Exam 9: Costs of Production

Exam 1: The Business Environment and Business Economics44 Questions

Exam 2: Economics and the World of Business48 Questions

Exam 3: Business Organisations50 Questions

Exam 4: The Working of Competitive Markets77 Questions

Exam 5: Business in a Market Environment69 Questions

Exam 6: Demand and the Consumer61 Questions

Exam 7: Demand and the Firm48 Questions

Exam 8: Products, Marketing and Advertising40 Questions

Exam 9: Costs of Production60 Questions

Exam 10: Revenue and Profit43 Questions

Exam 11: Profit Maximisation Under Perfect Competition and Monopoly47 Questions

Exam 12: Profit Maximisation Under Imperfect Competition62 Questions

Exam 13: An Introduction to Business Strategy69 Questions

Exam 14: Alternative Theories of the Firm48 Questions

Exam 15: Growth Strategy63 Questions

Exam 16: The Small-Firm Sector51 Questions

Exam 17: Pricing Strategy50 Questions

Exam 18: Labour Markets, Wages and Industrial Relations85 Questions

Exam 19: Investment and the Employment of Capital55 Questions

Exam 20: Reasons for Government Intervention in the Market89 Questions

Exam 21: Government and the Firm90 Questions

Exam 22: Government and the Market133 Questions

Exam 23: Globalisation and Multinational Business74 Questions

Exam 24: International Trade54 Questions

Exam 25: Trading Blocs56 Questions

Exam 26: The Macroeconomic Environment of Business160 Questions

Exam 27: The Balance of Payments and Exchange Rates107 Questions

Exam 28: Banking, Money and Interest Rates128 Questions

Exam 29: Business Activity, Employment and Inflation197 Questions

Exam 30: Demand-Side Policy123 Questions

Exam 31: Supply-Side Policy64 Questions

Exam 32: International Economic Policy67 Questions

Select questions type

The total physical product for any given amount of the variable factor is the sum of all the marginal physical products up to that point.

Free

(True/False)

4.8/5  (38)

(38)

Correct Answer: Verified

Verified

TRUE

Using a product of your choosing, identify the main fixed and variable costs of production.

Free

(Essay)

4.9/5 (34)

Correct Answer:Verified

The answer will depend on the example chosen. Fixed costs may include rent of factory or machinery, a manger's salary and the cost of some office functions (i.e. any cost that does not vary with output). Variable costs may include workers' wages, raw material costs and transporting products to market (i.e. any cost that does vary with output).

Why does the marginal product curve pass through the top of the average physical product curve?

Free

(Essay)

4.8/5 (45)

Correct Answer:Verified

To the left of this point the MPP is above the APP. Thus extra workers are producing more than the average. They have the effect of pulling the average up. The APP curve must therefore be rising. To the right of this point the MPP is below the APP. Extra workers produce less than the average and thus pull the average down. The APP must be falling.

Which of the following assumptions do we make when constructing long- run cost curves?

(Multiple Choice)

4.7/5 (34)

The 'minimum efficient scale' of operations refers to a scale of output at which

(Multiple Choice)

4.7/5 (40)

Which of the following represents the point at which diminishing returns will set in?

(Multiple Choice)

4.8/5 (33)

When counting the cost of a product to the firm making it, we should value inputs at their

(Multiple Choice)

4.7/5 (35)

With L representing the quantity of labour, which of the following is the formula for the marginal physical productivity of labour?

(Multiple Choice)

4.9/5 (34)

Which of the following is a correct statement about the relationship between average product (AP) and marginal product (MP)?

(Multiple Choice)

4.7/5 (36)

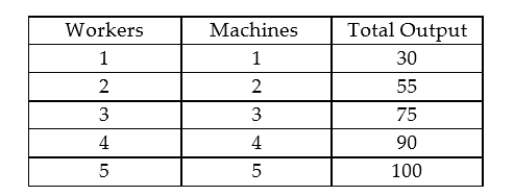

The following table provides information about the relationship between a firm's output and its factors of production in the short run:

Which one of the following statements describes the situation in this firm?

Which one of the following statements describes the situation in this firm?

(Multiple Choice)

4.9/5 (34)

If firm X benefits from research and development conducted by other firms in the industry, then this is an example of an external economy of scale for firm X.

(True/False)

4.9/5 (24)

In the short run, by definition, at least one factor is fixed in supply. The total cost to the firm of these factors is thus fixed with respect to time.

(True/False)

4.9/5 (34)

If a doubling of inputs leads to a doubling of output, the firm is said to experience decreasing returns to scale.

(True/False)

4.8/5 (32)

Economies of scale explain the falling part of a firm's SRATC curve.

(True/False)

4.9/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)