Exam 11: Return and Risk: the Capital Asset Pricing Model Capm

Exam 1: Introduction to Corporate Finance67 Questions

Exam 2: Financial Statements and Cash Flow94 Questions

Exam 3: Financial Statements Analysis and Financial Models120 Questions

Exam 4: Discounted Cash Flow Valuation134 Questions

Exam 5: Net Present Value and Other Investment Rules105 Questions

Exam 6: Making Capital Investment Decisions101 Questions

Exam 7: Risk Analysis, Real Options, and Capital Budgeting99 Questions

Exam 8: Interest Rates and Bond Valuation69 Questions

Exam 9: Stock Valuation77 Questions

Exam 10: Risk and Return: Lessons From Market History84 Questions

Exam 11: Return and Risk: the Capital Asset Pricing Model Capm136 Questions

Exam 12: An Alternative View of Risk and Return: The Arbitrage Pricing Theory51 Questions

Exam 13: Risk, Cost of Capital, and Valuation59 Questions

Exam 14: Efficient Capital Markets and Behavioral Challenges65 Questions

Exam 15: Long-Term Financing46 Questions

Exam 16: Capital Structure: Basic Concepts91 Questions

Exam 17: Capital Structure: Limits to the Use of Debt74 Questions

Exam 18: Valuation and Capital Budgeting for the Levered Firm57 Questions

Exam 19: Dividends and Other Payouts90 Questions

Exam 20: Raising Capital73 Questions

Exam 21: Leasing55 Questions

Exam 22: Options and Corporate Finance95 Questions

Exam 23: Options and Corporate Finance: Extensions and Applications46 Questions

Exam 24: Warrants and Convertibles58 Questions

Exam 25: Derivatives and Hedging Risk66 Questions

Exam 26: Short-Term Finance and Planning124 Questions

Exam 27: Cash Management59 Questions

Exam 28: Credit and Inventory Management61 Questions

Exam 29: Mergers, Acquisitions, and Divestitures83 Questions

Exam 30: Financial Distress52 Questions

Exam 31: International Corporate Finance95 Questions

Select questions type

The _____ tells us that the expected return on a risky asset depends only on that asset's nondiversifiable risk.

(Multiple Choice)

4.9/5  (38)

(38)

Which one of the following is an example of systematic risk?

(Multiple Choice)

4.8/5 (33)

We routinely assume that investors are risk-averse return-seekers; i.e.,they like returns and dislike risk. If so,why do we contend that only systematic risk and not total risk is important?

(Essay)

4.8/5 (31)

A portfolio contains four assets. Asset 1 has a beta of .8 and comprises 30% of the portfolio. Asset 2 has a beta of 1.1 and comprises 30% of the portfolio. Asset 3 has a beta of 1.5 and comprises 20% of the portfolio. Asset 4 has a beta of 1.6 and comprises the remaining 20% of the portfolio. If the riskless rate is expected to be 3% and the market risk premium is 6%,what is the beta of the portfolio?

(Multiple Choice)

4.9/5 (36)

A risk that affects a large number of assets,each to a greater or lesser degree is called:

(Multiple Choice)

4.8/5 (44)

The Rotor Co. stock is expected to earn 16% in a recession,7% in a normal economy,and lose 3% in a booming economy. The probability of a boom is 20% while the probability of a normal economy is 55% and the chance of a recession is 25%. What is the expected rate of return on this stock?

(Multiple Choice)

4.8/5 (37)

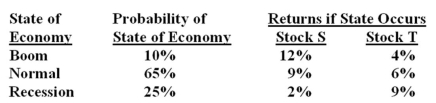

What is the standard deviation of a portfolio which is comprised of $4,500 invested in stock S and $3,000 in stock T?

(Multiple Choice)

4.8/5 (45)

The relationship between the covariance of the security with the market to the variance is called the:

(Multiple Choice)

4.8/5 (34)

You want your portfolio beta to be 1.20. Currently,your portfolio consists of $100 invested in stock A with a beta of 1.4 and $300 in stock B with a beta of .6. You have another $400 to invest and want to divide it between an asset with a beta of 1.6 and a risk-free asset. How much should you invest in the risk-free asset?

(Multiple Choice)

4.9/5 (35)

The excess return earned by an asset that has a beta of 1.0 over that earned by a risk-free asset is referred to as the:

(Multiple Choice)

4.9/5 (34)

The combination of the efficient set of portfolios with a riskless lending and borrowing rate results in:

(Multiple Choice)

4.8/5 (38)

Zoom,Inc. stock has a beta of 1.5. The risk-free rate of return is 3.7% and the market rate of return is 9.5%. What is the amount of the risk premium on Zoom stock?

(Multiple Choice)

4.8/5 (41)

You have a portfolio of two risky stocks which turns out to have no diversification benefit. The reason you have no diversification is the returns:

(Multiple Choice)

4.7/5 (41)

The majority of the benefits from portfolio diversification can generally be achieved with just _____ diverse securities.

(Multiple Choice)

4.9/5 (39)

A portfolio contains two assets. The first asset comprises 40% of the portfolio and has a beta of 1.2. The other asset has a beta of 1.5. The portfolio beta is:

(Multiple Choice)

4.8/5 (35)

Diversification can effectively reduce risk. Once a portfolio is diversified,the type of risk remaining is:

(Multiple Choice)

4.7/5 (28)

Your portfolio is comprised of 30% of stock X,50% of stock Y,and 20% of stock Z. Stock X has a beta of .64,stock Y has a beta of 1.48,and stock Z has a beta of 1.04. What is the beta of your portfolio?

(Multiple Choice)

4.9/5 (33)

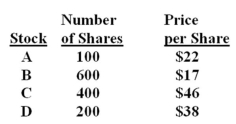

You own the following portfolio of stocks. What is the portfolio weight of stock C?

(Multiple Choice)

4.8/5 (41)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)