its share of the cola market. Under this assumption, some Pizza Hut patrons who order a cola at the restaurant and are told they are drinking a Pepsi will switch and become Pepsi drinkers instead of Coke drinkers on other purchase occasions. However, studies have shown that some customers refuse to eat at restaurants unless they can get a Coke.

PepsiCo sells Pepsi Cola to non-PepsiCo restaurants at $0.53 per gallon. This is the market price of Pepsi-Cola. Pepsi-Cola's variable manufacturing cost is $0.09 per gallon and its total (fixed and variable) manufacturing cost is $0.22 per gallon. PepsiCo produces Pepsi-Cola in numerous plants located around the world. Plant capacity can be added in small increments (e.g., a half-million gallons per year). The cost of additional capacity is approximately equal to the fixed costs per gallon of $0.13.

Required:

What transfer price should be set for Pepsi transferred from the soft drink division of PepsiCo to a PepsiCo restaurant such as Taco Bell? Justify your answer.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

26

Double Marginalization of Transfer Pricing

Serviflow manufactures products that move and measure various fluids, ranging from water to high-viscosity polymers, corrosive or abrasive chemicals, toxic substances, and other difficult pumping media. The Supply Division, a profit center, manufactures all products for the various marketing divisions, which also are profit centers. One of the marketing divisions, the Natural Gas Marketing Division (NGMD), designed and sells a liquid natural gas pressure regulating valve, NGM4010, which the Supply Division manufactures.

To produce one NGM4010, the Supply Division incurs a variable cost of $6, and NGMD incurs a variable cost of $14. The $6 and $14 variable costs per unit of NGM4010 are constant and do not vary with the number of units produced or sold. While both the Supply Division and NGMD have substantial fixed costs, for the purpose of this question, assume both divisions' fixed costs are zero.

The following table depicts how the price of the NGM4010 to outside customers varies with the number of units sold each week. (That is, the external customers' weekly demand curve for NGM4010 is given by the following formula: P 5 1000 2 10Q, where P is the final selling price and Q is the total number of units sold each week.) Required:

a. If the senior managers in the corporate headquarters of Serviflow knew all the relevant information (the variable costs in the Supply Division and NGMD and the market demand curve for NGM4010), what profit maximizing final price would they set for NGM4010 and how many units would they tell the Supply Division to produce and NGMD to sell each week?

b. How much total profit does Serviflow generate each week based on the profit maximizing price-quantity decision made in part (a)?

c. Assume that Serviflow senior managers do not know all the relevant information to choose the profit maximizing price-quantity decision for NGM4010. Instead, they assign the decision rights to set the transfer price to the Supply Division. Assume the Supply Division knows how many units of NGM4010 NGMD will purchase as a function of the transfer price. The following table shows how NGMD's purchase decision of NGM4010 depends on the transfer price set by the Supply Division. (In other words, the Supply Division knows that NGMD's demand curve for NGM4010 is T 5 986 2 20Q, where T is the transfer price and Q is the number of units of NGM4010 transferred from Supply to NGMD and sold by NGMD each week.) What transfer price will the Supply Division select to maximize the Supply Division's profit on NGM4010?

d. If the Supply Division selects the transfer price to maximize its profits in part (c), how much profit will the Supply Division make each week, and how much profit will NGMD make each week?

e. Compare the level of firmwide profits calculated in part (b) with the sum of the Supply Division's and NGMD's profits calculated in part (d). Which one is larger (firm profits or Supply Division profits plus NGMD profits), and explain why.

f. Suppose corporate headquarters has all the information about customer demand and costs in the two divisions [the same assumption as in part (a)], but instead of telling the two divisions how many units to produce and transfer each week, they set the transfer price on NGM4010. What transfer price would corporate headquarters set in order to maximize firmwide profit?

g. What organizational problems are created if the transfer price for NGM4010 is set following your recommendation in part (f) above? Describe the dysfunctional incentives created by such a transfer pricing rule.

Serviflow manufactures products that move and measure various fluids, ranging from water to high-viscosity polymers, corrosive or abrasive chemicals, toxic substances, and other difficult pumping media. The Supply Division, a profit center, manufactures all products for the various marketing divisions, which also are profit centers. One of the marketing divisions, the Natural Gas Marketing Division (NGMD), designed and sells a liquid natural gas pressure regulating valve, NGM4010, which the Supply Division manufactures.

To produce one NGM4010, the Supply Division incurs a variable cost of $6, and NGMD incurs a variable cost of $14. The $6 and $14 variable costs per unit of NGM4010 are constant and do not vary with the number of units produced or sold. While both the Supply Division and NGMD have substantial fixed costs, for the purpose of this question, assume both divisions' fixed costs are zero.

The following table depicts how the price of the NGM4010 to outside customers varies with the number of units sold each week. (That is, the external customers' weekly demand curve for NGM4010 is given by the following formula: P 5 1000 2 10Q, where P is the final selling price and Q is the total number of units sold each week.) Required:

a. If the senior managers in the corporate headquarters of Serviflow knew all the relevant information (the variable costs in the Supply Division and NGMD and the market demand curve for NGM4010), what profit maximizing final price would they set for NGM4010 and how many units would they tell the Supply Division to produce and NGMD to sell each week?

b. How much total profit does Serviflow generate each week based on the profit maximizing price-quantity decision made in part (a)?

c. Assume that Serviflow senior managers do not know all the relevant information to choose the profit maximizing price-quantity decision for NGM4010. Instead, they assign the decision rights to set the transfer price to the Supply Division. Assume the Supply Division knows how many units of NGM4010 NGMD will purchase as a function of the transfer price. The following table shows how NGMD's purchase decision of NGM4010 depends on the transfer price set by the Supply Division. (In other words, the Supply Division knows that NGMD's demand curve for NGM4010 is T 5 986 2 20Q, where T is the transfer price and Q is the number of units of NGM4010 transferred from Supply to NGMD and sold by NGMD each week.) What transfer price will the Supply Division select to maximize the Supply Division's profit on NGM4010?

d. If the Supply Division selects the transfer price to maximize its profits in part (c), how much profit will the Supply Division make each week, and how much profit will NGMD make each week?

e. Compare the level of firmwide profits calculated in part (b) with the sum of the Supply Division's and NGMD's profits calculated in part (d). Which one is larger (firm profits or Supply Division profits plus NGMD profits), and explain why.

f. Suppose corporate headquarters has all the information about customer demand and costs in the two divisions [the same assumption as in part (a)], but instead of telling the two divisions how many units to produce and transfer each week, they set the transfer price on NGM4010. What transfer price would corporate headquarters set in order to maximize firmwide profit?

g. What organizational problems are created if the transfer price for NGM4010 is set following your recommendation in part (f) above? Describe the dysfunctional incentives created by such a transfer pricing rule.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 26 flashcards in this deck.