Exam7: Materiality and risk

Exam 1: Demand for audit and assurance services74 Questions

Exam 2: Auditors’ legal environment89 Questions

Exam 3: Audit quality and ethics101 Questions

Exam 4: Audit responsibilities and objectives113 Questions

Exam 5: Audit evidence118 Questions

Exam 6: Audit planning and documentation105 Questions

Exam7: Materiality and risk105 Questions

Exam 8: Internal control and control risk119 Questions

Exam 9: Fraud auditing75 Questions

Exam 10: The impact of information technology on the audit process104 Questions

Exam 11: Overall audit plan and audit program105 Questions

Exam 12: Audit of the sales and collection cycle: Tests of controls and substantive tests of transactions120 Questions

Exam 13: Completing tests in the sales and collection cycle: Accounts receivable109 Questions

Exam 14: Audit sampling146 Questions

Exam 15: Audit of transaction cycles and financial statement balances I138 Questions

Exam 16: Audit of transaction cycles and financial statement balances II137 Questions

Exam 17: Completing the audit100 Questions

Exam 18: Audit reporting85 Questions

Exam 19: Other auditing and assurance engagements102 Questions

Select questions type

When management has an adequate level of integrity for the auditor to accept the engagement but cannot be regarded as completely honest in all dealings, auditors normally:

(Multiple Choice)

4.9/5  (38)

(38)

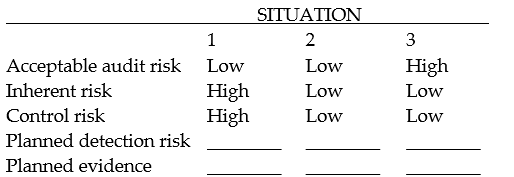

In practice, auditors rarely assign numerical probabilities to inherent risk, control risk, or acceptable audit risk.It is more common to assess these risks as high, medium or low.For each of the four situations below, fill in the blanks for planned detection risk and the amount of evidence you would plan to gather ('planned evidence')using the terms high, medium or low.

(Essay)

4.8/5 (37)

When allocating materiality, most practitioners choose to allocate to:

(Multiple Choice)

5.0/5 (40)

If acceptable audit risk is low and inherent and control risks are high, the amount of evidence required is:

(Multiple Choice)

4.9/5 (30)

The primary purpose of the audit risk model is to aid auditors in planning the extent of tests of controls and determining which particular controls should be tested.

(True/False)

4.9/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)