Auditing and Assurance Services 9th Edition by Alvin Arens,Mark Beasley,Randy Elder

Edition 9ISBN: 978-0130459206Auditing and Assurance Services 9th Edition by Alvin Arens,Mark Beasley,Randy Elder

Edition 9ISBN: 978-0130459206 Exercise 22

To support financial statement assertions, an auditor develops specific audit procedures to satisfy or accomplish each assertion.

Required:

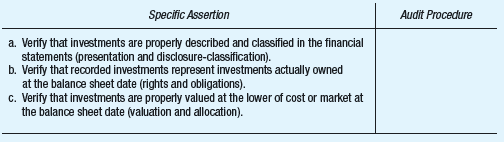

Items (a) through (c) represent assertions for investments. Select the most appropriate procedure from the following list and enter the number in the appropriate place on the grid. (An audit procedure may be selected once or not at all.)

Audit Procedure:

1. Vouch opening balances in the subsidiary ledgers to the prior year's audit working papers.

2. Determine that employees who are authorized to sell investments do not have access to cash.

3. Examine supporting documents for a sample of investment transactions to verify that prenumbered documents are used.

4. Determine that any impairments in the price of investments have been properly recorded.

5. Verify that transfers from the current to the noncurrent investment portfolio have been properly recorded.

6. Obtain positive confirmations as of the balance sheet date of investments held by independent custodians.

7. Trace investment transactions to minutes of board of directors' meetings to determine that transactions were properly authorized.

(AICPA, adapted)

Required:

Items (a) through (c) represent assertions for investments. Select the most appropriate procedure from the following list and enter the number in the appropriate place on the grid. (An audit procedure may be selected once or not at all.)

Audit Procedure:

1. Vouch opening balances in the subsidiary ledgers to the prior year's audit working papers.

2. Determine that employees who are authorized to sell investments do not have access to cash.

3. Examine supporting documents for a sample of investment transactions to verify that prenumbered documents are used.

4. Determine that any impairments in the price of investments have been properly recorded.

5. Verify that transfers from the current to the noncurrent investment portfolio have been properly recorded.

6. Obtain positive confirmations as of the balance sheet date of investments held by independent custodians.

7. Trace investment transactions to minutes of board of directors' meetings to determine that transactions were properly authorized.

(AICPA, adapted)

Explanation Verified

Verified

Audit Procedure

Audit procedure is a pr...

Auditing and Assurance Services 9th Edition by Alvin Arens,Mark Beasley,Randy Elder

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255