Deck 8: Partnerships: Formation, Operation and Reporting

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

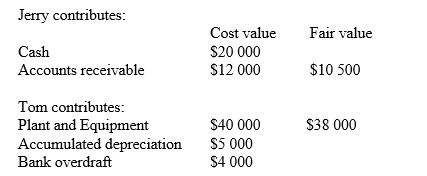

Tom and Jerry are two sole traders that have joined together to form a partnership by combining their net assets.

Jerry contributes:

The amount credited to Jerry's capital account is:

A) $(10 500).

B) $28 500.

C) $30 500.

D) $32 000.

Jerry contributes:

The amount credited to Jerry's capital account is:

A) $(10 500).

B) $28 500.

C) $30 500.

D) $32 000.

Question

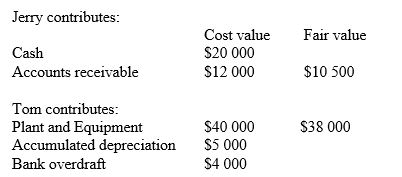

Tom and Jerry are two sole traders that have joined together to form a partnership by combining their net assets.

Jerry contributes:

What will be the amount shown in the allowance for doubtful debts account in the balance sheet prepared after the formation of the partnership of Tom and Jerry?

A) Nil

B) $500

C) $1000

D) $1500

Jerry contributes:

What will be the amount shown in the allowance for doubtful debts account in the balance sheet prepared after the formation of the partnership of Tom and Jerry?

A) Nil

B) $500

C) $1000

D) $1500

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

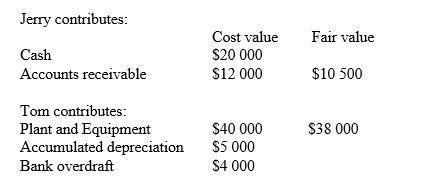

Tom and Jerry are two sole traders that have joined together to form a partnership by combining their net assets.

Jerry contributes:

What will be the amount shown in the accumulated depreciation account on formation of the partnership of Tom and Jerry?

A) $Nil

B) $2000

C) $3000

D) $5000

Jerry contributes:

What will be the amount shown in the accumulated depreciation account on formation of the partnership of Tom and Jerry?

A) $Nil

B) $2000

C) $3000

D) $5000

Question

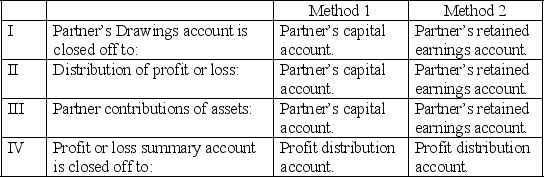

Which of the following are correct ways of recording partnership equity?

A) I, II and IV

B) I, II and III

C) II, and IV

D) I and III

A) I, II and IV

B) I, II and III

C) II, and IV

D) I and III

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/65

Play

Full screen (f)

Deck 8: Partnerships: Formation, Operation and Reporting

1

The text refers to two methods of accounting for equity in a partnership, method 1 and method 2; these are:

A) interest and no interest methods.

B) cash and credit capital methods.

C) variable and fixed capital account methods.

D) equal and proportionate profit sharing methods.

A) interest and no interest methods.

B) cash and credit capital methods.

C) variable and fixed capital account methods.

D) equal and proportionate profit sharing methods.

C

2

Which of the following is an advantage of a partnership over a sole proprietorship?

A) Transfer of ownership is easier.

B) Liability is unlimited.

C) Pooling of resources and skills

D) Mutual agency.

A) Transfer of ownership is easier.

B) Liability is unlimited.

C) Pooling of resources and skills

D) Mutual agency.

C

3

Which of the following is not a feature of the variable capital balances method (method 1) of accounting for partnership equity?

A) Each partner has one permanent capital account.

B) Partner's drawings are closed to their capital accounts.

C) Interest on capital is credited to the partners retained earnings accounts.

D) The profit or loss distribution account is closed to the partner's capital accounts.

A) Each partner has one permanent capital account.

B) Partner's drawings are closed to their capital accounts.

C) Interest on capital is credited to the partners retained earnings accounts.

