Exam 3: Consolidations-Subsequent to the Date of Acquisition

Exam 1: The Equity Method of Accounting for Investments121 Questions

Exam 2: Consolidation of Financial Information117 Questions

Exam 3: Consolidations-Subsequent to the Date of Acquisition124 Questions

Exam 4: Consolidated Financial Statements and Outside Ownership117 Questions

Exam 5: Consolidated Financial Statementsintra-Entity Asset Transactions127 Questions

Exam 6: Variable Interest Entities, Intra-Entity Debt, Consolidated Cash Flows, and Other Issues115 Questions

Exam 7: Foreign Currency Transactions and Hedging Foreign Exchange Risk93 Questions

Exam 8: Translation of Foreign Currency Financial Statements97 Questions

Exam 9: Partnerships: Formation and Operation88 Questions

Exam 10: Partnerships: Termination and Liquidation73 Questions

Exam 11: Accounting for State and Local Governments, Part I78 Questions

Exam 12: Accounting for State and Local Governments, Part II49 Questions

Select questions type

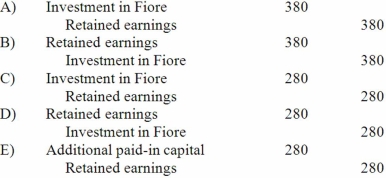

Kaye Company acquired 100% of Fiore Company on January 1, 2013. Kaye paid $1,000 excess consideration over book value which is being amortized at $20 per year. Fiore reported net income of $400 in 2013 and paid dividends of $100. Assume the initial value method is used. In the year subsequent to acquisition, what additional worksheet entry must be made for consolidation purposes that is not required for the equity method?

(Multiple Choice)

4.7/5  (40)

(40)

Jaynes Inc. acquired all of Aaron Co.'s common stock on January 1, 2012, by issuing 11,000 shares of $1 par value common stock. Jaynes' shares had a $17 per share fair value. On that date, Aaron reported a net book value of $120,000. However, its equipment (with a five-year remaining life) was undervalued by $6,000 in the company's accounting records. Any excess of consideration transferred over fair value of assets and liabilities is assigned to an unrecorded patent to be amortized over ten years. The following figures came from the individual accounting records of these two companies as of December 31,2012:

Jaynes Inc. Aaron Co. Revenues 720,000 \ 276,000 Expenses 528,000 144,000 Investment income Not given - Dividends paid 100,000 60,000

The following figures came from the individual accounting records of these two companies as of December 31,2013:

Jaynes Inc. Aaron Co. Revenues 840,000 336,000 Expenses 552,000 180,000 Investment income Not given - Dividends paid 110,000 50,000 Equipment 600,000 360,000 Retained earnings, 12/31/13 balance 960,000 216,000 What was the total for consolidated patents as of December 31, 2013?

(Essay)

4.9/5 (36)

Perry Company acquires 100% of the stock of Hurley Corporation on January 1, 2012, for $3,800 cash. As of that date Hurley has the following trial balance; Debit Credit Cash \ 500 Accounts receivable 600 Inventory 800 Buildings (net) (5 year life) 1,500 Equipment (net) (2 year life) 1,000 Land 900 Accounts payable \ 400 Long -term liabilities (due 12/31/15) 1,800 Common stock 1,000 Additional paid -in capital 600 Retained earnings 1,500 Total \5 ,300 \5 ,300

Net income \ 120 Dividends 30 40

Fair Value Inventory \ 900 Buildings 1,200 Equipment 1,250 Land 1,300 Long -term liabilities 1,700 Any excess of consideration transferred over fair value of net assets acquired is considered goodwill with an indefinite life. FIFO inventory valuation method is used. Compute the amount of Hurley's inventory that would be reported in a January 1, 2012, consolidated balance sheet.

(Multiple Choice)

4.8/5 (36)

When a company applies the partial equity method in accounting for its investment in a subsidiary and the subsidiary's equipment has a fair value greater than its book value, what consolidation worksheet entry is made in a year subsequent to the initial acquisition of the subsidiary?

A.Retained earnings

Investment in subsidiary

B. Investment in subsidiary

Retained earnings

C. Investment in subsidiary

Equity in subsidiary's income

D. Investment in subsidiary

Additional paid-in capital

E. Retained earnings

Additional paid-in capital

(Multiple Choice)

4.7/5 (38)

When consolidating a subsidiary under the equity method, which of the following statements is true?

