Exam 14: Firms in Competitive Markets

Exam 1: Ten Principles of Economics455 Questions

Exam 2: Thinking Like an Economist643 Questions

Exam 3: Interdependence and the Gains From Trade547 Questions

Exam 4: The Market Forces of Supply and Demand693 Questions

Exam 5: Elasticity and Its Application626 Questions

Exam 6: Supply, Demand, and Government Policies668 Questions

Exam 7: Consumers, Producers, and the Efficiency of Markets547 Questions

Exam 8: Applications: the Costs of Taxation509 Questions

Exam 9: Application: International Trade521 Questions

Exam 10: Externalities543 Questions

Exam 11: Public Goods and Common Resources452 Questions

Exam 12: The Design of the Tax System664 Questions

Exam 13: The Costs of Production649 Questions

Exam 14: Firms in Competitive Markets604 Questions

Exam 15: Monopoly662 Questions

Exam 16: Monopolistic Competition649 Questions

Exam 17: Oligopoly522 Questions

Exam 18: The Markets for the Factors of Production592 Questions

Exam 19: Earnings and Discrimination511 Questions

Exam 20: Income Inequality and Poverty478 Questions

Exam 21: The Theory of Consumer Choice570 Questions

Exam 22: Frontiers in Microeconomics461 Questions

Exam 23: Measuring a Nation S Income547 Questions

Exam 24: Measuring the Cost of Living565 Questions

Exam 25: Production and Growth527 Questions

Exam 26: Saving, Investment, and the Financial System637 Questions

Exam 27: Tools of Finance534 Questions

Exam 28: Unemployment and Its Natural Rate701 Questions

Exam 29: The Monetary System540 Questions

Exam 30: Money Growth and Inflation504 Questions

Exam 31: Open-Economy Macroeconomics: Basic Concepts540 Questions

Exam 32: A Macroeconomic Theory of the Open Economy511 Questions

Exam 33: Aggregate Demand and Aggregate Supply572 Questions

Exam 34: The Influence of Monetary and Fiscal Policy on Aggregate Demand523 Questions

Exam 35: The Short-Run Tradeoff Between Inflation and Unemployment536 Questions

Exam 36: Six Debates Over Macroeconomic Policy354 Questions

Select questions type

Which of the following statements regarding a competitive market is not correct?

Free

(Multiple Choice)

4.8/5  (34)

(34)

Correct Answer: Verified

Verified

D

A market might have an upward-sloping long-run supply curve if

Free

(Multiple Choice)

4.8/5 (38)

Correct Answer:Verified

A

Table 14-12  -Refer to Table 14-12. What is the marginal cost of the 5th unit?

-Refer to Table 14-12. What is the marginal cost of the 5th unit?

Free

(Multiple Choice)

4.8/5 (36)

Correct Answer:Verified

C

Roger owns a small health store that sells vitamins in a perfectly competitive market. If vitamins sell for $12 per bottle and the average total cost per bottle is $12.50 at the profit-maximizing output level, then in the long run

(Multiple Choice)

4.7/5 (34)

Suppose a competitive market is comprised of firms that face identical cost curves. The firms experience an increase in demand that results in positive profits for the firms. Which of the following events are then most likely to occur?

(i)New firms will enter the market.

(ii)In the short run, price will rise; in the long run, price will rise further.

(iii)In the long run, all firms will be producing at their efficient scale.

(Multiple Choice)

4.8/5 (35)

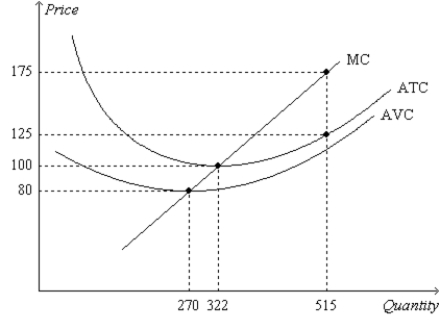

Figure 14-7  -Refer to Figure 14-7. Suppose AVC = $113 when the firm produces 515 units of output. Then the firm's fixed cost amounts to

