Deck 12: Budgeting for Planning and Control

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

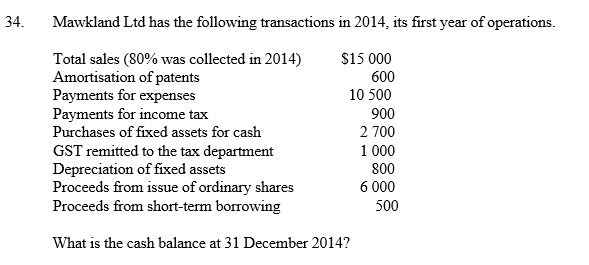

Question

Question

Question

Question

Question

Question

Question

A) $400

B) $2000

C) $2600

D) $3400

Question

Question

Question

Question

A) 4800.

B) 6480.

C) 7920.

D) 10 400.

Question

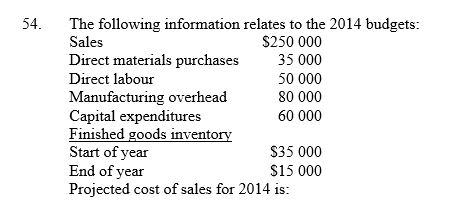

Question

Question

Question

Question

Question

Question

Question

A) $150

B) $1800

C) $1440

D) $2400

Question

Question

Question

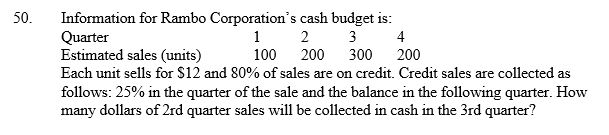

Information for Fine Line Fishing Product's cash budget is as follows.

Each unit sells for $12 and 80% of sales are on credit. Credit sales are collected as follows: 25% in the quarter of the sale and the balance in the following quarter. How many dollars of 3rd quarter sales will be collected in cash in the 4th quarter?

A) $225

B) $2160

C) $180

D) $2700

Each unit sells for $12 and 80% of sales are on credit. Credit sales are collected as follows: 25% in the quarter of the sale and the balance in the following quarter. How many dollars of 3rd quarter sales will be collected in cash in the 4th quarter?

A) $225

B) $2160

C) $180

D) $2700

Question

Question

Question

Question

A) $185 000.

B) $200 000.

C) $215 000.

D) $235 000.

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/65

Play

Full screen (f)

Deck 12: Budgeting for Planning and Control

1

Which of the following offers the best explanation of goal congruence?

A) Instructing lower levels of management what to do and how to do it.

B) All segments working towards the overall goals set by the organisation.

C) Rewarding managers who reach their performance targets.

D) All the business in an industry working together to solve problems.

A) Instructing lower levels of management what to do and how to do it.

B) All segments working towards the overall goals set by the organisation.

C) Rewarding managers who reach their performance targets.

D) All the business in an industry working together to solve problems.

B

2

Which of these is part of the operating set of budgets of a service organisation?

A) Capital expenditure budget

B) Cash budget

C) Expenses budget

D) Budgeted balance sheet

A) Capital expenditure budget

B) Cash budget

C) Expenses budget

D) Budgeted balance sheet

C

3

Which of these is not a benefit of budgeting?

A) Liquidity management

B) Motivation

C) Coordination

D) It saves management work

A) Liquidity management

B) Motivation

C) Coordination

D) It saves management work

D

4

For a budget to be most effective it is best approached from a:

A) top down approach.

B) middle up approach.

C) bottom up approach.

D) middle out approach.

A) top down approach.

B) middle up approach.

C) bottom up approach.

D) middle out approach.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

5

Which of these factors need not be present for budgeting to work efficiently?

A) Management participation.

B) An efficient accounting and reporting system.

C) An organisational structure in which responsibility is clearly defined.

D) A flat management structure.

A) Management participation.

B) An efficient accounting and reporting system.

C) An organisational structure in which responsibility is clearly defined.

D) A flat management structure.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

6

Which statement relating to a master budget is not true?

A) Budget targets are fixed and not subject to revision.

B) It is a set of interrelated budgets.

C) It is normally overseen by a budget committee.

D) It is typically prepared for a one-year period that coincides with the entity's financial year.

A) Budget targets are fixed and not subject to revision.

B) It is a set of interrelated budgets.

C) It is normally overseen by a budget committee.

D) It is typically prepared for a one-year period that coincides with the entity's financial year.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

7

The term used when the personal and corporate goals of the managers of an entity are consistent with the goals of the organisation is:

A) master budgeting.