D) The profit or loss distribution account is closed to the partner's capital accounts.

C

4

Which of the following is a not a disadvantage of operating as a partnership rather than as a company?

A) Fewer disclosure requirements

B) Greater difficulty in selling a share of the business.

C) Personal liability for all obligations of the partnership.

D) Partners can act on behalf of the other partners and bind them to a contract by acting within the apparent scope of the business.

A) Fewer disclosure requirements

B) Greater difficulty in selling a share of the business.

C) Personal liability for all obligations of the partnership.

D) Partners can act on behalf of the other partners and bind them to a contract by acting within the apparent scope of the business.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

5

Which of the following statements concerning partnership agreements is true?

A) The partnership agreement must be in writing.

B) The contractual authority of each partner should be specified.

C) Partner's must always contribute equal amounts of capital.

D) It is not necessary to specify the duration of the partnership.

A) The partnership agreement must be in writing.

B) The contractual authority of each partner should be specified.

C) Partner's must always contribute equal amounts of capital.

D) It is not necessary to specify the duration of the partnership.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

6

As compared to a company with a similar number of shareholder's as there are partners in the partnership, an advantage of a partnership is:

A) mutual agency.

B) unlimited liability.

C) limited contributions.

D) less government regulation.

A) mutual agency.

B) unlimited liability.

C) limited contributions.

D) less government regulation.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

7

Which of the following is not a feature of the fixed capital balances method of accounting for partnership equity?

A) Each partner has two permanent equity accounts, a capital account and a retained earnings account.

B) Apart from the initial investment very few adjustments are made to the capital account.

C) The partners retained earnings accounts include their proportions of the profit of loss for the period.

D) Partner's drawings accounts are closed at the end of the accounting period to their capital accounts.

A) Each partner has two permanent equity accounts, a capital account and a retained earnings account.

B) Apart from the initial investment very few adjustments are made to the capital account.

C) The partners retained earnings accounts include their proportions of the profit of loss for the period.

D) Partner's drawings accounts are closed at the end of the accounting period to their capital accounts.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

8

is the characteristic of a partnership whereby each partner is liable for partnership debts to the full extent of his or her private assets.

A) limited life.

B) limited liability.

C) unlimited liability.

D) mutual agency.

A) limited life.

B) limited liability.

C) unlimited liability.

D) mutual agency.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

9

The relationship that exists between persons carrying on a business in common with a view to profit is referred to as a:

A) company.

B) proprietorship.

C) retailer.

D) partnership.

A) company.

B) proprietorship.

C) retailer.

D) partnership.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

10

The legislation in Australia that is concerned with the formation, operation and dissolution of partnerships is the:

A) Corporations Act.

B) Bankruptcy Act.

C) Partnership Act.

D) Business law Act.

A) Corporations Act.

B) Bankruptcy Act.

C) Partnership Act.

D) Business law Act.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

11

A limited partner is one who has limited his/her:

A) management rights.

B) right to share in profits and losses.

C) obligation to contribute capital.

D) liability for partnership debts to the amount of their contribution.

A) management rights.

B) right to share in profits and losses.

C) obligation to contribute capital.

D) liability for partnership debts to the amount of their contribution.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

12

Cameron and Andrew each invested $45 000 in a partnership where they agreed to share profits as Cameron: 30%; Andrew 70% . The partnership business was unsuccessful and now has zero assets. In addition, they are being sued for $100 000 by a supplier for non-payment of invoices. What is the amount for which Andrew could be held personally responsible if the lawsuit is successful? (Ignore any possible legal costs.)

A) Zero

B) $45 000

C) $70 000

D) $100 000

A) Zero

B) $45 000

C) $70 000

D) $100 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

13

The legislation with the most significant influence on the formation, operation and dissolution of partnerships is the:

A) Partnership Act.

B) Federal Partnership Act.

C) Common Partnership Program.

D) Partnership Formation, Operation and Liquidation Rules.

A) Partnership Act.

B) Federal Partnership Act.

C) Common Partnership Program.

D) Partnership Formation, Operation and Liquidation Rules.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

14

Which of these is not a provision of the Partnership Act?