-Refer to Figure 14-7. Suppose AVC = $113 when the firm produces 515 units of output. Then the firm's fixed cost amounts to

(Multiple Choice)

4.8/5 (30)

Profit maximizing firms in competitive industries with free entry and exit face a price equal to the lowest possible

(Multiple Choice)

4.9/5 (37)

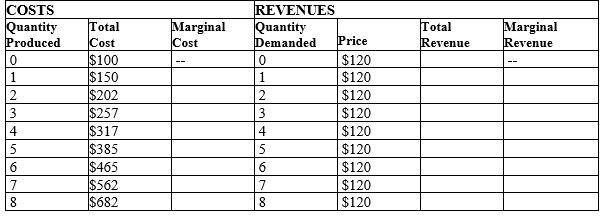

Table 14-13  -Refer to Table 14-13. In order to maximize profits, how many units should Diana's Dress Emporium produce?

-Refer to Table 14-13. In order to maximize profits, how many units should Diana's Dress Emporium produce?

(Multiple Choice)

4.8/5 (33)

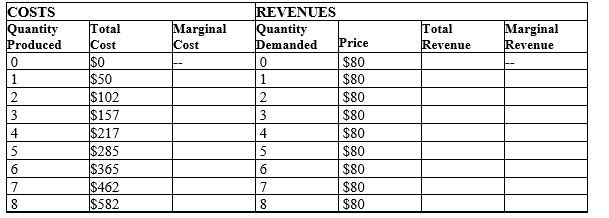

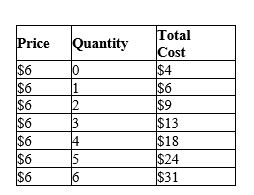

Table 14-11

Suppose that a firm in a competitive market faces the following prices and costs:  -Refer to Table 14-11. The marginal revenue from producing the 3rd unit equals

(i) $6.

(ii) the price.

(iii) the marginal cost.

-Refer to Table 14-11. The marginal revenue from producing the 3rd unit equals

(i) $6.

(ii) the price.

(iii) the marginal cost.

(Multiple Choice)

4.7/5 (34)

The accountants hired by the Brookside Racquet Club have determined total fixed cost to be $75,000, total variable cost to be $130,000, and total revenue to be $145,000. Because of this information, in the short run, the Brookside Racquet Club should

(Multiple Choice)

4.8/5 (30)

If a profit-maximizing firm in a competitive market discovers that, at its current level of production, price is greater than marginal cost, it should

(Multiple Choice)

4.8/5 (40)

Which of these curves is the competitive firm's short-run supply curve?

(Multiple Choice)

5.0/5 (28)

If firms are competitive and profit maximizing, the price of a good equals the

(Multiple Choice)

4.9/5 (34)

Scenario 14-1. A competitive firm sells its output for $20 per unit. When the firm produces 200 units of output, average variable cost is $16, marginal cost is $18, and average total cost is $23.

-Refer to Scenario 14-1. Compare the firm's profit or loss at 200 units of output with its profit or loss if it were to shut down.

(Essay)

4.9/5 (33)

In competitive markets, firms that raise their prices are typically rewarded with larger profits.

(True/False)

4.9/5 (33)

A competitive firm is currently producing a quantity of output at which marginal revenue exceeds marginal cost. In order to increase its profit, the firm should

(Multiple Choice)

4.8/5 (35)

Suppose that a firm operating in perfectly competitive market sells 50 units of output. Its total revenues from the sale are $500. Which of the following statements is correct?

(i)Marginal revenue equals $5.

(ii)Average revenue equals $10.

(iii)Price equals $15.

(Multiple Choice)

4.9/5 (41)

When fixed costs are ignored because they are irrelevant to a business's production decision, they are called

(Multiple Choice)

4.9/5 (29)

Tom produces commemorative t-shirts in a competitive market. If Tom decides to decrease his output, this will

(Multiple Choice)

4.8/5 (31)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)