B) goal congruence.

C) co-ordination.

D) a balanced scorecard.

A) master budgeting.

B) goal congruence.

C) co-ordination.

D) a balanced scorecard.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

8

Which of these is not a financial budget?

A) Budgeted income statement

B) Budgeted balance sheet

C) Cash budget

D) Capital expenditure budget

A) Budgeted income statement

B) Budgeted balance sheet

C) Cash budget

D) Capital expenditure budget

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

9

The behavioural aspect of budgeting is:

A) irrelevant.

B) only important for some firms.

C) generally important.

D) very important.

A) irrelevant.

B) only important for some firms.

C) generally important.

D) very important.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

10

Budgeting for a retailer requires a purchases budget to be prepared. When budgeting for a manufacturer the purchases budget is replaced by which budget?

A) Budgeted cost of sales

B) Budgeted income statement

C) Expense budget

D) Production budget

A) Budgeted cost of sales

B) Budgeted income statement

C) Expense budget

D) Production budget

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

11

Which statement concerning responsibility accounting is untrue?

A) For successful budgeting responsibility must be clearly defined.

B) A manager is held responsible for the activities of his/her department.

C) The choice of responsibility centres in an organisation depends on its characteristics.

D) Responsibility centres are usually determined by differences in the product the firm produces.

A) For successful budgeting responsibility must be clearly defined.

B) A manager is held responsible for the activities of his/her department.

C) The choice of responsibility centres in an organisation depends on its characteristics.

D) Responsibility centres are usually determined by differences in the product the firm produces.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

12

Which of the following statements relating to a budget is not true?

A) It is a detailed plan.

B) It is a management tool.

C) It provides many of the performance targets used in responsibility accounting.

D) It is prepared on an historical basis.

A) It is a detailed plan.

B) It is a management tool.

C) It provides many of the performance targets used in responsibility accounting.

D) It is prepared on an historical basis.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

13

Which statement is untrue?

A) A properly prepared budget is a motivating device.

B) An improperly prepared budget can have a negative effect on motivation.

C) Managers should be given sole responsibility for setting their own budget targets so that they are motivated to achieve these targets.

D) The budgeted level of performance should be attainable with a reasonably efficient amount of effort.

A) A properly prepared budget is a motivating device.

B) An improperly prepared budget can have a negative effect on motivation.

C) Managers should be given sole responsibility for setting their own budget targets so that they are motivated to achieve these targets.

D) The budgeted level of performance should be attainable with a reasonably efficient amount of effort.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

14

The first and last steps respectively in the developing a master budget are:

A) forecasting sales and estimating expenses.

B) preparation of the sales budget and preparation of the capital expenditure budget.

C) identifying goals and preparation of a set of budgeted financial statements.

D) identifying goals and preparation of the cash budget.

A) forecasting sales and estimating expenses.

B) preparation of the sales budget and preparation of the capital expenditure budget.

C) identifying goals and preparation of a set of budgeted financial statements.

D) identifying goals and preparation of the cash budget.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

15

How many of these are the benefits of budgeting?

Budgeting ensures future events will never catch management by surprise

Budgeting establishes organisational goals

Budgeting is a means of coordination

Budgeting provides useful work for accounting staff

A) One

B) Two

C) Three

D) Four

Budgeting ensures future events will never catch management by surprise

Budgeting establishes organisational goals

Budgeting is a means of coordination

Budgeting provides useful work for accounting staff

A) One

B) Two

C) Three

D) Four

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

16

Who should participate in the budgeting process?

A) Division heads

B) Senior management

C) All levels of management

D) Supervisors within a department

A) Division heads

B) Senior management

C) All levels of management

D) Supervisors within a department

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

17

The primary purpose of a budget is:

A) to identify which employees are doing a good job and which are doing a poor job.

B) to show how resources will be acquired and used.

C) to find the cheapest source of supplies and expenses.

D) to identify who should be promoted.

A) to identify which employees are doing a good job and which are doing a poor job.

B) to show how resources will be acquired and used.

C) to find the cheapest source of supplies and expenses.

D) to identify who should be promoted.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

18

For many companies in Australia the average profit margin could be as low as:

A) 5%.

B) 10%.

C) 12%.

D) 15%.

A) 5%.

B) 10%.

C) 12%.

D) 15%.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

19

Which statement relating to the provision of motivation as a benefit of budgeting is not true?

A) When all levels of management participate in preparing the budget it has a better chance of acceptance.