(Multiple Choice)

4.9/5 (39)

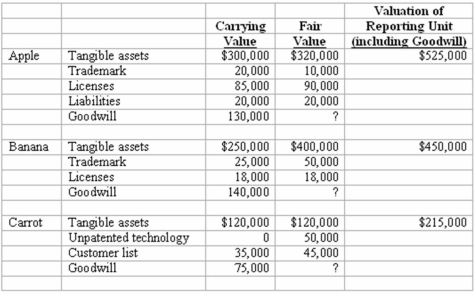

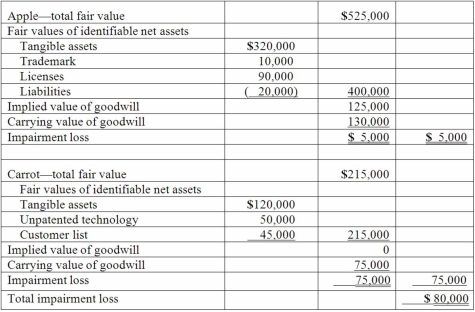

Pritchett Company recently acquired three businesses, recognizing goodwill in each acquisition. Destin has allocated its acquired goodwill to its three reporting units: Apple, Banana, and Carrot. Pritchett provides the following information in performing the 2013 annual review for impairment:  How much goodwill impairment should Pritchett report for 2013?

Goodwill Impairment Test-Step 2 (Apple and Carrot only)

How much goodwill impairment should Pritchett report for 2013?

Goodwill Impairment Test-Step 2 (Apple and Carrot only)

(Essay)

4.9/5 (36)

Jaynes Inc. acquired all of Aaron Co.'s common stock on January 1, 2012, by issuing 11,000 shares of $1 par value common stock. Jaynes' shares had a $17 per share fair value. On that date, Aaron reported a net book value of $120,000. However, its equipment (with a five-year remaining life) was undervalued by $6,000 in the company's accounting records. Any excess of consideration transferred over fair value of assets and liabilities is assigned to an unrecorded patent to be amortized over ten years.

The following figures came from the individual accounting records of these two companies as of December 31,2012:

Jaynes Inc. Aaron Co. Revenues 720,000 \ 276,000 Expenses 528,000 144,000 Investment income Not given - Dividends paid 100,000 60,000

The following figures came from the individual accounting records of these two companies as of December 31,2013:

Jaynes Inc. Aaron Co. Revenues 840,000 336,000 Expenses 552,000 180,000 Investment income Not given - Dividends paid 110,000 50,000 Equipment 600,000 360,000 Retained earnings, 12/31/13 balance 960,000 216,000 What balance would Jaynes' Investment in Aaron Co. account have shown on December 31, 2012, when the equity method was applied for this acquisition?

An allocation of the acquisition value (based on the fair value of the shares issued) must first be made.

(Essay)

4.8/5 (38)

Watkins, Inc. acquires all of the outstanding stock of Glen Corporation on January 1, 2012. At that date, Glen owns only three assets and has no liabilities: If Watkins pays $300,000 in cash for Glen, at what amount would the subsidiary's Building be represented in a January 2, 2012 consolidation?

(Multiple Choice)

4.7/5 (38)

Following are selected accounts for Green Corporation and Vega Company as of December 31, 2015. Several of Green's accounts have been omitted. Green Vega Revenues \ 900,000 \ 500,000 Cost of goods sold 360,000 200,000 Depreciation expense 140,000 40,000 Other expenses 100,000 60,000 Equity in Vega's income ? Retained earnings, 1/1/15 1,350,000 1,200,000 Dividends 195,000 80,000 Current assets 300,000 1,380,000 Land 450,000 180,000 Building (net) 750,000 280,000 Equipment (net) 300,000 500,000 Liabilities 600,000 620,000 Common stock 450,000 80,000 Additional paid-in capital 75,000 320,000 Green acquired 100% of Vega on January 1, 2011, by issuing 10,500 shares of its $10 par value common stock with a fair value of $95 per share. On January 1, 2011, Vega's land was undervalued by $40,000, its buildings were overvalued by $30,000, and equipment was undervalued by $80,000. The buildings have a 20-year life and the equipment has a 10-year life. $50,000 was attributed to an unrecorded trademark with a 16-year remaining life. There was no goodwill associated with this investment. Compute the December 31, 2015, consolidated buildings.

(Multiple Choice)

5.0/5 (40)

Goehler, Inc. acquires all of the voting stock of Kenneth, Inc. on January 4, 2012, at an amount in excess of Kenneth's fair value. On that date, Kenneth has equipment with a book value of $90,000 and a fair value of $120,000 (10-year remaining life). Goehler has equipment with a book value of $800,000 and a fair value of $1,200,000 (10-year remaining life). On December 31, 2013, Goehler has equipment with a book value of $975,000 but a fair value of $1,350,000 and Kenneth has equipment with a book value of $105,000 but a fair value of $125,000. If Goehler applies the equity method in accounting for Kenneth, what is the consolidated balance for the Equipment account as of December 31, 2013?

(Multiple Choice)

4.8/5 (35)

One company acquires another company in a combination accounted for as an acquisition. The acquiring company decides to apply the initial value method in accounting for the combination. What is one reason the acquiring company might have made this decision?

(Multiple Choice)

4.9/5 (34)

According to GAAP regarding amortization of goodwill and other intangible assets, which of the following statements is true?

