Exam 8: Government-Wide Statements, capital Assets, long-Term Debt

Exam 1: Introduction to Accounting and Financial Reporting for Governmental and Not-For-Profit Organizations144 Questions

Exam 2: Overview of Financial Reporting for State and Local Governments143 Questions

Exam 3: Modified Accrual Accounting: Including the Role of Fund Balances and Budgetary Authority154 Questions

Exam 4: Accounting for the General and Special Revenue Funds128 Questions

Exam 5: Accounting for Other Governmental Fund Types: Capital Projects, debt Service, and Permanent170 Questions

Exam 6: Proprietary Funds143 Questions

Exam 7: Fiduciary Trustfunds162 Questions

Exam 8: Government-Wide Statements, capital Assets, long-Term Debt162 Questions

Exam 9: Advanced Topics for State and Local Governments104 Questions

Exam 10: Accounting for Private Not-For-Profit Organizations154 Questions

Exam 11: College and University Accounting128 Questions

Exam 12: Accounting for Hospitals and Other Health Care Providers99 Questions

Exam 13: Auditing, tax-Exempt Organizations, and Evaluating Performance144 Questions

Exam 14: Financial Reporting by the Federal Government68 Questions

Select questions type

When preparing government-wide financial statements,the modified accrual based governments fund are adjusted.List 4 events requiring adjustment.

(Short Answer)

4.9/5  (36)

(36)

A government reported expenditures for infrastructure as follows: $20 million for improvements and additions; $18 million to extend the life of existing infrastructure; $16 million for general repairs.The cost of its infrastructure,excluding land,is $750 million,and the infrastructure has an estimated life of 50 years,on average.Which of the following would be the reported expense (in millions)under each of the following options?

(Multiple Choice)

4.7/5 (33)

A government recorded transfers out of the General Fund to the debt service fund in the amount of $600,000 and to the capital projects fund in the amount of $300,000.The amount that would be shown as a transfer in the governmental activities column of the Statement of Activities would be:

(Multiple Choice)

4.8/5 (32)

The City of Thomasville maintains its books so as to prepare fund accounting statements and prepares worksheet adjustments in order to prepare government-wide financial statements.Required:

You are to prepare,in journal form,worksheet adjustments for each of the following situations.

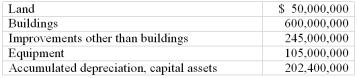

A.General fixed assets,as of the beginning of the year,which had not been recorded,were as follows:

B.During the year,expenditures for capital outlays amounted to $11,200,000.Of that amount,$7,800,000 was for buildings; $1,550,000 was for improvements other than buildings,and the remainder was for land.

C.The capital outlay expenditures outlined in (B)were completed at the end of the year (no depreciation until next year).For purposes of financial statement presentation,all capital assets are depreciated using the straight-line method,with no estimated salvage value.Estimated lives are as follows:

buildings,50 years; improvements other than buildings,20 years; equipment,10 years.

D.Equipment with a cost of $41,500 and accumulated depreciation at the time of sale of $16,600 was sold for $45,000.

B. During the year, expenditures for capital outlays amounted to $11,200,000. Of that amount, $7,800,000 was for buildings; $1,550,000 was for improvements other than buildings, and the remainder was for land.

C. The capital outlay expenditures outlined in (B) were completed at the end of the year (no depreciation until next year). For purposes of financial statement presentation, all capital assets are depreciated using the straight-line method, with no estimated salvage value. Estimated lives are as follows: buildings, 50 years; improvements other than buildings, 20 years; equipment, 10 years.

B.During the year,expenditures for capital outlays amounted to $11,200,000.Of that amount,$7,800,000 was for buildings; $1,550,000 was for improvements other than buildings,and the remainder was for land.

C.The capital outlay expenditures outlined in (B)were completed at the end of the year (no depreciation until next year).For purposes of financial statement presentation,all capital assets are depreciated using the straight-line method,with no estimated salvage value.Estimated lives are as follows:

buildings,50 years; improvements other than buildings,20 years; equipment,10 years.

