Deck 10: Auditing Purchases, Payables and Payroll

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

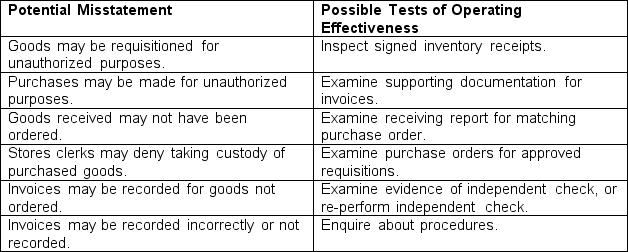

With regards to control risk assessment for purchase transactions, align the potential misstatements in the following chart with their possible tests of operating effectiveness.

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/69

Play

Full screen (f)

Deck 10: Auditing Purchases, Payables and Payroll

1

The segregation of receiving goods from the requisitioning and purchasing of those

goods prevents those making requisitions from ordering goods directly from suppliers and

also prevents the purchasing department from gaining access to goods improperly ordered.

goods prevents those making requisitions from ordering goods directly from suppliers and

also prevents the purchasing department from gaining access to goods improperly ordered.

True

2

The auditor knows that overstatements of payroll may result from unintentional errors or

fraud through payments to fictitious employees, payments to actual employees for hours not

worked, and payments to actual employees at higher than authorized rates.

fraud through payments to fictitious employees, payments to actual employees for hours not

worked, and payments to actual employees at higher than authorized rates.

True

3

On delivery of the goods to stores or other requisitioning departments, receiving clerks should obtain

A) a signed receipt on the copy of the receiving report retained by the receiving department.

B) an original copy of the receiving report released by the receiving department.

C) a copy of the receiving report retained by the receiving department.

D) an authority for receiving report retained by the receiving department.

A) a signed receipt on the copy of the receiving report retained by the receiving department.

B) an original copy of the receiving report released by the receiving department.

C) a copy of the receiving report retained by the receiving department.

D) an authority for receiving report retained by the receiving department.

A

4

Employees are generally hired by the company's purchasing department.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

5

The correct statement in relation to purchase requisitions is:

A) all purchase requisitions in the organization should originate from the warehouse.

B) all managers in the organization should be able to sign a requisition order.

C) the purchase requisition represents the start of the trail of documentary evidence in support of management's assertion as to the occurrence of the purchase transaction.

D) all of the above

A) all purchase requisitions in the organization should originate from the warehouse.

B) all managers in the organization should be able to sign a requisition order.

C) the purchase requisition represents the start of the trail of documentary evidence in support of management's assertion as to the occurrence of the purchase transaction.

D) all of the above

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

6

Purchases transactions relate

A) solely to the purchase of inventory held for sale.

B) to the purchase of inventory, plant & equipment and supplies.

C) to the purchase of all goods and services.

D) to the purchase of all goods and services and the payroll function.

A) solely to the purchase of inventory held for sale.

B) to the purchase of inventory, plant & equipment and supplies.

C) to the purchase of all goods and services.

D) to the purchase of all goods and services and the payroll function.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

7

A substantive audit procedure for verifying accounts payable should include tracing the

opening balance to the previous year's working papers.

opening balance to the previous year's working papers.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

8

Even though an employee's supervisor may initiate a request for payroll change, such as

a change in job classification or wage rate increase, all changes should be authorized in

writing by the personnel department before being entered into the personnel data master

file.

a change in job classification or wage rate increase, all changes should be authorized in

writing by the personnel department before being entered into the personnel data master

file.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

9

The occurrence objective for purchases, payables and payroll requires that accounts

payable and payroll liabilities include all amounts owed by the entity to suppliers of goods

and services at the end of the reporting period.

payable and payroll liabilities include all amounts owed by the entity to suppliers of goods

and services at the end of the reporting period.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

10

Purchase requisitions may originate from

A) personnel manager, for plant and equipment.

B) the warehouse, for inventory.

C) purchases for a delivery vehicle.

D) both b and c

A) personnel manager, for plant and equipment.

B) the warehouse, for inventory.

C) purchases for a delivery vehicle.

D) both b and c

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

11

The specific audit objective "accounts payable are liabilities of the entity at the balance date" is derived from the:

A) completeness assertion.

B) valuation assertion.

