Exam 33: Translating the Financial Statements of Foreign Operations

Exam 1: An Overview of the Australian External Reporting Environment70 Questions

Exam 2: The Conceptual Framework of Accounting and Its Relevance to Financial Reporting72 Questions

Exam 3: Theories of Accounting76 Questions

Exam 4: An Overview of Accounting for Assets77 Questions

Exam 5: Depreciation of Property, plant and Equipment77 Questions

Exam 6: Revaluations and Impairment Testing of Non-Current Assets76 Questions

Exam 7: Inventory75 Questions

Exam 8: Accounting for Intangibles77 Questions

Exam 9: Accounting for Heritage Assets and Biological Assets76 Questions

Exam 10: An Overview of Accounting for Liabilities78 Questions

Exam 11: Accounting for Leases81 Questions

Exam 12: Accounting for Employee Benefits84 Questions

Exam 13: Share Capital and Reserves85 Questions

Exam 14: Accounting for Financial Instruments90 Questions

Exam 15: Revenue Recognition Issues79 Questions

Exam 16: The Statement of Comprehensive Income and Statement of Changes in Equity77 Questions

Exam 17: Accounting for Share-Based Payments77 Questions

Exam 18: Accounting for Income Taxes80 Questions

Exam 19: The Statement of Cash Flows77 Questions

Exam 20: Accounting for the Extractive Industries75 Questions

Exam 21: Accounting for General Insurance Contracts73 Questions

Exam 22: Accounting for Superannuation Plans77 Questions

Exam 23: Events Occurring After the End of the Reporting Period77 Questions

Exam 24: Segment Reporting77 Questions

Exam 25: Related Party Disclosures77 Questions

Exam 26: Earnings Per Share76 Questions

Exam 27: Accounting for Group Structures87 Questions

Exam 28: Further Consolidation Issues I: Accounting for Intragroup Transactions60 Questions

Exam 29: Further Consolidation Issues II: Accounting for Non-Controlling Interests44 Questions

Exam 30: Further Consolidation Issues IV: Accounting for Changes in the Degree of Ownership of a Subsidiary49 Questions

Exam 31: Accounting for Equity Investments,including Investments in Associates and Joint Arrangements70 Questions

Exam 32: Accounting for Foreign Currency Transactions78 Questions

Exam 33: Translating the Financial Statements of Foreign Operations52 Questions

Exam 34: Accounting for Corporate Social Responsibility73 Questions

Select questions type

Aus Co Ltd has a foreign operation based in New Zealand.The following information was extracted from the foreign operation's accounts for the period ended 30 June 2015: \NZ 000 Machinery (purchased 1 July 2013, revalued 1 June 2015) 13000 Inventory on hand (purchased last quarter 2015) 9800 Depreciation expense-machinery 700 Land (purchased 1 July 2013) 75000 Exchange rate information is:

July 2013 A \1 .00 = \NZ 1.1255 Average for year ended 30 June 2015 A \1 .00 = \NZ 1.2135 1 June 2015 A \1 .00 = \NZ 1.1024 Last quarter 2015 A \1 .00 = \NZ 1.2503 30 June 2015 A \1 .00 = \NZ 1.3250 What is the amount at which each item will be translated (rounded to the nearest A$)?

(Multiple Choice)

4.8/5  (37)

(37)

AASB 121 requires foreign currency transactions to be recorded on initial recognition in the functional currency,by applying to the foreign currency amount the spot exchange rate between the functional currency and the foreign currency at the reporting date.

(True/False)

4.9/5 (33)

When a parent entity has an overseas subsidiary the first task before consolidation is to:

(Multiple Choice)

4.8/5 (37)

The foreign exchange exposure of the parent entity in relation to its foreign operation relates to the net cash flows of the investment in the operation.

(True/False)

4.9/5 (46)

As prescribed in AASB 121,in translating the accounts of a foreign operation from functional to presentation currency,the exchange rate to use for inventory is the average rate during the period the inventory was purchased.

(True/False)

4.9/5 (36)

When translating foreign subsidiary financial statements,net assets are translated at the ---- rate and the components of net assets are translated at the -----rate.

(Multiple Choice)

4.9/5 (36)

Under the translation method required by AASB 121,the approach to translating a foreign operation's accounts includes:

(Multiple Choice)

4.8/5 (35)

Rudd Ltd,an Australian entity purchased Lee Ltd and Kew Ltd on 1 July 2012.Both entities are considered foreign operations of Rudd Ltd based in Singapore.The following information was extracted from the foreign operation's accounts for the period ended 30 June 2015: In Singapore \ Lee Ltd Kew Ltd Equipment (purchased 1 July 2012, revalued 1 June 2014) 650000 200000 Debentures (issued 1 June 2014) 900000 500000 Inventory—asset (purchased last quarter 2015) 68000 50000 Depreciation expense-equipment 54000 25000 Share capital at acquisition of foreign operation 4000000 2000000 Sales revenue (earned evenly over the period) 850000 680000 Exchange rate information is:

1 July 2012 \ S1.00=A\ 1.0520 Average for year ended 30 June 2015 \ S1.00=A\ 1.0700 1 June 2014 \ S1.00=A\ 1.0735 Second quarter 2015 \ S1.00=A\ 1.0600 30 June 2015 \ S1.00=A\ 1.0690 The translation from Singapore dollars to Australian dollars resulted to the following balances:

In Singapore \ Lee Ltd Kew Ltd Equipment (purchased 1 July 2012, revalued 1 June 2014) 694850 214700 Debentures (issued 1 June 2014) 962100 962100 Inventory on hand(second quarter 2015) 72692 53000 Depreciation expense-equipment 57780 26838 Share capital at acquisition of foreign subsidiary 4208000 2104000 Sales revenue (earned evenly over the period) 909500 727600 Which of the following translation processes were applied to Lee Ltd and Kew Ltd,respectively,for the year ended 30 June 2015?

