Deck 24: Performance Evaluation for Managers

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

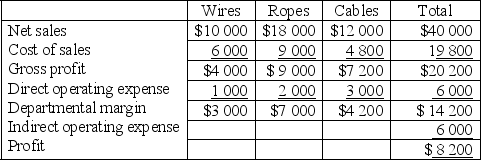

Northern Company has three departments, Wires, Ropes and Cables. At the end of the accounting period the following information is available:

Northern Company is considering eliminating the Wires department. What will be the change in Northern Company's profit if the Wires department is eliminated? Assume that all indirect expenses are unavoidable and that all other circumstances are held constant.

A) $1 000 fall

B) $4 000 fall

C) $3 000 fall

D) $3 000 increase

Northern Company is considering eliminating the Wires department. What will be the change in Northern Company's profit if the Wires department is eliminated? Assume that all indirect expenses are unavoidable and that all other circumstances are held constant.

A) $1 000 fall

B) $4 000 fall

C) $3 000 fall

D) $3 000 increase

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/63

Play

Full screen (f)

Deck 24: Performance Evaluation for Managers

1

A(n) is a responsibility centre that is held accountable for controlling both costs and income.

A) cost object.

B) cost centre.

C) profit centre.

D) investment centre.

A) cost object.

B) cost centre.

C) profit centre.

D) investment centre.

C

2

Which financial report is most commonly prepared for departmental reporting?

A) Statement of changes in equity

B) Balance sheet

C) Cash flow statement

D) Income statement

A) Statement of changes in equity

B) Balance sheet

C) Cash flow statement

D) Income statement

D

3

Match the following costs with their descriptions.

I) Controllable expenses A. Carefully predetermined costs

II) Standard costs B. Costs which are eliminated if a department is closed

III) Avoidable costs C. Expenses that cannot be directly traced to a cost object

IV) Indirect expenses D. Expenses which can be influenced by a manager

A) I:C, II:A, III:D, IV:B

B) I:D, II:A, III:B, IV:C

C) I:D, II:A, III:B, IV:C

D) I:A, II:D, III:B, IV:C

I) Controllable expenses A. Carefully predetermined costs

II) Standard costs B. Costs which are eliminated if a department is closed

III) Avoidable costs C. Expenses that cannot be directly traced to a cost object

IV) Indirect expenses D. Expenses which can be influenced by a manager

A) I:C, II:A, III:D, IV:B

B) I:D, II:A, III:B, IV:C

C) I:D, II:A, III:B, IV:C

D) I:A, II:D, III:B, IV:C

B

4

Which of the following is not included in the calculation of departmental gross profit?

A) Selling price.

B) Cost of sales.

C) Number of units sold.

D) Selling and distribution expenses.

A) Selling price.

B) Cost of sales.

C) Number of units sold.

D) Selling and distribution expenses.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

5

Which of the following statements is not true? A responsibility accounting system:

A) recognises that expenses are the collective responsibility of the organisation.

B) holds managers responsible for costs and income over which they have control.

C) measures separately the performance of each manager's area of responsible.

D) requires managers to participate in the development of financial plans for their unit.

A) recognises that expenses are the collective responsibility of the organisation.

B) holds managers responsible for costs and income over which they have control.

C) measures separately the performance of each manager's area of responsible.

D) requires managers to participate in the development of financial plans for their unit.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

6

A projected cost for the future is called a:

A) fixed cost.

B) period cost.

C) random cost.

D) budgeted cost.

A) fixed cost.

B) period cost.

C) random cost.

D) budgeted cost.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

7

A variance is the difference between:

A) an actual cost and a budgeted cost.

B) a standard cost and a budgeted cost.

C) actual costs at two different points of time.

D) budgeted costs at two different points of time.

A) an actual cost and a budgeted cost.

B) a standard cost and a budgeted cost.

C) actual costs at two different points of time.

D) budgeted costs at two different points of time.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

8

Bob's Warehouse allocates advertising expenses to its two departments, A and B, on the basis of sales. For the current year the sales for department A are $300 000 and for department B $200 000 and total advertising expenses are $12 600. The amount allocated to the two departments is:

A) A $9 450; B $3 150

B) A $6 300; B $6 300

C) A $5 040; B $7 560

D) A $7 560; B $5 040

A) A $9 450; B $3 150

B) A $6 300; B $6 300

C) A $5 040; B $7 560

D) A $7 560; B $5 040

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

9

Which of the following is not an example of a service department for a university?

