Exam 19: Valuation and Financial Modeling: a Case Study

Exam 1: The Corporation38 Questions

Exam 2: Introduction to Financial Statement Analysis103 Questions

Exam 3: Financial Decision Making and the Law of One Price89 Questions

Exam 4: The Time Value of Money91 Questions

Exam 5: Interest Rates68 Questions

Exam 6: Valuing Bonds115 Questions

Exam 7: Investment Decision Rules86 Questions

Exam 8: Fundamentals of Capital Budgeting95 Questions

Exam 9: Valuing Stocks96 Questions

Exam 10: Capital Markets and the Pricing of Risk103 Questions

Exam 11: Optimal Portfolio Choice and the Capital Asset Pricing Model134 Questions

Exam 12: Estimating the Cost of Capital104 Questions

Exam 13: Investor Behavior and Capital Market Efficiency77 Questions

Exam 14: Capital Structure in a Perfect Market99 Questions

Exam 15: Debt and Taxes95 Questions

Exam 16: Financial Distress,managerial Incentives,and Information111 Questions

Exam 17: Payout Policy96 Questions

Exam 18: Capital Budgeting and Valuation With Leverage99 Questions

Exam 19: Valuation and Financial Modeling: a Case Study49 Questions

Exam 20: Financial Options57 Questions

Exam 21: Option Valuation43 Questions

Exam 22: Real Options64 Questions

Exam 23: Raising Equity Capital52 Questions

Exam 24: Debt Financing54 Questions

Exam 25: Leasing46 Questions

Exam 26: Working Capital Management48 Questions

Exam 27: Short-Term Financial Planning47 Questions

Exam 28: Mergers and Acquisitions59 Questions

Exam 29: Corporate Governance46 Questions

Exam 30: Risk Management53 Questions

Exam 31: International Corporate Finance45 Questions

Select questions type

Use the table for the question(s)below.

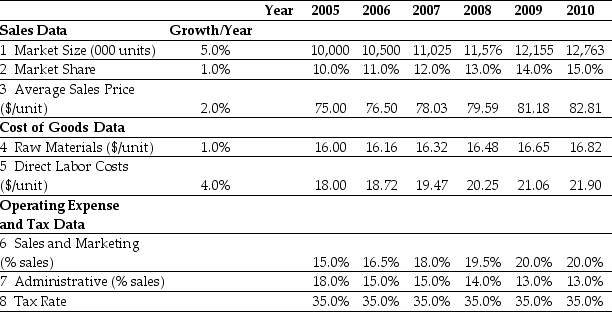

Ideko Sales and Operating Cost Assumptions  -Based upon Ideko's Sales and Operating Cost Assumptions,what production capacity will Ideko require in 2007?

-Based upon Ideko's Sales and Operating Cost Assumptions,what production capacity will Ideko require in 2007?

Free

(Multiple Choice)

4.9/5  (30)

(30)

Correct Answer: Verified

Verified

B

What is the purpose of the sensitivity analysis?

Free

(Essay)

4.8/5 (39)

Correct Answer:Verified

Any financial valuation is only as accurate as the estimates on which it is based.Before concluding our analysis,it is important to assess the uncertainty of our estimates and to determine their potential impact on the value of the deal.Once we have developed the spreadsheet model,it is straightforward to perform a sensitivity analysis to determine the impact of changes in different parameters on the deal's value.

Assuming that Ideko has a EBITDA multiple of 8.5,then the continuation unlevered P/E ratio of Ideko in 2010 is closest to:

Free

(Multiple Choice)

4.9/5 (46)

Correct Answer:Verified

A

Use the tables for the question(s)below.

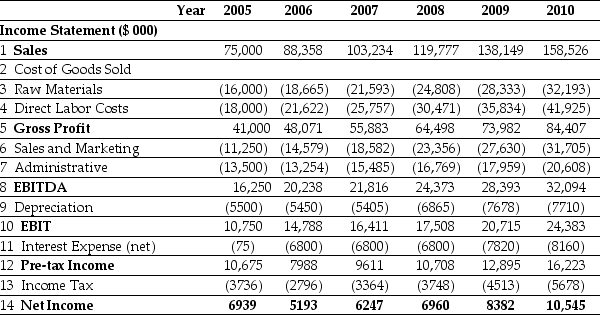

Pro Forma Income Statement for Ideko,2005-2010  Pro Forma Balance Sheet for Ideko,2005-2010

Pro Forma Balance Sheet for Ideko,2005-2010  -Assuming that Ideko has a EBITDA multiple of 8.5,then the continuation enterprise value of Ideko in 2010 is closest to:

-Assuming that Ideko has a EBITDA multiple of 8.5,then the continuation enterprise value of Ideko in 2010 is closest to:

(Multiple Choice)

4.9/5 (41)

Assuming that Ideko has a EBITDA multiple of 8.5,then the continuation equity value of Ideko in 2010 is closest to:

(Multiple Choice)

4.9/5 (37)

Based upon Ideko's Sales and Operating Cost Assumptions,what production capacity will Ideko require in 2008?