C) presentation assertion.

D) rights and obligations assertion.

A) completeness assertion.

B) valuation assertion.

C) presentation assertion.

D) rights and obligations assertion.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

12

In the audit of payroll, one of the key issues is to ensure that the payroll expense has

been properly recorded and the associated deductions for income tax, employee benefits,

and related liabilities are properly recorded as liabilities.

been properly recorded and the associated deductions for income tax, employee benefits,

and related liabilities are properly recorded as liabilities.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

13

Accounts payable is affected by purchase transactions that increase the account

balance and payment transactions that decrease the balance, thus, detection risk for

payables assertions is affected by the control and inherent risk factors related to both these

transaction classes.

balance and payment transactions that decrease the balance, thus, detection risk for

payables assertions is affected by the control and inherent risk factors related to both these

transaction classes.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

14

Accounts payable is usually the smallest current liability on the balance sheet and a

insignificant factor in the evaluation of an entity's short-term solvency, especially when the

accounts payable is affected by a high volume of transactions and thus is susceptible to

misstatements.

insignificant factor in the evaluation of an entity's short-term solvency, especially when the

accounts payable is affected by a high volume of transactions and thus is susceptible to

misstatements.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

15

Purchase and payroll transactions account for the major expenses incurred by a

business, and so are a major component in the determination of profit, and also relate to the

acquisition of major classes of asset including inventories and capital assets.

business, and so are a major component in the determination of profit, and also relate to the

acquisition of major classes of asset including inventories and capital assets.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

16

A purchase order is a form issued by the supplier detailing the goods or services supplied

and the amount owing.

and the amount owing.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

17

A proper cut-off of payment transactions at the year end, such as verifying and

examining the date of cheques outstanding as at the end of the reporting period, is essential

to the correct presentation of cash and accounts payable at the end of the reporting period.

examining the date of cheques outstanding as at the end of the reporting period, is essential

to the correct presentation of cash and accounts payable at the end of the reporting period.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

18

Which of these is not directly affected by purchases and payments transactions?

A) plant assets

B) work-in-process inventory

C) accounts payable

D) prepaid expenses

A) plant assets

B) work-in-process inventory

C) accounts payable

D) prepaid expenses

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following is least likely to be a function of the processing of purchase transactions?

A) storing goods received for inventory

B) checking and approving the supplier's invoice

C) return to customers

D) receiving the goods

A) storing goods received for inventory

B) checking and approving the supplier's invoice

C) return to customers

D) receiving the goods

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

20

The control related to the completeness assertion is

A) determining the mathematical accuracy of the suppliers' invoices.

B) serially numbering suppliers' invoices on receipt so that subsequent checks of numerical continuity can confirm that all invoices are recorded.

C) preparing a daily prelist of suppliers' invoices approved for payment.

D) coding the account distributions on the suppliers' invoices.

A) determining the mathematical accuracy of the suppliers' invoices.

B) serially numbering suppliers' invoices on receipt so that subsequent checks of numerical continuity can confirm that all invoices are recorded.

C) preparing a daily prelist of suppliers' invoices approved for payment.

D) coding the account distributions on the suppliers' invoices.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

21

A check by the auditor on the numeric sequence of prenumbered receiving reports to determine that a supplier's invoice was recorded for each relates to the

A) existence or occurrence assertion.

B) completeness assertion.

C) presentation assertion.

D) rights and obligations assertion.

A) existence or occurrence assertion.

B) completeness assertion.

C) presentation assertion.

D) rights and obligations assertion.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

22

Prior to recording purchases transactions, supplier's invoices are checked and approved in the accounts department. Controls over this function include all of the following except

A) marking all supporting documentation as "paid".

B) approving the supplier's invoice for payment by having an authorized person sign the invoice.

C) agreeing the details of the supplier's invoice with the related receiving report and purchase order.

D) determining the mathematical accuracy of the supplier's invoice.

A) marking all supporting documentation as "paid".

B) approving the supplier's invoice for payment by having an authorized person sign the invoice.

C) agreeing the details of the supplier's invoice with the related receiving report and purchase order.

D) determining the mathematical accuracy of the supplier's invoice.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

23

The quantity ordered may not be displayed on the copy of the purchase order sent directly to the

A) requesting department.

B) vouchers payable department.

C) receiving department.

