Deck 25: The Heath Jarrow Morton Libor Model

Full screen (f)

Question

Question

Use the following data for a caplet and floorlet to answer the questions that follow:

What is the floorlet's value?

A) 0.148434

B) 0.224304

C) 0.005835

D) 0.008877

E) 0.001248

What is the floorlet's value?

A) 0.148434

B) 0.224304

C) 0.005835

D) 0.008877

E) 0.001248

Question

Question

Question

Question

Zero-coupon bond prices are given by B(0,T ),where 0 is today,and T (measured in years)is the bond's maturity date.

Considering the time interval from 1 year to 1.5 years,the simple forward rate is given by:

A) 0.041667

B) 0.043478

C) 0.042588

D) 0.042553

E) None of these answers are correct.

Considering the time interval from 1 year to 1.5 years,the simple forward rate is given by:

A) 0.041667

B) 0.043478

C) 0.042588

D) 0.042553

E) None of these answers are correct.

Question

Zero-coupon bond prices are given by B(0,T ),where 0 is today,and T (measured in years)is the bond's maturity date.

The spot rate f (0,0)and the forward rate f (0,1)are given by:

A) 0.041667 and 0.042588

B) 0.041667 and 0.043478

C) 0.041667 and 0.042553

D) 0.043478 and 0.045455

E) None of these answers are correct.

The spot rate f (0,0)and the forward rate f (0,1)are given by:

A) 0.041667 and 0.042588

B) 0.041667 and 0.043478

C) 0.041667 and 0.042553

D) 0.043478 and 0.045455

E) None of these answers are correct.

Question

Question

Question

Zero-coupon bond prices are given by B(0,T ),where 0 is today,and T (measured in years)is the bond's maturity date.

Suppose that you compute the simple forward rate over the time period that begins after one year and continues over the next day,and use it as an approximation to the continuously compounded forward rate.Then the value that you obtain is:

A) 0.041667

B) 0.043478

C) 0.042588

D) 0.042553

E) None of these answers are correct.

Suppose that you compute the simple forward rate over the time period that begins after one year and continues over the next day,and use it as an approximation to the continuously compounded forward rate.Then the value that you obtain is:

A) 0.041667

B) 0.043478

C) 0.042588

D) 0.042553

E) None of these answers are correct.

Question

Use the following data for a caplet and floorlet to answer the questions that follow:

What is the floorlet's value?

A) 0.000717

B) 0.005433

C) 0.001690

D) 0.003256

E) 0.306680

What is the floorlet's value?

A) 0.000717

B) 0.005433

C) 0.001690

D) 0.003256

E) 0.306680

Question

Question

Use the following data for a caplet and floorlet to answer the questions that follow:

What is the caplet's value?

A) 0.000717

B) 0.005433

C) 0.001690

D) 0.003256

E) 0.306680

What is the caplet's value?

A) 0.000717

B) 0.005433

C) 0.001690

D) 0.003256

E) 0.306680

Question

Use the following data for a caplet and floorlet to answer the questions that follow:

What is the caplet's value?

A) 0.148434

B) 0.224304

C) 0.005835

D) 0.008877

E) 0.001248

What is the caplet's value?

A) 0.148434

B) 0.224304

C) 0.005835

D) 0.008877

E) 0.001248

Question

Question

Question

Which formula is correct for a simple forward interest rate over [T,T + ]?

A)![<strong>Which formula is correct for a simple forward interest rate over [T,T + \delta ]?</strong> A) B) C) D) E) None of these answers are correct. <div style=padding-top: 35px>](https://storage.examlex.com/TB4275/11eaa4a8_bafd_885f_9180_1105d04e7b50_TB4275_11.jpg)

B)![<strong>Which formula is correct for a simple forward interest rate over [T,T + \delta ]?</strong> A) B) C) D) E) None of these answers are correct. <div style=padding-top: 35px>](https://storage.examlex.com/TB4275/11eaa4a8_bafd_8860_9180_dbaf5ab39a13_TB4275_11.jpg)

