Exam 19: Gdp: Measuring Total Production and Income

Exam 1: Economics: Foundations and Models459 Questions

Exam 2: Trade-Offs, Comparative Advantage, and the Market System492 Questions

Exam 3: Where Prices Come From: the Interaction of Demand and Supply476 Questions

Exam 4: Economic Efficiency, Government Price Setting, and Taxes420 Questions

Exam 5: Externalities, Environmental Policy, and Public Goods262 Questions

Exam 6: Elasticity: the Responsiveness of Demand and Supply293 Questions

Exam 7: The Economics of Health Care337 Questions

Exam 8: Firms, the Stock Market, and Corporate Governance512 Questions

Exam 9: Comparative Advantage and the Gains From International Trade377 Questions

Exam 10: Consumer Choice and Behavioral Economics304 Questions

Exam 11: Technology, Production, and Costs326 Questions

Exam 12: Firms in Perfectly Competitive Markets296 Questions

Exam 13: Monopolistic Competition: the Competitive Model in a More Realistic Setting272 Questions

Exam 14: Oligopoly: Firms in Less Competitive Markets256 Questions

Exam 15: Monopoly and Antitrust Policy279 Questions

Exam 16: Pricing Strategy258 Questions

Exam 17: The Markets for Labor and Other Factors of Production279 Questions

Exam 18: Public Choice, Taxes, and the Distribution of Income258 Questions

Exam 19: Gdp: Measuring Total Production and Income260 Questions

Exam 20: Unemployment and Inflation290 Questions

Exam 21: Economic Growth, the Financial System, and Business Cycles251 Questions

Exam 22: Long-Run Economic Growth: Sources and Policies261 Questions

Exam 23: Aggregate Expenditure and Output in the Short Run305 Questions

Exam 24: Aggregate Demand and Aggregate Supply Analysis286 Questions

Exam 25: Money, Banks, and the Federal Reserve System278 Questions

Exam 26: Monetary Policy280 Questions

Exam 27: Fiscal Policy313 Questions

Exam 28: Inflation, Unemployment, and Federal Reserve Policy257 Questions

Exam 29: Macroeconomics in an Open Economy277 Questions

Exam 30: The International Financial System258 Questions

Select questions type

Table 19-18

A very simple economy produces three goods: cameras, legal services, and books. The quantities produced and their corresponding prices for 2013 and 2018 are shown in the table above.

-Refer to Table 19-18. What is real GDP in 2018, using 2013 as the base year?

A very simple economy produces three goods: cameras, legal services, and books. The quantities produced and their corresponding prices for 2013 and 2018 are shown in the table above.

-Refer to Table 19-18. What is real GDP in 2018, using 2013 as the base year?

(Multiple Choice)

4.8/5  (37)

(37)

In calculating gross domestic product, the Bureau of Economic Analysis uses the sum of the market value of final goods and services produced. This means that the BEA

(Multiple Choice)

4.9/5 (39)

In the term "real GDP," what does "GDP" stand for and what does it measure? What does "real" indicate?

(Essay)

4.9/5 (42)

Table 19-11

Consider the following data for Tyrovia, a country that produces only two products: guns and butter.

-Refer to Table 19-11. Real GDP for Tyrovia for 2018 using 2009 as the base year equals

Consider the following data for Tyrovia, a country that produces only two products: guns and butter.

-Refer to Table 19-11. Real GDP for Tyrovia for 2018 using 2009 as the base year equals

(Multiple Choice)

4.9/5 (38)

An increase in national income could by caused by which of the following?

(Multiple Choice)

4.8/5 (37)

The output of Mexican citizens who work in Texas would be included in the

(Multiple Choice)

4.8/5 (38)

The values of real GDP and real GNP are almost the same for the United States.

(True/False)

4.9/5 (37)

Which of the following could cause nominal GDP to increase next year, but real GDP to decrease?

(Multiple Choice)

4.8/5 (32)

Table 19-5

Consider the table above showing three stages of production of an automobile.

-Refer to Scenario 19-1. The value added of CANOES-R-US for each canoe equals

Consider the table above showing three stages of production of an automobile.

-Refer to Scenario 19-1. The value added of CANOES-R-US for each canoe equals

(Multiple Choice)

4.9/5 (31)

If Gladys sells her 2003 Jeep Cherokee for $3,500 in 2018, the sale of her car contributes $3,500 to 2018 GDP.

