Global Business 3rd Edition by Mike Peng

Edition 3ISBN: 978-1133485933Global Business 3rd Edition by Mike Peng

Edition 3ISBN: 978-1133485933 Exercise 41

As an innovative movement to solve financing problems in the developing world, microfinance has been phenomenally successful. However, it has also attracted significant criticisms lately. What has happened?

A Global Success

Teach a man to fish, and he will eat for a lifetime. However, here is a catch: In many poor developing countries, numerous eager fishermen-also known as entrepreneurs-cannot afford a fishing pole. In 1976, Muhammad Yunus, a young economics professor who received his PhD from Vanderbilt University, lent $27 out of his own pocket to a group of poor craftsmen in his native Bangladesh. He also helped found a village-based enterprise called the Grameen Project. It never occurred to Yunus that he would inspire a global movement for entrepreneurial financing, much less that 30 years later, in 2006, he and the Grameen Bank he founded would be awarded the Nobel Peace Prize.

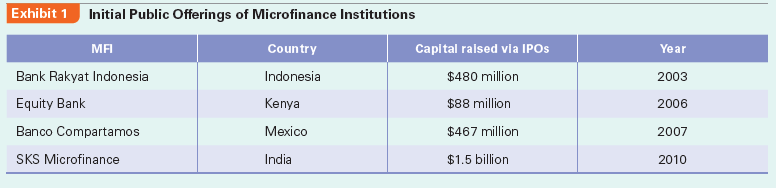

Used to buy everything from milk cows to mobile phones (to be used as pay phones by the entire village), microloans (between $50 and $300) can make a huge difference. The poor tend to have neither assets (necessary for collateral) nor credit history, making traditional loans risky. The innovative, simple solution is to lend to women. In lenders' opinion, women, on average, are more likely to use their earnings to support family needs than men, who may be more likely to indulge in drinking, gambling, or drugs. A more sophisticated solution is to organize the women in a village into a collective and lend money to the collective rather than to individuals. Overall, 84% of microloan recipients are women. While interest rates average a hefty 35%, they are still far below the rates charged by local loan sharks. By 2011, more than 7,000 microfinance institutions (MFIs) had served 120 million borrowers around the world. A number of them have successfully gone through initial public offerings (IPOs) (see Exhibit 1).

Debates and Controversies

However, as microfinance grows from periphery to mainstream, not all is rosy. Two ferocious debates have erupted recently. The first debate deals with how to view the IPOs of MFIs. The "successful" IPOs

of several MFIs have attracted criticisms that these MFIs and their new shareholders, most of whom are rich investors from the United States and Europe, have enriched themselves at the expense of very poor people at the base of the pyramid. In short, the rich have literally profited from the dirt poor. Is that right?

Second, with the onslaught of the 2008-2009 global crisis, default rates have skyrocketed. Several competitive MFIs may have dumped several microfinance loans to the same uneducated clients. In a microfinance boom, some lending practices have increasingly become competitive and reckless, similar to subprime lending in the West before the financial crisis. Should crops or ventures fail, clients thus face crushing debt loads. Recovery methods from MFIs sometimes involve intimidation. The Indian government had a list of 85 MFI "victims," who committed suicide.

In response, policymakers in some parts of India capped the interest rate at 24%, and called default borrowers to refuse to pay up. Thus, in some parts of India, nearly 80% of borrowers were in default. Because of the high costs of making and collecting payments on millions of tiny loans, MFIs' margins are razor-thin. Such massive defaults quickly pushed some MFIs to go under, and the Indian government reluctantly spent $221 million to bail them out in 2010.

Sheikh Hasina, Bangladesh's prime minister, charged MFIs with "sucking blood from the poor" and treating the people of Bangladesh as "guinea pigs." She launched an investigation into Grameen Bank's alleged questionable operations. Although as managing director of Grameen Bank, Yunus was eventually cleared of wrongdoing, microfinance-and its missionary pioneer-has suffered from a crisis of faith.

Case Discussion Questions

Using agency theory, identify the areas for improvement for the governance of certain MFIs that have been found to engage in questionable practices.

A Global Success

Teach a man to fish, and he will eat for a lifetime. However, here is a catch: In many poor developing countries, numerous eager fishermen-also known as entrepreneurs-cannot afford a fishing pole. In 1976, Muhammad Yunus, a young economics professor who received his PhD from Vanderbilt University, lent $27 out of his own pocket to a group of poor craftsmen in his native Bangladesh. He also helped found a village-based enterprise called the Grameen Project. It never occurred to Yunus that he would inspire a global movement for entrepreneurial financing, much less that 30 years later, in 2006, he and the Grameen Bank he founded would be awarded the Nobel Peace Prize.

Used to buy everything from milk cows to mobile phones (to be used as pay phones by the entire village), microloans (between $50 and $300) can make a huge difference. The poor tend to have neither assets (necessary for collateral) nor credit history, making traditional loans risky. The innovative, simple solution is to lend to women. In lenders' opinion, women, on average, are more likely to use their earnings to support family needs than men, who may be more likely to indulge in drinking, gambling, or drugs. A more sophisticated solution is to organize the women in a village into a collective and lend money to the collective rather than to individuals. Overall, 84% of microloan recipients are women. While interest rates average a hefty 35%, they are still far below the rates charged by local loan sharks. By 2011, more than 7,000 microfinance institutions (MFIs) had served 120 million borrowers around the world. A number of them have successfully gone through initial public offerings (IPOs) (see Exhibit 1).

Debates and Controversies

However, as microfinance grows from periphery to mainstream, not all is rosy. Two ferocious debates have erupted recently. The first debate deals with how to view the IPOs of MFIs. The "successful" IPOs

of several MFIs have attracted criticisms that these MFIs and their new shareholders, most of whom are rich investors from the United States and Europe, have enriched themselves at the expense of very poor people at the base of the pyramid. In short, the rich have literally profited from the dirt poor. Is that right?

Second, with the onslaught of the 2008-2009 global crisis, default rates have skyrocketed. Several competitive MFIs may have dumped several microfinance loans to the same uneducated clients. In a microfinance boom, some lending practices have increasingly become competitive and reckless, similar to subprime lending in the West before the financial crisis. Should crops or ventures fail, clients thus face crushing debt loads. Recovery methods from MFIs sometimes involve intimidation. The Indian government had a list of 85 MFI "victims," who committed suicide.

In response, policymakers in some parts of India capped the interest rate at 24%, and called default borrowers to refuse to pay up. Thus, in some parts of India, nearly 80% of borrowers were in default. Because of the high costs of making and collecting payments on millions of tiny loans, MFIs' margins are razor-thin. Such massive defaults quickly pushed some MFIs to go under, and the Indian government reluctantly spent $221 million to bail them out in 2010.

Sheikh Hasina, Bangladesh's prime minister, charged MFIs with "sucking blood from the poor" and treating the people of Bangladesh as "guinea pigs." She launched an investigation into Grameen Bank's alleged questionable operations. Although as managing director of Grameen Bank, Yunus was eventually cleared of wrongdoing, microfinance-and its missionary pioneer-has suffered from a crisis of faith.

Case Discussion Questions

Using agency theory, identify the areas for improvement for the governance of certain MFIs that have been found to engage in questionable practices.

Explanation Verified

Verified

Agency Theory:

It studies the relations...

Global Business 3rd Edition by Mike Peng

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255