Exam 8: Relative,asset-Oriented,and Real Option Valuation Basics

Exam 1: Introduction to Mergers, acquisitions, and Other Restructuring Activities108 Questions

Exam 2: The Regulatory Environment103 Questions

Exam 3: The Corporate Takeover Market: Common Takeover Tactics, anti-Takeover Defenses, and Corporate Governance126 Questions

Exam 4: Planning,developing Business,and Acquisition Plans: Phases 1 and 2 of the Acquisition Process109 Questions

Exam 5: Implementation: Search Through Closing: Phases 3 to 10 of the Acquisition Process106 Questions

Exam 6: Postclosing Integration: Mergers, acquisitions, and Business Alliances103 Questions

Exam 7: Merger and Acquisition Cash Flow Valuation Basics81 Questions

Exam 8: Relative,asset-Oriented,and Real Option Valuation Basics84 Questions

Exam 9: Applying Financial Models to Value, structure, and Negotiate Mergers and Acquisitions92 Questions

Exam 10: Analysis and Valuation of Privately Held Companies97 Questions

Exam 11: Structuring the Deal: Payment and Legal Considerations112 Questions

Exam 12: Structuring the Deal: Tax and Accounting Considerations97 Questions

Exam 13: Financing the Deal: Private Equity, hedge Funds, and Other Sources of Funds121 Questions

Exam 14: Highly Leveraged Transactions: Lbo Valuation and Modeling Basics98 Questions

Exam 15: Business Alliances: Joint Ventures, partnerships, strategic Alliances, and Licensing113 Questions

Exam 16: Alternative Exit and Restructuring Strategies: Divestitures, spin-Offs, carve-Outs, split-Ups, and Split-Offs119 Questions

Exam 17: Alternative Exit and Restructuring Strategies: Bankruptcy Reorganization and Liquidation80 Questions

Exam 18: Cross-Border Mergers and Acquisitions: Analysis and Valuation89 Questions

Select questions type

The so-called PEG ratio is calculated by dividing the firm's price-to-earning ratio by the expected growth rate in the firm's share price.

(True/False)

4.8/5  (33)

(33)

Which of the following are examples of intangible assets that may have value to the acquiring company?

(Multiple Choice)

4.9/5 (29)

Liquidation value provides an estimate of the minimum value of the target firm.

(True/False)

4.7/5 (39)

Investors may be willing to pay considerably more for a stock whose PEG ratio is greater than one if they believe the increase in earnings will result in future financial returns that significantly exceed the firm's cost of equity.

(True/False)

4.9/5 (31)

The comparable companies' transactions valuation method is generally considered the most accurate of all the valuation methods.

(True/False)

4.7/5 (34)

It is critical for the analyst to remember that high growth rates by themselves are likely to increase multiples such as a firm's price to earnings ratio even without any improvement in financial returns.

(True/False)

4.9/5 (33)

Relative valuation methods are often described as market-based,as they reflect the amounts investors are willing to pay for each dollar of earnings,cash flow,sales,or book value at a moment in time.

(True/False)

4.8/5 (37)

Case Study Short Essay Examination Questions

Valuation Methods Employed in Investment Bank Fairness Opinion Letters

Background

A fairness opinion letter is a written third-party certification of the appropriateness of the price of a proposed transaction such as a merger, acquisition, leveraged buyout, or tender offer. A typical fairness opinion provides a range of what is believed to be fair values, with a presumption that the actual deal price should fall within this range. The data used in this case study is found in SunGard's Schedule 14A Proxy Statement submitted to the SEC in May 2005.

On March 27, 2005, the investment banking behemoth Lazard Freres (Lazard) submitted a letter to the board of directors of SunGard Corporation pertaining to the fairness of a $10.9 billion bid to take the firm private made by an investor group. Lazard employed a variety of valuation methods to evaluate the offer price. These included the comparable company approach, the recent transactions method, discounted cash flow analysis, and an analysis of recent transaction premiums. The analyses were applied to each of the firm's major businesses: software services and recovery availability services. The software services' business provides software systems and support for application and transaction processing to financial services firms, universities, and government agencies. The recovery availability services business provides businesses and government agencies with backup and recovery support in the event their data processing systems are disrupted.

