Exam 17: Alternative Exit and Restructuring Strategies: Bankruptcy Reorganization and Liquidation

Exam 1: Introduction to Mergers, acquisitions, and Other Restructuring Activities108 Questions

Exam 2: The Regulatory Environment103 Questions

Exam 3: The Corporate Takeover Market: Common Takeover Tactics, anti-Takeover Defenses, and Corporate Governance126 Questions

Exam 4: Planning,developing Business,and Acquisition Plans: Phases 1 and 2 of the Acquisition Process109 Questions

Exam 5: Implementation: Search Through Closing: Phases 3 to 10 of the Acquisition Process106 Questions

Exam 6: Postclosing Integration: Mergers, acquisitions, and Business Alliances103 Questions

Exam 7: Merger and Acquisition Cash Flow Valuation Basics81 Questions

Exam 8: Relative,asset-Oriented,and Real Option Valuation Basics84 Questions

Exam 9: Applying Financial Models to Value, structure, and Negotiate Mergers and Acquisitions92 Questions

Exam 10: Analysis and Valuation of Privately Held Companies97 Questions

Exam 11: Structuring the Deal: Payment and Legal Considerations112 Questions

Exam 12: Structuring the Deal: Tax and Accounting Considerations97 Questions

Exam 13: Financing the Deal: Private Equity, hedge Funds, and Other Sources of Funds121 Questions

Exam 14: Highly Leveraged Transactions: Lbo Valuation and Modeling Basics98 Questions

Exam 15: Business Alliances: Joint Ventures, partnerships, strategic Alliances, and Licensing113 Questions

Exam 16: Alternative Exit and Restructuring Strategies: Divestitures, spin-Offs, carve-Outs, split-Ups, and Split-Offs119 Questions

Exam 17: Alternative Exit and Restructuring Strategies: Bankruptcy Reorganization and Liquidation80 Questions

Exam 18: Cross-Border Mergers and Acquisitions: Analysis and Valuation89 Questions

Select questions type

The debtor firm often initiates the voluntary settlement process,because it generally offers the best chance for the current owners to recover a portion of their investments either by continuing to operate the firm or through a planned liquidation of the firm.

(True/False)

4.8/5  (36)

(36)

A composition is an agreement in which creditors agree to settle for less than the full amount they are owed.

(True/False)

4.9/5 (40)

In the absence of a voluntary settlement out of court,the debtor firm may seek protection from its creditors by initiating bankruptcy.However,creditors cannot force the debtor firm into bankruptcy.

.

(True/False)

4.9/5 (34)

The leading causes of business failure include which of the following:

(Multiple Choice)

4.7/5 (36)

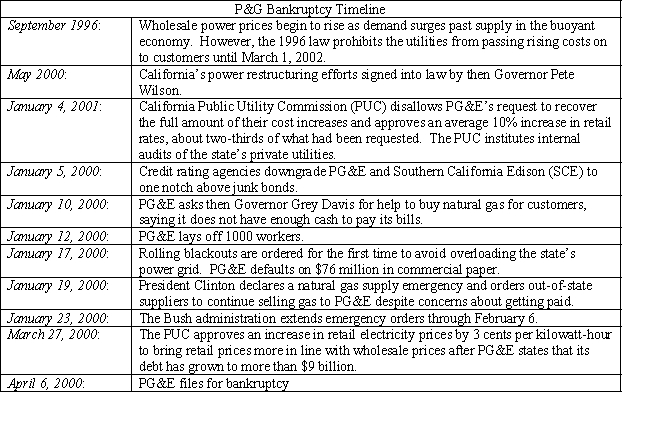

PG&E SEEKS BANKRUPTCY PROTECTION

Pacific, Gas, and Electric (PG&E), the San Francisco-based utility, filed for bankruptcy on April 7, 2001, citing nearly $9 billion in debt and un-reimbursed energy costs. The utility, one of three privately owned utilities in California, serves northern and central California. The intention of the Chapter 11 reorganization was to make the utility solvent again by protecting the firm from lawsuits or any other action by those who are owed money by the utility. The bankruptcy will also allow the utility to deal with all of the firm's debts in a single forum rather than with individual debtors in what had become a highly politicized venue. The following time line outlines the firm's road to bankruptcy.  .

Utility industry analysts saw PG&E's move as largely an effort to escape the political paralysis that had befallen the state's regulatory apparatus. The bankruptcy filing came one day after Governor Davis dropped his opposition to raising retail rates. However, the Governor's reversal came after five month's of negotiations with the state's privately owned utilities on a rescue plan.

PG&E's common shares fell 37 percent on the day the firm filed for reorganization. Fearing a similar fate for San Diego Gas and Electric, the shares of Sempra Energy, SDG&E's parent corporation, also dropped by 35 percent

In an attempt to insulate California ratepayers from escalating wholesale electricity prices, the state entered into a series of 5-to-10 year contracts with electricity power generators that account for more than two-thirds of the state's projected power needs. The last contracts were signed by the state in June 2001. By September, a slowing economy pushed the wholesale price of electricity well below the level the state was required to pay in the "take or pay" contracts the state had just signed. Estimates suggest that California taxpayers will have to pay between $40 and $45 billion in power costs over the next decade depending on what happens to future energy costs. PG&E has continued to supply its customers without disruption or blackout while being under the protection of the bankruptcy court.