A) No person may be expelled from the partnership without the consent of all existing partners.

B) A partner is entitled to interest on money advanced to the partnership that is in addition to their original contribution.

C) Each partner is permitted to withdraw up to 20% of their capital per annum for personal use.

D) Partners are entitled to share equally in the capital of the partnership.

A) No person may be expelled from the partnership without the consent of all existing partners.

B) A partner is entitled to interest on money advanced to the partnership that is in addition to their original contribution.

C) Each partner is permitted to withdraw up to 20% of their capital per annum for personal use.

D) Partners are entitled to share equally in the capital of the partnership.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

15

Which of the following statements relating to a 'general partnership' is incorrect?

A) Each partner is liable for the debts of the partnership only in proportion to their original contribution.

B) It is the most common form of partnership.

C) Each partner is personally liable for the obligations of the partnership.

D) Partners have unlimited liability.

A) Each partner is liable for the debts of the partnership only in proportion to their original contribution.

B) It is the most common form of partnership.

C) Each partner is personally liable for the obligations of the partnership.

D) Partners have unlimited liability.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

16

Accounting for a partnership is similar to accounting for a sole trader, except that:

A) tax must be calculated by the partnership on each partner's share of profit.

B) each partner's share of equity must be recorded separately.

C) each partner has limited liability.

D) most partnerships are not reporting entities.

A) tax must be calculated by the partnership on each partner's share of profit.

B) each partner's share of equity must be recorded separately.

C) each partner has limited liability.

D) most partnerships are not reporting entities.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following would not result in the automatic dissolution of a partnership?

A) A partner's illness

B) The bankruptcy of a partner

C) The death of a partner

D) The admission of a new partner

A) A partner's illness

B) The bankruptcy of a partner

C) The death of a partner

D) The admission of a new partner

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

18

The variable capital balances method (method 1), requires the profit or loss and partner's drawings to be closed off to each partner's:

A) capital account.

B) cash account.

C) profit or loss summary account.

D) retained earnings accounts.

A) capital account.

B) cash account.

C) profit or loss summary account.

D) retained earnings accounts.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following is not an advantage of a partnership?

A) Combination of various skills of the individual partners.

B) Flexibility in the running of the business.

C) The difficulty of transferring partnership interests

D) Easier and cheaper to establish.

A) Combination of various skills of the individual partners.

B) Flexibility in the running of the business.

C) The difficulty of transferring partnership interests

D) Easier and cheaper to establish.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

20

Which of the following would normally be referred to in a partnership agreement?

A) Profit and loss sharing ratios

B) Arrangements to terminate the partnership.

C) Procedures to follow in the event of a dispute.

D) All of these options.

A) Profit and loss sharing ratios

B) Arrangements to terminate the partnership.

C) Procedures to follow in the event of a dispute.

D) All of these options.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

21

A partner contributes plant and equipment when a partnership is established. The amount recognised by the partnership for this contributed asset is equal to:

A) the carrying amount of the asset at the date of contribution.

B) the fair value of the asset at the date of contribution.

C) the amount paid by the contributing partner when originally acquiring the asset.

D) the same proportion of contributions by other partners.

A) the carrying amount of the asset at the date of contribution.

B) the fair value of the asset at the date of contribution.

C) the amount paid by the contributing partner when originally acquiring the asset.

D) the same proportion of contributions by other partners.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

22

Tom and Jerry are two sole traders that have joined together to form a partnership by combining their net assets.

Jerry contributes:

The amount credited to Jerry's capital account is:

A) $(10 500).

B) $28 500.

C) $30 500.

D) $32 000.

Jerry contributes:

The amount credited to Jerry's capital account is:

A) $(10 500).

B) $28 500.

C) $30 500.

D) $32 000.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

23

Tom and Jerry are two sole traders that have joined together to form a partnership by combining their net assets.

Jerry contributes:

What will be the amount shown in the allowance for doubtful debts account in the balance sheet prepared after the formation of the partnership of Tom and Jerry?

A) Nil

B) $500

C) $1000

D) $1500

Jerry contributes:

What will be the amount shown in the allowance for doubtful debts account in the balance sheet prepared after the formation of the partnership of Tom and Jerry?

