Exam 7: Capital Asset Pricing and Arbitrage Pricing Theory

Exam 1: Investments: Background and Issues75 Questions

Exam 2: Asset Classes and Financial Instruments85 Questions

Exam 3: Securities Markets90 Questions

Exam 4: Mutual Funds and Other Investment Companies85 Questions

Exam 5: Risk and Return: Past and Prologue83 Questions

Exam 6: Efficient Diversification84 Questions

Exam 7: Capital Asset Pricing and Arbitrage Pricing Theory85 Questions

Exam 8: The Efficient Market Hypothesis86 Questions

Exam 9: Behavioral Finance and Technical Analysis87 Questions

Exam 10: Bond Prices and Yields93 Questions

Exam 11: Managing Bond Portfolios85 Questions

Exam 12: Macroeconomic and Industry Analysis89 Questions

Exam 13: Equity Valuation88 Questions

Exam 14: Financial Statement Analysis84 Questions

Exam 15: Options Markets88 Questions

Exam 16: Option Valuation85 Questions

Exam 17: Futures Markets and Risk Management87 Questions

Exam 18: Portfolio Performance Evaluation87 Questions

Exam 19: Globalization and International Investing70 Questions

Exam 20: Hedge Funds60 Questions

Exam 21: Taxes,inflation,and Investment Strategy73 Questions

Exam 22: Investors and the Investment Process81 Questions

Select questions type

Which of the following variables do Fama and French claim do a better job explaining stock returns than beta?

I.Book to market ratio

II.Unexpected change in industrial production

III.Firm size

(Multiple Choice)

4.9/5  (33)

(33)

The expected return of the risky asset portfolio with minimum variance is _________.

(Multiple Choice)

4.7/5 (36)

Research has revealed that regardless of what the current estimate of a firm's beta is,it will tend to move closer to ______ over time.

(Multiple Choice)

4.9/5 (33)

According to the CAPM,what is the market risk premium given an expected return on a security of 13.6%,a stock beta of 1.2,and a risk free interest rate of 4.0%?

(Multiple Choice)

4.8/5 (42)

A stock has a beta of 1.3.The unsystematic risk of this stock is ____________ the stock market as a whole.

(Multiple Choice)

4.8/5 (31)

According to the CAPM,investors are compensated for all but which of the following?

(Multiple Choice)

4.9/5 (40)

Which of the following are assumptions of the simple CAPM model?

I.Individual trades of investors do not affect a stock's price

II.All investors plan for one identical holding period

III.All investors analyze securities in the same way and share the same economic view of the world

IV.All investors have the same level of risk aversion

(Multiple Choice)

4.9/5 (38)

The two factor model on a stock provides a risk premium for exposure to market risk of 12%,a risk premium for exposure to silver commodity prices of 3.5% and a risk free rate of 4.0%.What is the expected return on the stock?

(Multiple Choice)

4.8/5 (30)

What is the alpha of a portfolio with a beta of 2 and actual return of 15%?

(Multiple Choice)

4.7/5 (37)

The measure of unsystematic risk can be found from an index model as _________.

(Multiple Choice)

4.8/5 (42)

The graph of the relationship between expected return and beta in the CAPM context is called the _________.

(Multiple Choice)

4.8/5 (39)

Consider the single factor APT.Portfolio A has a beta of 0.2 and an expected return of 13%.Portfolio B has a beta of 0.4 and an expected return of 15%.The risk-free rate of return is 10%.If you wanted to take advantage of an arbitrage opportunity,you should take a short position in portfolio __________ and a long position in portfolio _________.

(Multiple Choice)

4.9/5 (34)

Consider the following two stocks,A and B.Stock A has an expected return of 10% and a beta of 1.20.Stock B has an expected return of 14% and a beta of 1.80.The expected market rate of return is 9% and the risk-free rate is 5%.Security __________ would be considered a good buy because _________.

(Multiple Choice)

4.8/5 (35)

What is the expected return on a stock with a beta of 0.8,given a risk free rate of 3.5% and an expected market return of 15.5%?

(Multiple Choice)

4.7/5 (45)

In his famous critique of the CAPM,Roll argued that the CAPM ______________.

(Multiple Choice)

4.8/5 (33)

The capital asset pricing model was developed by _________.

(Multiple Choice)

4.9/5 (38)

In the context of the capital asset pricing model,the systematic measure of risk is captured by _________.

(Multiple Choice)

4.9/5 (39)

Investors require a risk premium as compensation for bearing ______________.

(Multiple Choice)

4.8/5 (41)

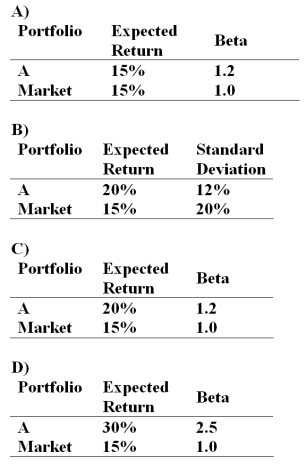

If the simple CAPM is valid and all portfolios are priced correctly,which of the situations below are possible? Consider each situation independently and assume the risk free rate is 5%.

(Multiple Choice)

4.9/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)