Exam 3: The Accounting Information System and Measurement Issues

Exam 1: The Canadian Financial Reporting Environment44 Questions

Exam 2: Conceptual Framework Underlying Financial Reporting56 Questions

Exam 3: The Accounting Information System and Measurement Issues68 Questions

Exam 4: Reporting Financial Performance79 Questions

Exam 5: Financial Position and Cash Flows78 Questions

Exam 6: Revenue Recognition79 Questions

Exam 7: Cash and Receivables75 Questions

Exam 8: Inventory127 Questions

Exam 9: Investments96 Questions

Exam 10: Property, Plant, and Equipment: Accounting Model Basics69 Questions

Exam 11: Depreciation, Impairment, and Disposition74 Questions

Exam 12: Intangible Assets and Goodwill72 Questions

Exam 13: Non-Financial Andcurrent Liabilities70 Questions

Exam 14: Long-Term Financial Liabilities62 Questions

Exam 15: Shareholders Equity123 Questions

Exam 16: Complex Financial Instruments76 Questions

Exam 17: Earnings Per Share50 Questions

Exam 18: Income Taxes55 Questions

Exam 19: Pensions and Other Employee Future Benefits72 Questions

Exam 20: Leases69 Questions

Exam 21: Accounting Changes and Error Analysis44 Questions

Exam 22: Statement of Cash Flows53 Questions

Exam 23: Other Measurement and Disclosure Issues37 Questions

Select questions type

Mark-Wall Corp.'s trademark was licensed to Rodgers Inc.for royalties of 12% of sales of the trademarked items.Royalties are payable semi-annually on March 15 for sales in July through December of the previous year, and on September 15 for sales in January through June of the same year.Mark-Wall received the following royalties from Rodgers:  Rodgers estimates that sales of the trademarked items would total $67,000 for July through December 2018.On their statement of comprehensive income for calendar 2018, Mark-Wall's royalty revenue should be

Rodgers estimates that sales of the trademarked items would total $67,000 for July through December 2018.On their statement of comprehensive income for calendar 2018, Mark-Wall's royalty revenue should be

(Multiple Choice)

4.8/5  (40)

(40)

On June 1, 2017, Carr Corp.loaned Farr Corp.$600,000 on a 5% note, payable in five annual instalments of $120,000 (plus interest), beginning January 2, 2018.Interest on the note is payable on the first day of each month beginning July 1, 2017.Farr made timely payments through November 1, 2017.On January 2, 2018, Carr received payment of the first principal instalment plus all interest due.At December 31, 2017, Carr's interest receivable on this loan is

(Multiple Choice)

4.8/5 (36)

White Resources determines that it has NOT yet recorded the 2017 accrual for Interest Revenue to be received in 2018.Assuming the amount to be recorded for 2017 is $2,000, the required adjustment at December 31, 2017 is

(Multiple Choice)

4.8/5 (40)

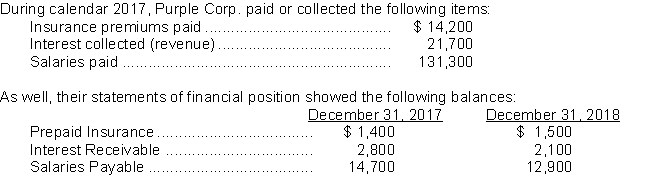

Use the following information for questions.

-The insurance expense on the 2017 statement of comprehensive income was

-The insurance expense on the 2017 statement of comprehensive income was

(Multiple Choice)

4.8/5 (28)

Which type of account is always debited during the closing process?

(Multiple Choice)

4.8/5 (28)

In order to measure fair value under IFRS13, an entity must determine

(Multiple Choice)

4.8/5 (39)

On September 1, 2017 Culver Corp.issued a 9% note payable to National Bank for $750,000, payable in three equal annual principal payments of $250,000, plus interest.On this date, the bank's prime rate was 8%.The first payment for interest and principal was made on September 1, 2018.At December 31, 2018, Culver should record accrued interest payable of

(Multiple Choice)

5.0/5 (39)

Grant Limited pays all salaried employees on a biweekly basis.Overtime pay, however, is paid in the next biweekly period.Grant accrues salaries expense only at its December 31 year end.Data relating to salaries earned in December 2017 are as follows:

Last payroll was paid on Dec 27, 2017, for the two-week period ended Dec 27, 2017.

Overtime pay earned in the two-week period ended Dec 27, 2017 was $7,000.

Remaining work days in 2017 were December 28, 29, 30, on which days there was no overtime.

The regular biweekly salaries total $100,000.Assuming a five-day work week, Grant should record a liability at December 31, 2017 for accrued salaries of

(Multiple Choice)

4.9/5 (42)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)