A) Nil

B) $500

C) $1000

D) $1500

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

24

With the fixed capital balances method (method 2) of accounting for partnership equity, the general journal entry to record interest on capital is:

A) DR Profit or loss summary account; CR Partner's capital accounts.

B) DR Profit or loss summary account; CR Partner's retained earnings accounts.

C) DR Profit distribution account; CR Partner's capital accounts.

D) DR Profit distribution account; CR Partner's retained profit accounts.

A) DR Profit or loss summary account; CR Partner's capital accounts.

B) DR Profit or loss summary account; CR Partner's retained earnings accounts.

C) DR Profit distribution account; CR Partner's capital accounts.

D) DR Profit distribution account; CR Partner's retained profit accounts.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

25

The objective of allocating profits and losses is to reward each partner fairly for the resources and services contributed to the partnership. Which of the following factors would not be directly relevant in negotiating a profit and loss sharing agreement for a partnership?

A) The risks assumed by each partner.

B) The size of each partner's non-partnership assets.

C) Work done by each partner in the partnership.

D) Capital contributed by each partner to the partnership.

A) The risks assumed by each partner.

B) The size of each partner's non-partnership assets.

C) Work done by each partner in the partnership.

D) Capital contributed by each partner to the partnership.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

26

Unless otherwise agreed amongst the partners, partners' salaries, interest on capital and interest on drawings are assumed in partnership accounting to be settled by means of:

A) a cash payment.

B) by offsetting entries.

C) an adjusting entry in the accounting records (book entry).

D) by private arrangement by the partners.

A) a cash payment.

B) by offsetting entries.

C) an adjusting entry in the accounting records (book entry).

D) by private arrangement by the partners.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

27

Bert and Ernie agree to share profits and losses in the ratios 6:4. If the net loss is $30,000, how much loss is allocated to each partner?

A) Bert $18 000; Ernie $12 000

B) Bert $12 000; Ernie $18 000

C) Bert $20 000; Ernie $10 000

D) Bert $26 000; Ernie $4 000

A) Bert $18 000; Ernie $12 000

B) Bert $12 000; Ernie $18 000

C) Bert $20 000; Ernie $10 000

D) Bert $26 000; Ernie $4 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

28

Steve, Chevy and Martin agree to share profits in the ratio 3: 5: 2. This means:

A) Steve is entitled to 3/5 of the profits.

B) Chevy is entitled to 1/2 of the profits.

C) Martin is entitled to 2/8 of the profits.

D) Steve is entitled to 1/3 of the profits.

A) Steve is entitled to 3/5 of the profits.

B) Chevy is entitled to 1/2 of the profits.

C) Martin is entitled to 2/8 of the profits.

D) Steve is entitled to 1/3 of the profits.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

29

Assets contributed to a partnership should be initially recorded at:

A) replacement value.

B) carrying amount.

C) fair value.

D) historical cost.

A) replacement value.

B) carrying amount.

C) fair value.

D) historical cost.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

30

A partner's allocation of the partnership's profit or loss is recorded in the:

A) drawings account.

B) balance sheet.

C) profit or loss summary account.

D) profit distribution account.

A) drawings account.

B) balance sheet.

C) profit or loss summary account.

D) profit distribution account.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

31

After completion of the closing entries, the profit distribution account in a partnership always has a:

A) nil balance.

B) debit balance.

C) credit balance.

D) negative balance.

A) nil balance.

B) debit balance.

C) credit balance.

D) negative balance.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

32

Only goodwill should be recorded in the balance sheet.

A) customer.

B) internally generated.

C) purchased.

D) current.

A) customer.

B) internally generated.

C) purchased.

D) current.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

33

Tom and Jerry are two sole traders that have joined together to form a partnership by combining their net assets.

Jerry contributes:

What will be the amount shown in the accumulated depreciation account on formation of the partnership of Tom and Jerry?

A) $Nil

B) $2000

C) $3000

D) $5000

Jerry contributes:

What will be the amount shown in the accumulated depreciation account on formation of the partnership of Tom and Jerry?

