Exam 4: Corporate Nonliquidating Distributions

Exam 1: Tax Research111 Questions

Exam 2: Corporate Formations and Capital Structure123 Questions

Exam 3: The Corporate Income Tax88 Questions

Exam 4: Corporate Nonliquidating Distributions113 Questions

Exam 5: Other Corporate Tax Levies60 Questions

Exam 6: Corporate Liquidating Distributions101 Questions

Exam 7: Corporate Acquisitions and Reorganizations101 Questions

Exam 8: Consolidated Tax Returns89 Questions

Exam 9: Partnership Formation and Operation116 Questions

Exam 10: Special Partnership Issues108 Questions

Exam 11: S Corporations105 Questions

Exam 12: The Gift Tax105 Questions

Exam 13: The Estate Tax107 Questions

Exam 14: Income Taxation of Trusts and Estates105 Questions

Exam 15: Administrative Procedures103 Questions

Exam 16: Us Taxation of Foreign-Related Transactions86 Questions

Select questions type

Susan owns 150 of the 200 outstanding shares of Parent Corporation's stock. Parent owns 160 of the 200 outstanding shares of Subsidiary Corporation's stock. Susan sells 50 shares of her Parent stock to Subsidiary for $40,000. Susan's basis in her Parent shares is $15,000 ($100 per share). Subsidiary Corporation and Parent Corporation have E&P of $60,000 and $25,000, respectively, at the end of the year in which the redemption occurs.

a)What is the amount and character of Susan's gain or loss on the sale?

b)What is Susan's basis in her remaining shares of Parent stock?

c)How does the sale affect the E&P of Parent and Subsidiary Corporations?

d)What basis does Subsidiary Corporation take in the Parent shares it purchases?

e)How would your answer to Part (a)change if Susan instead sells 100 of her Parent shares to Subsidiary Corporation for $80,000?

(Essay)

4.9/5  (43)

(43)

Identify which of the following increases Earnings & Profits.

(Multiple Choice)

4.8/5 (33)

Outline the computation of current E&P, including two examples for each adjustment.

(Essay)

4.8/5 (37)

Two corporations are considered to be brother-sister corporations for purposes of the Sec. 304 redemption rules if one shareholder owns more than 50% of each corporation.

(True/False)

4.8/5 (32)

Stone Corporation redeems 1,000 share of its stock from Steve for $100,000. Steve's basis in those shares is $80,000. What tax issues should Steve consider with respect to the transaction?

(Essay)

4.9/5 (39)

Ace Corporation has a single class of stock outstanding. Alan owns 200 shares of the common stock, which he purchased for $50 per share two years ago. On April 10, of the current year, Ace Corporation distributes to its shareholders one right to purchase a share of common stock at $60 per share for each share of common stock held. At the time of the distribution, the common stock is worth $75 per share, and the rights are worth $15 per right. On September 10, Alan sells 100 rights for $2,000 and exercises the remaining 100 rights. He sells 60 of the shares acquired with the rights for $80 each on November 10.

a)What is the amount and character of income Alan recognizes when he receives the rights?

b)What is the amount and character of gain or loss Alan recognizes when he sells the rights?

c)What is the amount and character of gain or loss Alan recognizes when he exercises the rights?

d)What is the amount and character of gain or loss Alan recognizes when he sells the new common stock?

e)What basis does Alan have in his remaining shares?

(Essay)

4.7/5 (40)

Boxer Corporation buys equipment in January of the current year with a seven-year class life for $15,000. The corporation expensed the $15,000 under Sec. 179. The deduction in the year of purchase for E&P purposes due to the acquisition and expensing of the equipment is

(Multiple Choice)

4.7/5 (45)

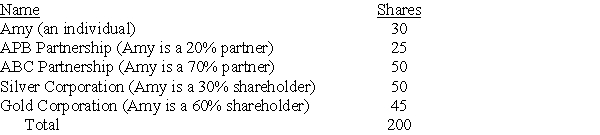

Maury Corporation has 200 shares of stock outstanding as follows:  How many shares is Amy deemed to own under the Sec. 318 attribution rules?

How many shares is Amy deemed to own under the Sec. 318 attribution rules?

(Essay)

4.9/5 (35)

Tomika Corporation has current and accumulated earnings and profits of $0. Tomika distributes $10,000 to its sole shareholder, Alana. What are Tomika's earnings and profits after the distribution?

(Multiple Choice)

4.8/5 (32)

Which of the following is not a reason for a stock redemption?

(Multiple Choice)

4.9/5 (29)

In 2010, Tru Corporation deducted $5,000 of bad debts. It received no tax benefit from the deduction because it had an NOL in 2010 that it was unable to carry back or forward. In 2011, Tru recovered $4,000 of the amount due.

a)What amount must Tru include in income in 2011?

b)What effect does the $4,000 have on E&P in 2011, if any?

(Essay)

4.9/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)