Exam 20: Forming and Operating Partnerships

Exam 1: An Introduction to Tax111 Questions

Exam 2: Tax Compliance, the Irs, and Tax Authorities111 Questions

Exam 3: Tax Planning Strategies and Related Limitations110 Questions

Exam 4: Individual Income Tax Overview, Exemptions, and Filing Status126 Questions

Exam 5: Gross Income and Exclusions131 Questions

Exam 6: Individual Deductions114 Questions

Exam 7: Individual Income Tax Computation and Tax Credits156 Questions

Exam 8: Business Income, Deductions, and Accounting Methods99 Questions

Exam 9: Property Acquisition and Cost Recovery105 Questions

Exam 10: Property Dispositions110 Questions

Exam 11: Investments104 Questions

Exam 12: Compensation102 Questions

Exam 13: Retirement Savings and Deferred Compensation115 Questions

Exam 14: Tax Consequences of Home Ownership115 Questions

Exam 15: Entities Overview70 Questions

Exam 16: Corporate Operations140 Questions

Exam 17: Accounting for Income Taxes100 Questions

Exam 18: Corporate Taxation: Nonliquidating Distributions100 Questions

Exam 19: Corporate Formation, Reorganization, and Liquidation98 Questions

Exam 20: Forming and Operating Partnerships105 Questions

Exam 21: Dispositions of Partnership Interests and Partnership Distributions101 Questions

Exam 22: S Corporations117 Questions

Exam 23: State and Local Taxes117 Questions

Exam 24: The Us Taxation of Multinational Transactions99 Questions

Exam 25: Transfer Taxes and Wealth Planning of the Cfa Institute123 Questions

Select questions type

Sarah, Sue, and AS Inc. formed a partnership on May 1, 20X9 called SSAS, LP. Now that the partnership is formed, they must determine its appropriate year-end. Sarah has a 30% profits and capital interest while Sue has a 35% profits and capital interest. Both Sarah and Sue have calendar year-ends. AS Inc. holds the remaining profits and capital interest in the LP, and it has a September 30 year-end. What tax year-end must SSAS, LP use for 20X9 and which test or rule requires this year-end?

Free

(Multiple Choice)

4.8/5  (43)

(43)

Correct Answer: Verified

Verified

B

A partnership can request a five month extension by filing Form 7004 prior to the original due date of the partnership return.

Free

(True/False)

4.9/5 (39)

Correct Answer:Verified

True

Tax elections are rarely made at the partnership level.

Free

(True/False)

4.8/5 (39)

Correct Answer:Verified

False

Kim received a 1/3 profits and capital interest in Bright Line, LLC in exchange for legal services she provided. In addition to her share of partnership profits or losses, she receives a $30,000 guaranteed payment each year for ongoing services she provides to the LLC. For X4, Bright Line reported the following revenues and expenses: Sales - $150,000, Cost of Goods Sold - $90,000, Depreciation Expense - $45,000, Long-Term Capital Gains - $15,000, Qualifying Dividends - $6,000, and Municipal Bond Interest - $3,000. How much ordinary business income (loss) will Bright Line allocate to Kim on her Schedule K-1 for X4?

(Multiple Choice)

4.8/5 (33)

The main difference between a partner's tax basis and at-risk amount is that qualified nonrecourse financing is not included in the at-risk amount.

(True/False)

4.7/5 (40)

What is the rationale for the specific rules partnerships must follow in determining a partnership's taxable year-end?

(Multiple Choice)

4.8/5 (38)

Illuminating Light Partnership had the following revenues, expenses, gains, losses, and distributions: Sales Long-Term Capital Gain Qualified Dividends Cost of Goods Sold Employee Wages Guaranteed Payment to Managing Partner Municipal Bond Interest Section 179 Expense MACRS Depreciation Section 1231 Gains Fines and Penalties \ 60,000 \ 8,000 \ 5,000 \ 40,000 \ 15,000 \ 25,000 \ 5,000 \ 10,000 \ 8,000 \ 3,000 \ 1,500 Given these items, what is Illuminating Light's ordinary business income (loss) for the year?

(Essay)

5.0/5 (36)

On April 18, 20X8, Robert sold his 35 percent partnership interest in Fruit Wonder, LLC to Richard for $120,000. Prior to selling his interest, Robert had a basis in Fruit Wonder of $80,000. Robert's basis included $5,000 of recourse debt and $15,000 of nonrecourse debt that had been allocated to him. Immediately after the purchase, what is Richard's tax basis in Fruit Wonder?

