Exam 16: Us Taxation of Foreign-Related Transactions

Exam 1: Tax Research107 Questions

Exam 2: Corporate Formations and Capital Structure120 Questions

Exam 3: The Corporate Income Tax116 Questions

Exam 4: Corporate Nonliquidating Distributions113 Questions

Exam 5: Other Corporate Tax Levies59 Questions

Exam 6: Corporate Liquidating Distributions103 Questions

Exam 7: Corporate Acquisitions and Reorganizations104 Questions

Exam 8: Consolidated Tax Returns90 Questions

Exam 9: Partnership Formation and Operation115 Questions

Exam 10: Special Partnership Issues107 Questions

Exam 11: S Corporations103 Questions

Exam 12: The Gift Tax105 Questions

Exam 13: The Estate Tax107 Questions

Exam 14: Income Taxation of Trusts and Estates105 Questions

Exam 15: Administrative Procedures105 Questions

Exam 16: Us Taxation of Foreign-Related Transactions86 Questions

Select questions type

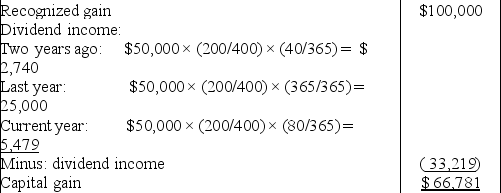

Domestic corporation B owns 200 of the 400 outstanding shares of foreign corporation K's stock. U.S. citizen R owns the remaining K stock. The domestic corporation held the stock for 40 days two years ago, 365 days last year, and 80 days this year. None of K's income is Subpart F income. The foreign corporation has E&P of $50,000 for each of the three years in question. None of the years is a leap year. On the 80th day of the current year, the stock is sold by B to R in a transaction in which a $100,000 gain is recognized by B. What part of B's gain is capital gain?

Free

(Essay)

4.8/5  (45)

(45)

Correct Answer: Verified

Verified

A nonresident alien can elect to be considered a resident alien if the nonresident alien is married to a U.S. citizen or a resident alien on the last day of the tax year and both spouses consent.

Free

(True/False)

4.7/5 (37)

Correct Answer:Verified

True

Identify which of the following statements is true.

Free

(Multiple Choice)

4.9/5 (32)

Correct Answer:Verified

D

What are the carryback and carryforward periods for the foreign tax credit?

(Multiple Choice)

4.8/5 (42)

A U.S. citizen accrued $120,000 of creditable foreign taxes last year. The citizen's foreign tax credit limitation for last year is $90,000 (only a single limitation need be calculated). The excess foreign tax credit limitation for the year preceding the year in which the excess foreign taxes were incurred is $2,000. A similar $2,000 excess foreign tax credit limitation position is expected in each of the next 10 years. What portion of the excess foreign taxes can be expected to be noncreditable because of the foreign tax credit limitation?

(Multiple Choice)

4.9/5 (40)

Which of the following characteristics is not used by the U.S. government to determine the tax treatment accorded foreign-related transactions?

(Multiple Choice)

4.9/5 (27)

A foreign corporation with a single class of stock is owned equally by Jericho Corporation, a U.S. corporation, and Joshua, a nonresident alien. Joshua owns no Alpha Corporation stock. Is the foreign corporation a controlled foreign corporation (CFC)?

(Essay)

4.8/5 (40)

If foreign taxes on foreign income exceed U.S. taxes on foreign income, the excess foreign taxes are credited against U.S. taxes in the current year.

(True/False)

4.9/5 (48)

Describe the financial statement implications of the foreign tax credit and a foreign subsidiary.

(Essay)

4.7/5 (38)

U.S. citizens, resident aliens, and domestic corporations are taxed by the U.S. government on their worldwide income at regular U.S. tax rates.

(True/False)

4.9/5 (41)

Darlene, a U.S. citizen, has foreign-earned income of $150,000 and incurs $33,750 of foreign-earned income taxes. How much of Darlene's foreign income taxes are noncreditable?

(Essay)

4.7/5 (33)

Zeta Corporation, incorporated in Country Z, is 100% owned by Zelda Corporation, a U.S. corporation. Zelda purchases some machines from an unrelated corporation, for use in Country A. The portion of the sales contract covering installation and maintenance of the machines is assigned by Zelda to Zeta. Zeta is to be paid for these services by Zelda. Does this qualify as foreign base company services income?

(Essay)

4.9/5 (35)

Income derived from the sale of merchandise inventory (i.e., final goods purchased for resale) are sourced in the country where the sale occurs.

(True/False)

4.8/5 (35)

A controlled foreign corporation (CFC) is incorporated in Country B, and is 100% owned by American Manufacturing Corporation. It purchases raw materials from its U.S. parent corporation, manufactures widgets, and sells 70% of the widgets to unrelated purchasers in Country A and 30% to unrelated purchasers in Country B. All widgets will be used in the countries in which they are purchased. The sales produce $100,000 of taxable income. The foreign-based company sales income reportable by American Manufacturing Corporation under the Subpart F rules is

(Multiple Choice)

5.0/5 (30)

Karen, a U.S. citizen, earns $40,000 of taxable income from U.S. sources, $20,000 in taxable wages from Country A and $20,000 in taxable interest from Country B. The U.S. tax rate is 21%. The tax on Country A income is $8,000, and Country B charges no tax on the interest income. Assuming only a single basket is required, Karen's foreign tax credit that can be claimed is

(Multiple Choice)

4.9/5 (34)

Alan, a U.S. citizen, works in Germany and earns $70,000, paying $20,000 in German taxes. His U.S. income is $40,000 and he pays $8,000 in U.S. taxes. His U.S. taxes on his worldwide income are $22,500. What is Alan's foreign tax credit? Assume he does not qualify for the foreign-earned income exclusion.

(Multiple Choice)

4.8/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)