Exam 22: The Firm: Cost and Output Determination

Exam 1: The Nature of Economics347 Questions

Exam 2: Scarcity and the World of Trade-Offs411 Questions

Exam 3: Demand and Supply448 Questions

Exam 4: Extensions of Demand and Supply Analysis399 Questions

Exam 5: Public Spending and Public Choice359 Questions

Exam 6: Funding the Public Sector202 Questions

Exam 19: Demand and Supply Elasticity413 Questions

Exam 20: Consumer Choice457 Questions

Exam 21: Rents, Profits, and the Financial Environment of Business445 Questions

Exam 22: The Firm: Cost and Output Determination387 Questions

Exam 23: Perfect Competition431 Questions

Exam 24: Monopoly386 Questions

Exam 25: Monopolistic Competition309 Questions

Exam 26: Oligopoly and Strategic Behavior302 Questions

Exam 27: Regulation and Antitrust Policy in a Globalized Economy309 Questions

Exam 28: The Labor Market: Demand, Supply and Outsourcing374 Questions

Exam 29: Unions and Labor Market Monopoly Power316 Questions

Exam 30: Income, Poverty, and Health Care302 Questions

Exam 31: Environmental Economics299 Questions

Exam 32: Comparative Advantage and the Open Economy313 Questions

Exam 33: Exchange Rates and the Balance of Payments300 Questions

Select questions type

The time period during which all factors of production can be varied is the

(Multiple Choice)

4.9/5  (43)

(43)

A decrease in long-run average costs resulting from decreases in output is

(Multiple Choice)

4.8/5 (31)

Marginal physical product of the first worker is 100, 120 for the second, 80 for the third, 30 for the fourth, 5 for the fifth, 3 for the sixth, 2 for the seventh, 1 for the eighth, and 0 for the ninth. What is total product for the fifth worker and the ninth worker respectively?

(Multiple Choice)

4.8/5 (29)

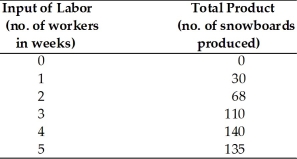

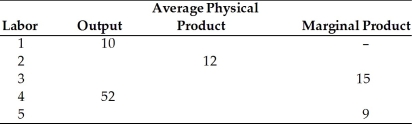

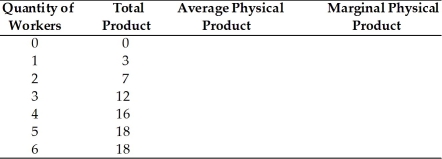

-In the above table, the marginal product of the second worker is

-In the above table, the marginal product of the second worker is

(Multiple Choice)

4.9/5 (33)

An increase in long-run average costs resulting from decreases in output is

(Multiple Choice)

4.7/5 (40)

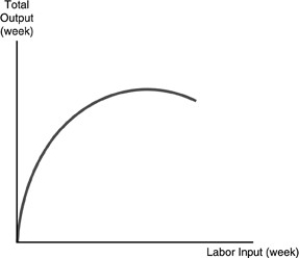

The long run is defined as a time period during which full adjustment can be made to any change in the economic environment. Thus in the long run, all factors of production are variable. Long-run curves are sometimes called planning curves, and the long run is sometimes called the

(Multiple Choice)

4.8/5 (29)

-Phil found that as he continued to crowd laborers into his hot dog stand, the extra output he was receiving from each additional laborer was beginning to fall off. This is an example of the

-Phil found that as he continued to crowd laborers into his hot dog stand, the extra output he was receiving from each additional laborer was beginning to fall off. This is an example of the

(Multiple Choice)

4.8/5 (23)

Which of the following is NOT one of the reasons a firm might be expected to experience economies of scale?

(Multiple Choice)

4.8/5 (33)

The ratio of total costs to the quantity produced is referred to as

(Multiple Choice)

4.8/5 (33)

The time period during which a firm's capital is fixed but its labor is variable is called

(Multiple Choice)

4.8/5 (35)

If the long-run average cost curve continuously slopes upward as output rises, minimum efficient scale would be

(Multiple Choice)

4.7/5 (33)

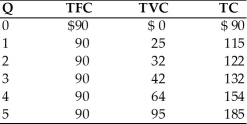

Assume that in the short run a firm is producing 100 units of output, has average total costs of $100, and average fixed costs of $20. The firm's total variable cost at this output level is

(Multiple Choice)

4.8/5 (38)

The marginal cost curve always intersects the average total cost curve at the point at which the average total cost curve

(Multiple Choice)

4.7/5 (37)

-Refer to the above table. At an output of 4 units, average variable costs are

-Refer to the above table. At an output of 4 units, average variable costs are

(Multiple Choice)

4.9/5 (31)

-Using the above table, the marginal product of the 2nd worker is

-Using the above table, the marginal product of the 2nd worker is

(Multiple Choice)

4.8/5 (34)

-In the above table, the marginal physical product of the 3rd worker is

-In the above table, the marginal physical product of the 3rd worker is

(Multiple Choice)

4.7/5 (31)

Graphically, what happens to the production function if a firm uses automation to raise the amount of output per worker? Explain.

(Essay)

4.7/5 (45)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)