Exam 11: College and University Accounting

Exam 1: Introduction to Accounting and Financial Reporting for Governmental and Not-For-Profit Organizations144 Questions

Exam 2: Overview of Financial Reporting for State and Local Governments143 Questions

Exam 3: Modified Accrual Accounting: Including the Role of Fund Balances and Budgetary Authority154 Questions

Exam 4: Accounting for the General and Special Revenue Funds128 Questions

Exam 5: Accounting for Other Governmental Fund Types: Capital Projects, debt Service, and Permanent170 Questions

Exam 6: Proprietary Funds143 Questions

Exam 7: Fiduciary Trustfunds162 Questions

Exam 8: Government-Wide Statements, capital Assets, long-Term Debt162 Questions

Exam 9: Advanced Topics for State and Local Governments104 Questions

Exam 10: Accounting for Private Not-For-Profit Organizations154 Questions

Exam 11: College and University Accounting128 Questions

Exam 12: Accounting for Hospitals and Other Health Care Providers99 Questions

Exam 13: Auditing, tax-Exempt Organizations, and Evaluating Performance144 Questions

Exam 14: Financial Reporting by the Federal Government68 Questions

Select questions type

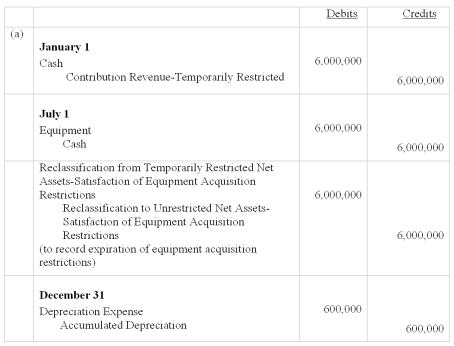

On January 1,2012,Antioch College,a private not-for-profit college,received $6,000,000 in cash to purchase an electron microscope.The microscope was delivered on July 1,2012 and payment was made.The microscope is expected to last 5 years and has no salvage value at the end of that time.The fiscal year end is December 31.

(a)Record the journal entries required on January 1,July 1,and December 31,2012 to record the receipt of the cash,the purchase of equipment,and one half year's depreciation,assuming the plant assets are recorded as unrestricted assets at the time of purchase.

(b)Record the journal entries required on January 1,July 1,and December 31,2012 to record the receipt of the cash,the purchase of equipment,and one half year's depreciation,assuming the plant assets are recorded as temporarily restricted assets at the time of purchase.

(Essay)

4.7/5  (39)

(39)

With respect to private colleges and universities,why are quasi-endowments not classified as permanently restricted net assets while true endowments are?

(Essay)

4.9/5 (40)

Distinguish between

(a)true endowments,

(b)term endowments,and

(c)quasi-endowments.Explain how the net assets of each is classified by a private college or university.

(Essay)

4.8/5 (32)

Which of the following is true of a Statement of Cash Flows for a private college or university?

(Multiple Choice)

4.9/5 (42)

Universities treat athletic scholarships as a reduction in revenue.

(True/False)

5.0/5 (41)

How does a private college or university treat an academic scholarship?

(Multiple Choice)

4.9/5 (29)

Which of the following is true of a Statement of Activities prepared for a private college or university?

(Multiple Choice)

4.9/5 (38)

In 2011 a faculty member at a private college received a grant from the National Science Foundation to conduct basic research on tree frogs in the amount of $400,000.Expenses associated with the grant totaled $390,000 in 2012.In the Statement of Activities for 2012,the college should show:

(Multiple Choice)

5.0/5 (24)

Private,Not-for-profit Colleges and Universities and Investor-owned Schools follow FASB standards and adhere to the accrual basis of accounting.

(True/False)

5.0/5 (30)

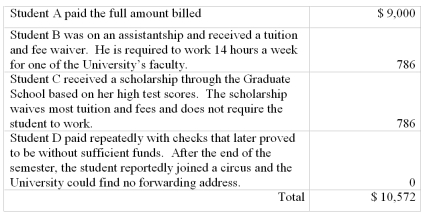

Ballard University,a private not-for-profit,billed four students for tuition and fees each in the amount of $8,450 each for fall semester.The University estimates 20% of tuition and fees will prove to be uncollectible.The University collected $9,422 as follows:

Required:

Prepare the journal entries to record the billing and subsequent collection or write-off for the transactions listed above.

Required:

Prepare the journal entries to record the billing and subsequent collection or write-off for the transactions listed above.

(Essay)

4.8/5 (37)

According to the rules for accounting for colleges and universities under the jurisdiction of the FASB,if an institution decides not to capitalize museum and other inexhaustible collections,note disclosures are required regarding the collections.

(True/False)

4.8/5 (42)

Ethan Allen University is a private university following FASB standards for reporting.The following transactions took place during the year ended June 30,2012.

(1)EAU had received $600,000 in tuition in June 2012 for the summer session that runs from

June 16 to August 14,2011 and had deferred $450,000 (75%)at June 30,2011.

(2)EAU received in cash tuition of $3,320,000; unrestricted contributions of $320,000;

contributions permanently restricted by donor agreement for the endowment of $805,000,

unrestricted interest income on endowments of $250,000; and auxiliary enterprise revenue of

$2,500,000.

(3)Contributions for student scholarships were received in the amount of $430,000.$360,000

was awarded to students during the year.Students receiving these scholarships are required to

work 10 hours a week (institutional support).

(4)Expenses amounted to $1,400,000 for instruction,$800,000 for research,$600,000 for

public service,$2,000,000 for auxiliary enterprises,$300,000 for student services,and

$890,000 for institutional support.Included in these amounts is $460,000 of depreciation.All

other expenses ($5,530,000)were paid in cash.Plant assets are classified as unrestricted.

(5)EAU received $580,000 in tuition in mid June 2012 for the summer session ending in mid

August 2012.

(6)At year-end,endowment investments were determined to have a fair value of $50,000 in

excess of their recorded amounts.No restrictions apply to this income.

Required:

(a)Prepare journal entries to record these events including closing entries.

(b)Prepare a Statement of Unrestricted Revenues,Expenses and Other Changes in

Unrestricted Net Assets.

(c)Prepare a Statement of Activities for the year ending June 30,2012,assuming the June 30,

2011 balances in net assets are:

$2,050,000 unrestricted,$830,000 temporarily restricted,and

$4,000,000 permanently restricted.

(Essay)

4.9/5 (29)

Universities treat athletic scholarships as an expense to the athletic department who must pay for the scholarship out of its net revenues.

(True/False)

4.8/5 (35)

A tuition waiver for a student who works as a graduate assistant is treated as compensation expense.

(True/False)

4.8/5 (37)

With respect to colleges and universities,if a tuition or fee reduction is an employee benefit it should be treated as a compensation expense,rather than a discount.

(True/False)

4.8/5 (26)

A donor gave a gift of $40,000 cash to a private college in 2011 with instructions that the funds be expended for psychology research.The funds were expended in 2012.The private college would recognize the $40,000 as:

(Multiple Choice)

4.9/5 (33)

The NACUBO Financial Accounting and Reporting Manual treats estimates of uncollectible student accounts as:

(Multiple Choice)

4.8/5 (38)

Public universities follow the authoritative standards of _____ and the _____ basis of accounting.

(Multiple Choice)

4.9/5 (39)

Under NACUBO guidelines,tuition waivers associated with student work study programs should be reported as:

(Multiple Choice)

4.8/5 (32)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)