C)![<strong>Which formula is correct for a simple forward interest rate over [T,T + \delta ]?</strong> A) B) C) D) E) None of these answers are correct. <div style=padding-top: 35px>](https://storage.examlex.com/TB4275/11eaa4a8_bafd_8861_9180_f30f9ae31803_TB4275_11.jpg)

D)![<strong>Which formula is correct for a simple forward interest rate over [T,T + \delta ]?</strong> A) B) C) D) E) None of these answers are correct. <div style=padding-top: 35px>](https://storage.examlex.com/TB4275/11eaa4a8_bafd_af72_9180_872d49ce65f5_TB4275_11.jpg)

E) None of these answers are correct.

A)

B)

C)

D)

E) None of these answers are correct.

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/23

Play

Full screen (f)

Deck 25: The Heath Jarrow Morton Libor Model

1

A company buys a caplet today (time 0)with maturity T = 1 year and a strike rate of k = 3 percent on a notional of LN = $200 million.Suppose the six-month bbalibor rate realized after one year is 4.5 percent.Assume that there are 181 days in this six-month period and the year has 365 days.

-Suppose that after one year,the price of a zero-coupon bond that matures after six months is worth $0.9780.The caplet's payoff after one year is:

A) $1,454,942

B) $1,470,000

C) $1,487,671

D) $1,500,000

E) None of these answers are correct.

-Suppose that after one year,the price of a zero-coupon bond that matures after six months is worth $0.9780.The caplet's payoff after one year is:

A) $1,454,942

B) $1,470,000

C) $1,487,671

D) $1,500,000

E) None of these answers are correct.

$1,454,942

2

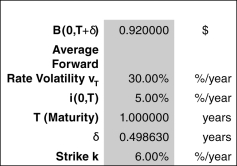

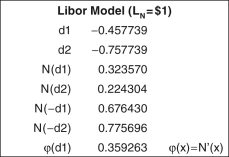

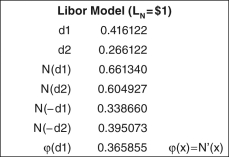

Use the following data for a caplet and floorlet to answer the questions that follow:

What is the floorlet's value?

A) 0.148434

B) 0.224304

C) 0.005835

D) 0.008877

E) 0.001248

What is the floorlet's value?

A) 0.148434

B) 0.224304

C) 0.005835

D) 0.008877

E) 0.001248

C

3

Once an interest rate caplet is priced using the HJM libor model,you CANNOT price which of the following derivatives using a closed-form solution?

A) an interest rate cap,which is a series of caplets

B) an Asian interest rate cap,by computing a series of caplets maturing on consecutive days and then taking their average

C) an interest rate floorlet,by caplet-floorlet parity

D) an interest rate floor,which is a series of floorlets

E) an interest rate collar,by pricing a cap and a floor

A) an interest rate cap,which is a series of caplets

B) an Asian interest rate cap,by computing a series of caplets maturing on consecutive days and then taking their average

C) an interest rate floorlet,by caplet-floorlet parity

D) an interest rate floor,which is a series of floorlets

E) an interest rate collar,by pricing a cap and a floor

B

4

A company buys a caplet today (time 0)with maturity T = 1 year and a strike rate of k = 3 percent on a notional of LN = $200 million.Suppose the six-month bbalibor rate realized after one year is 4.5 percent.Assume that there are 181 days in this six-month period and the year has 365 days.

-Which of the following statements is NOT true with respect to the HJM libor model?

A) The caplet's price can be computed using risk-neutral valuation.

B) The simple forward rate is a martingale using the pseudo-probabilities.

C) The model assumes investors are risk-neutral.

D) The pseudo-probabilities are the actual probabilities adjusted for an interest rate risk premium.

E) The HJM libor caplet formula is similar in appearance to the Black-Scholes-Merton model call formula.

-Which of the following statements is NOT true with respect to the HJM libor model?

A) The caplet's price can be computed using risk-neutral valuation.

