Exam 28: The Labor Market in the Macroeconomy

Exam 1: The Scope and Method of Economics238 Questions

Exam 2: The Economic Problem: Scarcity and Choice220 Questions

Exam 3: Demand, Supply, and Market Equilibrium298 Questions

Exam 4: Demand and Supply Applications173 Questions

Exam 5: Elasticity189 Questions

Exam 6: Household Behavior and Consumer Choice273 Questions

Exam 7: The Production Process: the Behavior of Profit-Maximizing Firms273 Questions

Exam 8: Short-Run Costs and Output Decisions387 Questions

Exam 9: Long-Run Costs and Output Decisions362 Questions

Exam 10: Input Demand: The Labor and Land Markets198 Questions

Exam 11: Input Demand: The Capital Market and the Investment Decision230 Questions

Exam 12: General Equilibrium and the Efficiency of Perfect Competition202 Questions

Exam 13: Monopoly and Antitrust Policy396 Questions

Exam 14: Oligopoly217 Questions

Exam 15: Monopolistic Competition235 Questions

Exam 16: Externalities, Public Goods, and Common Resources275 Questions

Exam 17: Uncertainty and Asymmetric Information132 Questions

Exam 18: Income Distribution and Poverty197 Questions

Exam 19: Public Finance: The Economics of Taxation281 Questions

Exam 20: Introduction to Macroeconomics241 Questions

Exam 21: Measuring National Output and National Income292 Questions

Exam 22: Unemployment, Inflation, and Long-Run Growth297 Questions

Exam 23: Aggregate Expenditure and Equilibrium Output355 Questions

Exam 24: The Government and Fiscal Policy360 Questions

Exam 25: Money, the Federal Reserve, and the Interest Rate357 Questions

Exam 26: The Determination of Aggregate Output, the Price Level, and the Interest Rate243 Questions

Exam 27: Policy Effects and Cost Shocks in the Asad Model200 Questions

Exam 28: The Labor Market in the Macroeconomy287 Questions

Exam 29: Financial Crises, Stabilization, and Deficits260 Questions

Exam 30: Household and Firm Behavior in the Macroeconomy: a Further Look364 Questions

Exam 31: Long-Run Growth196 Questions

Exam 32: Alternative Views in Macroeconomics294 Questions

Exam 33: International Trade, Comparative Advantage, and Protectionism289 Questions

Exam 34: Open-Economy Macroeconomics: the Balance of Payments and Exchange Rates308 Questions

Exam 35: Economic Growth in Developing Economies133 Questions

Exam 36: Critical Thinking About Research105 Questions

Select questions type

To be unemployed, a person must be without a job and actively looking for work.

(True/False)

4.9/5  (39)

(39)

The classical view of the labor market is basically consistent with the assumption of a vertical (or almost vertical) ________ curve.

(Multiple Choice)

4.8/5 (33)

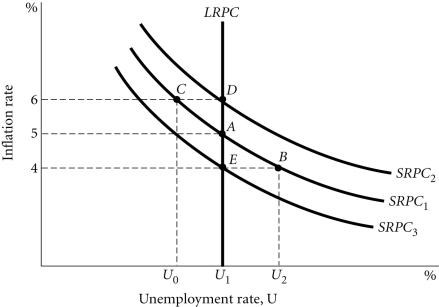

Refer to the information provided in Figure 28.7 below to answer the question(s) that follow.  Figure 28.7

-Refer to Figure 28.7. The unemployment rate at U1

Figure 28.7

-Refer to Figure 28.7. The unemployment rate at U1

(Multiple Choice)

4.7/5 (45)

In the classical view of the labor market, it is implied that unemployment does not exist.

(True/False)

4.9/5 (40)

If the minimum wage is set above the market clearing wage, wages will be "sticky" in the downward direction.

(True/False)

4.9/5 (35)

Refer to the information provided in Figure 28.7 below to answer the question(s) that follow. Figure 28.7

-Refer to Figure 28.7. Suppose the economy is initially at Point A. A contractionary fiscal policy moves the economy to Point ________ in the short run.

(Multiple Choice)

4.8/5 (44)

According to the classical theory, a contractionary monetary policy ________ the price level and ________ output in the long run.

(Multiple Choice)

4.9/5 (41)

If aggregate supply changes when aggregate demand is stable, then the Phillips curve is negatively sloped.

(True/False)

4.8/5 (34)

What sequence of events results from an increase in aggregate demand?

(Multiple Choice)

4.8/5 (34)

Frito Lay experienced a 20% drop in its sales. Even though the demand for its product decreased, Frito Lay did not cut the wages of its nonunionized workers. This is an example of

(Multiple Choice)

4.8/5 (33)

If unemployment is below the natural rate of unemployment, then output is below potential output.

(True/False)

4.9/5 (32)

A vertical aggregate supply curve implies a vertical Phillips curve.

(True/False)

4.8/5 (38)

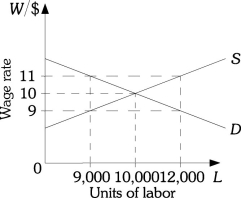

Refer to the information provided in Figure 28.2 below to answer the question(s) that follow.  Figure 28.2

-Refer to Figure 28.2. If this firm pays the efficient wage of $9

Figure 28.2

-Refer to Figure 28.2. If this firm pays the efficient wage of $9

(Multiple Choice)

4.8/5 (36)

Those who believe that the wage rate does not adjust quickly to clear the labor market are likely to believe that the aggregate supply curve is vertical.

(True/False)

4.7/5 (41)

Classical economists believe that economic policies are ineffective because they don't affect aggregate demand in the economy.

(True/False)

4.9/5 (34)

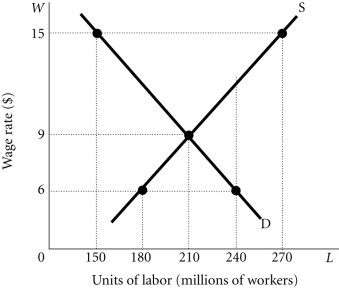

Refer to the information provided in Figure 28.1 below to answer the question(s) that follow.  Figure 28.1

-Refer to Figure 28.1. If the productivity of workers decreases, the equilibrium wage rate

Figure 28.1

-Refer to Figure 28.1. If the productivity of workers decreases, the equilibrium wage rate

(Multiple Choice)

4.8/5 (32)

Classical economists believe that when the aggregate supply curve is horizontal, monetary policy and fiscal policy will have no effect on real output.

(True/False)

4.8/5 (38)

The downward rigidity of wages as an explanation for the existence of unemployment is known as

(Multiple Choice)

4.9/5 (34)

If aggregate supply decreases and aggregate demand remains unchanged

(Multiple Choice)

4.9/5 (45)

In the long run, the Phillips curve will be ________ at the natural rate of unemployment if the long-run aggregate supply curve is vertical at potential output.

(Multiple Choice)

4.9/5 (39)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)