Exam 3: The Fundamental Economic Problem: Scarcity and Choice

Exam 1: What Is Economics?227 Questions

Exam 2: The Economy: Myth and Reality150 Questions

Exam 3: The Fundamental Economic Problem: Scarcity and Choice250 Questions

Exam 4: Supply and Demand: An Initial Look308 Questions

Exam 5: Consumer Choice: Individual and Market Demand202 Questions

Exam 6: Demand and Elasticity209 Questions

Exam 7: Production, Inputs, and Cost: Building Blocks for Supply Analysis216 Questions

Exam 8: Output, Price, and Profit: The Importance of Marginal Analysis189 Questions

Exam 9: Securities: Business Finance, and the Economy: The Tail that Wags the Dog?198 Questions

Exam 10: The Firm and the Industry under Perfect Competition208 Questions

Exam 11: Monopoly203 Questions

Exam 12: Between Competition and Monopoly225 Questions

Exam 13: Limiting Market Power: Regulation and Antitrust152 Questions

Exam 14: The Case for Free Markets I: The Price System220 Questions

Exam 15: The Shortcomings of Free Markets212 Questions

Exam 16: The Market's Prime Achievement: Innovation and Growth110 Questions

Exam 17: Externalities, the Environment, and Natural Resources217 Questions

Exam 18: Taxation and Resource Allocation219 Questions

Exam 19: Pricing the Factors of Production228 Questions

Exam 20: Labor and Entrepreneurship: The Human Inputs223 Questions

Exam 21: Poverty, Inequality, and Discrimination167 Questions

Exam 22: An Introduction to Macroeconomics211 Questions

Exam 23: The Goals of Macroeconomic Policy207 Questions

Exam 24: Economic Growth: Theory and Policy223 Questions

Exam 25: Aggregate Demand and the Powerful Consumer214 Questions

Exam 26: Demand-Side Equilibrium: Unemployment or Inflation?210 Questions

Exam 27: Bringing in the Supply Side: Unemployment and Inflation?223 Questions

Exam 28: Managing Aggregate Demand: Fiscal Policy205 Questions

Exam 29: Money and the Banking System219 Questions

Exam 30: Monetary Policy: Conventional and Unconventional205 Questions

Exam 31: The Financial Crisis and the Great Recession61 Questions

Exam 32: The Debate over Monetary and Fiscal Policy214 Questions

Exam 33: Budget Deficits in the Short and Long Run210 Questions

Exam 34: The Trade-Off between Inflation and Unemployment214 Questions

Exam 35: International Trade and Comparative Advantage226 Questions

Exam 36: The International Monetary System: Order or Disorder?213 Questions

Exam 37: Exchange Rates and the Macroeconomy214 Questions

Select questions type

Specialization of labor makes sense only if there is some means of exchange.

(True/False)

4.8/5  (33)

(33)

Waiting in line to get a free ticket does not involve any opportunity cost.

(True/False)

4.8/5 (45)

If a market system is functioning well, we can conclude that goods with

(Multiple Choice)

4.9/5 (44)

Which of the following is an example of opportunity cost not measured by money cost?

(Multiple Choice)

4.8/5 (38)

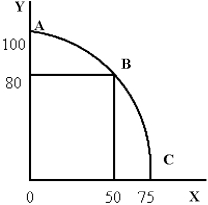

Figure 3-7

-What is the opportunity cost of moving from point B to point A in Figure 3-7?

-What is the opportunity cost of moving from point B to point A in Figure 3-7?

(Multiple Choice)

4.8/5 (35)

The production possibilities frontier has a tendency to bow outward from the origin.

(True/False)

4.8/5 (39)

See table below.Does production exhibit increasing costs? Which ring and machine combination will achieve the highest growth in the production of mood rings?

30 0 20 5 10 8 0 10

(Essay)

4.9/5 (39)

Table 3-2

A 12 16 B 17 15 C 21 13 D 23 9 E 24 5

-In Table 3-2, from point C, the opportunity cost of 3 more units of cotton would be

(Multiple Choice)

4.9/5 (41)

In the Wealth of Nations, Adam Smith wrote about how countries could increase their consumption of goods and services through specialization and trade with other countries.

(True/False)

4.9/5 (35)

How does scarcity affect the range of possible choices that decision makers face?

(Multiple Choice)

4.8/5 (40)

An optimal decision is one that chooses the most desirable from among all possibilities that are available.

(True/False)

4.9/5 (37)

Ex-London School of Economics student Mick Jagger sang, "You can't always get what you want, but if you try sometime, you just might find you can get what you need." Another statement of the basic economic principle expressed in this lyric is that

(Multiple Choice)

4.8/5 (41)

If production involves decreasing opportunity cost, the production possibilities curve

(Multiple Choice)

4.8/5 (43)

Specialization and division of labor are made easier by the existence of money.

(True/False)

4.9/5 (42)

As more of a good is produced, its opportunity cost tends to increase because resources are not equally efficient at producing all goods.

(True/False)

4.8/5 (37)

Draw a production possibilities frontier for an economy, with the axes labeled "military goods" and "peace goods." Indicate the region that is attainable and the region that is not.Explain the shape of the curve-what assumptions did you make in drawing it?

(Essay)

4.8/5 (35)

Karl Marx was critical of markets on the grounds that they are not efficient.

(True/False)

4.8/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)