Comparable Company Analysis

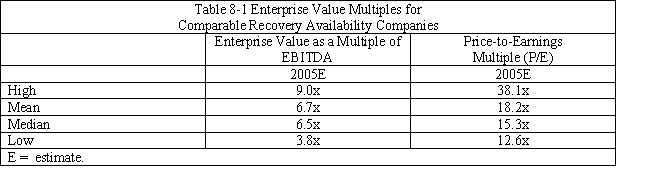

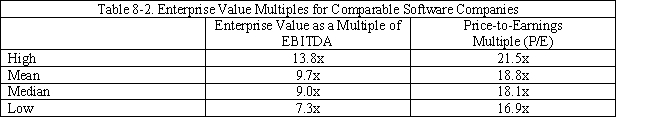

Using publicly available information, Lazard reviewed the market values and trading multiples of the selected publicly held companies for each business segment. Multiples were based on stock prices as of March 24, 2005 and specific company financial data on publicly available research analysts' estimates for 2005. In the case of SunGard's software business, Lazard reviewed the market values and trading multiples of four publicly traded financial services companies and three publicly traded securities trading companies. In the case of SunGard's recovery availability services business, Lazard reviewed the market values and trading multiples of the six selected publicly traded business continuity services (i.e., recoverability services firms) companies. These firms were believed to be representative of these segments of SunGard's operations.

Lazard calculated enterprise values for these comparable companies as equity value plus debt, preferred stock, and all out-of-the-money convertibles (i.e., convertible debt whose conversion price exceeded the merger offer price), less cash and cash equivalents (i.e., short-term liquid securities). Estimated enterprise value multiples of earnings before interest, taxes, depreciation and amortization (i.e., EBITDA) were created for 2005 by dividing enterprise values by publicly available estimates of EBITDA for each comparable company. Similarly, price-to-earnings ratios were created by dividing equity values per share by earnings per share for each comparable company for calendar 2005. See Tables 8-1 and 8.2.  Based on this analysis, Lazard determined an enterprise value to estimated 2005 EBITDA multiple range for SunGard's recovery availability services business of 5.5x to 7.0x. Lazard also determined a 2005 estimated P/E range for this segment of 14.0x to 16.0x. Multiplying SunGard's projected EBITDA and earnings per share for 2005 by these ranges, Lazard calculated an enterprise value range for SunGard's recovery availability services business of approximately $3.1 billion to $3.7 billion. Financial projections for SunGard were provided by SunGard's management.

Based on this analysis, Lazard determined an enterprise value to estimated 2005 EBITDA multiple range for SunGard's recovery availability services business of 5.5x to 7.0x. Lazard also determined a 2005 estimated P/E range for this segment of 14.0x to 16.0x. Multiplying SunGard's projected EBITDA and earnings per share for 2005 by these ranges, Lazard calculated an enterprise value range for SunGard's recovery availability services business of approximately $3.1 billion to $3.7 billion. Financial projections for SunGard were provided by SunGard's management.  Based on the results in Table 8-2, Lazard determined an enterprise value to estimated 2005 EBITDA multiple range for SunGard's software business of 7.5x to 9.5x. Lazard also determined a 2005 estimated P/E range for SunGard's software business of 17.0 to 19.0x. Multiplying SunGard's projected EBITDA and earnings per share for 2005 by these ranges, Lazard calculated an enterprise value range for SunGard's software business of approximately $4.3 billion to $5.2 billion.

Lazard then summed the enterprise value ranges for SunGard's software business and recovery availability services business to calculate a consolidated enterprise value range for SunGard of approximately $7.4 billion to $8.9 billion. Using this consolidated enterprise value range and assuming net debt (i.e., total debt less cash and cash equivalents on the balance sheet) of $273 million, Lazard calculated an implied price per share range for SunGard common stock of $24.20 to $29.00 by dividing the enterprise value less net debt by the SunGard shares outstanding.