A) $Nil

B) $2000

C) $3000

D) $5000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

34

Which of the following are correct ways of recording partnership equity?

A) I, II and IV

B) I, II and III

C) II, and IV

D) I and III

A) I, II and IV

B) I, II and III

C) II, and IV

D) I and III

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

35

Goodwill represents the future benefits of unidentifiable assets. Which of the factors listed below contribute to the value of goodwill?

I)Favourable location

II) Efficient manufacturing

III) Good customer relations

IV) Staff skills and experience

A) I, II and IV.

B) II and III.

C) II and IV.

D) I, II, III and IV

I)Favourable location

II) Efficient manufacturing

III) Good customer relations

IV) Staff skills and experience

A) I, II and IV.

B) II and III.

C) II and IV.

D) I, II, III and IV

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

36

Sole proprietors, Johnny and Simon, decide to form a partnership. Johnny contributes inventory with a fair value of $20 000, machinery with a fair value of $120 000 and it is agreed that the partnership will take over Johnny's bank loan of $50 000. Assuming the partnership agreement states that the balance of partnership capital will be equal to the fair value of the net assets contributed, what is the amount recorded in Johnny's capital account?

A) $70 000

B) $90 000

C) $120 000

D) $140 000

A) $70 000

B) $90 000

C) $120 000

D) $140 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

37

When non-current assets are contributed by a partner they should be recorded in the partnership books at:

A) historic cost.

B) depreciable value.

C) carrying amount.

D) fair value.

A) historic cost.

B) depreciable value.

C) carrying amount.

D) fair value.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

38

The fair value of an asset, as defined in the accounting standards, is:

A) the costs incurred to purchase an asset and make it ready for use.

B) the price that would be received to sell an asset in an orderly transaction between market participants at the measurement date, after deducting all the costs of that transfer.

C) the price paid for an asset less any directly attributable costs.

D) the costs that would be incurred if the asset needed to be replaced.

A) the costs incurred to purchase an asset and make it ready for use.

B) the price that would be received to sell an asset in an orderly transaction between market participants at the measurement date, after deducting all the costs of that transfer.

C) the price paid for an asset less any directly attributable costs.

D) the costs that would be incurred if the asset needed to be replaced.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

39

In a partnership, the profit and loss sharing ratio will be based:

A) proportionately as per the capital contributions of the partners.

B) on the relative effort contributed by the partners.

C) the relative business risks assumed by the partners.

D) on a formula that the partners agree upon.

A) proportionately as per the capital contributions of the partners.

B) on the relative effort contributed by the partners.

C) the relative business risks assumed by the partners.

D) on a formula that the partners agree upon.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

40

Accountants do not recognise internally generated goodwill because:

A) it is immaterial.

B) it is not a partnership asset.

C) it cannot be measured reliably.

D) it will not provide a future economic benefit.

A) it is immaterial.

B) it is not a partnership asset.

C) it cannot be measured reliably.

D) it will not provide a future economic benefit.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

41

Paula and Penny have capital balances of $120 000 and $150 000 respectively and use the variable capital balances method. If their profit/loss sharing ratios are Paula 40% and Penny 60%, the balance of Penny's capital balance after a profit of $60 000 is:

A) $114 000

B) $150 000

C) $174 000

D) $186 000

A) $114 000

B) $150 000

C) $174 000

D) $186 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

42

The partnership agreement between Allen and Barry states that profit and loss sharing arrangements will be based on the ratio of the partner's capital balances. Allen and Barry have capital balances of $90 000 and $60 000 respectively at the end of the accounting period. If profit for the period is $48 000, the profit allocations of each of the partners is:

A) Allen $24 000; Barry $24 000.

B) Allen $28 800; Barry $19 200.

C) Allen $30 000; Barry $18 000.

D) unable to be calculated from the information provided.

A) Allen $24 000; Barry $24 000.

B) Allen $28 800; Barry $19 200.

C) Allen $30 000; Barry $18 000.

D) unable to be calculated from the information provided.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

43

With the variable capital balances method (method 1) of accounting for partnership equity, the general journal entry to record interest on capital is:

A) DR Profit distribution account; CR Partner's capital accounts.