B) The budgeted level of performance should be beyond that attainable with a reasonably amount of effort, to provide employees with a challenge.

C) An improperly prepared budget may have an adverse effect on motivation.

D) To increase the chances of acceptance the budget is best approached from the bottom up.

A) When all levels of management participate in preparing the budget it has a better chance of acceptance.

B) The budgeted level of performance should be beyond that attainable with a reasonably amount of effort, to provide employees with a challenge.

C) An improperly prepared budget may have an adverse effect on motivation.

D) To increase the chances of acceptance the budget is best approached from the bottom up.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

20

Which statement concerning budgeting is correct?

A) A budget prepared by an individual is more detailed than one used by a business.

B) All budgets must be prepared in dollar values.

C) A budget is an essential step in managing a business efficiently.

D) Budgeting and performance evaluation are not closely related.

A) A budget prepared by an individual is more detailed than one used by a business.

B) All budgets must be prepared in dollar values.

C) A budget is an essential step in managing a business efficiently.

D) Budgeting and performance evaluation are not closely related.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

21

The unit purchasing requirements for a retail entity are calculated as:

A) forecast sales in units + desired ending inventory in units + beginning inventory in units.

B) forecast sales in units + desired ending inventory in units - beginning inventory in units.

C) forecast sales in units - desired ending inventory in units + beginning inventory in units.

D) forecast sales in units - desired ending inventory in units - beginning inventory in units.

A) forecast sales in units + desired ending inventory in units + beginning inventory in units.

B) forecast sales in units + desired ending inventory in units - beginning inventory in units.

C) forecast sales in units - desired ending inventory in units + beginning inventory in units.

D) forecast sales in units - desired ending inventory in units - beginning inventory in units.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

22

It is true in relation to cash budgets that:

A) they are prepared by entities that sell entirely on credit.

B) they include depreciation.

C) they are based on preparing a projected bank reconciliation.

D) they are the last budget to be prepared.

A) they are prepared by entities that sell entirely on credit.

B) they include depreciation.

C) they are based on preparing a projected bank reconciliation.

D) they are the last budget to be prepared.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

23

The following information was reported in the cash budget.

Beginning cash balance $57 000

Cash disbursements $214 000

Cash receipts $193 000

Minimum cash balance required $40 000

How much cash will the company have to borrow in order to meet its required needs?

A) $0

B) $21 000

C) $4000

D) $29 000

Beginning cash balance $57 000

Cash disbursements $214 000

Cash receipts $193 000

Minimum cash balance required $40 000

How much cash will the company have to borrow in order to meet its required needs?

A) $0

B) $21 000

C) $4000

D) $29 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

24

All of these factors can influence the reliability of the sales forecast except:

A) proposed advertising.

B) action of competitors.

C) a slow-down in the collection of cash from debtors.

D) a rise in general interest rates.

A) proposed advertising.

B) action of competitors.

C) a slow-down in the collection of cash from debtors.

D) a rise in general interest rates.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

25

Which of the following statements is not true?

A) Preparing operating budgets for service businesses is normally simpler than preparing them for retailers or manufacturers.

B) A service business does not need to prepare a cash budget.

C) GST estimates need to be included in a cash budget.

D) The emphasis in budgeting for not-for-profit organisations tends to be on cash flows and the final cash position rather than on profits, income and expenditure.

A) Preparing operating budgets for service businesses is normally simpler than preparing them for retailers or manufacturers.

B) A service business does not need to prepare a cash budget.

C) GST estimates need to be included in a cash budget.

D) The emphasis in budgeting for not-for-profit organisations tends to be on cash flows and the final cash position rather than on profits, income and expenditure.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

26

The Classy Cats Company has budgeted for sales of 100 000 units of its product for the year. Expected unit costs, based on past experience, should be $60 for direct materials, $40 for direct labour and $30 for manufacturing overhead. Assume no beginning and ending work in process inventories. Classy Cats begins the year with 40 000 finished units on hand and budgets the ending finished goods inventory at 10 000 units. Compute the budgeted production in units and dollars.

A) 70 000 units @ $100 = $7 000 000

B) 70 000 units @ $130 = $9 100 000

C) 150 000 units @ $100 = $15 000 000

D) 150 000 units @ $130 = $19 500 000

A) 70 000 units @ $100 = $7 000 000

B) 70 000 units @ $130 = $9 100 000

C) 150 000 units @ $100 = $15 000 000

D) 150 000 units @ $130 = $19 500 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

27

Which statement is true?