Recent Transactions Method

For the recovery availability services business, Lazard reviewed ten merger and acquisition transactions since October 2001 for companies in the information technology outsourcing business. To the extent publicly available, Lazard reviewed the transaction enterprise values of the recent transactions as a multiple of the last twelve months EBITDA for the period ending on the recent transaction announcement date. See Table 8-3.

Based on the results in Table 8-2, Lazard determined an enterprise value to estimated 2005 EBITDA multiple range for SunGard's software business of 7.5x to 9.5x. Lazard also determined a 2005 estimated P/E range for SunGard's software business of 17.0 to 19.0x. Multiplying SunGard's projected EBITDA and earnings per share for 2005 by these ranges, Lazard calculated an enterprise value range for SunGard's software business of approximately $4.3 billion to $5.2 billion.

Lazard then summed the enterprise value ranges for SunGard's software business and recovery availability services business to calculate a consolidated enterprise value range for SunGard of approximately $7.4 billion to $8.9 billion. Using this consolidated enterprise value range and assuming net debt (i.e., total debt less cash and cash equivalents on the balance sheet) of $273 million, Lazard calculated an implied price per share range for SunGard common stock of $24.20 to $29.00 by dividing the enterprise value less net debt by the SunGard shares outstanding.

Recent Transactions Method

For the recovery availability services business, Lazard reviewed ten merger and acquisition transactions since October 2001 for companies in the information technology outsourcing business. To the extent publicly available, Lazard reviewed the transaction enterprise values of the recent transactions as a multiple of the last twelve months EBITDA for the period ending on the recent transaction announcement date. See Table 8-3.  Based on Table 8-3, Lazard determined an EBITDA multiple range of 6.5x to 7.5x and multiplied this range by the last twelve months EBITDA for SunGard's recovery availability business to calculate an implied enterprise value range of approximately $3.4 billion to $4.0 billion.

Lazard reviewed 21 merger and acquisition transactions since February 2003 with a value greater than approximately $100 million for companies in the software business. To the extent publicly available, Lazard examined the transaction enterprise values of the recent transactions as a multiple of EBITDA for the last twelve months prior to the public announcement of the relevant recent transaction. See Table 8-4.

Based on Table 8-3, Lazard determined an EBITDA multiple range of 6.5x to 7.5x and multiplied this range by the last twelve months EBITDA for SunGard's recovery availability business to calculate an implied enterprise value range of approximately $3.4 billion to $4.0 billion.

Lazard reviewed 21 merger and acquisition transactions since February 2003 with a value greater than approximately $100 million for companies in the software business. To the extent publicly available, Lazard examined the transaction enterprise values of the recent transactions as a multiple of EBITDA for the last twelve months prior to the public announcement of the relevant recent transaction. See Table 8-4.  Based on the information contained in Table 8-5, Lazard determined an EBITDA multiple range of 9.0x to 11.0x and multiplied this range by the last twelve month EBITDA for SunGard's software business to calculate an implied enterprise value range for this business segment of approximately $5.0 billion to $6.1 billion.

Lazard then summed the enterprise value ranges for SunGard's software business and recovery availability services business to calculate a consolidated enterprise value range for SunGard of approximately $8.4 billion to $10.1 billion. Using this consolidated enterprise value range and assuming net debt of $273 million, Lazard calculated the value per share of SunGard common stock of $27.60 to $32.70 by dividing the estimated consolidated enterprise value less net debt by common shares outstanding.

Discounted Cash Flow Analysis

Using projections provided by SunGard's management, Lazard performed an analysis of the present value, as of March 31, 2005, of the free cash flows that SunGard could generate annually from calendar year 2005 through calendar year 2009. Lazard analyzed separately the cash flows for SunGard's software business and recovery availability services business.