(Multiple Choice)

4.9/5 (39)

If Ideko's loans will have an interest rate of 6.8%,then the interest expense paid in 2009 is closest to:

(Multiple Choice)

4.9/5 (37)

With the proper changes it is believed that Ideko's credit policies will allow for an account receivables days of 60.The forecasted accounts receivable for Ideko in 2008 is closest to:

(Multiple Choice)

4.9/5 (44)

Use the tables for the question(s)below.

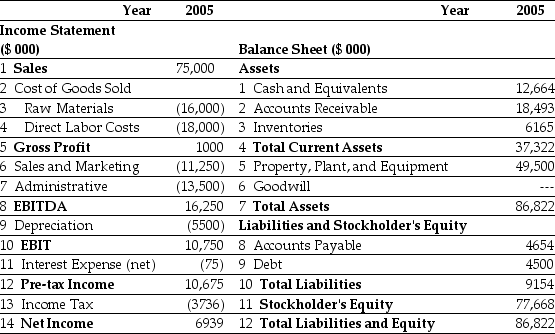

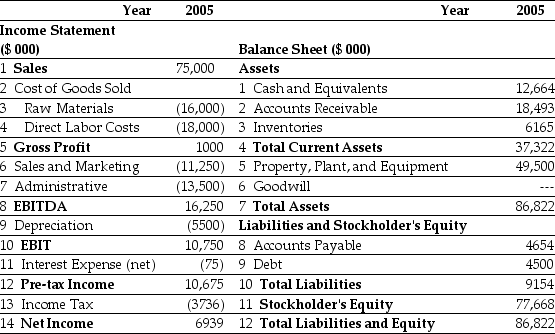

Estimated 2005 Income Statement and Balance Sheet Data for Ideko Corporation  -Ideko's Accounts Receivable Days is closest to:

-Ideko's Accounts Receivable Days is closest to:

(Multiple Choice)

4.9/5 (30)

Assuming that Ideko has a EBITDA multiple of 9.4,then the continuation unlevered P/E ratio of Ideko in 2010 is closest to:

(Multiple Choice)

4.8/5 (43)

Based upon Ideko's Sales and Operating Cost Assumptions,what production capacity will Ideko require in 2009?

(Multiple Choice)

4.9/5 (44)

Use the tables for the question(s)below.

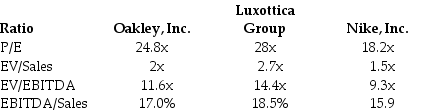

Estimated 2005 Income Statement and Balance Sheet Data for Ideko Corporation  The following are financial ratios for three comparable companies:

The following are financial ratios for three comparable companies:  -Based upon the average P/E ratio of the comparable firms,Ideko's target market value of equity is closest to:

-Based upon the average P/E ratio of the comparable firms,Ideko's target market value of equity is closest to:

(Multiple Choice)

4.8/5 (43)

Using the income statement above and the following information:

Calculate Ideko's Free Cash Flow to the Firm and Free Cash Flow to Equity in 2007.

Calculate Ideko's Free Cash Flow to the Firm and Free Cash Flow to Equity in 2007.

(Essay)

4.8/5 (40)

Using the income statement above and the following information:

Calculate Ideko's Free Cash Flow to the Firm and Free Cash Flow to Equity in 2009.

Calculate Ideko's Free Cash Flow to the Firm and Free Cash Flow to Equity in 2009.

(Essay)

4.9/5 (29)

Assuming that Ideko has a EBITDA multiple of 8.5,then the continuation EV/Sales ratio of Ideko in 2010 is closest to:

(Multiple Choice)

4.7/5 (38)

If the risk-free rate of interest is 6% and the market risk premium has historically averaged 5%,then the cost of capital for Oakley is closest to:

(Multiple Choice)

4.9/5 (33)

Based upon the average EV/EBITDA ratio of the comparable firms,if Ideko holds $6.5 million of cash in excess of its working capital needs,then Ideko's target market value of equity is closest to:

(Multiple Choice)

4.8/5 (43)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)