Exam 7: Inventory

Exam 1: An Overview of the Australian External Reporting Environment70 Questions

Exam 2: The Conceptual Framework of Accounting and Its Relevance to Financial Reporting72 Questions

Exam 3: Theories of Accounting76 Questions

Exam 4: An Overview of Accounting for Assets77 Questions

Exam 5: Depreciation of Property, plant and Equipment77 Questions

Exam 6: Revaluations and Impairment Testing of Non-Current Assets76 Questions

Exam 7: Inventory75 Questions

Exam 8: Accounting for Intangibles77 Questions

Exam 9: Accounting for Heritage Assets and Biological Assets76 Questions

Exam 10: An Overview of Accounting for Liabilities78 Questions

Exam 11: Accounting for Leases81 Questions

Exam 12: Accounting for Employee Benefits84 Questions

Exam 13: Share Capital and Reserves85 Questions

Exam 14: Accounting for Financial Instruments90 Questions

Exam 15: Revenue Recognition Issues79 Questions

Exam 16: The Statement of Comprehensive Income and Statement of Changes in Equity77 Questions

Exam 17: Accounting for Share-Based Payments77 Questions

Exam 18: Accounting for Income Taxes80 Questions

Exam 19: The Statement of Cash Flows77 Questions

Exam 20: Accounting for the Extractive Industries75 Questions

Exam 21: Accounting for General Insurance Contracts73 Questions

Exam 22: Accounting for Superannuation Plans77 Questions

Exam 23: Events Occurring After the End of the Reporting Period77 Questions

Exam 24: Segment Reporting77 Questions

Exam 25: Related Party Disclosures77 Questions

Exam 26: Earnings Per Share76 Questions

Exam 27: Accounting for Group Structures87 Questions

Exam 28: Further Consolidation Issues I: Accounting for Intragroup Transactions60 Questions

Exam 29: Further Consolidation Issues II: Accounting for Non-Controlling Interests44 Questions

Exam 30: Further Consolidation Issues IV: Accounting for Changes in the Degree of Ownership of a Subsidiary49 Questions

Exam 31: Accounting for Equity Investments,including Investments in Associates and Joint Arrangements70 Questions

Exam 32: Accounting for Foreign Currency Transactions78 Questions

Exam 33: Translating the Financial Statements of Foreign Operations52 Questions

Exam 34: Accounting for Corporate Social Responsibility73 Questions

Select questions type

The only difference between IAS 2 and AASB 102 is that the 'international' standards allow inventory to be valued using LIFO.

(True/False)

4.8/5  (37)

(37)

Generally,AASB 102 requires inventories to be measured at cost or net realisable value.Discuss circumstances when other measurement bases (such as current replacement cost)are permitted.

(Essay)

4.9/5 (38)

AASB 102 applies to all inventories including work in progress under construction contracts.

(True/False)

4.8/5 (42)

The first-in,first-out (FIFO)method assumes that items remaining in inventory at the end of the period are those most recently purchased or produced.

(True/False)

4.9/5 (36)

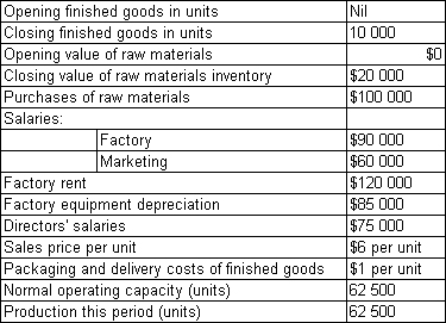

Video Productions Ltd commenced business manufacturing video tapes on 1 July 2011.Summary data for the first full year of production are:

Packaging and delivery are essential to be able to sell the product.What total value should be attributed to finished goods inventory in the financial statements in accordance with AASB 102?

Packaging and delivery are essential to be able to sell the product.What total value should be attributed to finished goods inventory in the financial statements in accordance with AASB 102?

(Multiple Choice)

4.8/5 (42)

The value of inventory reported in the financial statements under AASB 102 may be reported at an amount lower than its original cost.

(True/False)

4.9/5 (30)

Explain the circumstances where borrowing costs are permitted to be included in the cost of inventories?

(Short Answer)

5.0/5 (28)

Reversal of a previous inventory write down is not advocated in AASB 102.

(True/False)

4.7/5 (34)

Toey Ltd has provided the following information about the total production cost and estimates of realisable value of three lines of shoes they produce within the same class of inventory

Item Production cost \ 000 Sales proceeds \ 000 Packaging costs \ 000 Freight outwards \ 000 Sling back 13 15 3 2 Court 10 16 3 1 Stiletto 17 19 4 3

Packaging and freight are necessary in order to be able to sell the shoes.What is the value of the inventory in accordance with AASB 102?

(Multiple Choice)

4.9/5 (40)

Oblong Ltd manufactures cardboard boxes for a variety of purposes.The following information relates to the production of the extra large packing boxes used by removalists for the period ended 30 June 2012.

Date Manufactured Units sold 1 July (balance) 100@\ 3.05 15 July 2011 300@\ 3.00 19 July 2011 250 20 August 2011 200@\ 2.50 21 August 2011 190 15 October 2011 170@\ 3.12 30 October 2011 200 15 December 2011 320@\ 3.40 15 January 2012 175 13 March 2012 90@\ 2.90 30 March 2012 220 15 June 2012 80@\ 3.20 28 June 2012 100

The company uses a perpetual inventory system.The net realisable value per extra large cardboard box is $3.15 at the end of the period.What are the costs of sales and the value of ending inventory for Oblong Ltd assuming the FIFO cost-flow assumption is used?

(Multiple Choice)

4.8/5 (38)

AASB 102 requires,among others,disclosure of which of the following pieces of information?

(Multiple Choice)

4.7/5 (41)

Under the perpetual system,a difference with the stocktake records might indicate:

(Multiple Choice)

5.0/5 (46)

Which of the following statements is correct in relation to the costing of inventories?

(Multiple Choice)

4.9/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)