Fundamentals of Financial Accounting 4th Edition by Fred Phillips,Robert Libby,Patricia Libby

Edition 4ISBN: 978-0078025372Fundamentals of Financial Accounting 4th Edition by Fred Phillips,Robert Libby,Patricia Libby

Edition 4ISBN: 978-0078025372 Exercise 1

Preparing an Income Statement, Statement of Retained Earnings, and Balance Sheet

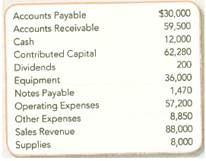

Assume that you are the president of Nuclear Company. At the end of the first year of operations (December 31, 2012), the following financial data for the company are available:

Required:

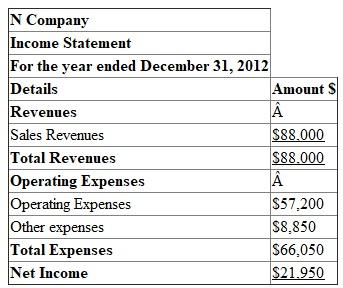

1. Prepare an income statement for the year ended December 31, 2012

TIP: Begin by classifying each account as asset, liability, stockholders' equity, revenue, or expense. Each account is reported on only one financial statement.

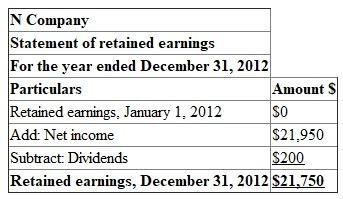

2. Prepare a statement of retained earnings for the year ended December 31, 2012

TIP: Because this is the first year of operations, the beginning balance in Retained Earnings will be zero.

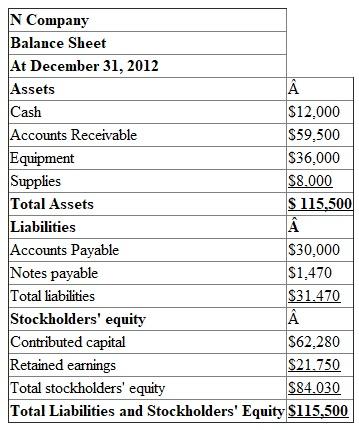

3. Prepare a balance sheet at December 31, 2012

TIP: The balance sheet includes the ending balance from the statement of retained earnings.

Assume that you are the president of Nuclear Company. At the end of the first year of operations (December 31, 2012), the following financial data for the company are available:

Required:

1. Prepare an income statement for the year ended December 31, 2012

TIP: Begin by classifying each account as asset, liability, stockholders' equity, revenue, or expense. Each account is reported on only one financial statement.

2. Prepare a statement of retained earnings for the year ended December 31, 2012

TIP: Because this is the first year of operations, the beginning balance in Retained Earnings will be zero.

3. Prepare a balance sheet at December 31, 2012

TIP: The balance sheet includes the ending balance from the statement of retained earnings.

Explanation Verified

Verified

1.

Income Statement:

The first financial statement prepared is the income statement. The income statement reports the net amount that a business earned (net income) over a period of time by subtracting the costs of running the business (expenses) from the total amount earned (revenues).

Prepare an income statement for the year ended December 31, 2012:

Prepare an income statement for the year ended December 31, 2012:

2.

2.

Prepare a statement of Retained earnings for the year ended December 31, 2012:

The statement of retained earnings explains changes in the Retained Earnings account over a period of time by considering increases (from net income) and decreases (from dividends to stockholders).

Beginning retained earnings plus net income minus dividends equals to retained earnings ending balance.

3.

3.

Balance sheet's purpose is to report the amount of a business's assets, liabilities, and stockholders' equity at a specific point in time.

Prepare a Balance sheet at December 31, 2012:

The basic accounting equation is as follows:

Resources owned by the company called assets.

Resources owned by the company called assets.

Resources owed to creditors, and to stockholders are called liabilities and stockholders' equity.

Income Statement:

The first financial statement prepared is the income statement. The income statement reports the net amount that a business earned (net income) over a period of time by subtracting the costs of running the business (expenses) from the total amount earned (revenues).

Prepare an income statement for the year ended December 31, 2012: 2. Prepare a statement of Retained earnings for the year ended December 31, 2012:

The statement of retained earnings explains changes in the Retained Earnings account over a period of time by considering increases (from net income) and decreases (from dividends to stockholders).

Beginning retained earnings plus net income minus dividends equals to retained earnings ending balance.

3. Balance sheet's purpose is to report the amount of a business's assets, liabilities, and stockholders' equity at a specific point in time.

Prepare a Balance sheet at December 31, 2012:

The basic accounting equation is as follows:

Resources owned by the company called assets.Resources owed to creditors, and to stockholders are called liabilities and stockholders' equity.

Fundamentals of Financial Accounting 4th Edition by Fred Phillips,Robert Libby,Patricia Libby

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255