B) DR Profit or loss summary account; CR Partner's capital accounts.

C) DR Profit distribution account; CR Partner's retained earnings accounts.

D) DR Profit or loss summary account; CR Partner's retained earnings accounts.

A) DR Profit distribution account; CR Partner's capital accounts.

B) DR Profit or loss summary account; CR Partner's capital accounts.

C) DR Profit distribution account; CR Partner's retained earnings accounts.

D) DR Profit or loss summary account; CR Partner's retained earnings accounts.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

44

How is the allocation of partnership profits affected by drawings?

A) Drawings must be deducted from partners' salaries.

B) Drawings must be added back to profits before they are allocated.

C) Drawings must be deducted from profits before they are allocated.

D) Drawings only affect profit allocation if the partnership agreement provides for interest on drawings.

A) Drawings must be deducted from partners' salaries.

B) Drawings must be added back to profits before they are allocated.

C) Drawings must be deducted from profits before they are allocated.

D) Drawings only affect profit allocation if the partnership agreement provides for interest on drawings.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

45

When preparing the closing entries for a partnership at the end of the accounting period which of the following statements is correct? Assume that capital account balances are not fixed.

A) The retained earnings account is closed to the profit or loss summary account.

B) The drawings accounts are closed to the capital accounts.

C) Income and expenses are closed to the capital accounts.

D) The profit or loss summary account is closed to the retained earnings accounts.

A) The retained earnings account is closed to the profit or loss summary account.

B) The drawings accounts are closed to the capital accounts.

C) Income and expenses are closed to the capital accounts.

D) The profit or loss summary account is closed to the retained earnings accounts.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

46

Bonnie and Cathy have a profit and loss sharing agreement where: (1) salaries of $20 000 each are credited, (2) 10% interest is allowed on capital balances (3) the remaining profit or loss is split 60-40 in favour of Bonnie. At the end of the year, before the distribution of profits or losses, capital account balances were $50 000 and $35 000 for Bonnie and Cathy, respectively. Profit for the year was $66 000 before distributions to partners. Assuming capital balances are adjusted to reflect profits and losses, what is Bonnie's ending capital account balance?

A) $89 600

B) $64 600

C) $85 500

D) $35 500

A) $89 600

B) $64 600

C) $85 500

D) $35 500

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

47

Fiona and Jason have capital balances of $40 000 and $80 000 respectively and use the variable capital balances method. If their profit/loss sharing ratios are Fiona 25% and Jason 75%, the balance of Fiona's capital account after a net loss of $50 000 is:

A) $23 333

B) $27 500

C) $10 000

D) $52 500

A) $23 333

B) $27 500

C) $10 000

D) $52 500

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

48

Hodges and Burton formed a partnership with capital of $30 000 and $45 000 respectively. The partnership agreement provides for the crediting of annual salaries of $45 000 to Hodges and $75 000 to Burton. Each partner is entitled to 20% interest on capital. The remaining profit or loss is divided equally. Assuming capital balances are adjusted to reflect profits and losses, how much, in total, will be credited to Burton's capital account if profit for the year is $198 000?

A) $ 82 500

B) $115 500

C) $ 52 500

D) $ 85 500

A) $ 82 500

B) $115 500

C) $ 52 500

D) $ 85 500

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

49

The partnership agreement of Snowy and Brodie provides that interest at 2% per annum is to be charged on partners' drawings. During the year ended 31 December drawings by both partners were:

What is the total amount of interest on drawings chargeable to Brodie's current account for the year?

A) $62

B) $73

C) $56

D) $31

What is the total amount of interest on drawings chargeable to Brodie's current account for the year?

A) $62

B) $73

C) $56

D) $31

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

50

Simon and Keith have a profit and loss sharing agreement where: (1) salaries of $30 000 each are credited, (2) 6% interest is allowed on capital balances (3) the remaining profit or loss is split 75-25, respectively. At the end of the year, before the distribution of profits or losses, capital account balances were $40 000 for Simon and $20 000 for Keith. There was a profit of $50 000 before distributions to the partners. What is Keith's year-end capital account balance assuming capital balances are adjusted to reflect profits and losses?