(Multiple Choice)

4.9/5 (34)

The amount of a foreign operation's post-acquisition retained earnings as translated into Australian dollars will depend on the amount translated from the statement of comprehensive income.

(True/False)

4.9/5 (36)

Under the translation method required by AASB 121,the approach to translating a foreign operation's accounts includes:

(Multiple Choice)

4.9/5 (29)

The net assets of a foreign operation at 30 June 2015 are constituted as assets of US$400 000 and liabilities of US$250 000.The parent entity purchased the foreign subsidiary on 1 July 2012.Exchange rate information is as follows: 1 July 2012 US \1 .00 = A \1 .6949 1 July 2014 US \1 .00 = A \1 .7857 30 June 2015 US \1 .00 = A \1 .9231 The foreign operation has not traded during the year ended 30 June 2015,so the net assets remained unchanged during the period.What is the parent entity's foreign currency exposure for the year ended 30 June 2015?

(Multiple Choice)

5.0/5 (35)

Explain how foreign currency translation reserves arise.When and how are these derecognised?

(Essay)

4.9/5 (38)

As prescribed in AASB 121,translation of the accounts of foreign operations to the presentation currency requires any gains or losses on translation be taken directly to reserves.

(True/False)

4.8/5 (36)

If the exchange rate for US dollars relative to Australian dollars goes from US$1 = A$2.10 to US$1 = A$2.20,the Australian dollar has strengthened.

(True/False)

4.8/5 (41)

On the disposal of a foreign operation,AASB 121 prescribed that the cumulative amount of the exchange differences deferred in equity be reclassified to retained earnings.

(True/False)

4.8/5 (36)

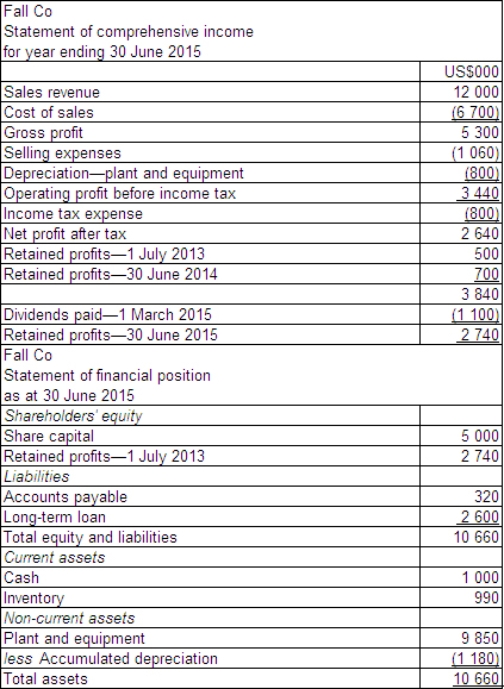

On 1 July 2013 Land Ltd acquired all of the issued shares of Fall Co,a company based in the US.The financial statements for Fall Co for the year ended 30 June 2015 are provided below.Exchange rate information is: 1 July 2013 A \1 .00 = US \0 .50 30 June 2014 A \1 .00 = US \0 .55 1 June 2015 A \1 .00 = US \0 .49 30 June 2015 A \1 .00 = US \0 .52 Average for the year ended 30 June 2015 A \1 .00 = US \0 .51 Dividends paid-1 March 2015 A \1 .00 = US \0 .53 Average rate for quarter ending 30 June 2015 A \1 .00 = US \0 .48  Additional information:

All revenues and expenses were earned or incurred evenly throughout the year.

All plant and equipment was purchased using a long-term loan when the exchange rate was A$1.00 = US$0.54.

Inventory was purchased evenly over the period,with the inventory on hand at the end of the period purchased over the quarter ending on 30 June,and accounts payable were accrued evenly over the period.

What are the translated amounts for operating profit,retained profit at 30 June 2015,total equity and liabilities and the gain or loss on foreign currency translation for Fall Co (rounded to the nearest A$)?

Additional information:

All revenues and expenses were earned or incurred evenly throughout the year.

All plant and equipment was purchased using a long-term loan when the exchange rate was A$1.00 = US$0.54.

Inventory was purchased evenly over the period,with the inventory on hand at the end of the period purchased over the quarter ending on 30 June,and accounts payable were accrued evenly over the period.

What are the translated amounts for operating profit,retained profit at 30 June 2015,total equity and liabilities and the gain or loss on foreign currency translation for Fall Co (rounded to the nearest A$)?

(Multiple Choice)

4.8/5 (36)

Yarra Manufacturing Ltd is an Australian registered entity that has a branch in Singapore,Kew Ltd.The Singapore branch has a foreign operation in China.The foreign operation maintains its accounting records in Chinese yuan.The functional currency of the Chinese operation is Singapore dollar.The presentation currency of Kew Ltd is Australian dollar. At reporting date,the translation of the financial statements of the Chinese foreign operation resulted in a loss of S$6500 and the translation of the financial statements of Kew Ltd to its presentation currency resulted to a gain of A$4500.

Which of the following results is consistent with AASB 121 with respect to Kew Ltd?

(Multiple Choice)

4.8/5 (32)

In translating the accounts of a foreign operation from functional to presentation currency,resulting exchange differences is recognised in other comprehensive income.

(True/False)

4.8/5 (26)

When consolidating financial statements of foreign operations,we use the same rate each year for goodwill,so that the amount recognised on consolidation will not fluctuate from year to year.

(True/False)

4.8/5 (47)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)