Exam 9: Firms in a Competitive Market

Exam 1: Five Foundations of Economics174 Questions

Exam 2: Model Building and Gains From Trade174 Questions

Exam 3: The Market at Work: Supply and Demand160 Questions

Exam 4: Elasticity170 Questions

Exam 5: Market Outcomes and Tax Incidence175 Questions

Exam 6: Price Controls156 Questions

Exam 7: Market Inefficiencies: Externalities and Public Goods171 Questions

Exam 8: Business Costs and Production175 Questions

Exam 9: Firms in a Competitive Market158 Questions

Exam 10: Understanding Monopoly175 Questions

Exam 11: Price Discrimination175 Questions

Exam 12: Monopolistic Competition and Advertising173 Questions

Exam 13: Oligopoly and Strategic Behavior158 Questions

Exam 14: The Demand and Supply of Resources154 Questions

Exam 15: Income,inequality,and Poverty182 Questions

Exam 16: Consumer Choice144 Questions

Exam 17: Behavioral Economics and Risk Taking145 Questions

Exam 18: Health Insurance and Health Care172 Questions

Exam 19: Introduction to Macroeconomics and Gross Domestic Product174 Questions

Exam 20: Unemployment171 Questions

Exam 21: The Price Level and Inflation174 Questions

Exam 22: Savings,interest Rates,and the Market for Loanable Funds175 Questions

Exam 23: Financial Markets and Securities169 Questions

Exam 24: Economic Growth and the Wealth of Nations166 Questions

Exam 25: Growth Theory166 Questions

Exam 26: The Aggregate Demandaggregate Supply Model147 Questions

Exam 27: The Great Recession, the Great Depression, and Great Macroeconomic Debates167 Questions

Exam 28: Federal Budgets: the Tools of Fiscal Policy174 Questions

Exam 29: Fiscal Policy168 Questions

Exam 30: Money and the Federal Reserve174 Questions

Exam 31: Monetary Policy158 Questions

Exam 32: International Trade159 Questions

Exam 33: International Finance159 Questions

Select questions type

You can tell a firm is operating in a market that is in long-run competitive equilibrium if

(Multiple Choice)

4.8/5  (32)

(32)

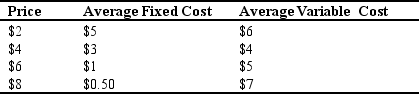

Refer to the accompanying table.A firm participating in a competitive market with these costs would break even if the price is

(Multiple Choice)

4.8/5 (37)

If the short-run supply curve and the demand curve intersect below the long-run supply curve,firms will experience ________ economic profits,meaning the price is ________ the minimum point on the average total cost curve.

(Multiple Choice)

4.8/5 (35)

The perfectly competitive firm's short-run supply curve is the

(Multiple Choice)

4.9/5 (29)

In a competitive market,if one firm raises its price relative to the other firms in the market,consumers are willing to go to another firm because

(Multiple Choice)

4.9/5 (42)

If firms in a competitive market are incurring economic losses,we would expect firms to ________ the market,causing the ________ curve to shift to the ________.

(Multiple Choice)

4.8/5 (33)

Use the following scenario to answer the following questions:

Lenora and Uma own a dog-grooming business in upstate New York,called Pawkeepsie Groomers.There are many buyers and many sellers in the dog-grooming service market.Pawkeepsie Groomers experiences normal cost curves,with the marginal cost (MC)curve crossing average variable cost (AVC)at $14 and average total cost (ATC)at $22.

-Pawkeepsie Groomers will make positive economic profits if the market price is

(Multiple Choice)

4.9/5 (41)

A company produces at an output level where marginal revenue is equal to marginal cost and has the following revenue and cost levels: Marginal cost curve intersects the average variable cost curve at $140.

Marginal cost curve intersects the average total cost curve at $150.

Marginal cost curve intersects the marginal revenue curve at $200.

What would you suggest this firm should do in the short run?

(Multiple Choice)

4.8/5 (45)

Use the following scenario to answer the following questions:

Carmela's Churros is a perfectly competitive firm that sells desserts in Houston,Texas.Carmela's Churros currently is taking in $40,000 in revenues,and has $15,000 in explicit costs and $25,000 in implicit costs.

-Carmela's Churros' accounting profits are

(Multiple Choice)

4.8/5 (37)

Which of the following is the closest example of a perfectly competitive market?

(Multiple Choice)

4.8/5 (35)

It's easy to determine if a firm is making long-run production decisions by looking at its cost structure because,in the long run,a firm does NOT have any ________ costs.

(Multiple Choice)

4.8/5 (35)

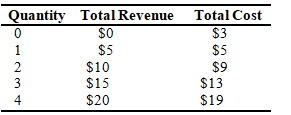

The accompanying table represents the quantity produced, the total revenue, and the total cost of a firm operating in a perfectly competitive market. Refer to this table to answer the following questions.  -Assuming that all firms have the same cost structure,the price is

-Assuming that all firms have the same cost structure,the price is

(Multiple Choice)

4.8/5 (35)

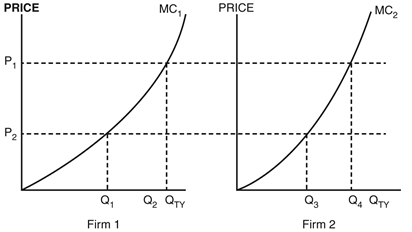

Refer to the following figure to answer the following questions.  -Firm 1 and firm 2 are the sole producers in the industry.At price P1,the industry's total quantity supplied is

-Firm 1 and firm 2 are the sole producers in the industry.At price P1,the industry's total quantity supplied is

(Multiple Choice)

4.8/5 (35)

If Kang's Knick-Knacks is a perfectly competitive firm and is making zero economic profits,

(Multiple Choice)

4.9/5 (47)

In its simplest form,the long-run market supply curve is a(n)

(Multiple Choice)

4.9/5 (34)

When firms exit a market,the ________-run market supply curve shifts ________,causing individual firms' profits to ________.

(Multiple Choice)

4.9/5 (39)

If the market price is $15 and marginal cost is represented by the equation 2 * Q,where Q is in thousands of units,what is the profit-maximizing quantity?

(Multiple Choice)

4.8/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)