A) Personnel

B) Marketing

C) University library

D) Engineering faculty

A) Personnel

B) Marketing

C) University library

D) Engineering faculty

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

10

With a management by exception system:

A) significant variances are investigated.

B) significant favourable variances are investigated.

C) significant unfavourable variances are investigated.

D) all variances are investigated.

A) significant variances are investigated.

B) significant favourable variances are investigated.

C) significant unfavourable variances are investigated.

D) all variances are investigated.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

11

Costs that can be influenced by a manager in the short term are called:

A) direct costs.

B) controllable costs.

C) departmental costs.

D) non-traceable costs.

A) direct costs.

B) controllable costs.

C) departmental costs.

D) non-traceable costs.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

12

A typical example of a direct cost for the distribution department is:

A) remuneration for the board of directors.

B) depreciation on the factory building.

C) distribution staff's wages.

D) building rent.

A) remuneration for the board of directors.

B) depreciation on the factory building.

C) distribution staff's wages.

D) building rent.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

13

Which departmental report is not suitable for use for responsibility accounting purposes?

A) A report that shows no significant variances.

B) A report that only includes costs controllable by the manager.

C) A report that the department manager has not participated in preparing.

D) A report where a share of all the businesses expenses have been allocated to departments.

A) A report that shows no significant variances.

B) A report that only includes costs controllable by the manager.

C) A report that the department manager has not participated in preparing.

D) A report where a share of all the businesses expenses have been allocated to departments.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

14

Management by exception means:

A) understanding that exceptional circumstances may affect expected results.

B) only variances that differ significantly from plan are investigated.

C) exceptional staff are rewarded.

D) responsibility is delegated.

A) understanding that exceptional circumstances may affect expected results.

B) only variances that differ significantly from plan are investigated.

C) exceptional staff are rewarded.

D) responsibility is delegated.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

15

Which of the following factors is the least controllable by the department manager and therefore not the managers main focus of attention?

A) Indirect operating expenses

B) Number of units sold

C) Mix of products sold

D) Selling prices

A) Indirect operating expenses

B) Number of units sold

C) Mix of products sold

D) Selling prices

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

16

Cyber Company occupies one site and consists of Departments, Alpha, Delta and Omega. If Department Alpha is the cost object, which of the following is an example of an indirect cost?

A) Building rental

B) Salary of Department Alpha manager

C) Stationery costs of Department Alpha

D) Commission of the sales persons for Department Alpha

A) Building rental

B) Salary of Department Alpha manager

C) Stationery costs of Department Alpha

D) Commission of the sales persons for Department Alpha

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

17

The item, department or job for which costs are accumulated is called a:

A) business.

B) cost object.

C) balanced scorecard.

D) business department.

A) business.

B) cost object.

C) balanced scorecard.

D) business department.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

18

Departmental gross profit, for a retailer, is calculated as:

A) departmental sales revenue, less gross profit.

B) departmental sales revenue, less cost of sales.

C) departmental sales revenue, less all expenses allocated to the department.

D) departmental sales revenue, less cost of sales, less selling expenses allocated to the department.

A) departmental sales revenue, less gross profit.

B) departmental sales revenue, less cost of sales.

C) departmental sales revenue, less all expenses allocated to the department.

D) departmental sales revenue, less cost of sales, less selling expenses allocated to the department.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

19

A deviation from a financial plan is called a(n):

A) departure.

B) allocation.

C) variance.

D) uncontrollable cost.

A) departure.

B) allocation.

C) variance.

D) uncontrollable cost.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

20

Which of the following statements concerning departmental (segmental) accounting is correct?

A) Segment/departmental information can only be produced by large organisations.

B) Segment/departmental information is only produced for use by internal management.

C) A balance sheet is normally produced for each segment of the business under segmental accounting.

D) There is an accounting standard dealing with segment reporting.

A) Segment/departmental information can only be produced by large organisations.

B) Segment/departmental information is only produced for use by internal management.

C) A balance sheet is normally produced for each segment of the business under segmental accounting.

D) There is an accounting standard dealing with segment reporting.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

21

In a decision relating to the possible elimination of a department consideration would need to be given to which of the following factors?

I) Alternative uses of the space currently occupied by the department

II) Adverse effect of the elimination of sales of other departments

III) Whether all of the direct operating expenses are avoidable

A) None of the factors.

B) I and III only.

C) I and II only.

D) I, II and III.