D.Equipment with a cost of $41,500 and accumulated depreciation at the time of sale of $16,600 was sold for $45,000.

B. During the year, expenditures for capital outlays amounted to $11,200,000. Of that amount, $7,800,000 was for buildings; $1,550,000 was for improvements other than buildings, and the remainder was for land.

C. The capital outlay expenditures outlined in (B) were completed at the end of the year (no depreciation until next year). For purposes of financial statement presentation, all capital assets are depreciated using the straight-line method, with no estimated salvage value. Estimated lives are as follows: buildings, 50 years; improvements other than buildings, 20 years; equipment, 10 years.

(Essay)

4.9/5 (46)

General (governmental)long term assets and debt have a balance of zero until the worksheet entries are made.

(True/False)

4.8/5 (36)

General obligation debt,which has as backing the full faith and credit of the governmental unit,is reported in both the government-wide statements and the fund basis statements.

(True/False)

4.8/5 (29)

Where in the basic financial statements would one find fiduciary activities reported?

(Multiple Choice)

4.8/5 (37)

The City of Casper levied property taxes for 2012 in the amount of $8,000,000.The amount estimated to be uncollectible is 3%.By the end of the year,$7,300,000 had been collected.It was estimated that $400,000 would be collected during the next 60 days of 2011 and that $240,000 would be collected after that.The City has a policy of recognizing the full amount possible for property taxes.Which of the following statements is true?

(Multiple Choice)

4.8/5 (30)

The City of Charlotte levied property taxes in 2012 in the amount of $10 million.It is estimated that 2% will be uncollectible.During 2012,$9,000,000 was collected,and it is anticipated that $400,000 will be collected during the next 60 days.When moving from the changes in fund balances in the Statement of Revenues,Expenditures,and Changes in Fund Balances to the changes in net assets in the Statement of Activities,what will be the adjustment? (ignore any possible effect resulting from the previous year's deferral)

(Multiple Choice)

4.8/5 (38)

Internal service funds are most commonly reported in which section of the Government-wide financial statements?

(Multiple Choice)

4.9/5 (24)

Assume a government reported Proceeds of Bonds in the amount of $1,000,000 in the governmental fund Statement of Revenues,Expenditures,and Changes in Fund Balances.When preparing the reconciliation from the changes in fund balances in that statement to the changes in net assets in the governmental funds column in the Statement of Activities,a decrease of $1,000,000 would be entered.

(True/False)

4.8/5 (36)

When converting to government-wide financial statements,the entry to record the amortization of the premium on a bond would look like:

(Multiple Choice)

5.0/5 (30)

Which of the following funds would not be included in the government-wide financial statements?

(Multiple Choice)

4.8/5 (37)

Identify and describe the required supplementary information schedules that must be prepared when using the modified approach.

(Essay)

4.8/5 (29)

The Statement of Net Assets and Statement of Activities are the only two statements for the government-wide financial statements.

(True/False)

4.9/5 (37)

Government-wide statements are prepared using the accrual basis; therefore,governmental fund-basis statements need to be adjusted from their original modified accrual basis.

(True/False)

4.7/5 (29)

A government's Statement of Revenues,Expenditures,and Changes in Fund Balances reflected expenditures for debt service in the amount of $12,000,000,including $5,000,000 for principal.It also reflected proceeds of bonds in the amount of $4,000,000.No interest accruals were involved.When moving from the changes in fund balances reported for the governmental funds to the change in net assets for governmental activities,the net change would be:

(Multiple Choice)

4.7/5 (36)

Which of the following is false about the worksheet entry process?

(Multiple Choice)

4.9/5 (37)

A governmental fund Statement of Revenues,Expenditures,and Changes in Fund Balances reported expenditures of $30 million,including capital outlay expenditures of $5 million.Capital assets for that government cost $90 million,including land of $10 million.Depreciable assets are amortized over 20 years,on average.The reconciliation from governmental changes in fund balances to governmental activities changes in net assets would reflect a(an):

(Multiple Choice)

4.8/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)