Introduction to Econometrics 3rd Edition by James Stock, Mark Watson

Edition 3ISBN: 978-9352863501Introduction to Econometrics 3rd Edition by James Stock, Mark Watson

Edition 3ISBN: 978-9352863501 Exercise 14

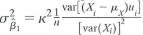

Suppose that Y i = 0 + 1 X i + ku i , where k is a non-zero constant and ( Y i , X i ) satisfy the three least squares assumptions. Show that the large sample variance of

1 is given by

1 is given by

.

.

1 is given by .Explanation Verified

Verified

Given that population regression is:

![]() ...

...

Introduction to Econometrics 3rd Edition by James Stock, Mark Watson

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255