For SunGard's software business, in calculating the terminal value, Lazard assumed perpetual growth rates (i.e., constant growth model) of 3.5% to 4.5% for the projected free cash flows for the periods subsequent to 2009. The projected annual cash flows through 2009 and beyond were then discounted to present value using discount rates ranging from 10.0% to 12.0%. Based on this analysis, Lazard calculated an implied enterprise value range for the software business of approximately $5.6 billion to $7.4 billion.

For SunGard's recovery availability services business, in calculating the terminal value Lazard assumed perpetual growth rates of 2.0% to 3.0% for the projected free cash flows for periods subsequent to 2009. The projected cash flows were then discounted to present value using discount rates ranging from 10.0% to 12.0%. Lazard then calculated an implied enterprise value range for SunGard's recovery availability business of approximately $2.6 billion to $3.3 billion.

Lazard then aggregated the enterprise value ranges for SunGard's two business segments to calculate a consolidated enterprise value range for SunGard of approximately $8.2 billion to $10.7 billion. Using this consolidated enterprise value range and assuming net debt of $273 million, Lazard calculated an implied price per share range for SunGard common stock of $26.70 to $34.60.

Premiums Paid Analysis

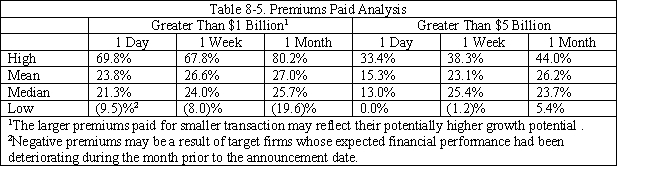

Lazard performed a premiums paid analysis based upon the premiums paid in 73 recent transactions (not involving "mergers of equals" transactions) that were announced from January 2004 through March 2005 and involved transaction values in excess of $1 billion. In conducting its analysis, Lazard analyzed the premiums paid for recent transactions over $1 billion and those over $5 billion, since premiums paid may vary with the size of the transaction.

The analysis was based on the one day, one week and four week implied premiums for the transactions examined. The implied premiums were calculated by comparing the offer price for the target firm on the announcement date with the per share price of the target firm one day, one week, and four weeks prior to the announcement of the transaction. The results of these calculations are given in Table 8-5.

Based on the information contained in Table 8-5, Lazard determined an EBITDA multiple range of 9.0x to 11.0x and multiplied this range by the last twelve month EBITDA for SunGard's software business to calculate an implied enterprise value range for this business segment of approximately $5.0 billion to $6.1 billion.

Lazard then summed the enterprise value ranges for SunGard's software business and recovery availability services business to calculate a consolidated enterprise value range for SunGard of approximately $8.4 billion to $10.1 billion. Using this consolidated enterprise value range and assuming net debt of $273 million, Lazard calculated the value per share of SunGard common stock of $27.60 to $32.70 by dividing the estimated consolidated enterprise value less net debt by common shares outstanding.

Discounted Cash Flow Analysis

Using projections provided by SunGard's management, Lazard performed an analysis of the present value, as of March 31, 2005, of the free cash flows that SunGard could generate annually from calendar year 2005 through calendar year 2009. Lazard analyzed separately the cash flows for SunGard's software business and recovery availability services business.

For SunGard's software business, in calculating the terminal value, Lazard assumed perpetual growth rates (i.e., constant growth model) of 3.5% to 4.5% for the projected free cash flows for the periods subsequent to 2009. The projected annual cash flows through 2009 and beyond were then discounted to present value using discount rates ranging from 10.0% to 12.0%. Based on this analysis, Lazard calculated an implied enterprise value range for the software business of approximately $5.6 billion to $7.4 billion.

For SunGard's recovery availability services business, in calculating the terminal value Lazard assumed perpetual growth rates of 2.0% to 3.0% for the projected free cash flows for periods subsequent to 2009. The projected cash flows were then discounted to present value using discount rates ranging from 10.0% to 12.0%. Lazard then calculated an implied enterprise value range for SunGard's recovery availability business of approximately $2.6 billion to $3.3 billion.