A) Most firms prepare cash budgets for periods of 5 years or more.

B) The bank figure in the budgeted balance sheet comes from the cash budget.

C) Budgeted retained profits is calculated as opening balance plus budgeted profit plus budgeted dividends.

D) GST can be ignored when preparing budgets.

A) Most firms prepare cash budgets for periods of 5 years or more.

B) The bank figure in the budgeted balance sheet comes from the cash budget.

C) Budgeted retained profits is calculated as opening balance plus budgeted profit plus budgeted dividends.

D) GST can be ignored when preparing budgets.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

28

Budgets that give details of the income and costs of projected activities needed to achieve satisfactory profit results are known as:

A) financial budgets.

B) master budgets.

C) operating budgets.

D) cash budgets.

A) financial budgets.

B) master budgets.

C) operating budgets.

D) cash budgets.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

29

Which of these is part of the financial set of budgets?

A) Production budget

B) Sales budget

C) Expense budget

D) Cash budget

A) Production budget

B) Sales budget

C) Expense budget

D) Cash budget

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

30

Which statement is not correct?

A) A retailer prepares a budget for purchases and then a cost of sales budget.

B) A manufacturer prepares a production budget, direct materials, direct labour and factory overhead budgets and then a cost of sales budget.

C) Both retailers and manufacturers prepare income, expense, capital expenditure and cash budgets.

D) A service provider only prepares financial budgets not operating budgets.

A) A retailer prepares a budget for purchases and then a cost of sales budget.

B) A manufacturer prepares a production budget, direct materials, direct labour and factory overhead budgets and then a cost of sales budget.

C) Both retailers and manufacturers prepare income, expense, capital expenditure and cash budgets.

D) A service provider only prepares financial budgets not operating budgets.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

31

Which of the following budgets is prepared after the cash budget?

A) Capital expenditure budget

B) Budgeted balance sheet

C) Budgeted income statement

D) Sales Budget

A) Capital expenditure budget

B) Budgeted balance sheet

C) Budgeted income statement

D) Sales Budget

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

32

Information on cash receipts would come from the:

A) sales budget.

B) direct labour budget.

C) direct materials budget.

D) capital expenditure budget.

A) sales budget.

B) direct labour budget.

C) direct materials budget.

D) capital expenditure budget.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

33

Virtually every phase of the master budget for a manufacturer is dependent on:

A) the sales forecast.

B) the capital expenditure forecast.

C) the wastage rate.

D) the production forecast.

A) the sales forecast.

B) the capital expenditure forecast.

C) the wastage rate.

D) the production forecast.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

34

For a manufacturing entity, if:

1 is the budgeted balance sheet

2 is the budgeted income statement

3 is the production budget

4 is the sales budget

5 is the cash budget

6 is the cost of sales budget;

Then the normal sequence of budget preparation is:

A) 4, 5, 6, 2, 3, 1.

B) 4, 3, 6, 2, 5, 1.

C) 4, 6, 2, 3, 5, 1.

D) 5, 2, 4, 6, 3, 1.

1 is the budgeted balance sheet

2 is the budgeted income statement

3 is the production budget

4 is the sales budget

5 is the cash budget

6 is the cost of sales budget;

Then the normal sequence of budget preparation is:

A) 4, 5, 6, 2, 3, 1.

B) 4, 3, 6, 2, 5, 1.

C) 4, 6, 2, 3, 5, 1.

D) 5, 2, 4, 6, 3, 1.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

35

Which expense varies directly with production?

A) Managers salary

B) Direct materials

C) Depreciation of equipment

D) Insurance

A) Managers salary

B) Direct materials

C) Depreciation of equipment

D) Insurance

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

36

The method which would not be used to forecast sales is:

A) extrapolation of past sales.

B) predictions by senior management.

C) statistical or mathematical techniques.

D) working out the maximum production that can be achieved.

A) extrapolation of past sales.

B) predictions by senior management.

C) statistical or mathematical techniques.

D) working out the maximum production that can be achieved.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

37

Purchases of buildings and equipment are formally planned in the:

A) selling and administrative expense budget.

B) capital expenditure budget.

C) depreciation budget.

D) budgeted balance sheet.

A) selling and administrative expense budget.

B) capital expenditure budget.

C) depreciation budget.

D) budgeted balance sheet.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

38

Which of these methods is least likely to be used to forecast sales?