A) $47 800

B) $54 600

C) $62 200

D) $82 600

A) $47 800

B) $54 600

C) $62 200

D) $82 600

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

51

If the fixed capital balances method (method 2) is used to account for partnership equity, both the profit or loss and the partner's drawings are closed to the:

A) profit or loss summary account.

B) profit distribution account.

C) partners' retained earnings accounts.

D) partners' capital accounts.

A) profit or loss summary account.

B) profit distribution account.

C) partners' retained earnings accounts.

D) partners' capital accounts.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

52

Sometimes the partnership agreement may specify that interest is to be charged on partner's drawings. The main reason for such a charge is:

A) to reduce partnership profits.

B) to increase the income of the partnership.

C) to encourage partner's to withdraw extra amounts.

D) to act as a disincentive to partners withdrawing excessive amounts from the partnership.

A) to reduce partnership profits.

B) to increase the income of the partnership.

C) to encourage partner's to withdraw extra amounts.

D) to act as a disincentive to partners withdrawing excessive amounts from the partnership.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

53

Which statement concerning drawings by partners in a partnership is correct?

A) Drawings are generally regarded as withdrawals of future profits.

B) Drawings are taken into account when calculating the final distribution of profit between the partners.

C) Interest is charged on drawings if the partnership agreement is silent on the matter.

D) Charging interest on drawings acts as an incentive to partners to withdraw money from the partnership.

A) Drawings are generally regarded as withdrawals of future profits.

B) Drawings are taken into account when calculating the final distribution of profit between the partners.

C) Interest is charged on drawings if the partnership agreement is silent on the matter.

D) Charging interest on drawings acts as an incentive to partners to withdraw money from the partnership.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

54

Macy and John have capital account balances at the end of the year of $100 000 and $25 000 respectively. Profit of the partnership is $105 000. The profit and loss sharing agreement calls for (1) a salary of $40 000 to Macy and $35 000 to John, (2) interest of 5% p.a. on capital balances, (3) the residual profit to be split 80:20 in favour of Macy. Macy's share of the distribution is:

A) $26 000

B) $64 000

C) $41 000

D) $45 000

A) $26 000

B) $64 000

C) $41 000

D) $45 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

55

A partner makes a cash advance to the partnership which is to be repaid in three years' time. The partner does not wish this advance to be included as a capital contribution. The correct classification for this in the balance sheet is:

A) Current asset

B) Non-current asset

C) Current liability

D) Non-current liability

A) Current asset

B) Non-current asset

C) Current liability

D) Non-current liability

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

56

When a partner makes an advance or loan to the partnership, which of the following statements is correct?

I)The partner is entitled to interest at the rate of 7% p.a. unless there is an agreement to the contrary.

II)The amount loaned is added to the partner's equity account balance.

III)Interest on the loan is regarded as an expense of the partnership and appears in the income statement.

A) I and II

B) I and III

C) II and III

D) I, II and III

I)The partner is entitled to interest at the rate of 7% p.a. unless there is an agreement to the contrary.

II)The amount loaned is added to the partner's equity account balance.

III)Interest on the loan is regarded as an expense of the partnership and appears in the income statement.

A) I and II

B) I and III

C) II and III

D) I, II and III

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

57

Interest paid on a loan provided by a partner should be:

A) a distribution of profit in the profit or loss distribution account.

B) recognised as income for the partner who provided the loan.

C) recorded as a prepayment in the balance sheet.

D) recognised by the partnership as an expense.

A) a distribution of profit in the profit or loss distribution account.

B) recognised as income for the partner who provided the loan.

C) recorded as a prepayment in the balance sheet.

