Exam 11: Property, Plant, and Equipment and Intangible Assets: Utilization and Disposition

Exam 1: Environment and Theoretical Structure of Financial Accounting181 Questions

Exam 2: Review of the Accounting Process 139 Questions

Exam 3: The Balance Sheet and Financial Disclosures168 Questions

Exam 4: The Income Statement, Comprehensive Income, and the Statement of Cash Flows178 Questions

Exam 5: Revenue Recognition316 Questions

Exam 6: Time Value of Money Concepts126 Questions

Exam 7: Cash and Receivables187 Questions

Exam 8: Inventories: Measurement182 Questions

Exam 9: Inventories: Additional Issues153 Questions

Exam 10: Property, Plant, and Equipment and Intangible Assets: Acquisition149 Questions

Exam 11: Property, Plant, and Equipment and Intangible Assets: Utilization and Disposition223 Questions

Exam 12: Investments183 Questions

Exam 13: Current Liabilities and Contingencies155 Questions

Exam 14: Bonds and Long-Term Notes256 Questions

Exam 15: Leases262 Questions

Exam 16: Accounting for Income Taxes176 Questions

Exam 17: Pensions and Other Postretirement Benefits246 Questions

Exam 18: Shareholders Equity179 Questions

Exam 19: Share-Based Compensation and Earnings Per Share231 Questions

Exam 20: Accounting Changes and Error Corrections152 Questions

Exam 21: The Statement of Cash Flows Revisited192 Questions

Select questions type

Listed below are five terms followed by a list of phrases that describe or characterize each of the terms. Match each phrase with the correct term.

-Change in depreciation method

(Multiple Choice)

4.7/5  (38)

(38)

The overriding principle for all depreciation methods is that the method must be:

(Multiple Choice)

4.9/5 (42)

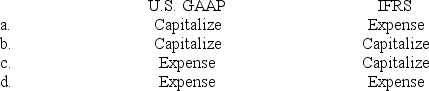

The normal treatment of litigation costs to successfully defend an intangible right under U.S. GAAP and International Financial Reporting Standards (IFRS), respectively, is:

(Multiple Choice)

4.8/5 (33)

Listed below are five terms followed by a list of phrases that describe or characterize each of the terms. Match each phrase with the correct term.

-Group method

(Multiple Choice)

4.7/5 (37)

Gains on the cash sales of property, plant, and equipment:

(Multiple Choice)

4.7/5 (23)

Smithson Ltd. prepares its financial statements according to IFRS. On March 30, 2018, the company purchased a franchise for $3,000,000. The franchise has a 10-year contractual life with no residual value. Smithson uses the straight-line amortization method for all intangible assets. On December 31, 2018, the end of the company's fiscal year, Smithson chooses to revalue the franchise. There is an active market for this particular franchise and its fair value on December 31 is $2,860,000.

Required:

1. Calculate amortization for 2018.

2. Prepare the journal entry to record the revaluation of the patent.

3. Calculate amortization for 2019.

(Essay)

4.8/5 (35)

Archie Co. purchased a framing machine for $45,000 on January 1, 2018. The machine is expected to have a four-year life, with a residual value of $5,000 at the end of four years.

- Using the straight-line method, depreciation for 2019 and book value at December 31, 2019, would be:

(Multiple Choice)

4.8/5 (30)

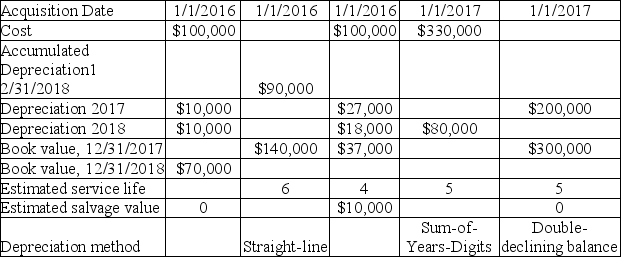

The table below contains data on depreciation for equipment.

Required: Fill in the missing data in the table.