B) The simple forward rate is a martingale using the pseudo-probabilities.

C) The model assumes investors are risk-neutral.

D) The pseudo-probabilities are the actual probabilities adjusted for an interest rate risk premium.

E) The HJM libor caplet formula is similar in appearance to the Black-Scholes-Merton model call formula.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

5

Why was Black's model not useful for pricing caplets?

A) It was a model for equity options,not futures.

B) It assumed that the spot rate of interest rates is constant.

C) It only applied to floorlets,not caplets.

D) Caplets are American options,and Black's model is for valuing European options.

E) Both (b)and (d).

A) It was a model for equity options,not futures.

B) It assumed that the spot rate of interest rates is constant.

C) It only applied to floorlets,not caplets.

D) Caplets are American options,and Black's model is for valuing European options.

E) Both (b)and (d).

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

6

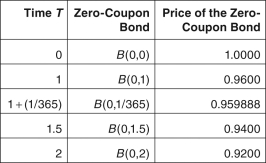

Zero-coupon bond prices are given by B(0,T ),where 0 is today,and T (measured in years)is the bond's maturity date.

Considering the time interval from 1 year to 1.5 years,the simple forward rate is given by:

A) 0.041667

B) 0.043478

C) 0.042588

D) 0.042553

E) None of these answers are correct.

Considering the time interval from 1 year to 1.5 years,the simple forward rate is given by:

A) 0.041667

B) 0.043478

C) 0.042588

D) 0.042553

E) None of these answers are correct.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

7

Zero-coupon bond prices are given by B(0,T ),where 0 is today,and T (measured in years)is the bond's maturity date.

The spot rate f (0,0)and the forward rate f (0,1)are given by:

A) 0.041667 and 0.042588

B) 0.041667 and 0.043478

C) 0.041667 and 0.042553

D) 0.043478 and 0.045455

E) None of these answers are correct.

The spot rate f (0,0)and the forward rate f (0,1)are given by:

A) 0.041667 and 0.042588

B) 0.041667 and 0.043478

C) 0.041667 and 0.042553

D) 0.043478 and 0.045455

E) None of these answers are correct.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

8

A company buys a caplet today (time 0)with maturity T = 1 year and a strike rate of k = 3 percent on a notional of LN = $200 million.Suppose the six-month bbalibor rate realized after one year is 4.5 percent.Assume that there are 181 days in this six-month period and the year has 365 days.

-Which of the following inputs into the HJM libor model caplets formula are NOT easily observable?

A) zero-coupon bond prices

B) simple forward interest rates

C) cap rate

D) maturity

E) the average forward rate volatility

-Which of the following inputs into the HJM libor model caplets formula are NOT easily observable?

A) zero-coupon bond prices

B) simple forward interest rates

C) cap rate

D) maturity

E) the average forward rate volatility

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

9

Which statement in connection with the alleged manipulation of bbalibor by several London-based international banks in 2008 is INCORRECT?

A) In early 2008,bbalibor was higher than what it should have been because of irrational reactions to the credit crisis.

B) Toward the end of 2007 and in early 2008,many market observers complained that bbalibor was lower than what it should have been,and that it did not reflect the true cost of bank funds.

C) Bbalibor's originator,the British Bankers' Association,initially denied any bias in bbalibor values,but eventually agreed to conduct a review of the matter.

D) The alleged mispricing was reduced after it became known that British Bankers' Association was conducting a review of the bbalibor.

E) The alleged mispricing of bbalibor has attracted regulatory probes and lawsuits.

A) In early 2008,bbalibor was higher than what it should have been because of irrational reactions to the credit crisis.

B) Toward the end of 2007 and in early 2008,many market observers complained that bbalibor was lower than what it should have been,and that it did not reflect the true cost of bank funds.

C) Bbalibor's originator,the British Bankers' Association,initially denied any bias in bbalibor values,but eventually agreed to conduct a review of the matter.

D) The alleged mispricing was reduced after it became known that British Bankers' Association was conducting a review of the bbalibor.