D) accounts receivable department.

A) requesting department.

B) vouchers payable department.

C) receiving department.

D) accounts receivable department.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

24

Payroll functions include all of the following except

A) hiring employees.

B) deciding on the number of workers required to work on a particular day.

C) preparing the payroll.

D) protecting unclaimed wages.

A) hiring employees.

B) deciding on the number of workers required to work on a particular day.

C) preparing the payroll.

D) protecting unclaimed wages.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

25

A programmed routine in the edit run for payroll lists all employees who worked more than 50 hours during the week for review. This is an example of a

A) reasonableness test.

B) validity test.

C) sequence test.

D) self-checking test.

A) reasonableness test.

B) validity test.

C) sequence test.

D) self-checking test.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

26

Responsibility for determining that unpaid supplier's invoices are processed for payment on their due dates generally lies with the

A) warehouse department.

B) accounts payable department.

C) purchasing department.

D) internal audit department.

A) warehouse department.

B) accounts payable department.

C) purchasing department.

D) internal audit department.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

27

The receiving department should be instructed to accept no goods without having on file a properly authorized

A) purchase requisition.

B) invoice.

C) receiving report.

D) purchase order.

A) purchase requisition.

B) invoice.

C) receiving report.

D) purchase order.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

28

Responsibility for updating of the personnel data master file should rest with authorized employees in the

A) personnel department.

B) payroll department.

C) controller's department.

D) employee's operating department.

A) personnel department.

B) payroll department.

C) controller's department.

D) employee's operating department.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

29

Purchase orders become part of the transaction trail of documentary evidence that directly supports which assertion for purchase transactions?

A) existence or occurrence

B) rights and obligations

C) accuracy and valuation

D) presentation

A) existence or occurrence

B) rights and obligations

C) accuracy and valuation

D) presentation

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

30

A responsibility not normally assigned to receiving department personnel is to

A) compare goods received with description of goods ordered.

B) prepare a prenumbered receiving report for every order received.

C) enter cheque requisition data and verify the batch total.

D) file the purchase order copy pending arrival of goods.

A) compare goods received with description of goods ordered.

B) prepare a prenumbered receiving report for every order received.

C) enter cheque requisition data and verify the batch total.

D) file the purchase order copy pending arrival of goods.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

31

Payroll functions include all of the following except

A) preparing attendance and timekeeping data.

B) authorized payroll changes.

C) terminating employees.

D) All of the above are payroll functions.

A) preparing attendance and timekeeping data.

B) authorized payroll changes.

C) terminating employees.

D) All of the above are payroll functions.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

32

Controls specific to the recording of cash payments include which of the following?

A) an independent check by the accounting supervisor of the agreement of the amounts authorized and posted to accounts payable with the cheque summary received from the general accounts department

B) an independent check of the agreement of the total of cheques issued with a batch total of the vouchers processed for payment.

C) limits on access to blank cheques

D) all of the above

A) an independent check by the accounting supervisor of the agreement of the amounts authorized and posted to accounts payable with the cheque summary received from the general accounts department

B) an independent check of the agreement of the total of cheques issued with a batch total of the vouchers processed for payment.

C) limits on access to blank cheques

D) all of the above

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

33

A special supervisor's password is required in order to add a new employee to the personnel data master file. This control relates primarily to the

A) existence or occurrence assertion.

B) completeness assertion.

C) presentation assertion.

D) accuracy and valuation assertion.

A) existence or occurrence assertion.

B) completeness assertion.

C) presentation assertion.

D) accuracy and valuation assertion.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

34

Segregation of the functions of payroll and personnel do all of the following, except

A) reduce the risk of payments to fictitious employees.

B) reduce the risk of payments to terminated employees.

C) restrict the recording of new employee data to the payroll department.

D) restrict the payment of wages to the payroll department.

A) reduce the risk of payments to fictitious employees.

B) reduce the risk of payments to terminated employees.

C) restrict the recording of new employee data to the payroll department.

D) restrict the payment of wages to the payroll department.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

35

In most modern organizations, employee timekeeping data is recorded via

A) employee badges.

B) time-clock cards.

C) security identification cards.

D) sign-in/sign-off book.

A) employee badges.

B) time-clock cards.

C) security identification cards.

D) sign-in/sign-off book.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

36

For proper control, unclaimed payroll cheques should be stored by the

A) finance department.

