Exam 4: Complex Financial Instruments

Exam 1: Current Liabilities and Contingencies81 Questions

Exam 2: Non-Current Financial Liabilities97 Questions

Exam 3: Equities78 Questions

Exam 4: Complex Financial Instruments100 Questions

Exam 5: Earnings Per Share91 Questions

Exam 6: Pensions and Other Employee Future Benefits69 Questions

Exam 7: Accounting for Leases43 Questions

Exam 8: Accounting for Income Taxes78 Questions

Exam 9: Accounting Changes39 Questions

Exam 10: Statement of Cash Flows75 Questions

Select questions type

A company issues convertible bonds with face value of $7,000,000 and receives proceeds of $8,500,000. Each $1,000 bond can be converted, at the option of the holder, into 100 common shares. The underwriter estimated the market value of the bonds alone, excluding the conversion rights, to be approximately $7,300,000.

Required:

Record the journal entry for the issuance of these bonds based on IFRS.

(Essay)

4.8/5  (36)

(36)

Which of the following statements is correct about accounting for financial liabilities?

(Multiple Choice)

4.8/5 (45)

How would the liability portion of the compound instrument be recorded?

(Multiple Choice)

4.8/5 (37)

Assume that on January 15, 2021 MAK agrees to purchase US$500,000 for C$550,000 for delivery on January 15, 2022. The exchange rate at MAK's December 31, 2021 year-end was US$1 = C$0.95 and the January 15, 2022 exchange rate is US$1 = C$0.97. What is the foreign exchange gain or loss recognized at year-end?

(Multiple Choice)

4.7/5 (38)

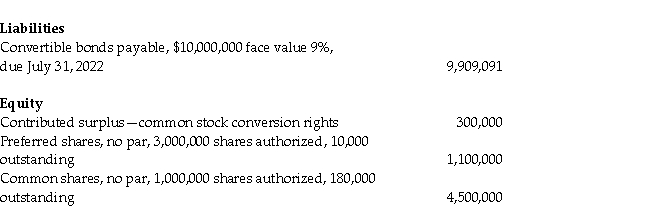

LMN Company reported the following amounts on its balance sheet at July 31, 2022:  Additional information

1. The bonds pay interest each July 31. Each $1,000 bond is convertible into 10 common shares. The bonds were originally issued to yield 10%. On July 31, 2022, all the bonds were converted after the final interest payment was made. LMN uses the book value method to record bond conversions as recommended under IFRS.

2. No other share or bond transactions occurred during the year.

Required:

a. Prepare the journal entry to record the bond interest payment on July 31, 2022.

b. Calculate the total number of common shares outstanding after the bonds' conversion on July 31, 2022.

c. Prepare the journal entry to record the bond conversion.

Additional information

1. The bonds pay interest each July 31. Each $1,000 bond is convertible into 10 common shares. The bonds were originally issued to yield 10%. On July 31, 2022, all the bonds were converted after the final interest payment was made. LMN uses the book value method to record bond conversions as recommended under IFRS.

2. No other share or bond transactions occurred during the year.

Required:

a. Prepare the journal entry to record the bond interest payment on July 31, 2022.

b. Calculate the total number of common shares outstanding after the bonds' conversion on July 31, 2022.

c. Prepare the journal entry to record the bond conversion.

(Essay)

4.8/5 (39)

Explain what a "fair value" and "cash flow" hedge is and how each is accounted for under IFRS.

(Essay)

4.8/5 (35)

A company issued 100,000 preferred shares and received proceeds of $5,750,000. These shares have a benchmark value of $50 per share and pay cumulative dividends of 6%. Buyers of the preferred shares also received a detachable warrant with each share purchased. Each warrant gives the holder the right to buy one common share at $35 per share within 10 years.

The underwriter estimated that the market value of the preferred shares alone, excluding the conversion rights, is approximately $55 per share. Shortly after the issuance of the preferred shares, the detachable warrants traded at $5 each.

Required:

Record the journal entry for the issuance of these shares and warrants under IFRS.

(Essay)

4.9/5 (40)

Nappy Lodge issued 15,000 at-the-money stock options to its management on January 1, 2021. These options vest on January 1, 2024. Nappy's share price was $20 on the grant date and $25 on the vesting date. Estimates of the fair value of the options showed that they were worth $3 on the grant date and $11 on the vesting date. On the vesting date, management exercised all 15,000 options. Nappy has a December 31 year-end.

Required:

Record all of the journal entries relating to the stock options.

(Essay)

4.8/5 (36)

O'Neil Manufacturing issued 200,000 stock options to its employees. The company granted the stock options at-the-money, when the share price was $40. These options have no vesting conditions. By year-end, the share price had increased to $42. O'Neil's management estimates the value of these options at the grant date to be $1.75 each.

Required:

Record the issuance of the stock options.

(Essay)

4.9/5 (43)

On January 1, 2021, Braeben Inc. granted stock options to officers and key employees for the purchase of 180,000 of the company's no par value common shares at $30 each. The options were exercisable within a five-year period beginning January 1, 2023 by grantees still in the employ of the company, and they expire December 31, 2027. The market price of Braeben's common share was $20 per share at the date of grant. Using the Black-Scholes option pricing model, the company estimated the value of each option on January 1, 2021 to be $2.75.

On March 31, 2023, 30,000 options were exercised when the market value of common stock was $44 per share. The remainder of the options expired unexercised. The company has a December 31 year-end.