E) The alleged mispricing of bbalibor has attracted regulatory probes and lawsuits.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

10

Zero-coupon bond prices are given by B(0,T ),where 0 is today,and T (measured in years)is the bond's maturity date.

Suppose that you compute the simple forward rate over the time period that begins after one year and continues over the next day,and use it as an approximation to the continuously compounded forward rate.Then the value that you obtain is:

A) 0.041667

B) 0.043478

C) 0.042588

D) 0.042553

E) None of these answers are correct.

Suppose that you compute the simple forward rate over the time period that begins after one year and continues over the next day,and use it as an approximation to the continuously compounded forward rate.Then the value that you obtain is:

A) 0.041667

B) 0.043478

C) 0.042588

D) 0.042553

E) None of these answers are correct.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

11

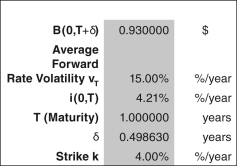

Use the following data for a caplet and floorlet to answer the questions that follow:

What is the floorlet's value?

A) 0.000717

B) 0.005433

C) 0.001690

D) 0.003256

E) 0.306680

What is the floorlet's value?

A) 0.000717

B) 0.005433

C) 0.001690

D) 0.003256

E) 0.306680

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

12

A company buys a caplet today (time 0)with maturity T = 1 year and a strike rate of k = 3 percent on a notional of LN = $200 million.Suppose the six-month bbalibor rate realized after one year is 4.5 percent.Assume that there are 181 days in this six-month period and the year has 365 days.

-The caplet's payoff after 1.5 years:

A) $971,945

B) $991,781

C) $1,457,918

D) $1,487,671

E) None of these answers are correct.

-The caplet's payoff after 1.5 years:

A) $971,945

B) $991,781

C) $1,457,918

D) $1,487,671

E) None of these answers are correct.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

13

Use the following data for a caplet and floorlet to answer the questions that follow:

What is the caplet's value?

A) 0.000717

B) 0.005433

C) 0.001690

D) 0.003256

E) 0.306680

What is the caplet's value?

A) 0.000717

B) 0.005433

C) 0.001690

D) 0.003256

E) 0.306680

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

14

Use the following data for a caplet and floorlet to answer the questions that follow:

What is the caplet's value?

A) 0.148434

B) 0.224304

C) 0.005835

D) 0.008877

E) 0.001248

What is the caplet's value?

A) 0.148434

B) 0.224304

C) 0.005835

D) 0.008877

E) 0.001248

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

15

Suppose that you have computed the historical average forward rate variance with weekly data.To convert this to an annual variance,use the following adjustment:

A) Variance (Annual)= Variance (Weekly)* 12

B) Variance (Annual)= Variance (Weekly)* 52

C) Variance (Annual)= Variance (Weekly)* 250

D) Variance (Annual)=Variance (Weekly)*260

E) None of these answers are correct.

A) Variance (Annual)= Variance (Weekly)* 12

B) Variance (Annual)= Variance (Weekly)* 52

C) Variance (Annual)= Variance (Weekly)* 250

D) Variance (Annual)=Variance (Weekly)*260

E) None of these answers are correct.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

16

The HJM libor model does NOT assume which of the following?

A) no market frictions

B) no credit risk

C) competitive and well-functioning markets

D) no arbitrage opportunities

E) no interest rate risk

A) no market frictions

B) no credit risk

C) competitive and well-functioning markets

D) no arbitrage opportunities

E) no interest rate risk

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

17

Which formula is correct for a simple forward interest rate over [T,T + ]?

A)

B)

C)

D)

E) None of these answers are correct.

A)

B)

C)

D)

E) None of these answers are correct.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

18

The alleged manipulation of bbalibor by several London-based international banks in 2008 led to the violation of which of the following assumptions underlying the HJM libor model?