B) payroll department.

C) personnel department.

D) timekeeping department.

A) finance department.

B) payroll department.

C) personnel department.

D) timekeeping department.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

37

Controls over the preparation and signing of cheques include all of the following except

A) authorized personnel in the accounting department should be responsible for signing the cheques.

B) the cheque requisition and supporting documents should be cancelled (stamped) when the cheque is signed.

C) the signed cheque and the supporting documents should be returned to the accounts payable clerk for review and mailing.

D) prenumbered cheques should be used.

A) authorized personnel in the accounting department should be responsible for signing the cheques.

B) the cheque requisition and supporting documents should be cancelled (stamped) when the cheque is signed.

C) the signed cheque and the supporting documents should be returned to the accounts payable clerk for review and mailing.

D) prenumbered cheques should be used.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

38

Wage rate increases should be authorized in writing by the

A) payroll department.

B) personnel department.

C) finance department.

D) data entry department.

A) payroll department.

B) personnel department.

C) finance department.

D) data entry department.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

39

A copy of the receiving report should be sent directly by the receiving department to the

A) accounts (receivable) department.

B) chief financial controller.

C) purchasing department.

D) accounts (payable) department.

A) accounts (receivable) department.

B) chief financial controller.

C) purchasing department.

D) accounts (payable) department.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

40

For the purchasing firm the processing of purchases and payment transactions requires all of the following functions except:

A) requisitioning goods and services.

B) preparing purchase invoices.

C) preparing the cheque requisition.

D) All of the above functions are required.

A) requisitioning goods and services.

B) preparing purchase invoices.

C) preparing the cheque requisition.

D) All of the above functions are required.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

41

The batching of payroll documents is normally done in the

A) timekeeping department.

B) payroll department.

C) data entry department.

D) personnel department.

A) timekeeping department.

B) payroll department.

C) data entry department.

D) personnel department.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

42

In witnessing a payroll distribution, the auditor would not be expected to observe that

A) the segregation of duties exist between the preparation and payment of payroll.

B) the correct payroll entries are made in the firm's ledger and journal

C) there is proper control and disposal of unclaimed cheques.

D) each employee receives only one cheque or pay envelope.

A) the segregation of duties exist between the preparation and payment of payroll.

B) the correct payroll entries are made in the firm's ledger and journal

C) there is proper control and disposal of unclaimed cheques.

D) each employee receives only one cheque or pay envelope.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

43

Which of these tests would be the least useful when using analytical procedures on expenses?

A) comparing prior year amounts with current year amounts

B) comparing current year amounts as a percentage of sales with prior year

C) comparing relationships between related expenses

D) comparing total expenses to the bank balance at balance date

A) comparing prior year amounts with current year amounts

B) comparing current year amounts as a percentage of sales with prior year

C) comparing relationships between related expenses

D) comparing total expenses to the bank balance at balance date

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

44

Test data may be used to test application controls over accepting and recording data for unpaid suppliers' invoices. Which of the following conditions would not be relevant?

A) numeric characters in an alphanumeric field

B) missing or invalid supplier numbers

C) missing due date or payment terms

D) alphabetical characters in a numeric field

A) numeric characters in an alphanumeric field

B) missing or invalid supplier numbers

C) missing due date or payment terms

D) alphabetical characters in a numeric field

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

45

Confirmation of accounts payable will provide the least amount of evidence for the

A) existence or occurrence assertion.

B) completeness assertion.

C) accuracy and valuation assertion.

D) rights and obligations assertion.

A) existence or occurrence assertion.

B) completeness assertion.

C) accuracy and valuation assertion.

D) rights and obligations assertion.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

46

Which of these is the least likely risk factor for payroll?

A) payments to fictitious employees

B) payments to actual employees for hours less than they worked

C) payment to actual employees for hours not worked

D) payments to actual employees at higher than authorized rates

A) payments to fictitious employees

B) payments to actual employees for hours less than they worked

C) payment to actual employees for hours not worked

D) payments to actual employees at higher than authorized rates

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

47

The third stage of applying analytical procedures is to

A) identify absolute changes in amounts between the current year and the prior year.

B) use ratios and trends.

C) make an objective assessment regarding usability of analytical procedures.

D) document expected and unexpected changes.

