Exam 20: Forming and Operating Partnerships

Exam 1: An Introduction to Tax111 Questions

Exam 2: Tax Compliance, the Irs, and Tax Authorities111 Questions

Exam 3: Tax Planning Strategies and Related Limitations110 Questions

Exam 4: Individual Income Tax Overview, Exemptions, and Filing Status126 Questions

Exam 5: Gross Income and Exclusions131 Questions

Exam 6: Individual Deductions114 Questions

Exam 7: Individual Income Tax Computation and Tax Credits156 Questions

Exam 8: Business Income, Deductions, and Accounting Methods99 Questions

Exam 9: Property Acquisition and Cost Recovery105 Questions

Exam 10: Property Dispositions110 Questions

Exam 11: Investments104 Questions

Exam 12: Compensation102 Questions

Exam 13: Retirement Savings and Deferred Compensation115 Questions

Exam 14: Tax Consequences of Home Ownership115 Questions

Exam 15: Entities Overview70 Questions

Exam 16: Corporate Operations140 Questions

Exam 17: Accounting for Income Taxes100 Questions

Exam 18: Corporate Taxation: Nonliquidating Distributions100 Questions

Exam 19: Corporate Formation, Reorganization, and Liquidation98 Questions

Exam 20: Forming and Operating Partnerships105 Questions

Exam 21: Dispositions of Partnership Interests and Partnership Distributions101 Questions

Exam 22: S Corporations117 Questions

Exam 23: State and Local Taxes117 Questions

Exam 24: The US Taxation of Multinational Transactions99 Questions

Exam 25: Transfer Taxes and Wealth Planning of the Cfa Institute123 Questions

Select questions type

In X1, Adam and Jason formed ABC, LLC, a car dealership in Kansas City. In X2, Adam and Jason realized they needed an advertising expert to assist in their business. Thus, the two members offered Cory, a marketing expert, a 1/3 capital interest in their partnership for contributing his expert services. Cory agreed to this arrangement and received his capital interest in X2. If the value of the LLC's capital equals $180,000 when Cory receives his 1/3 capital interest, which of the following tax consequences does not occur in X2?

Free

(Multiple Choice)

4.7/5  (34)

(34)

Correct Answer: Verified

Verified

B

A partner's self-employment earnings (loss) may be affected by her share of ordinary business income (loss) and any guaranteed payments she receives. The impact of these amounts typically depends on the status of the partner. Which of the following statements correctly describes the effect these items have on the partner's self-employment earnings (loss)?

Free

(Multiple Choice)

4.8/5 (38)

Correct Answer:Verified

E

TQK, LLC provides consulting services and was formed on 1/31/X5. Aaron and ABC, Inc. each hold a 50% capital and profits interest in TQK. If TQK averaged $7,000,000 in annual gross receipts over the last three years, what accounting method can TQK use for X9?

Free

(Multiple Choice)

5.0/5 (37)

Correct Answer:Verified

A

Gerald received a 33% capital and profit (loss) interest in XYZ Limited Partnership (LP). In exchange for this interest, Gerald contributed a building with a FMV of $30,000. His adjusted basis in the building was $15,000. In addition, the building was encumbered with a $9,000 nonrecourse mortgage that XYZ, LP assumed at the time the property was contributed. What is Gerald's outside basis immediately after his contribution?

(Multiple Choice)

4.8/5 (39)

Clint noticed that the Schedule K-1 he just received from ABC Partnership included a $20,000 ordinary business loss allocation. His tax basis in ABC at the beginning of ABC's most recent tax year was $10,000. Comparing the Schedule K-1 he recently received from ABC with the Schedule K-1 he received from ABC last year, Clint noted that his share of ABC partnership debt changed as follows: recourse debt increased from $0 to $2,000, qualified nonrecourse debt increased from $0 to $3,000, and nonrecourse debt increased from $0 to $3,000. Finally, the Schedule K-1 Clint recently received from ABC reflected a $1,000 cash contribution he made to ABC during the year.

Clint is not a material participant in ABC partnership, and he received $10,000 of passive income from another investment during the same year he received the loss allocation from ABC. How much of the $20,000 loss from ABC can Clint deduct currently, and how much of the loss is suspended because of the tax basis, the at-risk, and the passive activity loss limitations?

(Essay)

4.8/5 (34)

Which of the following statements regarding the process for determining a partnership's tax year-end is true?

(Multiple Choice)

4.8/5 (43)

J&J, LLC was in its third year of operations when J&J decided to expand the number of members from two, A & B, with equal profits and capital interests to three members, A, B, andC. The third member, C, will contribute her financial expertise to the LLC in exchange for a 1/3 capital interest in J&J. Given the balance sheet below reflecting the financial position of J&J on the date member C is admitted, what are the tax consequences to members A, B, and C, and to J&J when C receives her capital interest? If, instead, member C receives a 1/3 profit interest, what would be the tax consequences to members A, B, and C, and to J&J?

J\&.J Limited Liability Company Balance Sheet

Basis FMV Basis FMV Cash 20,000 20,000 Accounts Payable 7,000 7,000 Inventory 5,000 5,000 Mortgage Payable 20,000 20,000 Equipment 10,000 17,000 Building 30,000 45,000 A - Capital 22,000 30,000 B - Capital 16,000 30,000 Total Assets 65,000 87,000 Total Liab. \& OE 65,000 87,000

(Essay)

4.8/5 (40)

The least aggregate deferral test uses the profit percentage of each partner to determine the minimum amount of tax deferral for the partner group as a whole.