(Essay)

4.9/5 (38)

Under proposed rules issued by the IRS, in which of the following situations should an LLC member be treated as a general partner for self-employment tax purposes?

(Multiple Choice)

4.8/5 (36)

Frank and Bob are equal members in Soxy Socks, LLC. When forming the LLC, Frank contributed $50,000 in cash and $50,000 worth of equipment. Frank's adjusted basis in the equipment was $35,000. Bob contributed $50,000 in cash and $50,000 worth of land. Bob's adjusted basis in the land was $30,000. On 3/15/X4, Soxy Socks sells the land Bob contributed for $60,000. How much gain (loss) related to this transaction will Bob report on his X4 return?

(Multiple Choice)

4.8/5 (42)

What is the difference between a partner's tax basis and at-risk amount?

(Essay)

4.8/5 (44)

Income earned by flow-through entities is usually taxed once at the entity level.

(True/False)

4.8/5 (33)

On March 15, 20X9, Troy, Peter, and Sarah formed Picture Perfect general partnership. This partnership was created to sell a variety of cameras, picture frames, and other photography accessories. When it was formed, the partners received equal profits and capital interests and the following items were contributed by each partner:

• Troy - cash of $3,000, inventory with a FMV and tax basis of $5,000, and a building with a FMV of $22,000 and adjusted basis of $10,000. Additionally, the building was secured by a $10,000 nonrecourse mortgage.

• Peter - cash of $5,000, accounts payable of $12,000 (recourse debt for which each partner becomes equally responsible), and land with a FMV of $27,000 and tax basis of $20,000.

• Sarah - cash of $2,000, accounts receivable with a FMV and tax basis of $1,000, and equipment with a FMV of $40,000 and adjusted basis of $3,500. Sarah also contributed a $23,000 nonrecourse note payable secured by the equipment.

What is each partner's outside basis and how much gain (loss) must the partners recognize in 20X9 when Picture Perfect was formed?

(Essay)

4.7/5 (33)

What is the difference between the aggregate and entity theory of partnership taxation? Provide two examples of how partnership tax rules reflect the aggregate theory and two examples of how they reflect the entity theory.

(Essay)

4.7/5 (42)

Explain why partners must increase their tax basis for their share of partnership taxable and nontaxable income or gain and reduce their basis by their share of partnership deductible and nondeductible expenses or losses?

(Essay)

4.8/5 (38)

At the end of year 1, Tony had a tax basis of $40,000 in Tall Ladders, Limited Partnership. Tony has a 20 percent profits interest in Tall Ladders. For year 2, Tall Ladders will pay Tony a $10,000 guaranteed payment for extra services he provides to the partnership. Given the following Income Statement and Balance Sheet from Tall Ladders, what is Tony's adjusted tax basis at the end of year 2?

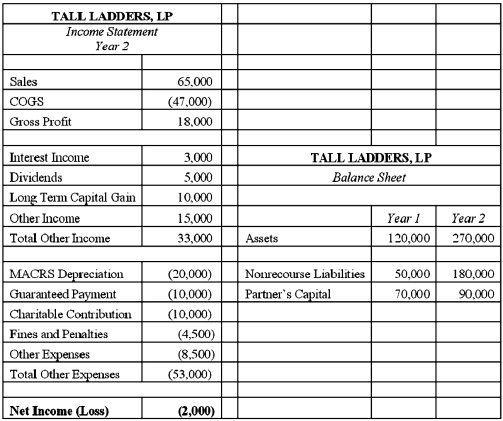

(Essay)

4.9/5 (40)

Which person would generally be treated as a material participant in an activity?

(Multiple Choice)

4.9/5 (32)

Adjustments to a partner's outside basis are made annually to prevent double taxation on the sale of a partnership interest or at the time of a partnership distribution.

(True/False)

4.8/5 (33)

Partnerships can use special allocations to shift built-in gains and built-in losses on contributed property from a partner who contributed the property to other partners.

(True/False)

4.9/5 (44)

If a partner participates in partnership activities on a regular, continuous, and substantial basis, then the partnership's activities with respect to this individual partner are not considered passive.

(True/False)

4.8/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)