A) identify absolute changes in amounts between the current year and the prior year.

B) use ratios and trends.

C) make an objective assessment regarding usability of analytical procedures.

D) document expected and unexpected changes.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

48

Identify and describe three key issues relevant to the audit of purchases, payables and payroll.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

49

Tests of details of transactions for payables balances include

A) vouching recorded payables to supporting documentation.

B) confirming payables with major suppliers by reviewing the accounts payable ledger or accounts payable master file.

C) comparing financial statement presentation with applicable regulations and accounting standards.

D) verifying directors' and executive officers' remuneration.

A) vouching recorded payables to supporting documentation.

B) confirming payables with major suppliers by reviewing the accounts payable ledger or accounts payable master file.

C) comparing financial statement presentation with applicable regulations and accounting standards.

D) verifying directors' and executive officers' remuneration.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

50

Tests of details of balances for payables include all of the following except

A) reconciling payables with monthly statements received by the entity from suppliers.

B) confirming accounts payable.

C) searching for unrecorded liabilities.

D) verifying directors' and executive officers' remuneration.

A) reconciling payables with monthly statements received by the entity from suppliers.

B) confirming accounts payable.

C) searching for unrecorded liabilities.

D) verifying directors' and executive officers' remuneration.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

51

A purchases cut-off test would satisfy the audit objective assertion of

A) classification.

B) rights and obligations.

C) completeness

D) none of the above

A) classification.

B) rights and obligations.

C) completeness

D) none of the above

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

52

Which of these is not a source of potential misstatement for the function of recording a payment?

A) a cheque may be issued for unauthorised purchases

B) a cheque may not be recorded promptly

C) errors may be made in recording cheques

D) All of the above are sources of potential misstatement for the function of recording a payment.

A) a cheque may be issued for unauthorised purchases

B) a cheque may not be recorded promptly

C) errors may be made in recording cheques

D) All of the above are sources of potential misstatement for the function of recording a payment.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

53

Which of the following is not a factor that tends to increase the inherent risk for purchases and payables?

A) the number of directors

B) a high volume of transactions

C) issues over costs being capitalized versus being expensed

D) All of the above are factors that tend to increase the inherent risk for purchases and payables.

A) the number of directors

B) a high volume of transactions

C) issues over costs being capitalized versus being expensed

D) All of the above are factors that tend to increase the inherent risk for purchases and payables.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

54

An important consideration in assessing inherent risk for purchase transactions is any motivation management may have to misstate expenditure. Which of the following is not a factor that may contribute to misstatement?

A) the need to achieve announced profitability targets.

B) the need to disclose concern over control problems.

C) temptations for employees to make unauthorized purchases.

D) temptations for employees to misappropriate purchased assets.

A) the need to achieve announced profitability targets.

B) the need to disclose concern over control problems.

C) temptations for employees to make unauthorized purchases.

D) temptations for employees to misappropriate purchased assets.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

55

A confirmation is performed less frequently for accounts payable than it is for accounts receivable because

A) only a negative confirmation can be sent.

B) confirmation offers no assurance that unrecorded liabilities will be discovered.

C) it is only performed when detection risk is high.

D) it specifies the amount due to the supplier.

A) only a negative confirmation can be sent.

B) confirmation offers no assurance that unrecorded liabilities will be discovered.

C) it is only performed when detection risk is high.

D) it specifies the amount due to the supplier.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

56

Factors relating to the internal control environment that the auditor needs to consider when assessing control risk for purchase, payment and payroll transactions include all of these except

A) integrity and ethical values.

B) management's commitment to competence.

C) design of substantive procedures.

D) assignment of authority and responsibility.

A) integrity and ethical values.

B) management's commitment to competence.

C) design of substantive procedures.

D) assignment of authority and responsibility.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

57

Controls applicable to paying the payroll and protecting unclaimed wages include all of the following except

A) payroll cheques and bank transfers should be signed or authorized by finance office personnel involved in preparing or recording the payroll.

B) payroll cheques, where used should be distributed to employees by finance office personnel not involved in preparing or recording the payroll.

C) any unclaimed payroll cheques should be stored in a safe or vault in the finance office.

D) finance office personnel should check the agreement of the names and amounts on cheques or bank transfers with payroll register entries.

