Exam 17: Audit Sampling for Tests of Details of Balances

Exam 1: The Demand for Audit and Other Assurance Services47 Questions

Exam 2: The Cpa Profession79 Questions

Exam 3: Audit Reports140 Questions

Exam 4: Professional Ethics119 Questions

Exam 5: Legal Liability115 Questions

Exam 6: Audit Responsibilities and Objectives132 Questions

Exam 7: Audit Evidence105 Questions

Exam 8: Audit Planning and Analytical Procedures102 Questions

Exam 9: Materiality and Risk113 Questions

Exam 10: Internal Control, Control Risk, and Section 404 Audits116 Questions

Exam 11: Fraud Auditing93 Questions

Exam 12: The Impact of Information Technology on the Audit Process106 Questions

Exam 13: Overall Audit Strategy and Audit Program94 Questions

Exam 14: Audit of the Sales and Collection Cycle: Tests of Controls and Substantive Tests of Transactions109 Questions

Exam 15: Audit Sampling for Tests of Controls and Substantive Tests of Transactions119 Questions

Exam 16: Completing the Tests in the Sales and Collection Cycle: Accounts Receivable101 Questions

Exam 17: Audit Sampling for Tests of Details of Balances114 Questions

Exam 18: Audit of the Acquisition and Payment Cycle: Tests of Controls, Substantive Tests of Transactions, and Accounts Payable116 Questions

Exam 19: Completing the Tests in the Acquisition and Payment Cycle: Verification of Selected Accounts101 Questions

Exam 20: Audit of the Payroll and Personnel Cycle113 Questions

Exam 21: Audit of the Inventory and Warehousing Cycle116 Questions

Exam 22: Audit of the Capital Acquisition and Repayment Cycle91 Questions

Exam 23: Audit of Cash and Financial Instruments121 Questions

Exam 24: Completing the Audit120 Questions

Exam 25: Other Assurance Services104 Questions

Exam 26: Internal and Governmental Financial Auditing and Operational Auditing73 Questions

Select questions type

If acceptable audit risk is increased, acceptable risk of incorrect acceptance should be:

(Multiple Choice)

4.8/5  (39)

(39)

Stratified sampling is applicable to difference, mean-per-unit, and ratio estimation, but it is most commonly used with:

(Multiple Choice)

4.8/5 (44)

Which balance-related audit objective cannot be assessed using monetary unit sampling?

(Multiple Choice)

4.7/5 (37)

Acceptable risk of incorrect acceptance is directly affected by acceptable audit risk.

(True/False)

4.8/5 (28)

If an auditor concludes that internal controls are likely to be effective, the preliminary assessment of control risk can be reduced, leading to which of the following impacts on the acceptable risk of incorrect acceptance?

(Multiple Choice)

4.8/5 (44)

Discuss the advantages and disadvantages of monetary-unit sampling over other sampling methods.

(Essay)

4.8/5 (40)

For stratified sampling, the auditor selects samples independently from each stratum.

(True/False)

4.8/5 (43)

As the amount of misstatements expected in the population approaches tolerable misstatement, the planned sample size will:

(Multiple Choice)

4.7/5 (27)

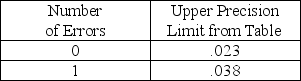

The auditor must deal with layers of the computed upper deviation rate from the attributes table because there are different error assumptions for each error.Assume a sample of 100 had found one error, and the computed upper deviation rate is shown in the following table:  The precision limit for the layer with one error is:

The precision limit for the layer with one error is:

(Multiple Choice)

4.9/5 (35)

The use of monetary unit sampling is most appropriate when the auditor expects to find many errors and when a monetary result is desired.

(True/False)

4.9/5 (39)

When auditors apply MUS to a sample, the sample is selected using random sampling techniques.

(True/False)

4.8/5 (32)

The primary factor affecting the auditor's decision about acceptable risk of incorrect acceptance (ARIA)is assessed inherent risk.

(True/False)

4.9/5 (43)

MUS has the statistical simplicity of attributes sampling, yet provides a statistical result expressed as a percentage.

(True/False)

4.7/5 (36)

While performing a substantive test of details during an audit, the auditor determined that the sample results supported the conclusion that the recorded account balance was materially misstated.Which of the following is the least likely auditor reaction to this discovery?

(Multiple Choice)

4.8/5 (45)

The auditor is concerned with the audited value rather than the error amount of each item in the sample when using:

(Multiple Choice)

4.8/5 (45)

Explain the decision rule used in monetary unit sampling to determine whether the population is acceptable.

(Essay)

4.8/5 (40)

While performing a substantive test of details during an audit, the auditor determined that the sample results supported the conclusion that the recorded account balance was not materially misstated.It was, in fact, materially misstated.This situation illustrates the risk of:

(Multiple Choice)

5.0/5 (43)

Match six of the terms (a-l)with the definitions provided below (1-6):

Correct Answer: Verified

Verified

Premises:

Responses:

(Matching)

4.9/5 (35)

Calculating the sample size using monetary unit sampling depends on which of the following factors?

(Multiple Choice)

4.8/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)