Exam 10: The Firm and the Industry Under Perfect Competition

Exam 1: What Is Economics229 Questions

Exam 2: The Economy Myth and Reality154 Questions

Exam 3: The Fundamental Economic Problem Scarcity and Choice254 Questions

Exam 4: Supply and Demand an Initial Look287 Questions

Exam 5: Consumer Choice Individual and Market Demand190 Questions

Exam 6: Demand and Elasticity210 Questions

Exam 7: Production Inputs and Cost Building Blocks for Supply Analysis206 Questions

Exam 8: Output Price and Profit the Importance of Marginal Analysis188 Questions

Exam 9: Securities Business Finance and the Economy the Tail That Wags the Dog201 Questions

Exam 10: The Firm and the Industry Under Perfect Competition194 Questions

Exam 11: Monopoly206 Questions

Exam 12: Between Competition and Monopoly228 Questions

Exam 13: Limiting Market Power Regulation and Antitrust144 Questions

Exam 14: The Case for Free Markets the Price System224 Questions

Exam 15: The Shortcomings of Free Markets207 Questions

Exam 16: Externalities the Environment and Natural Resources216 Questions

Exam 17: Taxation and Resource Allocation219 Questions

Exam 18: Pricing the Factors of Production231 Questions

Exam 19: Labor and Entrepreneurship the Human Inputs267 Questions

Exam 20: Poverty Inequality and Discrimination169 Questions

Exam 21: Is Us Economic Leadership Threatened75 Questions

Exam 22: International Trade and Comparative Advantage221 Questions

Select questions type

A perfectly competitive firm is a "price taker" because it cannot sell its product for more than the market price.

Free

(True/False)

4.8/5  (43)

(43)

Correct Answer: Verified

Verified

True

A firm that is earning zero economic profit should go out of business.

Free

(True/False)

4.7/5 (39)

Correct Answer:Verified

False

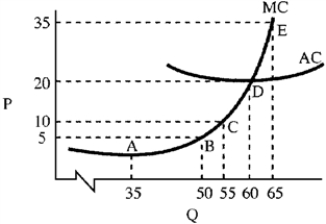

Figure 10-6  -In Figure 10-6, the price at long-run equilibrium is

-In Figure 10-6, the price at long-run equilibrium is

Free

(Multiple Choice)

4.8/5 (29)

Correct Answer:Verified

C

Which of the following most resembles a perfectly competitive market?

(Multiple Choice)

4.7/5 (36)

The difference between zero accounting profit and zero economic profit is that

(Multiple Choice)

4.8/5 (35)

Which of the following statements concerning equilibrium in the long run is not true?

(Multiple Choice)

4.8/5 (36)

The short-run supply curve for a perfectly competitive firm is that portion of the MC curve above the AVC curve.

(True/False)

4.8/5 (42)

For the perfectly competitive firm in Figure 10-8, what is the long-run price and quantity?

(Multiple Choice)

4.8/5 (38)

Sally Rand owns a ceiling fan company.She sells 1,000 ceiling fans at $50 each.Each fan costs her $20.She uses her own money to buy the fans; she withdraws the money from her savings account where it earns 5 percent interest.Before going into the ceiling fan business, she worked as a fan-dancer at $25,000 a year.Should Sally remain in business?

(Essay)

4.9/5 (30)

A perfectly competitive firm will always maximize profits by producing where

(Multiple Choice)

4.8/5 (42)

Explain why Adam Smith believed that competitive markets are a key component of achieving the gains from the invisible hand.

(Essay)

4.8/5 (31)

A perfectly competitive firm should continue to expand output until

(Multiple Choice)

4.7/5 (36)

In a market with perfectly competitive firms, the market demand curve is usually ____ and the demand curve facing each individual firm ____.

(Multiple Choice)

5.0/5 (35)

The market demand schedule in perfect competition is horizontal.

(True/False)

4.8/5 (33)

The market for toothpaste is a good example of perfect competition.

(True/False)

4.9/5 (36)

A perfectly competitive firm's short-run supply is infinite at the market price.

(True/False)

4.9/5 (32)

A firm that is operating at a loss may continue to operate for a while because of costs that it will still have to pay even if production ceases.

(True/False)

4.9/5 (37)

A firm sells in a competitive market in which price is $12.Its marginal cost is 6 + .25Q.Determine the profit-maximizing level of output.

(Essay)

4.9/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)