Exam 6: Analyzing and Journalizing Payroll

Exam 1: The Need for Payroll and Personnel Records108 Questions

Exam 2: Computing Wages and Salaries110 Questions

Exam 3: Social Security Taxes94 Questions

Exam 4: Income Tax Withholding88 Questions

Exam 5: Unemployment Compensation Taxes93 Questions

Exam 6: Analyzing and Journalizing Payroll75 Questions

Select questions type

At the time that the entry is made to record the employer's payroll taxes, the SUTA tax is recorded at the net amount (0.6%).

(True/False)

4.8/5  (47)

(47)

In recording the monthly adjusting entry for accrued wages at the end of the accounting period, the amount of the adjustment would usually be determined by:

(Multiple Choice)

4.9/5 (38)

Tax withholdings from employees' pays reduce the amount of the debit to Salary Expense in the payroll entry.

(True/False)

4.8/5 (36)

Under the Uniform Unclaimed Property Act, any unclaimed paychecks must be turned over to the state after the next payday.

(True/False)

4.7/5 (37)

Under the provisions of the Consumer Credit Protection Act, an employer can discharge an employee simply because the employee's wage is subject to garnishment for a single indebtedness.

(True/False)

4.7/5 (38)

The entry to record the employer's payroll taxes usually includes credits to the liability accounts for FICA (OASDI and HI), FUTA, and SUTA taxes.

(True/False)

4.8/5 (38)

The payment of the FUTA tax and the FICA taxes by the employer to the IRS is recorded in the same journal entry.

(True/False)

4.9/5 (46)

Since the credit against the FUTA tax (for SUTA contributions) is made on Form 940, the employer's payroll tax entries should include the FUTA tax at the gross amount (6.0%).

(True/False)

4.9/5 (41)

Disposable earnings are the earnings remaining after withholding only federal income taxes.

(True/False)

4.7/5 (38)

In the adjusting entry to accrue wages at the end of the accounting period, there is no need to credit any tax withholding accounts.

(True/False)

4.9/5 (44)

Once the journal entry for the payroll is complete, the information is posted to the appropriate general ledger accounts.

(True/False)

4.7/5 (36)

The FICA taxes on the employer represent both business expenses and liabilities of the employer.

(True/False)

4.8/5 (37)

In the garnishment process, federal tax levies take secondary priority to wages withheld for child support orders.

(True/False)

4.7/5 (29)

When withheld union dues are turned over to the union by the employer, a journal entry is made debiting the liability account and crediting the cash account.

(True/False)

4.7/5 (36)