A) Predictions by sales staff

B) Extrapolation of past sales

C) Field studies by market research staff

D) Predictions by production employees

A) Predictions by sales staff

B) Extrapolation of past sales

C) Field studies by market research staff

D) Predictions by production employees

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

39

A) $400

B) $2000

C) $2600

D) $3400

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

40

The budget that sets out the proposed acquisition of facilities and equipment planned for the period is the:

A) budgeted income statement.

B) capital expenditure budget.

C) purchases budget.

D) budgeted balance sheet.

A) budgeted income statement.

B) capital expenditure budget.

C) purchases budget.

D) budgeted balance sheet.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

41

Stockport Manufacturing is preparing its purchases budget for the 2nd quarter of the year. The following information is given in units.

Beginning inventory = 350

Ending inventory = 425

Sales forecast for second quarter = 950

How many units should be purchased in the second quarter?

A) 600

B) 950

C) 1025

D) 1375

Beginning inventory = 350

Ending inventory = 425

Sales forecast for second quarter = 950

How many units should be purchased in the second quarter?

A) 600

B) 950

C) 1025

D) 1375

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

42

The sales budget for Joy Time Toys for the first three months of the year is expected to be $50 000, $40 000 and $60 000 with 30% of each month's sales being on credit. Collections of accounts receivable are scheduled at 40% during the month of sale, 55% during the month following the sale with 5% uncollectable. The total budgeted cash receipts from sales for the second month will be:

A) $32 800.

B) $38 000.

C) $40 000.

D) $41 050.

A) $32 800.

B) $38 000.

C) $40 000.

D) $41 050.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

43

A) 4800.

B) 6480.

C) 7920.

D) 10 400.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

44

The technique in which budget variables are altered and the effect of the changes on the income statement and the balance sheet are recorded is known as:

A) what if analysis.

B) variable analysis.

C) spreadsheet analysis.

D) profit analysis.

A) what if analysis.

B) variable analysis.

C) spreadsheet analysis.

D) profit analysis.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

45

The budget that should be prepared before the others listed is:

A) manufacturing overhead budget.

B) cost of goods manufactured budget.

C) cash budget.

D) production budget.

A) manufacturing overhead budget.

B) cost of goods manufactured budget.

C) cash budget.

D) production budget.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

46

Which of these is not part of the control phase of budgeting?

A) Comparing actual performance with budget estimates.

B) Identifying any significant variances.

C) Deciding what action should be taken.

D) Setting goals.

A) Comparing actual performance with budget estimates.

B) Identifying any significant variances.

C) Deciding what action should be taken.

D) Setting goals.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

47

Which of these account balances is not reported on the balance sheet?

A) Cost of sales

B) Materials inventory

C) Work in progress inventory

D) Finished goods inventory

A) Cost of sales

B) Materials inventory

C) Work in progress inventory

D) Finished goods inventory

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

48

An example of a fixed factory overhead cost is:

A) indirect materials.

B) council rates and taxes.

C) direct labour.

D) light and power.

A) indirect materials.

B) council rates and taxes.

C) direct labour.

D) light and power.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

49

DigiSnaps plans to produce 65 000 units per month during 2014. Sales are projected at 55 000 for January and will increase 5% per month thereafter. There are 2000 units on hand at 1 January 2014. How many units will be on hand at 28 February 2014?

A) 15 750

B) 17 250

C) 19 250

D) 22 000

A) 15 750

B) 17 250

C) 19 250

D) 22 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

50

Budgeted direct materials purchases in units equals:

A) budgeted direct materials usage plus beginning direct materials less desired ending direct materials.

B) budgeted direct materials usage less beginning direct materials plus desired ending direct materials.

C) budgeted direct materials in stock plus beginning direct materials inventory less desired ending direct materials.

D) budgeted direct materials in stock less beginning direct materials inventory plus desired ending direct materials.

A) budgeted direct materials usage plus beginning direct materials less desired ending direct materials.

B) budgeted direct materials usage less beginning direct materials plus desired ending direct materials.

C) budgeted direct materials in stock plus beginning direct materials inventory less desired ending direct materials.

D) budgeted direct materials in stock less beginning direct materials inventory plus desired ending direct materials.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

51

A) $150

B) $1800

C) $1440

D) $2400

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

52

It is estimated that direct materials, direct labour and factory overhead for the period will total $500 000. If work in process at the start is $35 000 and estimated work in process at the end is $40 000, the cost of goods manufactured is:

A) $495 000.

B) $250 000.

C) $350 000.

D) $505 000.

A) $495 000.

B) $250 000.