D) recognised by the partnership as an expense.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

58

Louise and Thelma are in partnership sharing residual profits and losses 50:50. The profit for the year is $96 000. Thelma is entitled to a salary of $40 000 per annum (to be paid by means of a book entry). The amount credited to Thelma's retained earnings account after the final distribution of profits is:

A) $88 000

B) $48 000

C) $28 000

D) $68 000

A) $88 000

B) $48 000

C) $28 000

D) $68 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

59

Gemma and Audrey are in partnership. Their capital balances at the end of the accounting period are $200 000 and $150 000 respectively. Gemma decides to make a permanent cash withdrawal from her capital account of $75 000. Assuming the variable capital balances method (method 1) is used, the correct accounting entry to record this transaction is:

A) DR Gemma - Retained earnings account $75 000; CR Cash account $75 000

B) DR Gemma - Capital account $75 000; CR Cash account $75 000

C) DR Gemma - Capital account $75 000; CR Profit distribution account $75 000

D) DR Gemma - Retained earnings account $75 000; CR Profit distribution account $75 000

A) DR Gemma - Retained earnings account $75 000; CR Cash account $75 000

B) DR Gemma - Capital account $75 000; CR Cash account $75 000

C) DR Gemma - Capital account $75 000; CR Profit distribution account $75 000

D) DR Gemma - Retained earnings account $75 000; CR Profit distribution account $75 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

60

Partner's drawings are:

A) amounts credited for working in the partnership.

B) partner's artwork.

C) cash amounts withdrawn or private expenses paid by the partnership on behalf of a partner, in anticipation of profits.

D) money borrowed from the partnership.

A) amounts credited for working in the partnership.

B) partner's artwork.

C) cash amounts withdrawn or private expenses paid by the partnership on behalf of a partner, in anticipation of profits.

D) money borrowed from the partnership.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

61

Gemma and Audrey are in partnership. Their capital balances at the end of the accounting period are $200 000 and $150 000 respectively. Gemma decides to make a permanent cash withdrawal from her capital account of $75 000. Assuming the fixed capital balances method (method 2) is used, the accounting entry to record this transaction is:

A) DR Gemma capital account $75 000; CR Profit distribution account $75 000

B) DR Gemma capital account $75 000; CR Bank account $75 000

C) DR Gemma retained earnings account $75 000; CR Profit distribution account $75 000

D) DR Gemma retained earnings account $75 000; CR Bank account $75 000

A) DR Gemma capital account $75 000; CR Profit distribution account $75 000

B) DR Gemma capital account $75 000; CR Bank account $75 000

C) DR Gemma retained earnings account $75 000; CR Profit distribution account $75 000

D) DR Gemma retained earnings account $75 000; CR Bank account $75 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

62

When the final financial statements are prepared the profit or loss allocation for a partnership is normally shown in the:

A) statement of changes in partner's equity.

B) profit or loss allocation statement.

C) profit distribution statement.

D) cash distribution statement.

A) statement of changes in partner's equity.

B) profit or loss allocation statement.

C) profit distribution statement.

D) cash distribution statement.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

63

A partnership that is a reporting entity must produce which of these financial statements?

I) Income statement

Ii) Balance sheet

Iii) Statement of cash flows

Iv) Statement of changes in partners' equity

A) i, ii, iii

B) i, iii

C) i, ii, iii, iv

D) None of these statements

I) Income statement

Ii) Balance sheet

Iii) Statement of cash flows

Iv) Statement of changes in partners' equity

A) i, ii, iii

B) i, iii

C) i, ii, iii, iv

D) None of these statements

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

64

The part of the financial statements of a partnership that differs most from that of a sole trader is the:

A) assets section of the balance sheet.

B) equity section of the balance sheet.

C) expense section of the income statement.

D) income section of the income statement.

A) assets section of the balance sheet.

B) equity section of the balance sheet.

C) expense section of the income statement.

D) income section of the income statement.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

65

Which of the following statements relating to financial reports for a partnership is incorrect?

A) Partners' salaries are normally treated as an allocation of profit.

B) Each individual partner's equity in the business is reported separately.

C) Interest on capital contributions is treated as an allocation of profits.

D) Income tax expense is deducted from the partnership profit at the end of the income statement.

A) Partners' salaries are normally treated as an allocation of profit.

B) Each individual partner's equity in the business is reported separately.

C) Interest on capital contributions is treated as an allocation of profits.

D) Income tax expense is deducted from the partnership profit at the end of the income statement.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 65 flashcards in this deck.