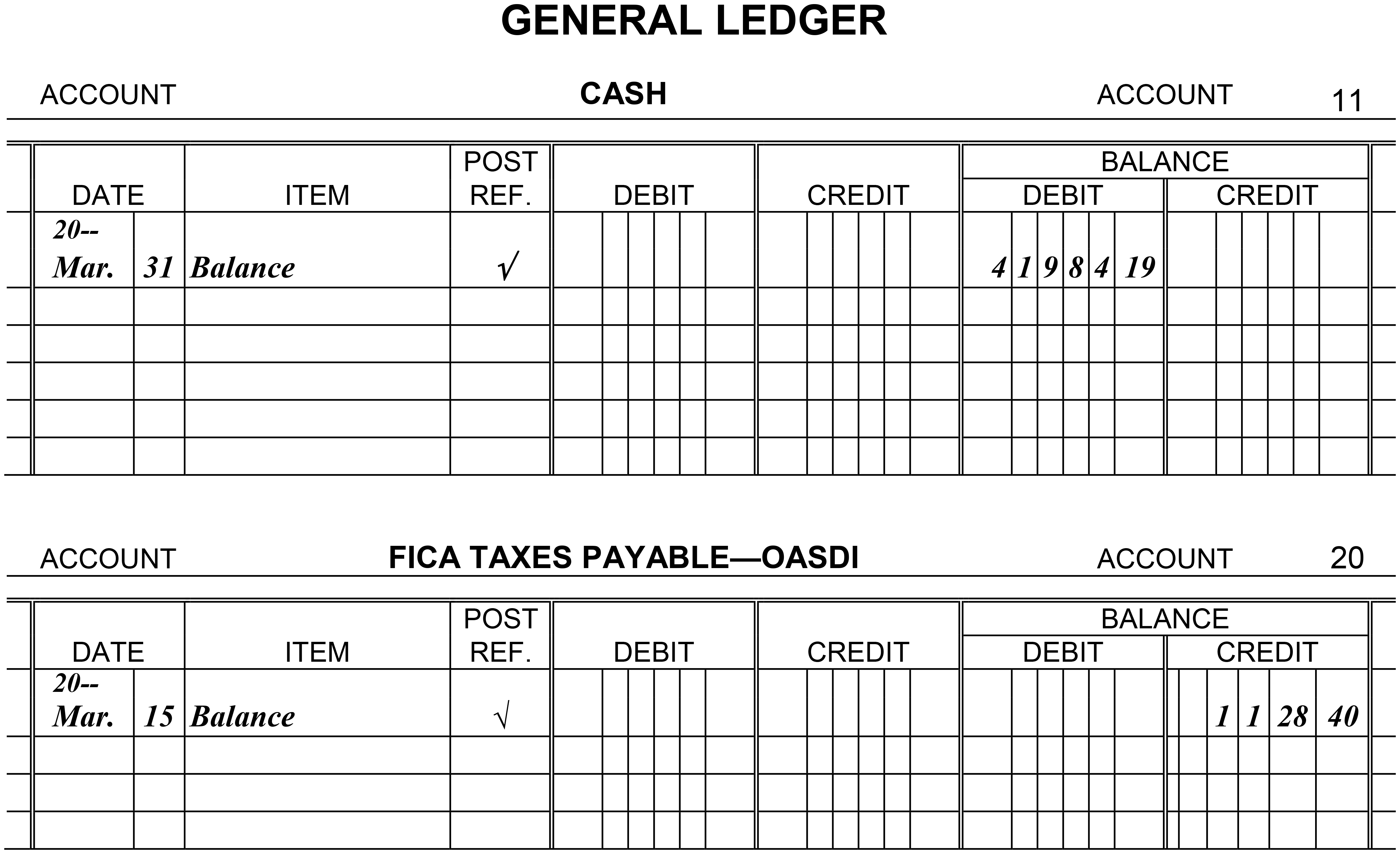

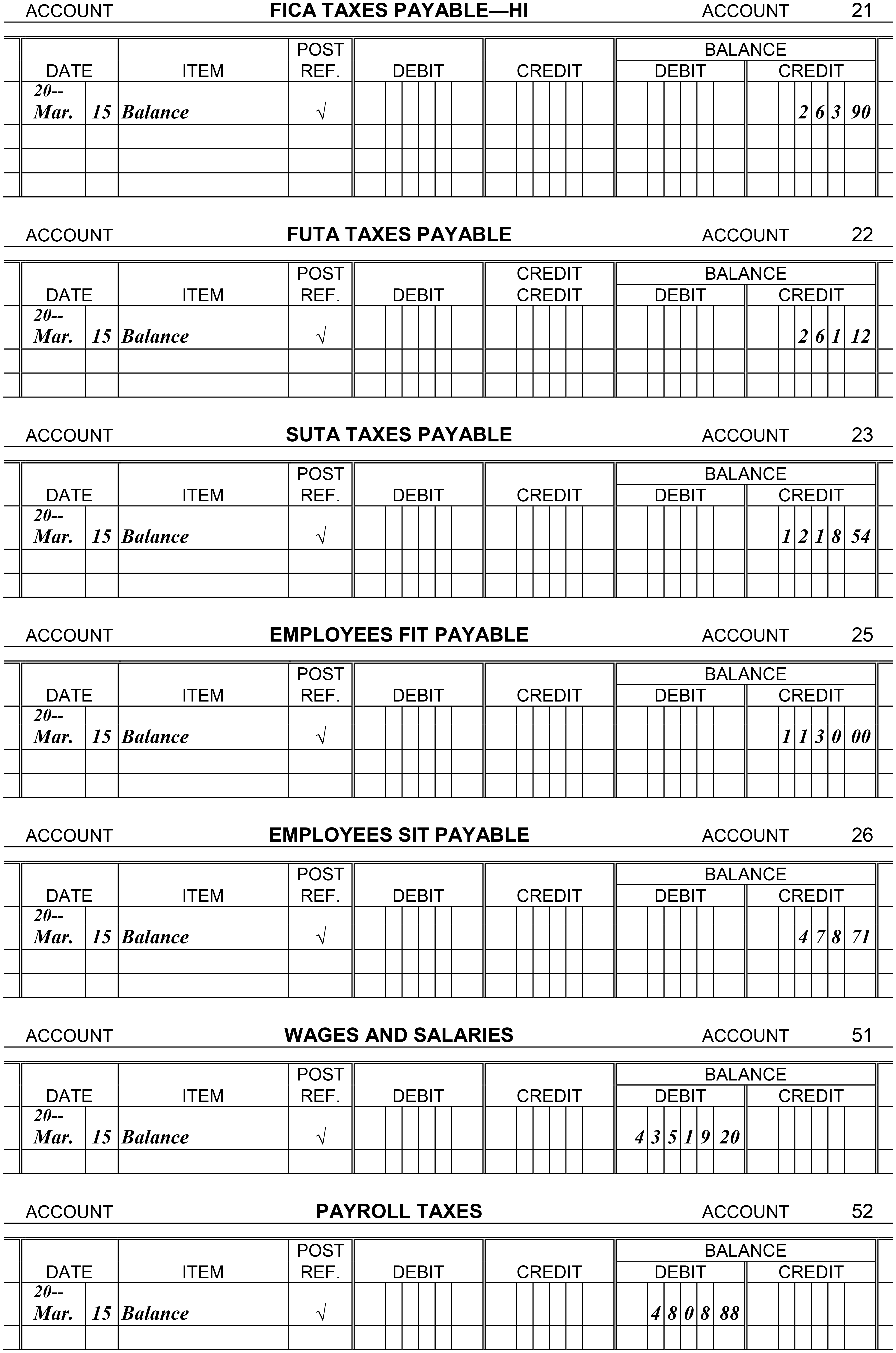

Journalize each of the payroll transactions listed below. Omit the writing of a description or explanation for each journal entry, and do not skip a line between each entry . Then post all entries except the last two to the appropriate general ledger accounts.

The balances listed in the general ledger accounts for Cash, FUTA Taxes Payable, SUTA Taxes Payable, Employees SIT Payable, Wages and Salaries, and Payroll Taxes are the results of all payroll transactions for the first quarter, not including the last pay of the quarter. The balances in FICA Taxes Payable-OASDI, FICA Taxes Payable-HI, and Employees FIT Payable are the amounts due from

the March 15 payroll.

March 31, 20--: Paid total wages of $9,350.00. These are the wages for the last semimonthly pay of March. All of this amount is taxable under FICA (OASDI and HI). In addition, withhold $1,175 for federal income taxes and $102.03 for state income taxes. These are the only deductions made from the employees' wages.

March 31, 20--: Record the employer's payroll taxes for the last pay in March. All of the earnings are taxable under FICA (OASDI and HI), FUTA (0.6%), and SUTA (2.8%).

April 15, 20--: Made a deposit to remove the liability for the FICA taxes and the employees' federal income taxes withheld on the two March payrolls.

May 2, 20--: Made the deposit to remove the liability for FUTA taxes for the first quarter of 20--.

May 2, 20--: Filed the state unemployment contributions return for the first quarter of 20-- and paid the total amount owed for the quarter to the state unemployment compensation fund.

May 2, 20--: Filed the state income tax return for the first quarter of 20-- and paid the total amount owed for the quarter to the state income tax bureau.

December 31, 20--: In July 20--, the company changed from a semimonthly pay system to a weekly pay system. The employees were paid every Friday through the rest of 20--. Record the adjusting entry for wages accrued at the end of December ($770) but not paid until the first Friday in January. Do not post this entry.

December 31, 20--: The company has determined that employees have earned $19,300 in unused vacation time. Record the adjusting entry to put this expense on the books. Do not post this entry.

(Essay)

4.8/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)