I) Alternative uses of the space currently occupied by the department

II) Adverse effect of the elimination of sales of other departments

III) Whether all of the direct operating expenses are avoidable

A) None of the factors.

B) I and III only.

C) I and II only.

D) I, II and III.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

22

Northern Company has three departments, Wires, Ropes and Cables. At the end of the accounting period the following information is available:

Northern Company is considering eliminating the Wires department. What will be the change in Northern Company's profit if the Wires department is eliminated? Assume that all indirect expenses are unavoidable and that all other circumstances are held constant.

A) $1 000 fall

B) $4 000 fall

C) $3 000 fall

D) $3 000 increase

Northern Company is considering eliminating the Wires department. What will be the change in Northern Company's profit if the Wires department is eliminated? Assume that all indirect expenses are unavoidable and that all other circumstances are held constant.

A) $1 000 fall

B) $4 000 fall

C) $3 000 fall

D) $3 000 increase

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

23

Performance reports should only contain costs, income or resources that are:

A) actual rather than budgeted amounts.

B) different from budgeted amounts.

C) more than budgeted amounts.

D) controllable by the manager.

A) actual rather than budgeted amounts.

B) different from budgeted amounts.

C) more than budgeted amounts.

D) controllable by the manager.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

24

Gross profit less direct operating expenses equals:

A) departmental contribution.

B) departmental profit.

C) direct costs.

D) a variance.

A) departmental contribution.

B) departmental profit.

C) direct costs.

D) a variance.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

25

An allocation of delivery expenses to other departments which results in an answer that is not an estimate could be based on:

A) sales volume.

B) number of deliveries.

C) cubic volume of deliveries.

D) None of the above. The allocation of indirect expenses is always an estimate no matter which method is used.

A) sales volume.

B) number of deliveries.

C) cubic volume of deliveries.

D) None of the above. The allocation of indirect expenses is always an estimate no matter which method is used.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

26

Which of the following departments would not be considered a service department in a restaurant business?

A) Human resources department

B) Food preparation

C) Accounting department

D) Security

A) Human resources department

B) Food preparation

C) Accounting department

D) Security

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

27

Which of the following departments would not be considered a service department for a tyre retailer?

A) Workshop

B) Marketing

C) Accounting

D) Human resources

A) Workshop

B) Marketing

C) Accounting

D) Human resources

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

28

Which of the following could be cost objects?

I) A product

II) An activity

III) A department

IV) A specialised item of equipment

A) II, III and IV only.

B) I, II, and IV only. c I, II, III and IV.

D) I and II only.

I) A product

II) An activity

III) A department

IV) A specialised item of equipment

A) II, III and IV only.

B) I, II, and IV only. c I, II, III and IV.

D) I and II only.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

29

Department H has a gross profit of $48 000, direct departmental expenses of $33 500 and allocated expenses of $18 200 giving a net loss of $3 700. What would be the effect on the total organisation's profit if Department H was closed?

A) Profits would decrease $14 500

B) Profits would increase by $3 700

C) Profits would increase by $18 200

D) Profits would decrease by $18 200

A) Profits would decrease $14 500

B) Profits would increase by $3 700

C) Profits would increase by $18 200

D) Profits would decrease by $18 200

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

30

Star Manufacturing has departments A and B with departmental income statements as follows.

Star Manufacturing is considering eliminating Department B. Of the total 'other expenses' for the two departments of $22 000, $16 000 are fixed general overhead expenses and the rest are variable expenses based on 10% of sales. What is the present departmental contribution of Department B?

A) ($1 500)

B) $8 000

C) $11 500

D) $14 000

Star Manufacturing is considering eliminating Department B. Of the total 'other expenses' for the two departments of $22 000, $16 000 are fixed general overhead expenses and the rest are variable expenses based on 10% of sales. What is the present departmental contribution of Department B?

A) ($1 500)

B) $8 000

C) $11 500

D) $14 000

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

31

In a decision relating to the possible elimination of a department consideration needs to be given to all of the following except:

A) unavoidable expenses.

B) alternative uses of the space currently occupied.

C) whether all of the direct operating expenses are avoidable.

D) adverse effects of the elimination on sales of other departments.

A) unavoidable expenses.

B) alternative uses of the space currently occupied.

C) whether all of the direct operating expenses are avoidable.

D) adverse effects of the elimination on sales of other departments.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

32

A budget is a summary of expected costs for a range of activity levels geared to changes in the level of productive output.