Lazard then aggregated the enterprise value ranges for SunGard's two business segments to calculate a consolidated enterprise value range for SunGard of approximately $8.2 billion to $10.7 billion. Using this consolidated enterprise value range and assuming net debt of $273 million, Lazard calculated an implied price per share range for SunGard common stock of $26.70 to $34.60.

Premiums Paid Analysis

Lazard performed a premiums paid analysis based upon the premiums paid in 73 recent transactions (not involving "mergers of equals" transactions) that were announced from January 2004 through March 2005 and involved transaction values in excess of $1 billion. In conducting its analysis, Lazard analyzed the premiums paid for recent transactions over $1 billion and those over $5 billion, since premiums paid may vary with the size of the transaction.

The analysis was based on the one day, one week and four week implied premiums for the transactions examined. The implied premiums were calculated by comparing the offer price for the target firm on the announcement date with the per share price of the target firm one day, one week, and four weeks prior to the announcement of the transaction. The results of these calculations are given in Table 8-5.  Based on this analysis, Lazard determined an applicable premium range of 20% to 30% for SunGard and applied this range to SunGard's share price of $24.95 on March 18, 2005. Using this information, Lazard calculated an implied price per share range for SunGard common stock of $29.94 .

Summary and Conclusions

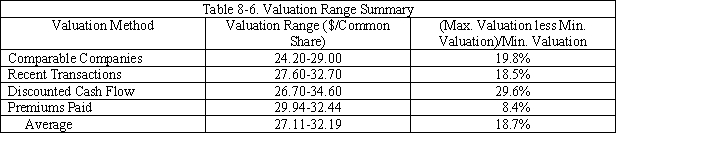

Table 8-6 summarizes the estimated valuation ranges based on the alternative valuation methods employed by Lazard Freres. Note that the $36 per offer price compares favorably to the estimated average valuation range, representing a premium of 12% . Consequently, Lazard Freres viewed the investor group's offer price for SunGard as fair.

Based on this analysis, Lazard determined an applicable premium range of 20% to 30% for SunGard and applied this range to SunGard's share price of $24.95 on March 18, 2005. Using this information, Lazard calculated an implied price per share range for SunGard common stock of $29.94 .

Summary and Conclusions

Table 8-6 summarizes the estimated valuation ranges based on the alternative valuation methods employed by Lazard Freres. Note that the $36 per offer price compares favorably to the estimated average valuation range, representing a premium of 12% . Consequently, Lazard Freres viewed the investor group's offer price for SunGard as fair.  -Why do you believe that the percentage difference between the maximum and minimum valuation estimates varies so much from one valuation method to another? See Table 8-7.

-Why do you believe that the percentage difference between the maximum and minimum valuation estimates varies so much from one valuation method to another? See Table 8-7.

(Essay)

4.9/5 (35)

The comparable companies' method and recent transactions methods of valuation are conceptually similar.

(True/False)

4.8/5 (34)

Book values are maligned as measures of value,because they represent historical rather than current market values.

(True/False)

4.7/5 (37)

In constructing the enterprise value,the market value of the firm's common equity value is added to the market value of the firm's long-term debt and the market value of preferred stock.

(True/False)

4.8/5 (43)