(True/False)

4.7/5 (42)

Which of the following items are subject to the Medicare contribution tax when a partner is a not a material participant in the partnership?

(Multiple Choice)

4.8/5 (34)

What form does a partnership use when filing an annual informational return?

(Multiple Choice)

4.9/5 (30)

On March 15, 20X9, Troy, Peter, and Sarah formed Picture Perfect general partnership. This partnership was created to sell a variety of cameras, picture frames, and other photography accessories. When it was formed, the partners received equal profits and capital interests and the following items were contributed by each partner:

• Troy - cash of $3,000, inventory with a FMV and tax basis of $5,000, and a building with a FMV of $22,000 and adjusted basis of $10,000. Additionally, the building was secured by a $10,000 nonrecourse mortgage.

• Peter - cash of $5,000, accounts payable of $12,000 (recourse debt for which each partner becomes equally responsible), and land with a FMV of $27,000 and tax basis of $20,000.

• Sarah - cash of $2,000, accounts receivable with a FMV and tax basis of $1,000, and equipment with a FMV of $40,000 and adjusted basis of $3,500. Sarah also contributed a $23,000 nonrecourse note payable secured by the equipment.

What is each partner's outside basis and how much gain (loss) must the partners recognize in 20X9 when Picture Perfect was formed?

(Essay)

4.8/5 (34)

Which requirement must be satisfied in order to specially allocate partnership income or losses to partners?

(Multiple Choice)

4.8/5 (47)

Jordan, Inc., Bird, Inc., Ewing, Inc., and Barkley, Inc. formed Nothing-But-Net Partnership on June 1st, 20X9. Now, Nothing-But-Net must adopt its required tax year-end. The partners' year-ends, profits interests, and capital interests are reflected in the table below. Given this information, what tax year-end must Nothing-But-Net use and what rule requires this year-end? Nothing-But-Net Partnership

Year-End Profits Capital Jordan, Inc. 4/30 45\% 25\% Bird, Inc. 9/30 25\% 25\% Ewing, Inc. 10/31 0\% 25\% Barkley, Inc. 12/31 30\% 25\%

(Essay)

4.8/5 (35)

On April 18, 20X8, Robert sold his 35 percent partnership interest in Fruit Wonder, LLC to Richard for $120,000. Prior to selling his interest, Robert had a basis in Fruit Wonder of $80,000. Robert's basis included $5,000 of recourse debt and $15,000 of nonrecourse debt that had been allocated to him. Immediately after the purchase, what is Richard's tax basis in Fruit Wonder?

(Essay)

4.8/5 (43)

At the end of year 1, Tony had a tax basis of $40,000 in Tall Ladders, Limited Partnership. Tony has a 20 percent profits interest in Tall Ladders. For year 2, Tall Ladders will pay Tony a $10,000 guaranteed payment for extra services he provides to the partnership. Given the following Income Statement and Balance Sheet from Tall Ladders, what is Tony's adjusted tax basis at the end of year 2?

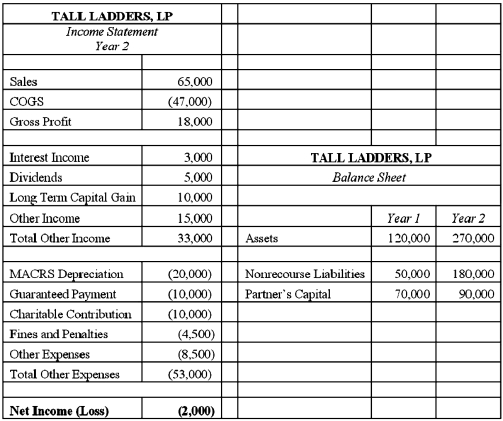

(Essay)

4.8/5 (41)

Under general circumstances, debt is allocated from the partnership to each partner in the following manner:

(Multiple Choice)

4.8/5 (44)

Jerry, a partner with 30% capital and profit interest, received his Schedule K-1 from Plush Pillows, LP. At the beginning of the year, Jerry's tax basis in his partnership interest was $50,000. His current year Schedule K-1 reported an ordinary loss of $15,000, long-term capital gain of $3,000, qualifying dividends of $2,000, $500 of non-deductible expenses, a $10,000 cash contribution, and a reduction of $4,000 in his share of partnership debt. What is Jerry's adjusted basis in his partnership interest at the end of the year?

(Multiple Choice)

4.8/5 (35)

On January 1, 20X9, Mr. Blue and Mr. Grey each contributed $100,000 to form the B&G general partnership. Their partnership agreement states that they will each receive a 50% profits and loss interest. The partnership agreement also provides that Mr. Blue will receive an annual $36,000 guaranteed payment.

B&G began business on January 1, 20X9. For its first taxable year, its accounting records contained the following information. Gross receipts from sales Cost of sales Gross profit Guaranteed payments to Mr. Blue Interest paid on business debt Dividend income Tax exempt interest Operating expenses Depreciation expense Sec. 1231 Gains \ 150,000 (\ 220,000) (\ 70,000) (\ 36,000) (\ 3,000) \ 500 \ 1,500 (\ 138,000) (\ 9,000) \ 8,000

(Essay)

4.9/5 (36)

Partnerships must maintain their capital accounts according to which of the following rules?

(Multiple Choice)

4.8/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)