(Multiple Choice)

4.9/5 (42)

Perry Company acquires 100% of the stock of Hurley Corporation on January 1, 2012, for $3,800 cash. As of that date Hurley has the following trial balance; Debit Credit Cash \ 500 Accounts receivable 600 Inventory 800 Buildings (net) (5 year life) 1,500 Equipment (net) (2 year life) 1,000 Land 900 Accounts payable \ 400 Long -term liabilities (due 12/31/15) 1,800 Common stock 1,000 Additional paid -in capital 600 Retained earnings 1,500 Total \5 ,300 \5 ,300

Net income \ 120 Dividends 30 40

Fair Value Inventory \ 900 Buildings 1,200 Equipment 1,250 Land 1,300 Long -term liabilities 1,700 Any excess of consideration transferred over fair value of net assets acquired is considered goodwill with an indefinite life. FIFO inventory valuation method is used. Compute the amount of Hurley's long-term liabilities that would be reported in a December 31, 2013, consolidated balance sheet.

(Multiple Choice)

4.8/5 (36)

On 4/1/11, Sey Mold Corporation acquired 100% of DotDot.Com for $2,000,000 cash. On the date of acquisition, DotDot's net book value was $900,000. DotDot's assets included land that was undervalued by $300,000, a building that was undervalued by $400,000, and equipment that was overvalued by $50,000. The building had a remaining useful life of 8 years and the equipment had a remaining useful life of 4 years. Any excess fair value over consideration transferred is allocated to an undervalued patent and is amortized over 5 years.

Determine the amortization expense related to the consolidation at the year-end date of 12/31/19.

(Essay)

4.7/5 (48)

Factors that should be considered in determining the useful life of an intangible asset include

(Multiple Choice)

4.7/5 (43)

Following are selected accounts for Green Corporation and Vega Company as of December 31, 2015. Several of Green's accounts have been omitted. Green Vega Revenues \ 900,000 \ 500,000 Cost of goods sold 360,000 200,000 Depreciation expense 140,000 40,000 Other expenses 100,000 60,000 Equity in Vega's income ? Retained earnings, 1/1/15 1,350,000 1,200,000 Dividends 195,000 80,000 Current assets 300,000 1,380,000 Land 450,000 180,000 Building (net) 750,000 280,000 Equipment (net) 300,000 500,000 Liabilities 600,000 620,000 Common stock 450,000 80,000 Additional paid-in capital 75,000 320,000 Green acquired 100% of Vega on January 1, 2011, by issuing 10,500 shares of its $10 par value common stock with a fair value of $95 per share. On January 1, 2011, Vega's land was undervalued by $40,000, its buildings were overvalued by $30,000, and equipment was undervalued by $80,000. The buildings have a 20-year life and the equipment has a 10-year life. $50,000 was attributed to an unrecorded trademark with a 16-year remaining life. There was no goodwill associated with this investment. Compute the December 31, 2015, consolidated equipment.

(Multiple Choice)

4.9/5 (45)

Which of the following statements is false regarding push-down accounting?

(Multiple Choice)

4.7/5 (38)

Watkins, Inc. acquires all of the outstanding stock of Glen Corporation on January 1, 2012. At that date, Glen owns only three assets and has no liabilities: If Watkins pays $450,000 in cash for Glen, at what amount would Glen's Inventory acquired be represented in a December 31, 2012 consolidated balance sheet?

(Multiple Choice)

4.9/5 (38)

Prince Company acquires Duchess, Inc. on January 1, 2011. The consideration transferred exceeds the fair value of Duchess' net assets. On that date, Prince has a building with a book value of $1,200,000 and a fair value of $1,500,000. Duchess has a building with a book value of $400,000 and fair value of $500,000. If push-down accounting is not used, what amounts in the Building account appear on Duchess' separate balance sheet and on the consolidated balance sheet immediately after acquisition?

(Multiple Choice)

4.8/5 (37)

Jaynes Inc. acquired all of Aaron Co.'s common stock on January 1, 2012, by issuing 11,000 shares of $1 par value common stock. Jaynes' shares had a $17 per share fair value. On that date, Aaron reported a net book value of $120,000. However, its equipment (with a five-year remaining life) was undervalued by $6,000 in the company's accounting records. Any excess of consideration transferred over fair value of assets and liabilities is assigned to an unrecorded patent to be amortized over ten years. The following figures came from the individual accounting records of these two companies as of December 31,2012:

Jaynes Inc. Aaron Co. Revenues 720,000 \ 276,000 Expenses 528,000 144,000 Investment income Not given - Dividends paid 100,000 60,000

The following figures came from the individual accounting records of these two companies as of December 31,2013:

Jaynes Inc. Aaron Co. Revenues 840,000 336,000 Expenses 552,000 180,000 Investment income Not given - Dividends paid 110,000 50,000 Equipment 600,000 360,000 Retained earnings, 12/31/13 balance 960,000 216,000 What was consolidated equipment as of December 31, 2013?

(Essay)

4.9/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)