Case Study Short Essay Examination Questions

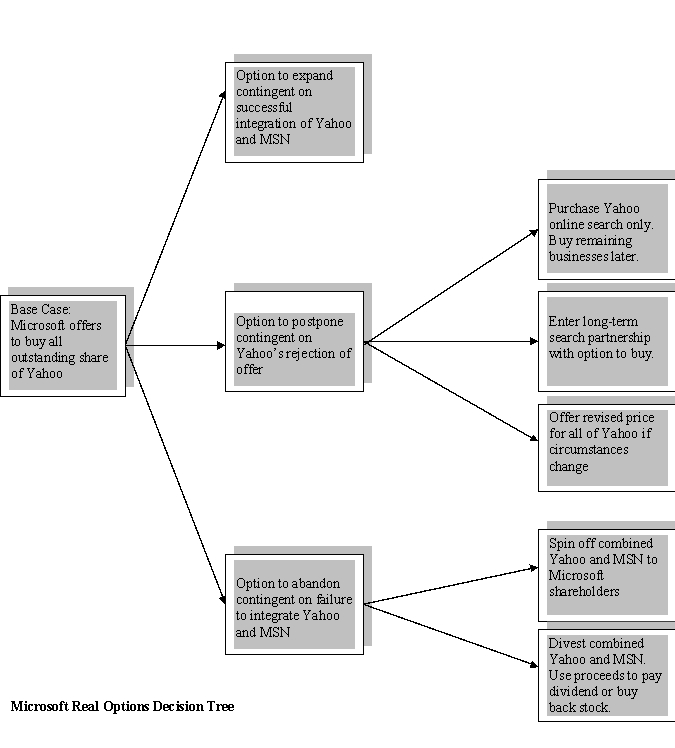

A Real Options' Perspective on Microsoft's Dealings with Yahoo

In a bold move to transform two relatively weak online search businesses into a competitor capable of challenging market leader Google, Microsoft proposed to buy Yahoo for $44.6 billion on February 2, 2008. At $31 per share in cash and stock, the offer represented a 62 percent premium over Yahoo's prior day closing price. Despite boosting its bid to $33 per share to offset a decline in the value of Microsoft's share price following the initial offer, Microsoft was rebuffed by Yahoo's board and management. In early May, Microsoft withdrew its bid to buy the entire firm and substituted an offer to acquire the search business only. Incensed at Yahoo's refusal to accept the Microsoft bid, activist shareholder Carl Icahn initiated an unsuccessful proxy fight to replace the Yahoo board. Throughout this entire melodrama, critics continued to ask how Microsoft could justify an offer valued at $44.6 billion when the market prior to the announcement had valued Yahoo at only $27.5 billion.

Microsoft could have continued to slug it out with Yahoo and Google, as it has been for the last five years, but this would have given Google more time to consolidate its leadership position. Despite having spent billions of dollars on Microsoft's online service (Microsoft Network or MSN) in recent years, the business remains a money loser (with losses exceeding one half billion dollars in 2007). Furthermore, MSN accounted for only 5 percent of the firm's total revenue at that time.

Microsoft argued that its share of the online Internet search (i.e., ads appearing with search results) and display (i.e., website banner ads) advertising markets would be dramatically increased by combining Yahoo with MSN. Yahoo also is the leading consumer email service. Anticipated cost savings from combining the two businesses were expected to reach $1 billion annually. Longer term, Microsoft expected to bundle search and advertising capabilities into the Windows operating system to increase the usage of the combined firms' online services by offering compatible new products and enhanced search capabilities.

The two firms have very different cultures. The iconic Silicon Valley-based Yahoo often is characterized as a company with a free-wheeling, fun-loving culture, potentially incompatible with Microsoft's more structured and disciplined environment. Melding or eliminating overlapping businesses represents a potentially mind-numbing effort given the diversity and complexity of the numerous sites available. To achieve the projected cost savings, Microsoft would have to choose which of the businesses and technologies would survive. Moreover, the software driving all of these sites and services is largely incompatible.

As an independent or stand-alone business, the market valued Yahoo at approximately $17 billion less than Microsoft's valuation. Microsoft was valuing Yahoo based on its intrinsic stand-alone value plus perceived synergy resulting from combining Yahoo and MSN. Standard discounted cash flow analysis assumes implicitly that, once Microsoft makes an investment decision, it cannot change its mind. In reality, once an investment decision is made, management often has a number of opportunities to make future decisions based on the outcome of things that are currently uncertain. These opportunities, or real options, include the decision to expand (i.e., accelerate investment at a later date), delay the initial investment, or abandon an investment. With respect to Microsoft's effort to acquire Yahoo, the major uncertainties dealt with the actual timing of an acquisition and whether the two businesses could be integrated successfully. For Microsoft's attempted takeover of Yahoo, such options included the following:

Base case. Buy 100 percent of Yahoo immediately.