C) $350 000.

D) $505 000.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

53

Which of the following is a typical example of a variable cost?

A) Sales commission

B) Depreciation

C) Rent

D) Cleaning

A) Sales commission

B) Depreciation

C) Rent

D) Cleaning

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

54

Information for Fine Line Fishing Product's cash budget is as follows.

Each unit sells for $12 and 80% of sales are on credit. Credit sales are collected as follows: 25% in the quarter of the sale and the balance in the following quarter. How many dollars of 3rd quarter sales will be collected in cash in the 4th quarter?

A) $225

B) $2160

C) $180

D) $2700

Each unit sells for $12 and 80% of sales are on credit. Credit sales are collected as follows: 25% in the quarter of the sale and the balance in the following quarter. How many dollars of 3rd quarter sales will be collected in cash in the 4th quarter?

A) $225

B) $2160

C) $180

D) $2700

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

55

Predetermined overhead rates are generally useful for all of the following purposes, except:

A) product costing.

B) estimating production levels.

C) price determination.

D) inventory valuation.

A) product costing.

B) estimating production levels.

C) price determination.

D) inventory valuation.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

56

It is not necessary in the control phase of budgeting to:

A) decide on management action.

B) compare actual performance with budget estimates.

C) provide timely information to management.

D) investigate all variances.

A) decide on management action.

B) compare actual performance with budget estimates.

C) provide timely information to management.

D) investigate all variances.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

57

If estimated direct raw materials and direct labour costs are $50 000 in total, what is the direct cost per unit if forecast production is 5000 units?

A) $10

B) $25

C) $20

D) $15

A) $10

B) $25

C) $20

D) $15

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

58

A) $185 000.

B) $200 000.

C) $215 000.

D) $235 000.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

59

If the cost object is the product, which of the following labour costs would be most likely to be classified as direct labour?

A) General manager's salary

B) Accounting staff's salaries

C) Maintenance staff's wages

D) Machine operator's wages

A) General manager's salary

B) Accounting staff's salaries

C) Maintenance staff's wages

D) Machine operator's wages

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

60

A company expects to begin the coming year with 6000 units of Product DD in finished goods inventory. It expects to sell 85 000 units of the product and end the year with 8000 units in finished goods inventory. Each unit of product DD requires 4kgs of Material X. The company expects to have 4000 kg of Material X on hand at the beginning of the coming year and wishes to end the year with 6000 kg in inventory. How many kilograms of Material X must the company purchase during the year?

A) 250 000

B) 400 000

C) 300 000

D) 350 000

A) 250 000

B) 400 000

C) 300 000

D) 350 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

61

If budgeted sales revenue is $250 000 and actual sales revenue is $230 000, and budgeted expenses are $125 000 and actual expenses are $142 000, the profit variance for the period is:

A) $37 000F.

B) $37 000U.

C) $108 000 F.

D) $108 000 U.

A) $37 000F.

B) $37 000U.

C) $108 000 F.

D) $108 000 U.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

62

A budget performance report is being prepared and will be sent to the appropriate segment manager. Which term best describes the type of costs and income that should be included in this report?

A) Unfavourable

B) Controllable

C) Administrative

D) Fixed

A) Unfavourable

B) Controllable

C) Administrative

D) Fixed

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

63

Identify the unfavourable variance.

A) Budgeted income $100 000; actual income $105 000

B) Budgeted expenses $80 000; actual expenses $85 000

C) Budgeted expenses $32 000; actual expenses $28 000

D) Budgeted loss $20 100; actual loss $17 500

A) Budgeted income $100 000; actual income $105 000

B) Budgeted expenses $80 000; actual expenses $85 000

C) Budgeted expenses $32 000; actual expenses $28 000

D) Budgeted loss $20 100; actual loss $17 500

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

64

Large favourable variances between actual and planned performance may indicate:

A) that actual expenses were higher than budgeted expenses.

B) that the firm must be operating efficiently.

C) budget income targets may need to be revised upwards in the future.

D) that actual income was too high and should be revised downwards in the future.

A) that actual expenses were higher than budgeted expenses.

B) that the firm must be operating efficiently.

C) budget income targets may need to be revised upwards in the future.

D) that actual income was too high and should be revised downwards in the future.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

65

The direct labour budget is developed from the:

A) cash budget.

B) production budget.

C) materials budget.

D) budgeted income statement.

A) cash budget.

B) production budget.

C) materials budget.

D) budgeted income statement.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 65 flashcards in this deck.