A) payroll cheques and bank transfers should be signed or authorized by finance office personnel involved in preparing or recording the payroll.

B) payroll cheques, where used should be distributed to employees by finance office personnel not involved in preparing or recording the payroll.

C) any unclaimed payroll cheques should be stored in a safe or vault in the finance office.

D) finance office personnel should check the agreement of the names and amounts on cheques or bank transfers with payroll register entries.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

58

Which of these is not a procedure for identifying unrecorded liabilities?

A) examination of the subsequent period's purchase and payment transactions

B) analytical procedures for expense and liability balances

C) examination of contractual commitments

D) confirmation of accounts payable

A) examination of the subsequent period's purchase and payment transactions

B) analytical procedures for expense and liability balances

C) examination of contractual commitments

D) confirmation of accounts payable

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

59

Each major class of creditors and borrowings must be disclosed in the balance sheet. Which of these would not be shown as a class of creditors and borrowings?

A) taxation liabilities

B) revenue owing

C) employee benefits

D) lease liabilities

A) taxation liabilities

B) revenue owing

C) employee benefits

D) lease liabilities

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

60

Which of the following is not an initial procedure for verifying accounts payable?

A) trace the opening balance to the prior year's working papers (if applicable)

B) review activity in the general ledger account for any unusual entries

C) reconcile accounts to monthly supplier's statements

D) obtain a listing of amounts owed at the balance sheet date

A) trace the opening balance to the prior year's working papers (if applicable)

B) review activity in the general ledger account for any unusual entries

C) reconcile accounts to monthly supplier's statements

D) obtain a listing of amounts owed at the balance sheet date

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

61

Following is a description of Out of Control corporations' inventory purchases process for skateboard wheels. Identify the weaknesses in the controls and suggest possible improvements.

When stock falls below 100 the computer automatically produces a purchase requisition for more stock from the supplier. If there is a special promotion coming up, Anthony, the marketing manager, might put in an extra purchase requisition for promotional stock. The computer numbers the dockets in sequence and sends them to the purchasing department.

The purchasing department issues a purchase order with their standard supplier when they receive an authorised purchase requisition. Anthony used to work in purchasing, and is good friends with Chris who now manages the purchasing department. Anthony sometimes covers a shift for Chris when he has a day off.

When the order arrives at the warehouse receiving dock, the purchase order is compared to the goods received: The personnel check that the right types of wheels are included, the right number of wheels is included, and that they are undamaged. They then prepare a prenumbered receiving report and forward it to accounting along with the suppliers invoice.

Accounting then enters the amounts from the supplier invoices into the system.

When stock falls below 100 the computer automatically produces a purchase requisition for more stock from the supplier. If there is a special promotion coming up, Anthony, the marketing manager, might put in an extra purchase requisition for promotional stock. The computer numbers the dockets in sequence and sends them to the purchasing department.

The purchasing department issues a purchase order with their standard supplier when they receive an authorised purchase requisition. Anthony used to work in purchasing, and is good friends with Chris who now manages the purchasing department. Anthony sometimes covers a shift for Chris when he has a day off.

When the order arrives at the warehouse receiving dock, the purchase order is compared to the goods received: The personnel check that the right types of wheels are included, the right number of wheels is included, and that they are undamaged. They then prepare a prenumbered receiving report and forward it to accounting along with the suppliers invoice.

Accounting then enters the amounts from the supplier invoices into the system.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

62

Identify the need for controls over hiring employees, authorising payroll changes and preparing attendance and timekeeping data.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

63

Why are directors' and executive officers' remuneration considered to be audit sensitive?

What procedure could be used to check directors' and executive officers' remuneration?

What procedure could be used to check directors' and executive officers' remuneration?

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

64

Describe the audit process for purchase transactions. Indicate the audit risks that need to be addressed and the mitigating controls that can be implemented.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

65

With regards to control risk assessment for purchase transactions, align the potential misstatements in the following chart with their possible tests of operating effectiveness.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

66

Describe the audit process for payroll transactions. Indicate the audit risks that need to be addressed and the mitigating controls that can be implemented.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

67

Identify key controls that ought to be in place for the preparation and signing of cheques.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

68

What could motivate management to misstate expenditures? What other factors may lead to misstatements?

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

69

Explain the nature and use of an imprest payroll account.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 69 flashcards in this deck.