Option to expand. If Yahoo were to accept the bid, accelerate investment in new products and services contingent on the successful integration of Yahoo and MSN.

Option to delay. (1) Temporarily walk away keeping open the possibility of returning for 100 percent of Yahoo if circumstances change, (2) offer to buy only the search business with the intent of purchasing the remainder of Yahoo at a later date, or (3) enter into a search partnership, with an option to buy at a later date.

Option to abandon. If Yahoo were to accept the bid, spin off or divest combined Yahoo/MSN if integration is unsuccessful.

The decision tree in the following exhibit illustrates the range of real options (albeit an incomplete list) available to the Microsoft board at that time. Each branch of the tree represents a specific option. The decision-tree framework is helpful in depicting the significant flexibility senior management often has in changing an existing investment decision at some point in the future.

With neither party making headway against Google, Microsoft again approached Yahoo in mid-2009, which resulted in an announcement in early 2010 of an internet search agreement between the two firms. Yahoo transferred control of its internet search technology to Microsoft in an attempt to boost its sagging profits. Microsoft is relying on a 10-year arrangement with Yahoo to help counter the dominance of Google in the internet search market. Both firms hope to be able to attract more advertising dollars paid by firms willing to pay for links on the firms' sites.  Case Study Short Essay Examination Questions

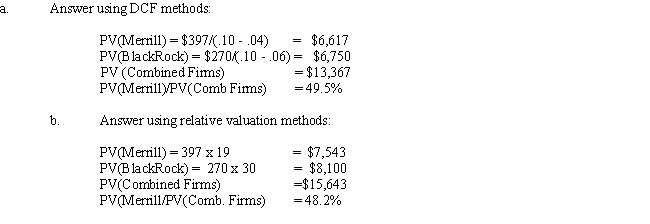

Merrill Lynch and BlackRock Agree to Swap Assets

During the 1990s, many financial services companies began offering mutual funds to their current customers who were pouring money into the then booming stock market. Hoping to become financial supermarkets offering an array of financial services to their customers, these firms offered mutual funds under their own brand name. The proliferation of mutual funds made it more difficult to be noticed by potential customers and required the firms to boost substantially advertising expenditures at a time when increased competition was reducing mutual fund management fees. In addition, potential customers were concerned that brokers would promote their own firm's mutual funds to boost profits.

This trend reversed in recent years, as banks, brokerage houses, and insurance companies are exiting the mutual fund management business. Merrill Lynch agreed on February 15, 2006, to swap its mutual funds business for an approximate 49 percent stake in money-manager BlackRock Inc. The mutual fund or retail accounts represented a new customer group for BlackRock, founded in 1987, which had previously managed primarily institutional accounts.

At $453 billion in 2005, BlackRock's assets under management had grown four times faster than Merrill's $544 billion mutual fund assets. During 2005, BlackRock's net income increased to $270 million, or 63 percent over the prior year, as compared to Merrill's 27 percent growth in net income in its mutual fund business to $397 million. BlackRock and Merrill stock traded at 30 and 19 times estimated 2006 earnings, respectively.

Merrill assets and net income represented 55 percent and 60 percent of the combined BlackRock and Merrill assets and net income, respectively. Under the terms of the transaction, BlackRock would issue 65 million new common shares to Merrill. Based on BlackRock's February 14, 2005, closing price, the deal is valued at $9.8 billion. The common stock gave Merrill 49 percent of the outstanding BlackRock voting stock. PNC Financial and employees and public shareholders owned 34 percent and 17 percent, respectively. Merrill's ability to influence board decisions is limited, since it has only 2 of 17 seats on the BlackRock board of directors. Certain "significant matters" require a 70 percent vote of all board members and 100 percent of the nine independent members, which include the two Merrill representatives. Merrill (along with PNC) must also vote its shares as recommended by the BlackRock board.