A) master

B) flexible

C) continuous

D) departmental

A) master

B) flexible

C) continuous

D) departmental

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

33

Snowy Mountain Retailers are considering closing one of its low-profit departments. Assume that discontinuance of this department will not affect sales of the remaining departments. Which of the cost classifications below should be compared with departmental income to determine whether or not to close the department?

A) Fixed costs

B) Variable costs

C) Controllable costs

D) Avoidable costs

A) Fixed costs

B) Variable costs

C) Controllable costs

D) Avoidable costs

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

34

A variable costing income statement is the same as a:

A) classified income statement.

B) traditional income statement.

C) contribution margin income statement.

D) departmental income statement.

A) classified income statement.

B) traditional income statement.

C) contribution margin income statement.

D) departmental income statement.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

35

Which department is typically responsible for direct materials price variances?

A) Sales

B) Production

C) Purchasing

D) Engineering

A) Sales

B) Production

C) Purchasing

D) Engineering

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

36

Department M has a gross profit of $50 000, direct departmental expenses of $28 000 and allocated expenses of $26 000, giving it a net loss of $4 000. What would be the effect on the total organisation's profit if Department M were closed?

A) Profits would decrease $2 000

B) Profits would increase by $4 000

C) Profits would decrease by $22 000

D) Profits would increase by $26 000

A) Profits would decrease $2 000

B) Profits would increase by $4 000

C) Profits would decrease by $22 000

D) Profits would increase by $26 000

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

37

Which of the following statements concerning the allocation of indirect expenses to departments is correct?

A) Accountants have developed methods that have completely removed the subjectivity in allocating indirect costs to departments.

B) A departmental profit calculation should exclude expenses that the departmental manager has no control over.

C) When preparing departmental profit reports, it is best to assume that the departments are independent businesses.

D) Different accountants will normally choose similar bases to allocate overhead costs to departments.

A) Accountants have developed methods that have completely removed the subjectivity in allocating indirect costs to departments.

B) A departmental profit calculation should exclude expenses that the departmental manager has no control over.

C) When preparing departmental profit reports, it is best to assume that the departments are independent businesses.

D) Different accountants will normally choose similar bases to allocate overhead costs to departments.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

38

The biggest problem with allocating indirect expenses to segments is that:

A) fixed costs are ignored.

B) it is a time-consuming exercise.

C) allocations can be somewhat arbitrary and the results can vary widely.

D) some departments consume more indirect expenses.

A) fixed costs are ignored.

B) it is a time-consuming exercise.

C) allocations can be somewhat arbitrary and the results can vary widely.

D) some departments consume more indirect expenses.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

39

will continue to exist even if a department is eliminated.

A) Traceable expenses.

B) Controllable costs.

C) Unavoidable costs.

D) Indirect expenses.

A) Traceable expenses.

B) Controllable costs.

C) Unavoidable costs.

D) Indirect expenses.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

40

If consideration is being given to closing a department a complete analysis should include all of the following except:

A) the costs of closure.

B) alternative uses of the space provided.

C) the effect that the closure might have on the sales of other departments.

D) the overhead costs of the entity that have been allocated to the department.

A) the costs of closure.

B) alternative uses of the space provided.

C) the effect that the closure might have on the sales of other departments.

D) the overhead costs of the entity that have been allocated to the department.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

41

Which of the following are benefits of standard costing?

I) It makes employees more aware of the impact of costs on operations

II) It serves as a target against which to evaluate performance

III) It eliminates the need to compute variances

IV) It is a cheap way of valuing inventory

A) I, II, III and IV.

B) I, II and IV only.

C) II, III and IV only.

D) I and II only.

I) It makes employees more aware of the impact of costs on operations

II) It serves as a target against which to evaluate performance

III) It eliminates the need to compute variances

IV) It is a cheap way of valuing inventory

A) I, II, III and IV.

B) I, II and IV only.

C) II, III and IV only.

D) I and II only.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

42

Crystal Clear Company's budgeted production costs for the current year at an expected output of 20 000 units were:

Assume Crystal Clear uses a flexible budgeting system and actually produced 24 000 units at a total cost of $1 150 000. By how much did actual production cost differ from the flexible budget amount and in which direction?

A) Actual cost was $145 000 over flexible budget

B) Actual cost was $145 000 under flexible budget

C) Actual cost was $47 000 over flexible budget

D) Actual cost was $47 000 under flexible budget

Assume Crystal Clear uses a flexible budgeting system and actually produced 24 000 units at a total cost of $1 150 000. By how much did actual production cost differ from the flexible budget amount and in which direction?