(Essay)

4.8/5 (27)

Canliss Mining uses the replacement method to determine depreciation on its office equipment. During 2016, its first year of operations, office equipment was purchased at a cost of $14,000. Useful life of the equipment averages four years and no salvage value is anticipated. In 2018, equipment costing $5,000 was sold for $600 and replaced with new equipment costing $6,000. Canliss would record 2018 depreciation of:

(Multiple Choice)

4.8/5 (30)

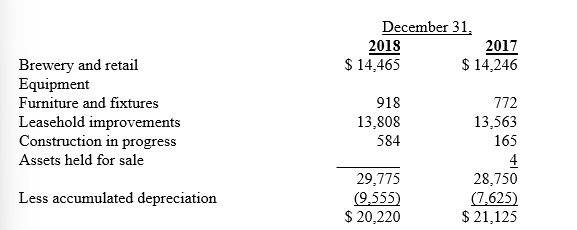

In its 2018 annual report to shareholders, Plank Breweries included the following note:

Property, Plant, and Equipment

Property, plant, and equipment consist of the following (in $ thousands):

Total depreciation expense was approximately $2.121 million and $2.179 million for the years ended December 31, 2018 and 2017, respectively.

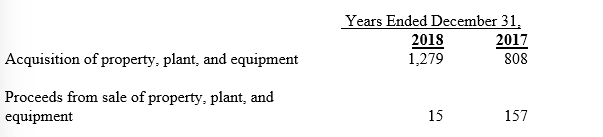

Also, Plank Breweries reported the following information in its annual report (in $ thousands):

Total depreciation expense was approximately $2.121 million and $2.179 million for the years ended December 31, 2018 and 2017, respectively.

Also, Plank Breweries reported the following information in its annual report (in $ thousands):

-Required:

Use a T- account to show the balances and changes during 2018 in Plank Breweries:

Property, plant, and equipment account and Accumulated depreciation-Property, plant, and equipment (PPE) account (in $ thousands).

-Required:

Use a T- account to show the balances and changes during 2018 in Plank Breweries:

Property, plant, and equipment account and Accumulated depreciation-Property, plant, and equipment (PPE) account (in $ thousands).

(Essay)

4.8/5 (41)

Eckland Manufacturing Co. purchased equipment on January 1, 2016, at a cost of $90,000. Straight-line depreciation for 2016 and 2017 was based on an estimated eight-year life and $2,000 estimated residual value. In 2018, Eckland revised its estimate and now believes the equipment will have a total service life of only six years, while the residual value remains the same.

Required:

Compute depreciation for 2018 and 2019.

(Essay)

4.8/5 (41)

Total depreciation is the same over the life of an asset regardless of the method of depreciation used.

(True/False)

5.0/5 (38)

On September 30, 2018, Bricker Enterprises purchased a machine for $200,000. The estimated service life is 10 years with a $20,000 residual value. Bricker records partial-year depreciation based on the number of months in service.

-Depreciation for 2018, using the straight-line method is:

(Multiple Choice)

5.0/5 (46)

Ryan Company purchased a building on January 1, 2018, for $250,000. In addition, during 2018 the following costs related to the building have been incurred:  The amount of expenditures to capitalize for the year (not including the initial purchase of the building) is:

The amount of expenditures to capitalize for the year (not including the initial purchase of the building) is:

(Multiple Choice)

4.9/5 (34)

An asset was acquired on October 1, 2018, for $78,000 with an estimated 5-year life and $13,000 residual value. The company uses units-of-production depreciation and expects the asset to produce 20,000 units. Calculate the gain or loss if the asset was sold on March 31, 2021, for $58,000. Actual production was: 2018=500 units; 2019=3,000 units; 2020=3,500 units; 2021=1,000 units.

(Multiple Choice)

4.8/5 (38)

According to International Financial Reporting Standards (IFRS), the revaluation of equipment when fair value exceeds book value, results in:

(Multiple Choice)

4.9/5 (31)

On March 30, 2018, Calvin Exploration purchased a drilling machine for $840,000. The estimated useful life of the machine is 10 years and no residual value is anticipated. An important component of the machine is the drill housing component that will need to be replaced in five years. The $200,000 cost of the drill housing component is included in the $840,000 cost of the machine. Calvin uses the straight-line depreciation method for all machinery. The company's fiscal year ends on December 31.

Required:

1. Calculate depreciation on the drilling machine for 2018 and 2019 applying the typical U.S. GAAP treatment.

2. Repeat requirement 1 applying IFRS.

(Essay)

4.9/5 (34)

MACRS (modified accelerated cost recovery system) depreciation is equivalent to sum-of-the-years' digits depreciation.

(True/False)

4.8/5 (32)

On September 30, 2018, Bricker Enterprises purchased a machine for $200,000. The estimated service life is 10 years with a $20,000 residual value. Bricker records partial-year depreciation based on the number of months in service.

-Depreciation (to the nearest dollar) for 2018, using sum-of-the-years' digits method, would be:

(Multiple Choice)

4.8/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)