A) no market frictions

B) no credit risk

C) competitive and well-functioning markets

D) no intermediate cash flows

E) no arbitrage opportunities

A) no market frictions

B) no credit risk

C) competitive and well-functioning markets

D) no intermediate cash flows

E) no arbitrage opportunities

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

19

The HJM libor model assumes which of the following?

A) continuously compounded forward rates are lognormally distributed

B) zero-coupon bond prices are normally distributed

C) simple forward rates are normally distributed

D) simple forward rates are lognormally distributed

E) continuously compounded forward rates are normally distributed

A) continuously compounded forward rates are lognormally distributed

B) zero-coupon bond prices are normally distributed

C) simple forward rates are normally distributed

D) simple forward rates are lognormally distributed

E) continuously compounded forward rates are normally distributed

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

20

A company buys a caplet today (time 0)with maturity T = 1 year and a strike rate of k = 3 percent on a notional of LN = $200 million.Suppose the six-month bbalibor rate realized after one year is 4.5 percent.Assume that there are 181 days in this six-month period and the year has 365 days.

-Which of the following statements is NOT true with respect to the average forward rate volatility?

A) It can be estimated using historical data on forward rates.

B) It can be estimated implicitly using caplet prices.

C) If the HJM libor model is rejected using historical data,it can be estimated using calibration.

D) If the HJM libor model is accepted using historical data,it can be estimated using calibration.

E) If the HJM libor model is rejected,it can be estimated using historical data.

-Which of the following statements is NOT true with respect to the average forward rate volatility?

A) It can be estimated using historical data on forward rates.

B) It can be estimated implicitly using caplet prices.

C) If the HJM libor model is rejected using historical data,it can be estimated using calibration.

D) If the HJM libor model is accepted using historical data,it can be estimated using calibration.

E) If the HJM libor model is rejected,it can be estimated using historical data.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

21

Which of the following statements is INCORRECT?

A) A caplet's delta measures how a small change in the underlying simple forward rate changes the caplet's value.

B) A portfolio of caplets can be delta- and gamma-hedged.

C) The hedging approach in the case of the HJM libor model is analogous to that of the Black-Scholes-Merton model.

D) As the HJM libor model specifies an evolution for simple forward rates,rho hedging becomes an effective tool for managing interest rate risk in a portfolio consisting of caplets.

E) A delta-hedge involves trading another interest rate-sensitive security in order to remove all the interest rate risk from a long caplet position.

A) A caplet's delta measures how a small change in the underlying simple forward rate changes the caplet's value.

B) A portfolio of caplets can be delta- and gamma-hedged.

C) The hedging approach in the case of the HJM libor model is analogous to that of the Black-Scholes-Merton model.

D) As the HJM libor model specifies an evolution for simple forward rates,rho hedging becomes an effective tool for managing interest rate risk in a portfolio consisting of caplets.

E) A delta-hedge involves trading another interest rate-sensitive security in order to remove all the interest rate risk from a long caplet position.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

22

Which of the following statements is NOT true of the HJM libor model?

A) Continuous compounded forward rates have a lognormal distribution.

B) There are no closed-form solutions for floorlets.

C) There are no closed-form solutions for American floorlets.

D) There are no closed-form solutions for swaptions.

E) Floorlets can be priced using caplet prices and caplet-floorlet parity.

A) Continuous compounded forward rates have a lognormal distribution.

B) There are no closed-form solutions for floorlets.

C) There are no closed-form solutions for American floorlets.

D) There are no closed-form solutions for swaptions.

E) Floorlets can be priced using caplet prices and caplet-floorlet parity.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

23

Identify the INCORRECT statement.The HJM libor model's closed-form solution:

A) cannot be used for pricing American options

B) cannot be used for pricing Asian options

C) cannot be used for pricing interest rate futures

D) cannot be used for pricing swaptions

E) cannot be used for pricing an interest rate collar

A) cannot be used for pricing American options

B) cannot be used for pricing Asian options

C) cannot be used for pricing interest rate futures

D) cannot be used for pricing swaptions

E) cannot be used for pricing an interest rate collar

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 23 flashcards in this deck.