A) Actual cost was $145 000 over flexible budget

B) Actual cost was $145 000 under flexible budget

C) Actual cost was $47 000 over flexible budget

D) Actual cost was $47 000 under flexible budget

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

43

Which of the following is the performance standard usually considered best in setting standard costs?

A) Profitable

B) Optimal

C) Attainable

D) Historical

A) Profitable

B) Optimal

C) Attainable

D) Historical

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

44

A flexible budget is one where:

A) fixed costs are not included.

B) the budget estimates are prepared for a range of activities.

C) the estimates are amended if they are not attained in the period.

D) preparation may be postponed if the entity is very busy or is short staffed.

A) fixed costs are not included.

B) the budget estimates are prepared for a range of activities.

C) the estimates are amended if they are not attained in the period.

D) preparation may be postponed if the entity is very busy or is short staffed.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

45

If the actual quantity of direct materials used equals the budgeted quantity of direct materials that should have been used, any difference between the budgeted total cost and the actual total cost of direct materials used must be due to a:

A) overhead variance.

B) materials price variance.

C) materials quantity variance.

D) materials efficiency variance.

A) overhead variance.

B) materials price variance.

C) materials quantity variance.

D) materials efficiency variance.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

46

Which of the following is a financial performance measure?

A) Number of set-ups

B) Number of invoices issued

C) Number of orders received

D) Profit as a percentage of sales

A) Number of set-ups

B) Number of invoices issued

C) Number of orders received

D) Profit as a percentage of sales

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

47

A standard cost accounting system can be used for which of the following costs?

I) Direct labour

II) Direct materials

III) Indirect materials

IV) Manufacturing overhead

A) I and II only.

B) II and IV only.

C) I, II and IV only.

D) I, II, III and IV.

I) Direct labour

II) Direct materials

III) Indirect materials

IV) Manufacturing overhead

A) I and II only.

B) II and IV only.

C) I, II and IV only.

D) I, II, III and IV.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

48

The performance standard is usually considered best for use in setting standard costs.

A) ideal

B) average

C) historical

D) attainable

A) ideal

B) average

C) historical

D) attainable

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

49

Which of the following is a key purpose of standard costing?

A) Determining break-even production level

B) Allocating costs more accurately

C) Profit determination

D) Controlling costs

A) Determining break-even production level

B) Allocating costs more accurately

C) Profit determination

D) Controlling costs

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

50

Redoing the budget to actual output is most useful:

A) for planning purposes.

B) to calculate profitability accurately.

C) as a tool to help evaluate performance.

D) when actual output equals budgeted output.

A) for planning purposes.

B) to calculate profitability accurately.

C) as a tool to help evaluate performance.

D) when actual output equals budgeted output.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

51

Calculate the correct variances from the following: budgeted sales $78 000; actual sales $83 000; actual direct labour $36 000; budgeted direct labour $40 000.

A) Sales variance $5000 U: direct labour variance $4000 F

B) Sales variance $5000 F: direct labour variance $4000 F

C) Sales variance $5000 F: direct labour variance $4000 U

D) Sales variance $5000 U: direct labour variance $4000 U

A) Sales variance $5000 U: direct labour variance $4000 F

B) Sales variance $5000 F: direct labour variance $4000 F

C) Sales variance $5000 F: direct labour variance $4000 U

D) Sales variance $5000 U: direct labour variance $4000 U

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

52

Marcy's Roses uses a special potting mix that has a standard price of $8.00 per bag. During the year, the purchase price for the potting mix averaged $7.60 per bag. The business purchased and used 2360 bags of potting mix during the year. Calculate the direct materials price variance indicating whether it is favourable or unfavourable.

A) $944 (F)

B) $944 (U)

C) $1 416 (F)

D) $1 416 (U)

A) $944 (F)

B) $944 (U)

C) $1 416 (F)

D) $1 416 (U)

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

53

Which of the following is not an engineering method that can be used to develop standards?

A) Work sampling

B) Balanced scorecard

C) Simulation procedures

D) Time and motion studies

A) Work sampling

B) Balanced scorecard

C) Simulation procedures

D) Time and motion studies

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

54

Which of the following statements relating to standard costs is incorrect?

A) They are predetermined costs.

B) The approach is not suitable for a service business.

C) An unfavourable variance occurs when actual costs exceed standard costs.

D) They serve as benchmarks against which actual performance can be evaluated.

A) They are predetermined costs.

B) The approach is not suitable for a service business.