Southern California Edison, nearing bankruptcy for reasons similar to those that drove PG&E to seek protection from its creditors, reached agreement with the Public Utility Commission to pay off $3.3 billion in debt owed to power generators from customer revenues. Previously, the PUC had forbid the utility to use monies generated from two previous rate increases for this purpose. The U.S. District Court judge approved the plan on October 5, 2001. While some creditors complained that the settlement was not reassuring because it did not include a timetable for repayment of outstanding debt, others viewed the agreement as a voluntary reorganization plan without going through the expensive process of filing for bankruptcy with the federal court.

:

-PG&E pursued bankruptcy protection,while Southern California Edison did not.What could PG&E have been done differently to avoid bankruptcy?

.

Utility industry analysts saw PG&E's move as largely an effort to escape the political paralysis that had befallen the state's regulatory apparatus. The bankruptcy filing came one day after Governor Davis dropped his opposition to raising retail rates. However, the Governor's reversal came after five month's of negotiations with the state's privately owned utilities on a rescue plan.

PG&E's common shares fell 37 percent on the day the firm filed for reorganization. Fearing a similar fate for San Diego Gas and Electric, the shares of Sempra Energy, SDG&E's parent corporation, also dropped by 35 percent

In an attempt to insulate California ratepayers from escalating wholesale electricity prices, the state entered into a series of 5-to-10 year contracts with electricity power generators that account for more than two-thirds of the state's projected power needs. The last contracts were signed by the state in June 2001. By September, a slowing economy pushed the wholesale price of electricity well below the level the state was required to pay in the "take or pay" contracts the state had just signed. Estimates suggest that California taxpayers will have to pay between $40 and $45 billion in power costs over the next decade depending on what happens to future energy costs. PG&E has continued to supply its customers without disruption or blackout while being under the protection of the bankruptcy court.

Southern California Edison, nearing bankruptcy for reasons similar to those that drove PG&E to seek protection from its creditors, reached agreement with the Public Utility Commission to pay off $3.3 billion in debt owed to power generators from customer revenues. Previously, the PUC had forbid the utility to use monies generated from two previous rate increases for this purpose. The U.S. District Court judge approved the plan on October 5, 2001. While some creditors complained that the settlement was not reassuring because it did not include a timetable for repayment of outstanding debt, others viewed the agreement as a voluntary reorganization plan without going through the expensive process of filing for bankruptcy with the federal court.

:

-PG&E pursued bankruptcy protection,while Southern California Edison did not.What could PG&E have been done differently to avoid bankruptcy?

(Essay)

4.8/5 (39)

A workout is an arrangement conducted inside of bankruptcy court by a debtor and its creditors for payment or re-scheduling of payment of the debtor's obligations.

(True/False)

4.8/5 (32)

By law,corporate liquidation can only be conducted outside of the U.S.bankruptcy court.

(True/False)

4.9/5 (39)

Prepackaged bankruptcies are less common today than in years past.

(True/False)

4.8/5 (31)

Financially distressed firms also affect communities in which they are located in terms of increasing unemployment and eroding the tax base.

(True/False)

4.8/5 (39)

To determine which strategy to pursue,the failing firm's management needs to estimate which of the following:

(Multiple Choice)

4.7/5 (38)

Debt restructuring of a bankrupt firm is usually accomplished in which of the following ways:

(Multiple Choice)

4.9/5 (30)

A debt-for-equity swap occurs when creditors surrender a portion of their claims on the firm in exchange for an ownership position in the firm.

(True/False)

4.8/5 (37)

Moody's credit rating agency defines instances of default as which of the following:

(Multiple Choice)

4.9/5 (35)

As part of a Chapter 15 proceeding,the U.S.bankruptcy court may authorize a trustee to act in a foreign country on behalf of the U.S.Bankruptcy Court.

(True/False)

4.7/5 (35)

Chapter 11 reorganization often enables creditors to recover relatively more of their claims than under liquidation.

(True/False)

4.7/5 (36)

All of the following represent different forms of debt restructuring except for

(Multiple Choice)

4.8/5 (36)

Increasingly,distressed companies are choosing to restructure inside of bankruptcy court,rather than reaching a general agreement with creditors before seeking Chapter 11 protection.

(True/False)

4.9/5 (36)

Empirical studies show that company size (measured by assets),case duration (measured in days),and the number of parties involved in the proceedings (measured in terms of the numbers of professional firms working)explain most of the case-to-case variation in professional fees.

(True/False)

4.8/5 (40)

If a creditor is owed a large amount of money,it could become a major or even the controlling shareholder in the reorganized firm.

(True/False)

4.8/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)