(True/False)

4.7/5 (43)

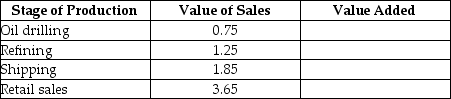

Table 19-10

a. What is the value added by each stage of production?

b. What is the total value added?

For simplicity, you can ignore the cost of the inputs for oil drilling.

Answer:

a. What is the value added by each stage of production?

b. What is the total value added?

For simplicity, you can ignore the cost of the inputs for oil drilling.

Answer:

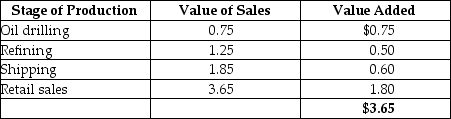

a. The value added is the difference between the price the firm sells a good for and the price it paid other firms for the intermediate good. The firm that does the oil drilling sells the gallon of oil to the refinery for $0.75. Since we are assuming no other input costs for simplicity, the value added by the drilling firm is $0.75. The refinery processes the oil and then sells it to the transport company for $1.25. The refinery's value added is $0.50. The transport company sells the oil to the retail company for $1.85. The transport company's value added is $1.85 - $1.25 = $0.60. Finally, the retail gas station sells the gallon of gas for $3.65. The value added by the retail station is $1.80.

b. The total value added is found by summing the value added by each firm involved the production of the gallon of gas. The retail price is the same at this total of value added.

Diff: 2 Page Ref: 646/262

Topic: Measuring GDP by the Value Added Method

*: Recurring

Learning Outcome: Macro-3: Identify and interpret key macroeconomic measures

AACSB: Analytical thinking

19.2 Does GDP Measure What We Want It to Measure?

-The Philippines and Vietnam have roughly the same size population. Suppose the GDP of the Philippines is $1,000 billion and the GDP of Vietnam is $10,000 billion. You should conclude

a. The value added is the difference between the price the firm sells a good for and the price it paid other firms for the intermediate good. The firm that does the oil drilling sells the gallon of oil to the refinery for $0.75. Since we are assuming no other input costs for simplicity, the value added by the drilling firm is $0.75. The refinery processes the oil and then sells it to the transport company for $1.25. The refinery's value added is $0.50. The transport company sells the oil to the retail company for $1.85. The transport company's value added is $1.85 - $1.25 = $0.60. Finally, the retail gas station sells the gallon of gas for $3.65. The value added by the retail station is $1.80.

b. The total value added is found by summing the value added by each firm involved the production of the gallon of gas. The retail price is the same at this total of value added.

Diff: 2 Page Ref: 646/262

Topic: Measuring GDP by the Value Added Method

*: Recurring

Learning Outcome: Macro-3: Identify and interpret key macroeconomic measures

AACSB: Analytical thinking

19.2 Does GDP Measure What We Want It to Measure?

-The Philippines and Vietnam have roughly the same size population. Suppose the GDP of the Philippines is $1,000 billion and the GDP of Vietnam is $10,000 billion. You should conclude

(Multiple Choice)

4.8/5 (34)

When consumers are less confident about their jobs or incomes, they are more likely to

(Multiple Choice)

4.7/5 (36)

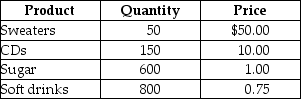

Table 19-8

-Refer to Table 19-8. Suppose that a simple economy produces only four goods and services: sweaters, CDs, sugar, and soft drinks. Assume one half of the sugar is used in making the soft drinks and the other half of the sugar is purchased by households. Calculate nominal GDP for this simple economy.

-Refer to Table 19-8. Suppose that a simple economy produces only four goods and services: sweaters, CDs, sugar, and soft drinks. Assume one half of the sugar is used in making the soft drinks and the other half of the sugar is purchased by households. Calculate nominal GDP for this simple economy.

(Essay)

4.8/5 (36)

Why do we not count the value of intermediate goods and services in gross domestic product? Does the value of intermediate goods and services show up in gross domestic product? If so, how?

(Essay)

4.8/5 (39)

Government spending on transfer payments is included in government purchases when calculating GDP because it results in the production of new goods and services.

(True/False)

4.9/5 (39)

Table 19-18

A very simple economy produces three goods: cameras, legal services, and books. The quantities produced and their corresponding prices for 2013 and 2018 are shown in the table above.

-Refer to Table 19-18. What is real GDP in 2018, using 2018 as the base year?

(Multiple Choice)

4.7/5 (36)

Which of the following would increase GNP in the United States?

(Multiple Choice)

4.7/5 (32)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)