Exam 23: Aggregate Expenditure and Output in the Short Run

Exam 1: Economics: Foundations and Models459 Questions

Exam 2: Trade-Offs, Comparative Advantage, and the Market System492 Questions

Exam 3: Where Prices Come From: the Interaction of Demand and Supply476 Questions

Exam 4: Economic Efficiency, Government Price Setting, and Taxes420 Questions

Exam 5: Externalities, Environmental Policy, and Public Goods262 Questions

Exam 6: Elasticity: the Responsiveness of Demand and Supply293 Questions

Exam 7: The Economics of Health Care337 Questions

Exam 8: Firms, the Stock Market, and Corporate Governance512 Questions

Exam 9: Comparative Advantage and the Gains From International Trade377 Questions

Exam 10: Consumer Choice and Behavioral Economics304 Questions

Exam 11: Technology, Production, and Costs326 Questions

Exam 12: Firms in Perfectly Competitive Markets296 Questions

Exam 13: Monopolistic Competition: the Competitive Model in a More Realistic Setting272 Questions

Exam 14: Oligopoly: Firms in Less Competitive Markets256 Questions

Exam 15: Monopoly and Antitrust Policy279 Questions

Exam 16: Pricing Strategy258 Questions

Exam 17: The Markets for Labor and Other Factors of Production279 Questions

Exam 18: Public Choice, Taxes, and the Distribution of Income258 Questions

Exam 19: Gdp: Measuring Total Production and Income260 Questions

Exam 20: Unemployment and Inflation290 Questions

Exam 21: Economic Growth, the Financial System, and Business Cycles251 Questions

Exam 22: Long-Run Economic Growth: Sources and Policies261 Questions

Exam 23: Aggregate Expenditure and Output in the Short Run305 Questions

Exam 24: Aggregate Demand and Aggregate Supply Analysis286 Questions

Exam 25: Money, Banks, and the Federal Reserve System278 Questions

Exam 26: Monetary Policy280 Questions

Exam 27: Fiscal Policy313 Questions

Exam 28: Inflation, Unemployment, and Federal Reserve Policy257 Questions

Exam 29: Macroeconomics in an Open Economy277 Questions

Exam 30: The International Financial System258 Questions

Select questions type

________ consumption is consumption that depends upon the level of GDP and ________ consumption is consumption that does not depend upon the level of GDP.

(Multiple Choice)

4.9/5  (34)

(34)

An increase in the price level in the United States will reduce U.S. imports and increase U.S. exports.

(True/False)

4.9/5 (40)

Firms in a small economy anticipated that inventories would grow over the past year by $750,000, and over that year, inventories grew by exactly $750,000. This implies that

(Multiple Choice)

4.8/5 (40)

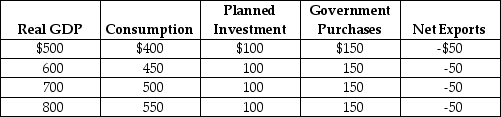

Table 23-15

-Refer to Table 23-15. Using the table above, answer the following questions. The numbers in the table are in billions of dollars.

a. What is the equilibrium level of real GDP?

b. What is the MPC?

c. If investment spending declines by $10 billion, what will happen to equilibrium GDP?

-Refer to Table 23-15. Using the table above, answer the following questions. The numbers in the table are in billions of dollars.

a. What is the equilibrium level of real GDP?

b. What is the MPC?

c. If investment spending declines by $10 billion, what will happen to equilibrium GDP?

(Essay)

4.8/5 (41)

If aggregate expenditure is less than GDP, then inventories rise and GDP falls.

(True/False)

4.7/5 (30)

Actual investment spending includes spending by consumers on

(Multiple Choice)

4.7/5 (35)

On the 45 degree-line diagram, the 45 degree line shows points where real aggregate expenditure equals

(Multiple Choice)

4.7/5 (34)

If economists forecast a decrease in aggregate expenditure, which of the following is likely to occur?

(Multiple Choice)

4.8/5 (41)

What is the difference between aggregate expenditure and aggregate demand?

(Essay)

4.8/5 (30)

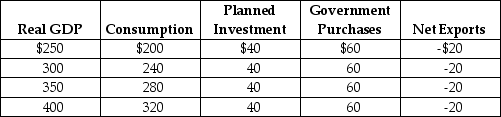

Table 23-13

-Refer to Table 23-13. Using the table above, answer the following questions. The numbers in the table are in billions of dollars.

a. What is the equilibrium level of real GDP?

b. What is the MPC?

c. If investment spending declines by $50 billion, what will happen to equilibrium GDP?

-Refer to Table 23-13. Using the table above, answer the following questions. The numbers in the table are in billions of dollars.

a. What is the equilibrium level of real GDP?

b. What is the MPC?

c. If investment spending declines by $50 billion, what will happen to equilibrium GDP?

(Essay)

4.8/5 (32)

What are the five main determinants of consumption spending? Which of these is the most important?

(Essay)

4.8/5 (32)

If the consumption function is defined as C = 7,250 + 0.8Y, what is the value of the multiplier?

(Multiple Choice)

4.9/5 (38)

If planned aggregate expenditure equals GDP, the economy is in macroeconomic equilibrium.

(True/False)

4.9/5 (37)

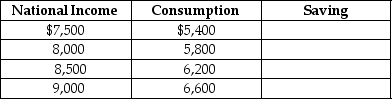

Table 23-5

Answer: When taxes are zero, saving is the difference between national income and consumption:

Saving = national income - consumption.

S = Y - C

Using the table:

Answer: When taxes are zero, saving is the difference between national income and consumption:

Saving = national income - consumption.

S = Y - C

Using the table:

Diff: 1 Page Ref: 784-786/400-402

Topic: Income, Consumption, and Saving

*: Recurring

Learning Outcome: Macro-2: Explain the relationship between expenditure and income

AACSB: Analytical thinking

-Given Table 23-6 below, fill in the values for saving. Assume taxes = $800.

Diff: 1 Page Ref: 784-786/400-402

Topic: Income, Consumption, and Saving

*: Recurring

Learning Outcome: Macro-2: Explain the relationship between expenditure and income

AACSB: Analytical thinking

-Given Table 23-6 below, fill in the values for saving. Assume taxes = $800.

(Essay)

4.9/5 (30)

An increase in the price level ________ real wealth, which causes consumption to ________.

(Multiple Choice)

4.8/5 (35)

The recession of 2007-2009 resulted in falling revenues and large layoffs for a vast number of companies. By 2017, unemployment ________ and spending ________ in the economy.

(Multiple Choice)

4.9/5 (41)

Discuss the leading causes of the Great Depression. Use the 45-degree line diagram to show how they caused a decline in GDP.

(Essay)

4.7/5 (24)

If firms are more pessimistic and believe that future profits will fall and remain weak for the next few years, then

(Multiple Choice)

4.9/5 (42)

Which of the following is not one of the four main categories of spending identified by John Maynard Keynes?

(Multiple Choice)

4.9/5 (32)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)