C) An unfavourable variance occurs when actual costs exceed standard costs.

D) They serve as benchmarks against which actual performance can be evaluated.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

55

Fifteen minutes of direct labour is needed to produce one unit of product and direct labour is paid $20 per hour. Budgeted output for the period is estimated to be 14 000 units. Actual output for the period turns out to be 14 600 units and actual labour costs are $77 900. What budgeted direct labour amount should actual direct labour costs be compared to in order to calculate a valid variance?

A) $70 000

B) $73 000

C) $56 000

D) $58 400

A) $70 000

B) $73 000

C) $56 000

D) $58 400

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

56

Which of the following statements is not true?

A) Performance reports normally report standard costs and variances.

B) Performance reports should contain space for explanations of variances.

C) Performance reports do not present the causes of variances.

D) Performance reports should be tailored to the responsibilities of the manager or department for which they are prepared.

A) Performance reports normally report standard costs and variances.

B) Performance reports should contain space for explanations of variances.

C) Performance reports do not present the causes of variances.

D) Performance reports should be tailored to the responsibilities of the manager or department for which they are prepared.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

57

The fixed budget performance report of Boston Associates for the year ended 30 June 2019 shows budgeted manufacturing costs of $540 000 and actual manufacturing costs of $570 000. The unfavourable variance of $30 000 must have been due to:

A) cost factors.

B) poor budgeting.

C) lack of supervision of workers.

D) cannot be determined from the information provided.

A) cost factors.

B) poor budgeting.

C) lack of supervision of workers.

D) cannot be determined from the information provided.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

58

Which of the following methods is not employed in the establishment of standard costs?

A) management judgement concerning future operating conditions.

B) analysis of historical performance data.

C) discounted cash flow analysis.

D) time and motion studies.

A) management judgement concerning future operating conditions.

B) analysis of historical performance data.

C) discounted cash flow analysis.

D) time and motion studies.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

59

Which of the following statements is correct?

A) Standard costs are the costs necessary to produce an average or standard product.

B) Standard costs can serve as benchmarks against which budgeted performance is measured.

C) The limitation of actual costs is that they represent what happened not necessarily what should have happened.

D) Standard costs can only be used for analytical purposes and can never be incorporated into the formal accounting system.

A) Standard costs are the costs necessary to produce an average or standard product.

B) Standard costs can serve as benchmarks against which budgeted performance is measured.

C) The limitation of actual costs is that they represent what happened not necessarily what should have happened.

D) Standard costs can only be used for analytical purposes and can never be incorporated into the formal accounting system.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

60

Compute the correct variances: budgeted sales $95 000: actual sales $79 000. Actual direct materials $33 000: budgeted direct materials $28 000.

A) Sales variance $16 000 U: direct materials variance $5 000 U

B) Sales variance $16 000 U: direct materials variance $5 000 F

C) Sales variance $67 000 F: direct materials variance $46 000 F

D) Sales variance $67 000 U: direct materials variance $46 000 F

A) Sales variance $16 000 U: direct materials variance $5 000 U

B) Sales variance $16 000 U: direct materials variance $5 000 F

C) Sales variance $67 000 F: direct materials variance $46 000 F

D) Sales variance $67 000 U: direct materials variance $46 000 F

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

61

The balanced scorecard approach requires the organisation to be viewed from four perspectives. Which of the following are included in this approach?

I) Supplier.

II) Taxation obligations.

III) Financial performance.

IV) Customer perspectives.

A) III and IV only.

B) I and IV only.

C) II and III only.

D) I, II, III and IV.

I) Supplier.

II) Taxation obligations.

III) Financial performance.

IV) Customer perspectives.

A) III and IV only.

B) I and IV only.

C) II and III only.

D) I, II, III and IV.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

62

Which of the following is a financial performance measure?

A) Hours of inspections

B) Customer complaints

C) Working capital ratio

D) Number of orders shipped

A) Hours of inspections

B) Customer complaints

C) Working capital ratio

D) Number of orders shipped

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

63

In current times the focus of managers has tended to shift away from measurement systems that rely on financial data to the design of total management systems. Which of the following is not a total management system?

A) Total quality management (TQM)

B) Activity-based costing (ABC)

C) The balanced scorecard (BSC)

D) Management by objectives (MBO)

A) Total quality management (TQM)

B) Activity-based costing (ABC)

C) The balanced scorecard (BSC)

D) Management by objectives (MBO)

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 63 flashcards in this deck.