-Merrill owns less than half of the combined firms,although it contributed more than one- half of the combined firms' assets and net income.Discuss how you might use DCF and relative valuation methods to determine Merrill's proportionate ownership in the combined firms.

Case Study Short Essay Examination Questions

Merrill Lynch and BlackRock Agree to Swap Assets

During the 1990s, many financial services companies began offering mutual funds to their current customers who were pouring money into the then booming stock market. Hoping to become financial supermarkets offering an array of financial services to their customers, these firms offered mutual funds under their own brand name. The proliferation of mutual funds made it more difficult to be noticed by potential customers and required the firms to boost substantially advertising expenditures at a time when increased competition was reducing mutual fund management fees. In addition, potential customers were concerned that brokers would promote their own firm's mutual funds to boost profits.

This trend reversed in recent years, as banks, brokerage houses, and insurance companies are exiting the mutual fund management business. Merrill Lynch agreed on February 15, 2006, to swap its mutual funds business for an approximate 49 percent stake in money-manager BlackRock Inc. The mutual fund or retail accounts represented a new customer group for BlackRock, founded in 1987, which had previously managed primarily institutional accounts.

At $453 billion in 2005, BlackRock's assets under management had grown four times faster than Merrill's $544 billion mutual fund assets. During 2005, BlackRock's net income increased to $270 million, or 63 percent over the prior year, as compared to Merrill's 27 percent growth in net income in its mutual fund business to $397 million. BlackRock and Merrill stock traded at 30 and 19 times estimated 2006 earnings, respectively.

Merrill assets and net income represented 55 percent and 60 percent of the combined BlackRock and Merrill assets and net income, respectively. Under the terms of the transaction, BlackRock would issue 65 million new common shares to Merrill. Based on BlackRock's February 14, 2005, closing price, the deal is valued at $9.8 billion. The common stock gave Merrill 49 percent of the outstanding BlackRock voting stock. PNC Financial and employees and public shareholders owned 34 percent and 17 percent, respectively. Merrill's ability to influence board decisions is limited, since it has only 2 of 17 seats on the BlackRock board of directors. Certain "significant matters" require a 70 percent vote of all board members and 100 percent of the nine independent members, which include the two Merrill representatives. Merrill (along with PNC) must also vote its shares as recommended by the BlackRock board.

-Merrill owns less than half of the combined firms,although it contributed more than one- half of the combined firms' assets and net income.Discuss how you might use DCF and relative valuation methods to determine Merrill's proportionate ownership in the combined firms.

(Essay)

4.9/5 (32)

The replacement cost approach to valuation estimates what it would cost to replace the target firm's assets at current market prices using professional appraisers less the present value of the firm's liabilities.

(True/False)

4.8/5 (35)

Studies show that rival firms' share prices will rise in response to the announced acquisition of a competitor,regardless of whether the proposed acquisition is ultimately successful or unsuccessful.

(True/False)

4.8/5 (42)

Which of the following represent limitations of real options?

(Multiple Choice)

4.8/5 (32)

What is the appropriate cost of equity for discounting future cash flows? Should it be Google's or YouTube's? Explain your

answer.

(Essay)

4.7/5 (35)

An option is the exclusive right,but not the obligation,to buy,sell,or use property for a specific period of time in exchange for a predetermined amount of money.

(True/False)

4.8/5 (32)

Real options include the right to buy land,commercial property,and equipment.Such assets can be valued as call options if its current value exceeds the difference between the asset's current value and some predetermined level.

(True/False)

4.8/5 (34)

Which of the following is not true about the liquidation/break-up valuation methods?

(Multiple Choice)

4.7/5 (40)

Liquidation or breakup value is the projected price of the firm's assets sold separately in liquidating or breaking up the firm.

(True/False)

4.9/5 (27)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)