Required:

Record the journal entries for Braeben's stock options.

(Essay)

4.7/5 (39)

Which statement is correct about the accounting for employee stock options?

(Multiple Choice)

5.0/5 (46)

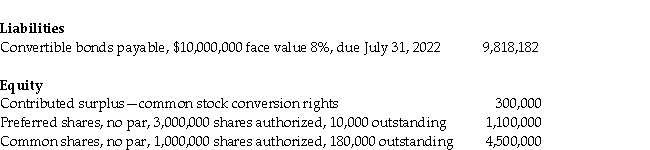

LMN Company reported the following amounts on its balance sheet at July 31, 2021:  Additional information

1. The bonds pay interest each July 31. Each $1,000 bond is convertible into 5 common shares. The bonds were originally issued to yield 10%. On July 31, 2022, all the bonds were converted after the final interest payment was made. LMN uses the book value method to record bond conversions as recommended under IFRS.

2. No other share or bond transactions occurred during the year.

Required:

a. Prepare the journal entry to record the bond interest payment on July 31, 2022.

b. Calculate the total number of common shares outstanding after the bonds' conversion on July 31, 2022.

c. Prepare the journal entry to record the bond conversion.

Additional information

1. The bonds pay interest each July 31. Each $1,000 bond is convertible into 5 common shares. The bonds were originally issued to yield 10%. On July 31, 2022, all the bonds were converted after the final interest payment was made. LMN uses the book value method to record bond conversions as recommended under IFRS.

2. No other share or bond transactions occurred during the year.

Required:

a. Prepare the journal entry to record the bond interest payment on July 31, 2022.

b. Calculate the total number of common shares outstanding after the bonds' conversion on July 31, 2022.

c. Prepare the journal entry to record the bond conversion.

(Essay)

4.8/5 (42)

On December 15, a company enters into a foreign currency forward to buy €100,000 at C$1.60 per euro in 30 days. The exchange rate on the day of the company's year-end of December 31 was C$1.55: €l.

Required:

Record the journal entries related to this forward contract.

(Essay)

4.8/5 (32)

Princeton Inc. granted 290,000 stock options to its employees. The options expire 45 years after the grant date of January 1, 2021, when the share price was $23. Employees still employed by the company four years after the grant date may exercise the option to purchase shares at $45 each; that is, the options vest to the employees after four years. A consultant estimated the value of each option at the date of grant to be $2.50 each.

Required:

Record the journal entries relating to the issuance of stock options.

(Essay)

4.9/5 (41)

A company issues convertible bonds with face value of $5,000,000 and receives proceeds of $6,500,000. Each $1,000 bond can be converted, at the option of the holder, into 80 common shares. The underwriter estimated the market value of the bonds alone, excluding the conversion rights, to be approximately $6,300,000.

Required:

Record the journal entry for the issuance of these bonds based on IFRS.

(Essay)

4.8/5 (41)

What are the similarities and differences between forwards and futures?

(Essay)

4.9/5 (31)

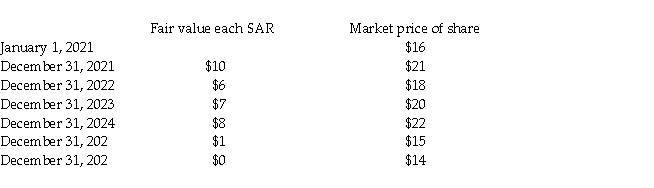

On January 1, 2021 Taffy Inc. granted 210,000 stock appreciation rights (SARs)to its executives. Each SAR entitled its holder to receive cash equal to the difference between the market price of the common share and the benchmark price of $16. The SARs vested after three years and expired on Dec. 31, 20 23. On January 1, 2024, 100,000 SARs are exercised. The market price of the shares remained at $20. On January 1, 2025, 50,000 SARS are exercised. The market price of the shares remained at $22. The remaining SARs expired.

Pertinent stock-related data are listed below:  Assume that Taffy Inc. reports its financial results in accordance with ASPE.

Required:

a. Prepare the journal entry at December 31, 2021, to record compensation expense.

b. Prepare the journal entry at December 31, 2022, to record compensation expense.

c. Prepare the journal entry at December 31, 2023, to record compensation expense.

d. Prepare the journal entry at January 1, 2024, to record the partial exercise of the SARs.

e. Prepare the journal entry at December 31, 2024, to record compensation expense.

f. Prepare the journal entry at January 1, 2025, to record the partial exercise of the SARs.

g. Prepare the journal entry at December 31, 2025, to record compensation expense.

h. Prepare the journal entry at December 31, 2026, to record compensation expense.

Assume that Taffy Inc. reports its financial results in accordance with ASPE.

Required:

a. Prepare the journal entry at December 31, 2021, to record compensation expense.

b. Prepare the journal entry at December 31, 2022, to record compensation expense.

c. Prepare the journal entry at December 31, 2023, to record compensation expense.

d. Prepare the journal entry at January 1, 2024, to record the partial exercise of the SARs.

e. Prepare the journal entry at December 31, 2024, to record compensation expense.

f. Prepare the journal entry at January 1, 2025, to record the partial exercise of the SARs.

g. Prepare the journal entry at December 31, 2025, to record compensation expense.

h. Prepare the journal entry at December 31, 2026, to record compensation expense.

(Essay)

4.8/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)